USD/KRW Breaks 1,510 — Should You Exchange Now? KRW -8.2% Causes · 4 Dollar Investment Methods · Fee-Saving Tips

Real-Time Issue · May 20, 2026

USD/KRW Breaks 1,510 — Should You Exchange Now? KRW -8.2% Causes · 4 Dollar Investment Methods · Fee-Saving Tips · Personalized Strategy

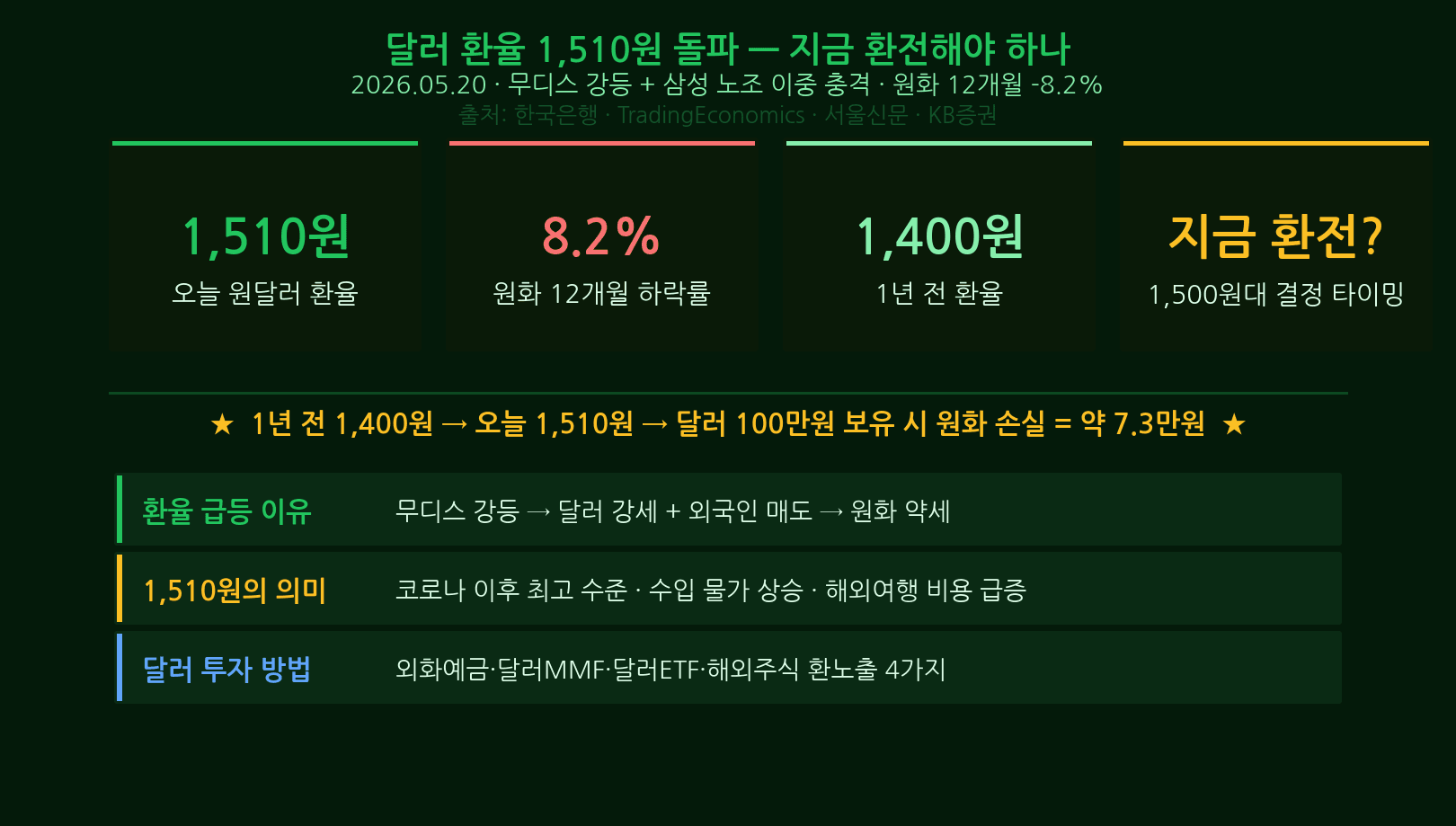

The USD/KRW exchange rate has broken through 1,510 won. — The Korean won has fallen 8.2% over the past year, and the dollar remains strong despite Moody’s US credit downgrade. Should you exchange now? We break down 4 dollar investment methods, fee-saving tips, and personalized strategies by investor type.

1. Key Facts: What Is Happening Right Now

On May 20, 2026, the USD/KRW exchange rate surged past 1,510 won intraday in the Seoul foreign exchange market. The closing rate settled at 1,508 won, approaching levels last seen during the financial stress of October 2022.

