Macro Calendar D-30 — June 17 FOMC Warsh First Meeting / PCE + CPI + Nvidia Earnings + SpaceX IPO + Hormuz / 30 Events + 5 Strategies

Real-Time Issue · May 19, 2026

Macro Calendar D-30 — June 17 FOMC Warsh First Meeting — From May PCE and CPI to Nvidia earnings, SpaceX IPO, and Hormuz negotiations: 30 key events and 5 trading strategies every Korean investor must know before June 17.

1. Overview — The D-30 Countdown Begins

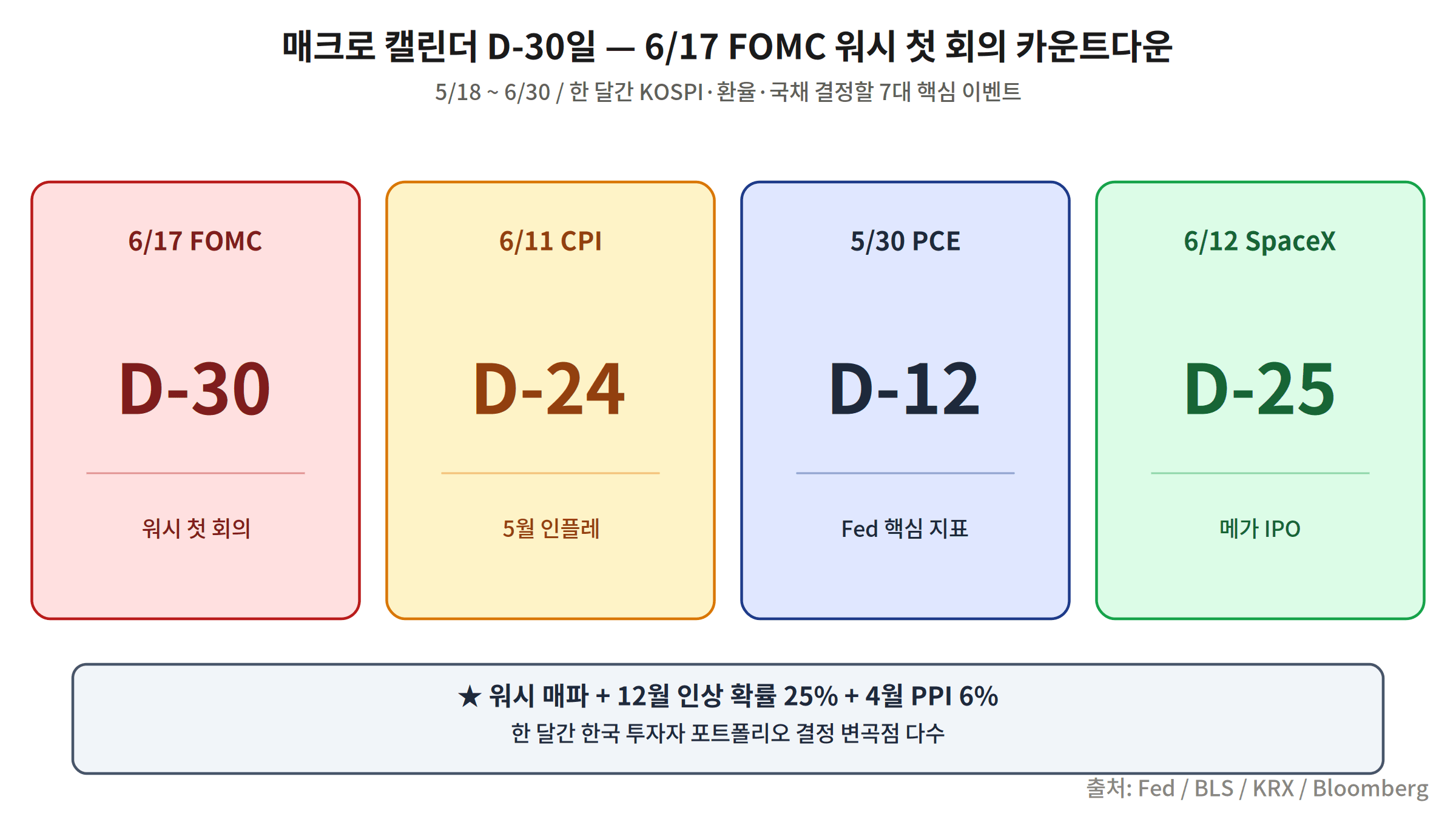

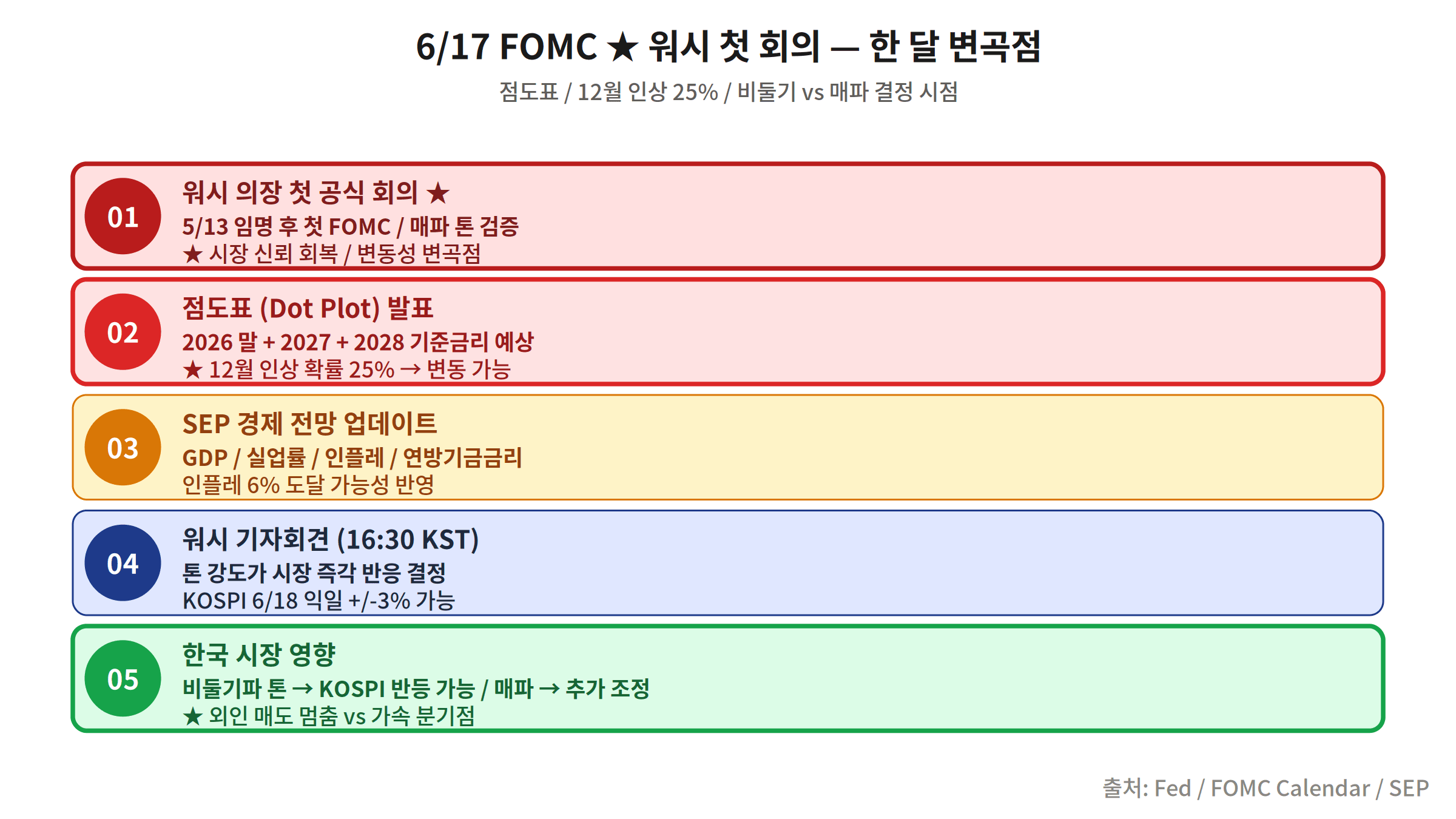

As of today, May 19, 2026 (Tuesday), we are exactly D-30 from the Federal Reserve’s FOMC rate decision scheduled for June 17 (Wednesday). The reason this particular meeting commands such intense market attention is straightforward: it will be the first regular FOMC meeting chaired by the hawkish new Fed Chair, Kevin Warsh.