- Current USD/KRW rate: 1,510 won breached (intraday, May 20, 2026)

- Annual KRW depreciation: -8.2% over 12 months (May 2025: 1,395 won → May 2026: 1,510 won)

- Moody’s US downgrade: Aaa → Aa1 (Nov 2025) — paradoxically followed by dollar strength

- Bank of Korea intervention threshold: Market expects action around 1,520 won

- Timing debate: Further upside vs. pullback — expert opinions divided

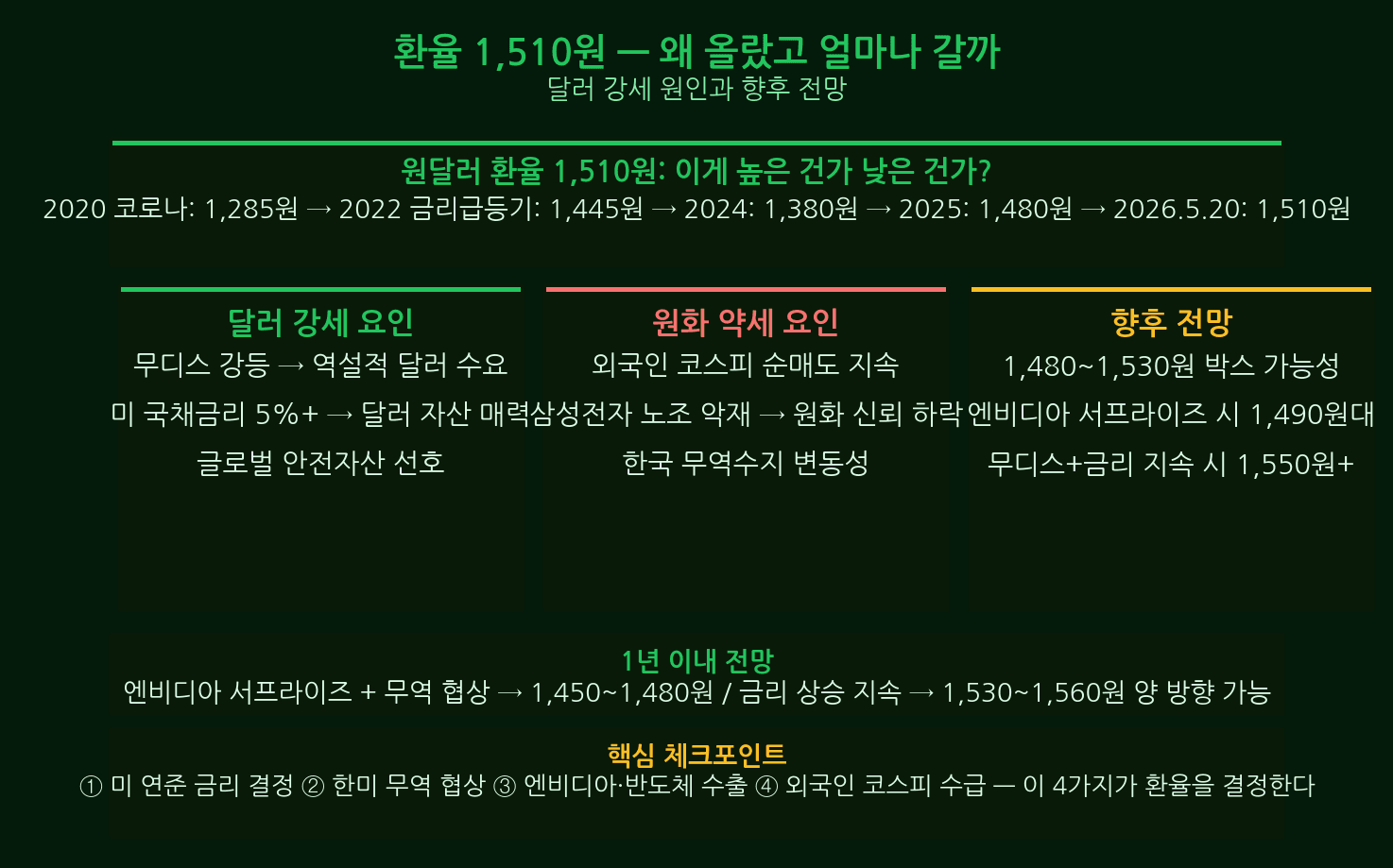

2. Why 1,510? — 4 Structural Drivers of the Surge

① US-Korea Rate Gap: Fed Holds, BoK Cuts

The US Federal Reserve holds its benchmark rate at 4.5% as of May 2026. The Bank of Korea, facing recession concerns, has cut to 2.75%. The resulting 1.75 percentage-point spread continuously draws capital away from Korean won assets toward dollar-denominated ones.

② Dollar Strength Despite Moody’s Downgrade — The Paradox Explained

When Moody’s stripped the US of its Aaa rating in November 2025, conventional logic suggested dollar weakness. The opposite happened. In times of global uncertainty, investors still flee to US Treasuries as the ultimate safe haven, regardless of credit rating. The downgrade itself amplified this “flight to safety” dynamic.

③ Persistent Foreign Equity Outflows from Korea

Foreign investors sold a net 9.8 trillion won (≈ $6.5 billion) from the KOSPI between January and May 2026. Each sale requires converting won proceeds back to dollars, applying constant downward pressure on the Korean currency.

④ Middle East Geopolitical Risk — Iran Tensions Reignite

Renewed Iran-Israel tensions in early 2026 pushed crude oil above $95 per barrel. South Korea imports 100% of its crude oil, meaning higher oil prices directly erode the current account balance and weaken the won further.

3. Should You Exchange Now? — Timing Analysis

Scenario A: Further Upside — 1,530~1,550 Possible

If the rate differential holds and foreign selling continues, analysts see room for 1,530–1,550 won. An escalation in Middle East tensions or a stronger-than-expected US jobs report could add fuel to dollar demand.

Scenario B: Pullback — Correction to 1,480s Possible

The market widely views 1,520 won as the Bank of Korea’s verbal or direct intervention line. In October 2022, the BoK deployed concentrated smoothing operations that capped the rate at 1,445 before a sharp reversal. A similar response near 1,520 is likely this time as well.