Since taking office, Chair Warsh has repeatedly made clear that he sees no basis for pivoting to an easing stance until inflation is decisively contained. Against this backdrop, the US PPI has surged to +6.0% year-over-year — well above expectations — while geopolitical tensions with Iran have destabilized oil supply flows through the Strait of Hormuz. Layered on top are market-moving events including Nvidia’s earnings report and the highly anticipated SpaceX IPO, driving volatility to its highest levels in months.

This article systematically maps the 30 critical events Korean investors must track during the D-30 window (5/18–6/17) and presents five concrete trading strategies for each scenario. The four-headed pressure front — ①Warsh’s hawkish stance, ②6% PPI inflation, ③Iran war risk, ④Hormuz negotiation deadline — is operating simultaneously. Here is how to navigate it.

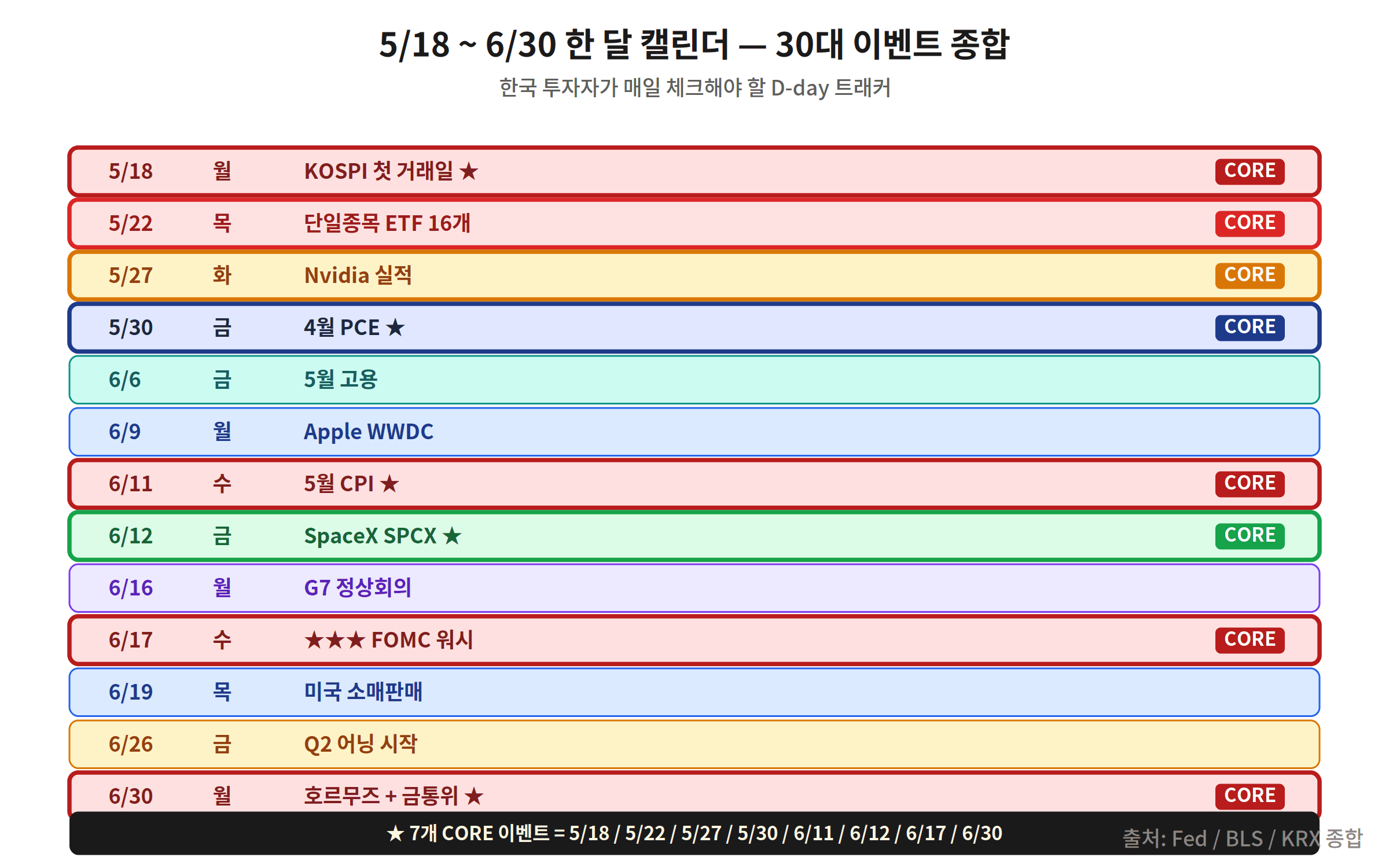

2. Late May Schedule (5/18–5/31)

Late May may appear calm, but four high-intensity events are stacked in rapid succession.

- 5/18 (Mon) — KOSPI Reopens: Korean equities resume trading after the extended holiday. Foreign investor flows and the USD/KRW exchange rate are the first signals to watch. The 1,380 KRW level is the critical short-term support line for the won.

- 5/22 (Thu) — Nvidia Q1 Earnings (★): Bloomberg consensus: EPS $0.93, revenue $43.5B. Blackwell chip shipment guidance will set the directional tone for the entire semiconductor sector. An earnings beat could trigger a +3–5% sympathetic move in the KOSPI semiconductor index.

- 5/27 (Tue) — US Q1 GDP Revision: The advance reading came in at -0.3% annualized. A confirmed contraction in the revision would reignite recession debate, typically triggering a dollar-weakness, gold-strength pattern.

- 5/30 (Fri) — April PCE Price Index (★): The Fed’s preferred inflation gauge. Headline PCE consensus: +2.7% YoY; core PCE: +2.6% YoY. A surprise above consensus could immediately push the probability of a June rate hike above 30%.

The critical combination to watch is Nvidia earnings (5/22) paired with PCE (5/30). If Nvidia beats and PCE prints below consensus, risk-on momentum is likely. If PCE surprises to the upside and Nvidia guidance disappoints simultaneously, immediate position reduction is warranted.

3. Early June Schedule (6/1–6/11)

The first week of June represents the most data-dense segment of the D-30 window. Employment figures, manufacturing PMI, and services PMI are released in rapid succession — providing the final data inputs before the FOMC blackout period begins.

- 6/1 (Mon) — ISM Manufacturing PMI: Prior reading: 48.7 (contraction territory). A return above 50 would signal recovery momentum and complicate the case for rate cuts.

- 6/3 (Tue) — JOLTS Job Openings: Prior: 8.4 million openings. A leading indicator for how quickly labor demand is cooling — watch for a trend below 8 million as a dovish signal.

- 6/6 (Fri) — May Non-Farm Payrolls (NFP): Consensus: +170,000 jobs, unemployment rate 4.2%. A stronger-than-expected print would reinforce the Fed’s hawkish case.

- 6/9 (Mon) — ISM Services PMI: Services account for over 75% of the US economy, making this a more direct driver of the PCE trajectory than manufacturing PMI.

- 6/11 (Wed) — May CPI (★★): The last major inflation data point before the FOMC meeting. Consensus: headline CPI +3.1% YoY, core CPI +3.3% YoY. A surprise of +0.2pp or more above consensus would immediately price in a June rate hike. A miss to the downside would trigger a short-term surge in risk assets.

The June 11 CPI is the single most important event of the D-30 window after the FOMC meeting itself. Adjusting positions within the 24–48 hours before and after this release is a proven tactical approach.

4. June 17 FOMC — Everything About Warsh’s First Meeting

Kevin Warsh served as a Federal Reserve Governor during the George W. Bush administration and is widely remembered for his dissent against emergency rate cuts during the 2008 financial crisis — one of the most hawkish stances on record. Since taking the helm in February 2026, he has emphasized “price stability above all” in every public appearance.