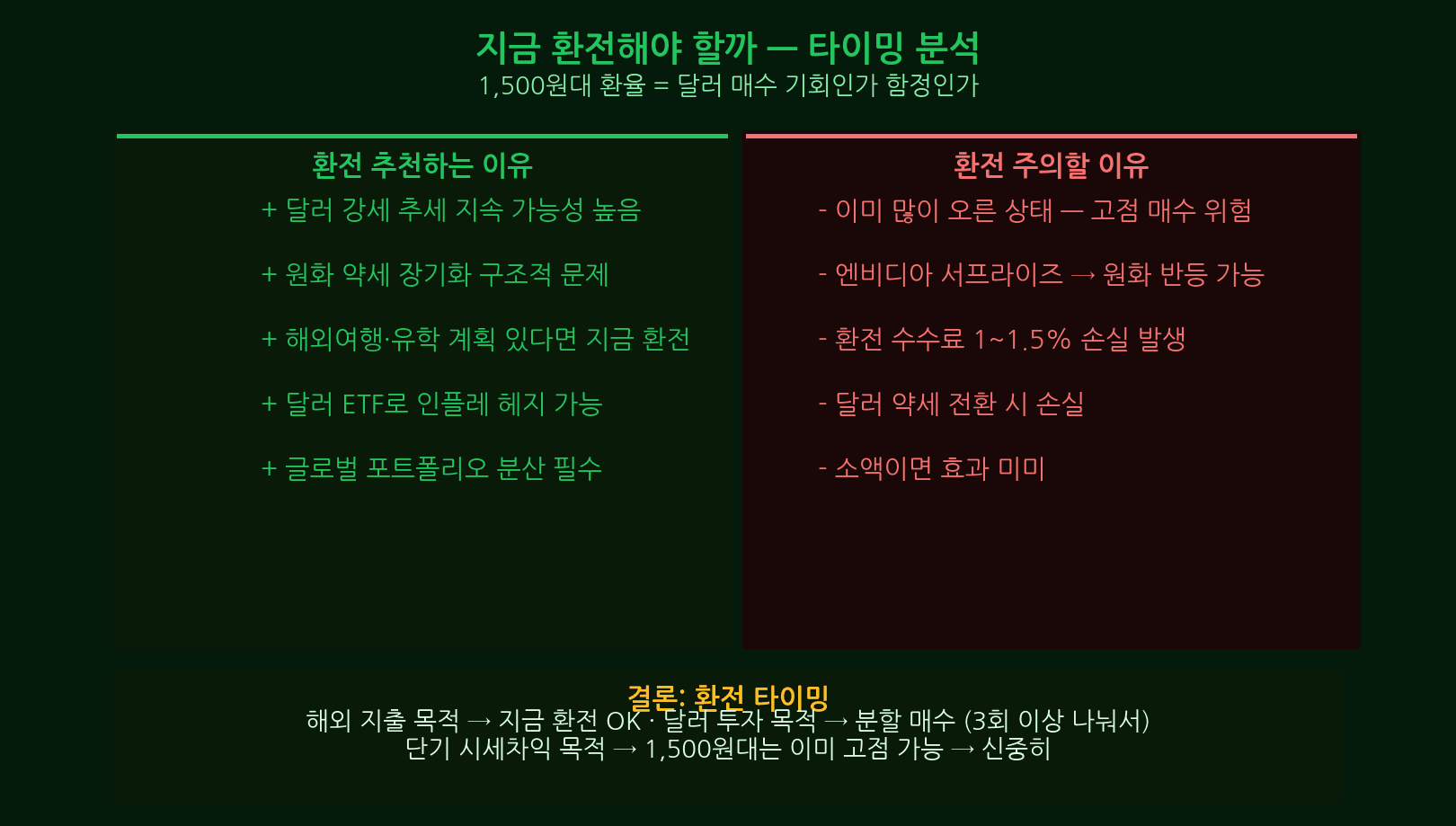

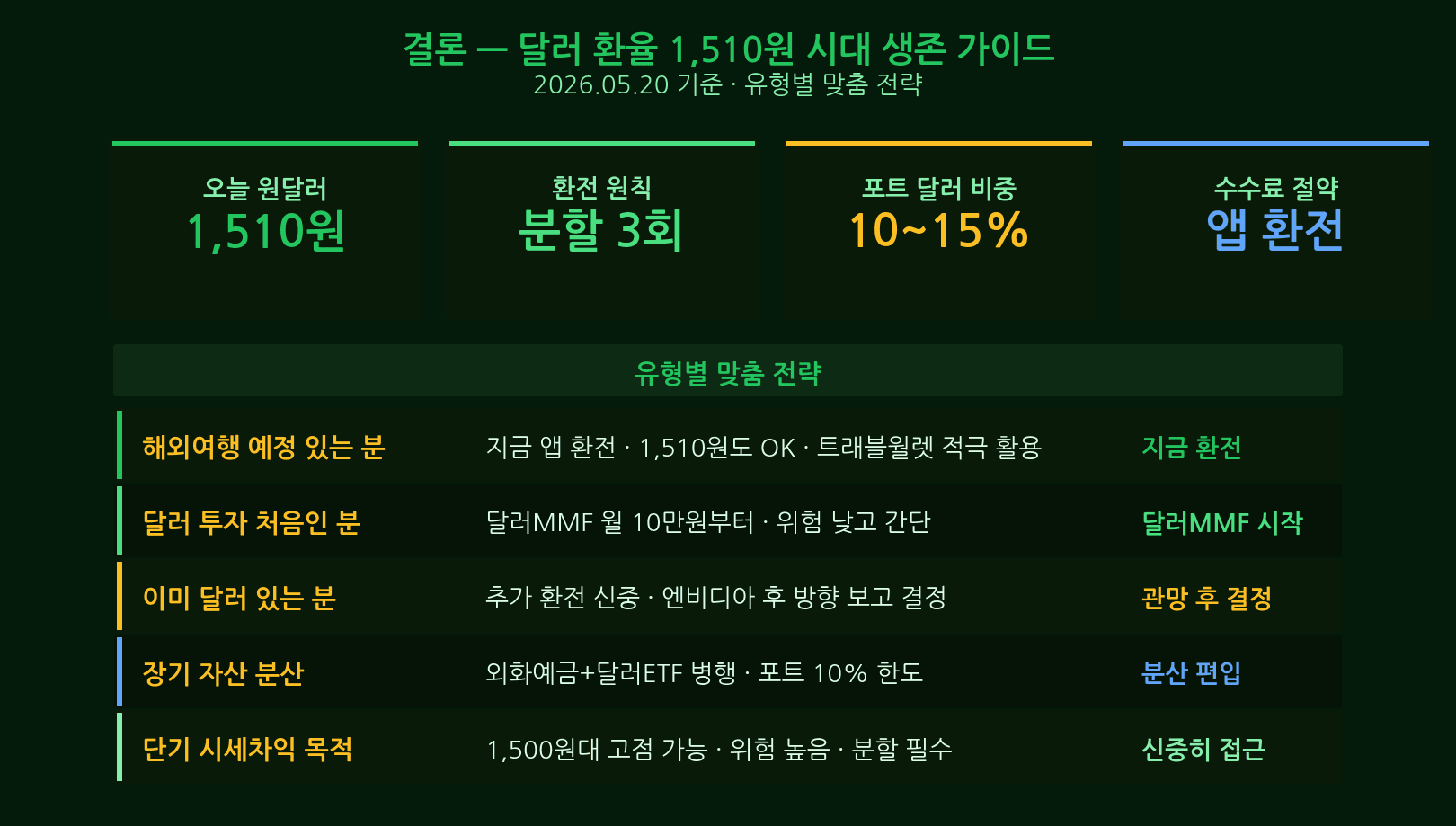

Bottom Line: Staggered Buying Is the Answer

Current levels are clearly near a historical peak, yet further upside cannot be ruled out. The consensus recommendation: split your exchange into 3 or more tranches. Example: 30% at 1,510 → 40% at 1,490 → 30% at or below 1,470 to reduce your average cost basis.