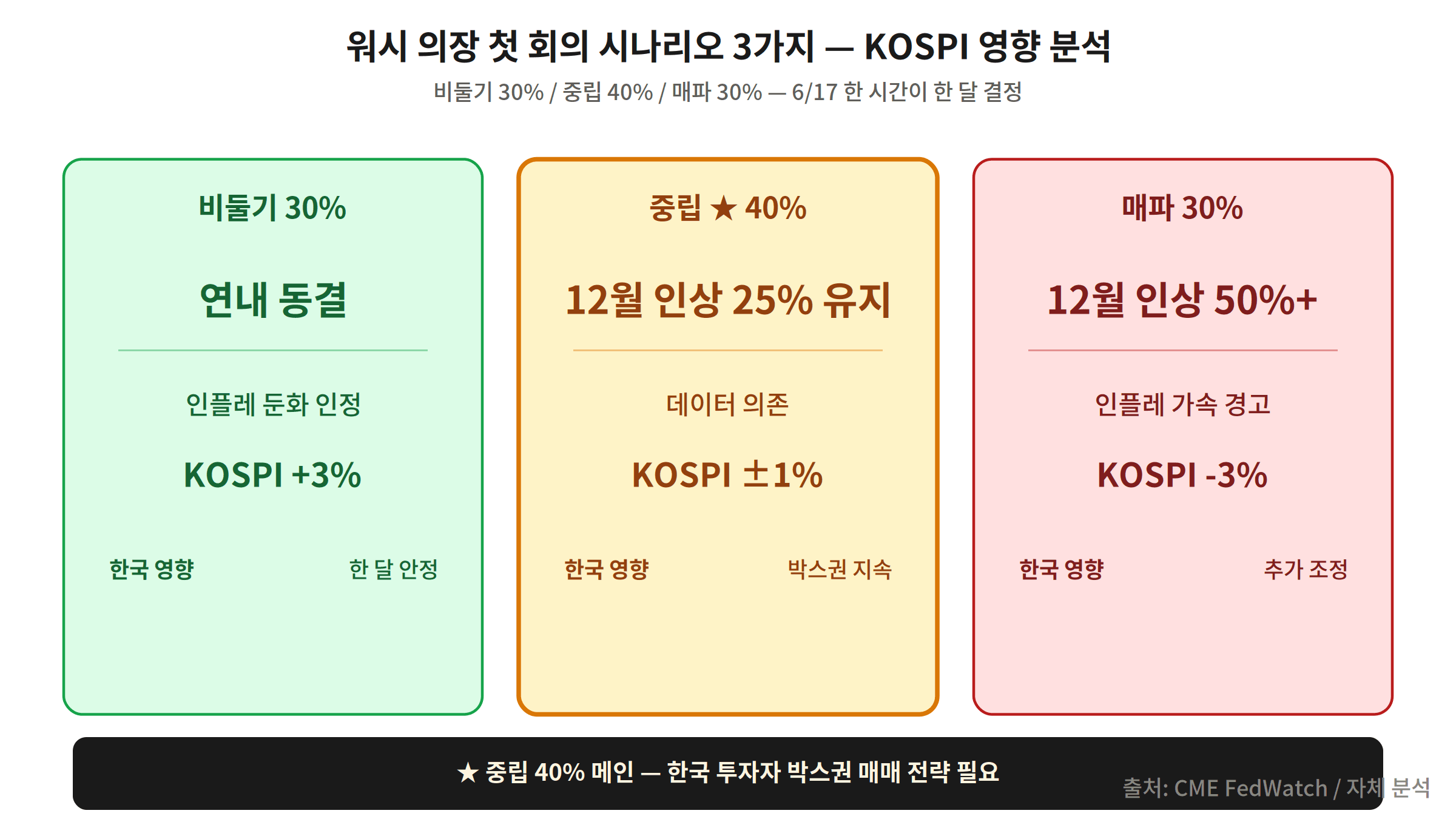

The current federal funds rate target range stands at 4.75–5.00%. Markets are pricing three possible outcomes from the June 17 decision.

- Hold + Dovish Tone (Dove Scenario): Condition — both PCE and CPI print below consensus. Probability: 30%. Market impact: S&P 500 +2–3%, KOSPI +1.5–2%, TLT bonds +2–3%, USD/KRW toward 1,350.

- Hold + Hawkish Tone (Neutral Scenario): Condition — mixed data, inflation in line with expectations. Probability: 40% — the most likely outcome. Market impact: initial sell-off followed by bounce, VIX in the 20–25 range, range-bound price action. Most dangerous environment for retail traders due to whipsaw signals.

- 25bp Hike Signal or Actual Hike (Hawk Scenario): Condition — core CPI ≥3.5%, strong employment. Probability: 30%. Market impact: S&P 500 -3–5%, Nasdaq -5–7%, Dollar Index +1.5–2%, USD/KRW touching 1,400–1,420. KOSPI -2–3%, with REITs and high-PER growth stocks hit hardest.