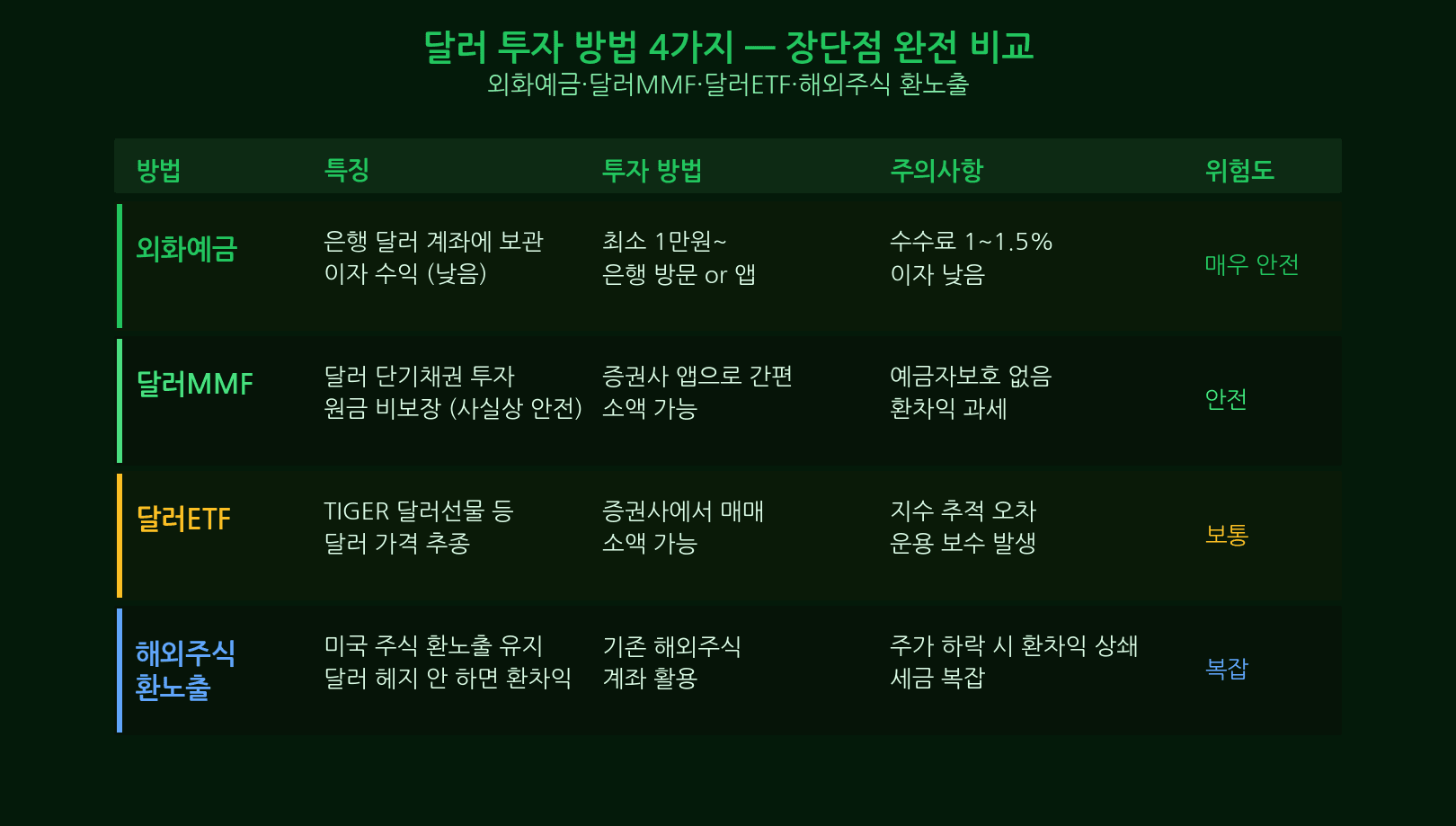

4. 4 Ways to Invest in the Dollar — Compared

① Foreign Currency Deposit — Safest, Lowest Yield

Deposit dollars directly at a Korean bank. Principal is guaranteed and exchange fee discounts of up to 90% apply via banking apps. Dollar deposit rates run at 4.2–4.5% per annum, subject to 15.4% interest income tax. Currency gains are tax-exempt. Best for capital-preservation-first investors.

② Dollar ETF — KODEX US Dollar Futures (138230)

Trade dollar exposure through a domestic brokerage account in Korean won. This ETF tracks USD/KRW nearly 1:1. Capital gains are taxed as dividend income at 15.4%. Highest liquidity — buy or sell in small amounts at any time.

③ Dollar RP / Short-Term Bond — Steady Interest + FX Gain