The dot plot is equally important. Under former Chair Powell, the median dot projected two rate cuts in 2026. If Warsh’s first dot plot reduces this to one or zero, the bond market shock could be significant — comparable in scale to the 2022 hawkish pivot repricing.

5. Late June Schedule (6/12–6/30)

The calendar does not clear after the FOMC. Three structurally significant events remain in the latter half of June, each capable of reshaping market dynamics on its own.

- 6/12 (Thu) — SpaceX IPO Subscription Opens (Expected): Estimated valuation: $250B–$300B. If confirmed as the largest technology IPO on record, the capital absorption effect would create near-term headwinds for existing tech holdings as liquidity is redirected. Korean retail investors should check in advance whether their overseas brokerage accounts support direct IPO participation.

- 6/30 (Tue) — Bank of Korea Monetary Policy Decision: Current base rate: 2.75%. If the Fed maintains its hawkish stance, the BOK’s room for additional cuts narrows considerably. With USD/KRW above 1,400, a hold is the base case. However, if domestic growth indicators deteriorate sharply, a 25bp minority dissent vote in favor of a cut may appear.

- 6/30 (Tue) — Iran-US Hormuz Negotiation Deadline: The Strait of Hormuz handles approximately 20% of global seaborne oil trade. The current diplomatic track reportedly has a provisional deadline of June 30. If negotiations collapse, WTI crude could breach $100 per barrel, reigniting energy inflation and handing the Fed additional justification for continued tightening.

6. Three FOMC Scenarios — Probability and Market Impact

Breaking each scenario down by asset class provides a more actionable picture of the risk-reward landscape.

- Dove Scenario (30% probability): Trigger conditions — core PCE ≤2.4%, core CPI ≤3.0%. Outcome — hold + dot plot maintains or increases 2026 cut projections. Assets: Nasdaq +3–4%, gold +1–2%, Dollar Index -0.8–1.2%, USD/KRW strengthens to 1,350 range. KOSPI semiconductors and growth stocks lead. TLT bonds +2–3%.

- Neutral Scenario (40% probability): Trigger — mixed data, inflation roughly in line. Outcome — hold + “data-dependent” language repeated. Assets: initial sell-off then recovery, elevated volatility, VIX 20–25, directionless range-bound action. Most dangerous phase for retail investors prone to overtrading.

- Hawk Scenario (30% probability): Trigger — core CPI ≥3.5%, strong labor data. Outcome — 25bp hike signal or actual hike, dot plot reduced to 0–1 cuts for 2026. Assets: S&P 500 -3–5%, Nasdaq -5–7%, Dollar Index +1.5–2%, USD/KRW 1,400–1,420. Gold dips short-term then rebounds. KOSPI -2–3%, REITs and high-PER growth stocks directly hit.

Probability-weighted across all three scenarios, the market’s implicit expectation is “a hold, but not a comfortable one.” In other words, the rate itself is likely to stay put, but Warsh’s hawkish rhetoric at the press conference is expected to keep a ceiling on risk assets — making selectivity more important than directional bets.