Invest in dollar-denominated short-term government bonds or repurchase agreements. Earn dollar interest of 4.8–5.1% annually while retaining currency upside. Available at major Korean brokerages from as little as $100.

④ Overseas Direct Investment — US Stocks/ETFs, FX + Capital Gain

Buy US equities or broad index ETFs (VOO, SPY) directly. During a dollar bull run, you capture both FX gains and price appreciation simultaneously. Note: overseas equity gains above 2.5 million won are taxed at 22% in Korea. Highest risk, highest potential return.

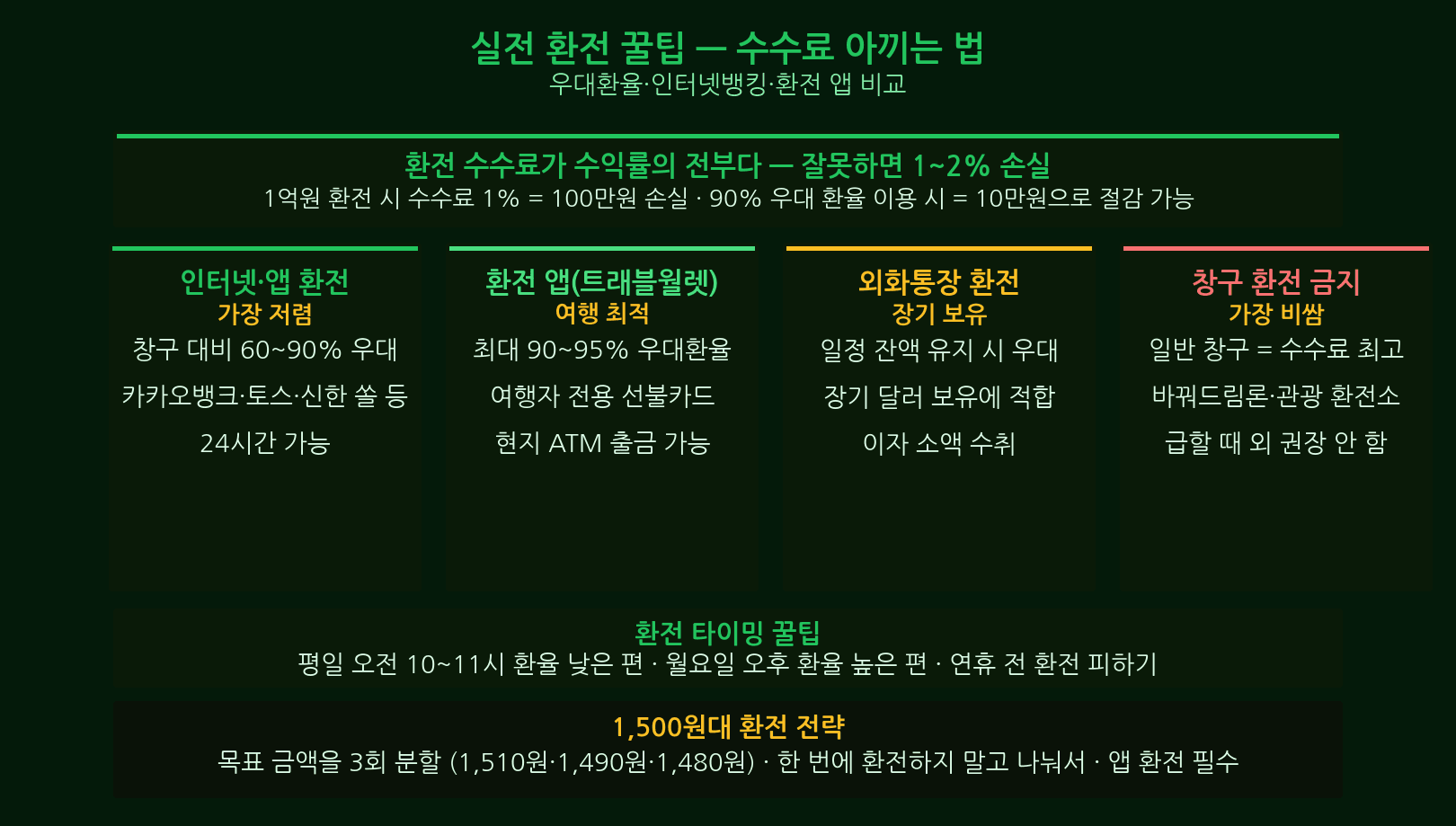

5. Fee-Saving Tips — How to Save Up to 90% on Exchange Fees

When the exchange rate is high, fee savings matter more. At 1,510 won per dollar, exchanging $1,000 costs the following depending on channel:

- Bank branch (no discount): ~1.75% spread → approximately 26,425 won in fees on $1,000

- Bank app (90% fee discount): ~0.175% spread → approximately 2,642 won — a 10× reduction

- Toss Bank foreign currency account: Zero fees — unlimited free exchange in USD, JPY, EUR

- KakaoBank foreign currency account: 100% discount on standard exchange fee — effectively free

- Airport exchange kiosk: 0–30% discount → you can lose 26,000+ won per $1,000 exchanged

Key tip: Open a Toss Bank or KakaoBank foreign currency account in advance and build your dollar position gradually in small amounts. Never exchange at the airport.

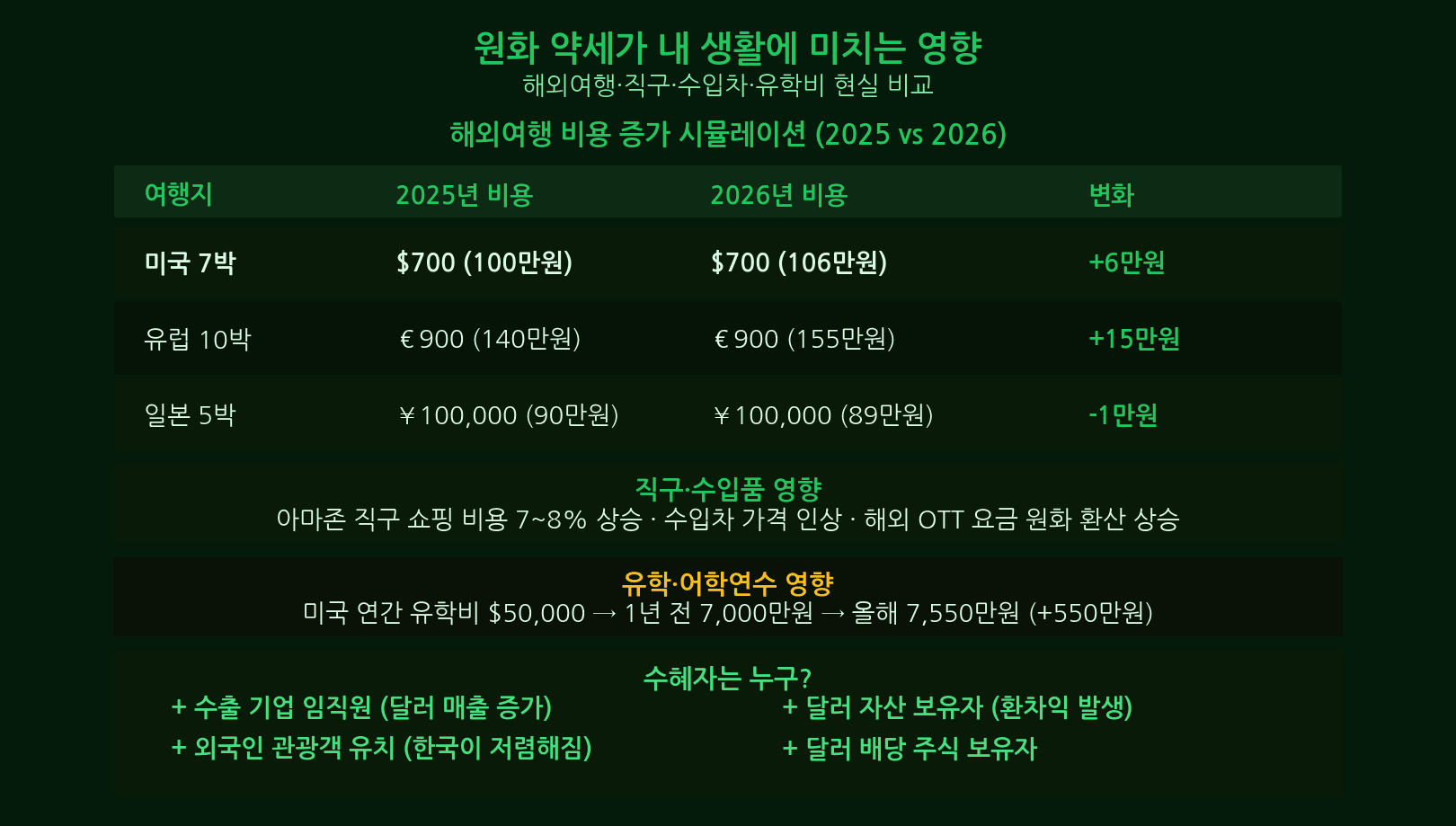

6. How a Weak Won Hits Your Daily Life

① Import Price Inflation — Food and Energy Take the Hit

South Korea imports most of its grain, crude oil, and raw materials priced in dollars. An 8.2% drop in won value means the same imports now cost 8.2% more in won terms. Rising prices for wheat, corn, and soybeans flow through to bread, snacks, and feed costs — lifting household living expenses across the board.

② International Travel Costs Jump Sharply

A traveler spending $200/day in the US paid 279,000 won a year ago (at 1,395 won). Today (at 1,510 won) that same day costs 302,000 won — 23,000 won (8.2%) more. For a two-week trip, that adds up to roughly 322,000 won in extra costs.

③ US Stock Investors — FX Gain or FX Loss?

Investors already holding US equities during a dollar rally enjoy FX gains on top of stock returns. However, buying US stocks now with freshly exchanged dollars means any future won recovery will generate FX losses. This is why choosing between currency-hedged (H) and unhedged ETF versions matters more than ever.

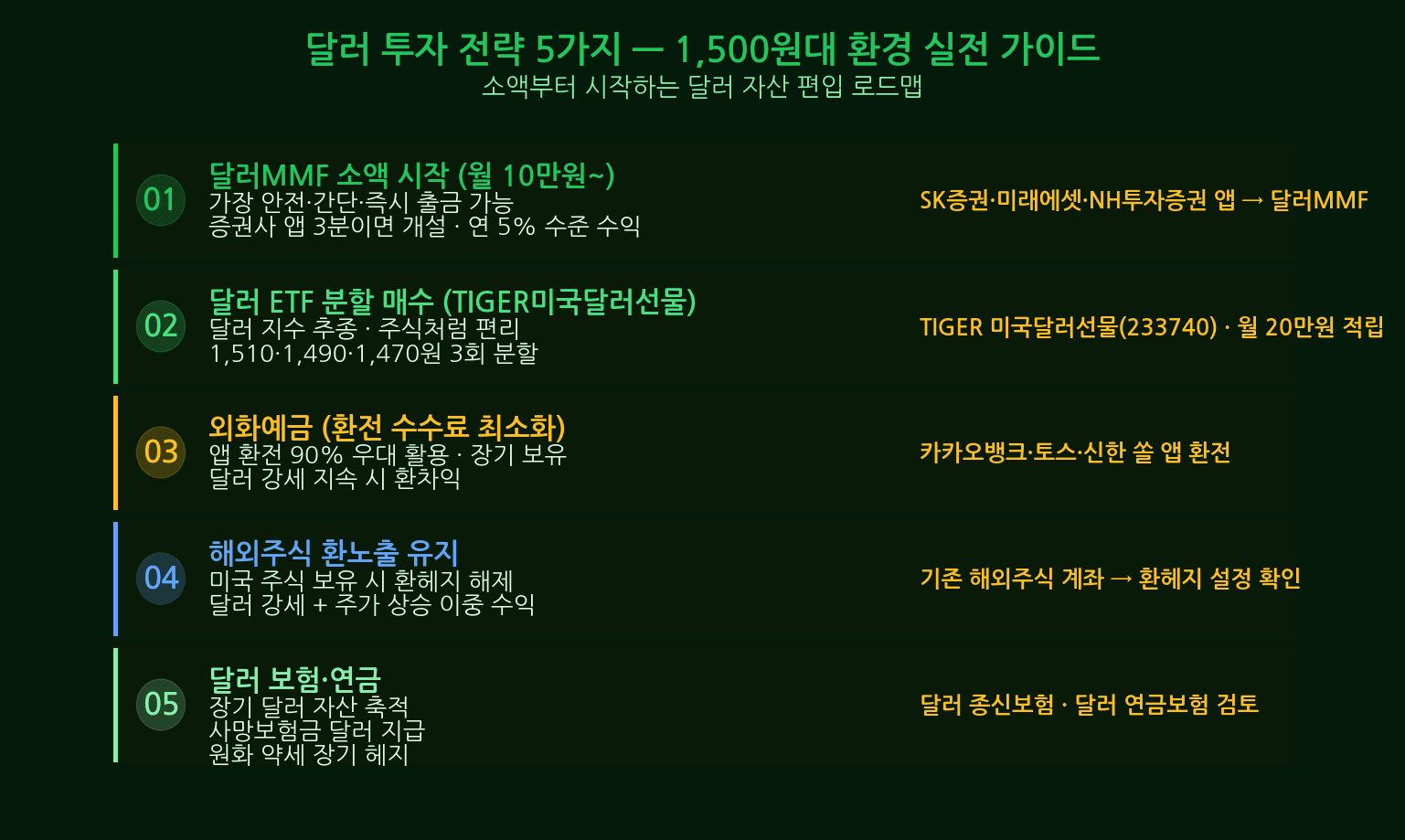

7. Five Dollar Investment Strategies for Right Now

- 3-tranche staggered buying: 30% now → 40% near 1,490 won → 30% at or below 1,470 won. Lowers your average cost and reduces timing risk.

- 30% in foreign currency deposit: Park 30% of your dollar allocation in a bank FD. Earn ~4.2% interest annually plus FX upside, with principal protection.

- 20% in dollar ETF (KODEX 138230): Maintain quick-exit liquidity. Sell rapidly if the rate spikes toward 1,530 and you want to lock in gains.

- Increase US Treasury ETF weighting: Products like ACE US 30Y Treasury Active (H) offer stable dollar yields of ~4.8% with lower volatility than equities.

- Remove currency hedges: If holding hedged (H) ETFs, switch to unhedged versions to capture direct USD/KRW appreciation without drag from the hedge cost.