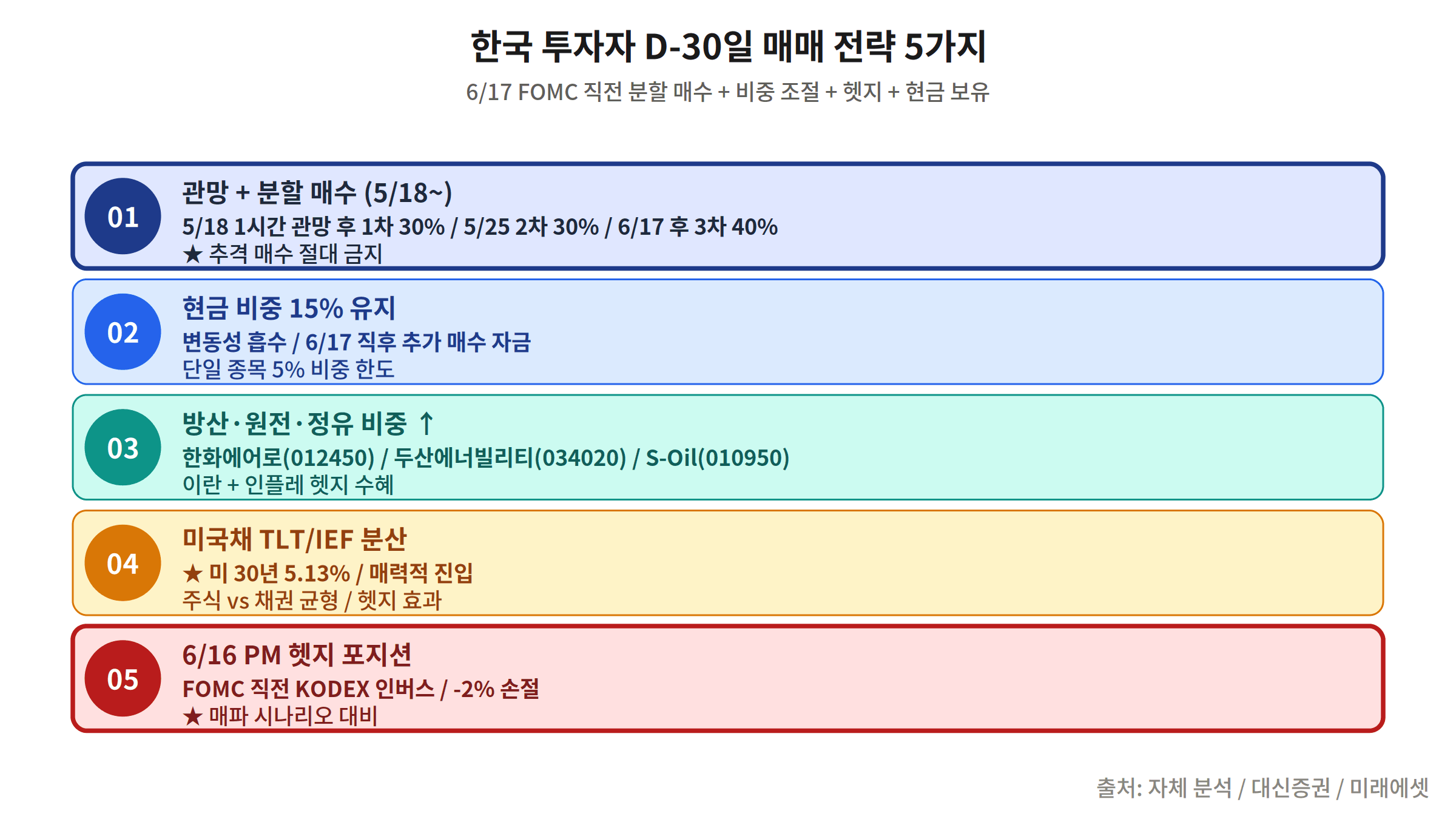

7. Five D-30 Trading Strategies

In a period of peak uncertainty like D-30, defense outranks offense. Apply the following five strategies in sequence.

- Maintain 30%+ Cash Allocation: Right now, convert at least 30% of your portfolio to cash or short-duration bonds (SGOV, Korean CMA accounts). Under the four-headed pressure scenario, this reserve becomes the ammunition for buying dips at attractive levels. Cash is not a zero-return asset — it carries option value when volatility is high.

- Three-Stage Scaled Buying: ① After Nvidia earnings (5/22): first tranche into semiconductors (10% of portfolio). ② After CPI release (6/11): conditional second tranche based on the print (10%). ③ After FOMC confirmation (6/17): third tranche once directional clarity emerges (10%). Never buy in one lump — let each event’s outcome inform the next entry.

- Nvidia 5/22 Earnings — Semiconductor Sector Inflection Point: If EPS clears consensus by +10% or more ($1.02+) and next-quarter guidance exceeds $45B revenue, treat it as a buy signal for Samsung Electronics and SK Hynix. If EPS misses and guidance is cut, reduce semiconductor exposure and hold cash until the June 11 CPI.

- Exploit 6/11 CPI Volatility: By the afternoon of June 10 (the day before CPI), reduce high-volatility positions. Immediately after the print: if below consensus → add Nasdaq ETFs (QQQ, KODEX US Nasdaq 100); if above consensus → add gold (GLD, KODEX Gold Futures) and USD ETFs, sell high-PER positions.

- Clear Risk Positions Before FOMC (by June 16 close): By the close of trading on June 16 (Tuesday), exit or reduce to less than half: leveraged ETFs, individual high-PER growth stocks, and margin positions. On FOMC day itself, act only after the decision is announced. In the D-30 window, making money through reaction rather than prediction is the core discipline.

8. Sector Outlook for D-30

The following sector ratings assume the four-headed pressure environment (hawkish Fed + high inflation + geopolitical risk + IPO liquidity absorption) persists through the D-30 window.

- Overweight Sectors:

- 🛡 Defense: Escalating Hormuz risk → accelerating global defense spending. Focus: Hanwha Aerospace, LIG Nex1, domestic defense ETFs.

- 🥇 Gold & Precious Metals: 6% PPI + geopolitical instability = sustained safe-haven demand. Target price: over $3,200/oz. Instruments: KODEX Gold Futures (H), GLD.

- 🏦 Banks & Financials: Net interest margin (NIM) expands in a hold-or-hike rate environment. Focus: KB Financial, Shinhan Financial, JPMorgan.

- Neutral Sectors:

- 📦 Exporters (Auto, Chemicals): Weak-won tailwind offset by global demand slowdown. Individual stock selection required; avoid blanket sector bets.

- 💾 Semiconductors: Nvidia earnings (5/22) will determine the short-term direction for the entire sector. Hold neutral until the results are confirmed.

- Underweight Sectors:

- 🏢 REITs / Real Estate: Most vulnerable to rate-hike risk. In the hawk scenario, a decline of -10% or more is plausible.

- ⚡ Utilities: Functions as a bond proxy — demand deteriorates rapidly when rate expectations rise.

- 📈 High-PER Growth Stocks: Tech and biotech names trading at 50x+ PER are directly exposed to discount-rate increases. SpaceX IPO liquidity absorption compounds the headwind.

9. Full 30-Event Calendar (5/18–6/30)

Below is a comprehensive chronological list of the 30 events to monitor across the D-30 window. ★ denotes high-impact events with significant market-moving potential.

- 5/18 (Mon) KOSPI Reopens — monitor foreign investor flows

- 5/19 (Tue) US Housing Starts

- 5/20 (Wed) FOMC Minutes Release (May meeting) ★

- 5/21 (Thu) US Weekly Jobless Claims

- 5/22 (Thu) Nvidia Q1 Earnings ★★

- 5/23 (Fri) US Manufacturing PMI Flash

- 5/27 (Tue) US Q1 GDP Revision ★

- 5/28 (Wed) US Durable Goods Orders

- 5/29 (Thu) US Weekly Jobless Claims

- 5/30 (Fri) April PCE Price Index ★★

- 6/1 (Mon) ISM Manufacturing PMI

- 6/2 (Tue) Auto Sales Data

- 6/3 (Tue) JOLTS Job Openings ★

- 6/4 (Wed) ADP Private Payrolls

- 6/5 (Thu) US Trade Balance

- 6/6 (Fri) May Non-Farm Payrolls (NFP) ★★

- 6/9 (Mon) ISM Services PMI ★

- 6/10 (Tue) US Producer Price Index (PPI Revision) ★

- 6/11 (Wed) May CPI ★★★

- 6/12 (Thu) SpaceX IPO Subscription Opens (Expected) ★★

- 6/13 (Fri) University of Michigan Consumer Sentiment (Flash)

- 6/16 (Mon) Fed Blackout Period Ends — last Fed official comments before FOMC

- 6/17 (Tue) FOMC Rate Decision + Warsh Press Conference ★★★

- 6/18 (Wed) FOMC Dot Plot Analysis — post-decision market follow-through

- 6/19 (Thu) US Weekly Jobless Claims

- 6/20 (Fri) US Futures Expiration (Quadruple Witching) ★

- 6/24 (Tue) US Consumer Confidence (CB)

- 6/27 (Fri) May PCE Price Index (Preliminary) ★

- 6/30 (Mon) Bank of Korea Monetary Policy Decision ★★

- 6/30 (Mon) Iran-US Hormuz Negotiation Deadline ★★

Of these 30 events, the five that absolutely must be in every investor’s calendar with pre-planned response protocols are: 5/22 (Nvidia), 5/30 (PCE), 6/11 (CPI), 6/17 (FOMC), and 6/30 (BOK + Hormuz). Building your position adjustment plan around these five anchor dates is the foundation of any D-30 survival strategy.