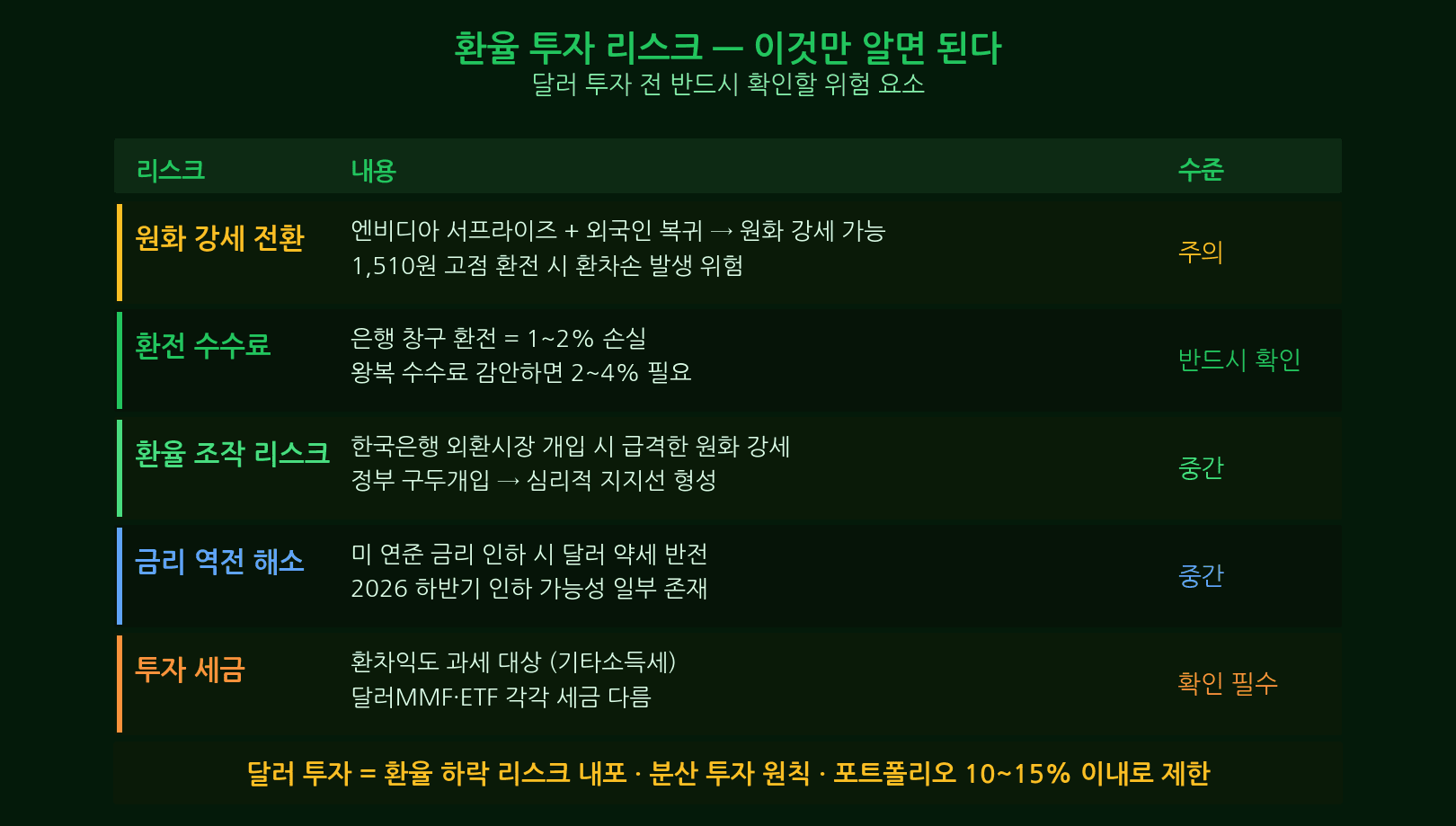

8. Risks — Dollar Strength Is Not Guaranteed to Last

Risk ① Sharp Dollar Reversal — FX Loss Exposure

Buying all-in at 1,510 and watching the rate fall to the 1,400s means an FX loss of 7%+. There is precedent: after the October 2022 peak at 1,445, USD/KRW fell back to the 1,220s within six months. Staggered buying is not optional — it is essential.

Risk ② US-Korea Currency Swap Reactivation

If a new US-Korea currency swap line is established, a sudden injection of dollar liquidity could flip won sentiment sharply. Following the March 2020 swap agreement, USD/KRW dropped from 1,285 to the 1,100s in roughly one month — a swift and painful reversal for late dollar buyers.

Risk ③ US Fiscal Crisis Deepens — Paradoxical Dollar Weakness

If structural US fiscal deterioration accelerates post-downgrade, dollar hegemony could face longer-term erosion. A scenario where the dollar index (DXY) falls below 95 would materially hurt dollar-asset returns. Long-term investors must weigh this tail risk, even if near-term momentum favors dollar strength.

9. Conclusion — Personalized Strategy by Investor Type

The same exchange rate of 1,510 won calls for different responses depending on your situation. Find your type below.

- Salaried worker (no existing dollar assets): Accumulate 5–10% of monthly income via a Toss Bank foreign currency account. Zero fees + built-in savings discipline. Target dollar allocation: 10–15% of liquid assets.

- Self-employed (importing raw materials): Pre-purchase 3–6 months of projected dollar needs via foreign currency deposit now. Hedge against future exchange rate spikes before they hurt your margins.

- Overseas traveler (departing within 1–3 months): Open a KakaoBank foreign currency account, exchange 30% today and the remaining 70% two weeks before departure. Absolutely avoid airport kiosks.

- US stock investor (existing holdings): Reduce exposure to currency-hedged ETFs; shift to unhedged versions. For new purchases, convert to dollars in tranches before investing. Consider adding to positions when USD/KRW pulls back below 1,480.

Bottom line: USD/KRW at 1,510 is near a historical peak, but structural dollar strength may persist. Do not deploy a lump sum. Stagger across at least 3 tranches, minimize fees via Toss Bank or KakaoBank, and size your dollar allocation to a level you can hold through potential volatility.

Tags: USD KRW exchange rate, dollar won, KRW depreciation, dollar investment Korea, foreign currency deposit, dollar ETF Korea, exchange fee savings, Toss Bank, KakaoBank, Moody’s downgrade