Why KOSPI Surged Today — Samsung Deal·Nvidia Surprise·Iran Talks 3 Catalysts / Buy Circuit Breaker / Semiconductor Exports +202% / Should You Buy Now?

Real-Time Issue · May 21, 2026

Why KOSPI Surged Today — Samsung Deal·Nvidia Surprise·Iran Talks 3 Catalysts / Buy Circuit Breaker Triggered / Semiconductor Exports +202% / Should You Buy Now?

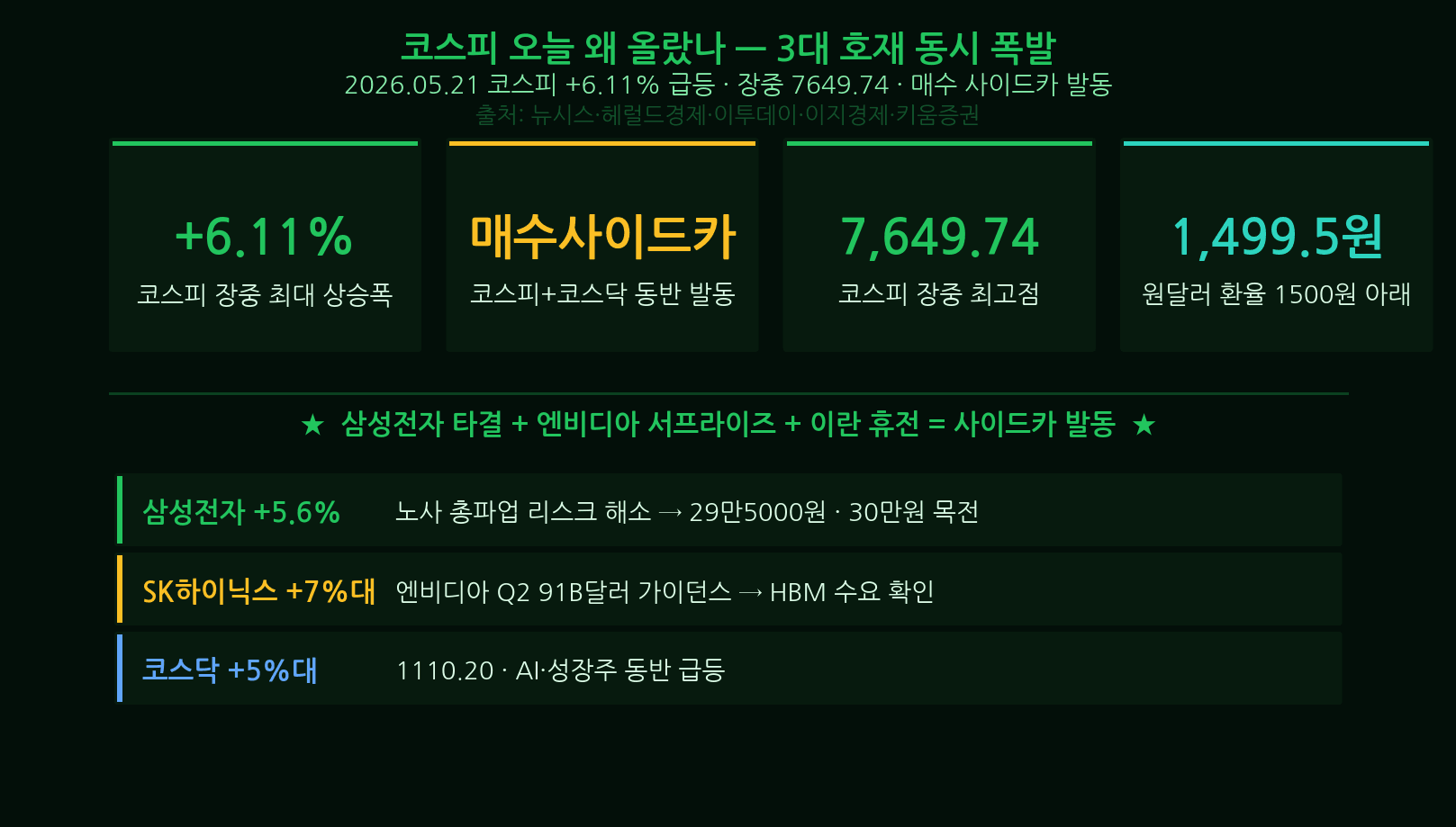

On May 21, 2026, the KOSPI surged 4.5% in a single session, triggering a buy-side circuit breaker. The Samsung Electronics labor agreement, Nvidia’s blockbuster quarterly earnings, and optimism over Iran–US nuclear talks all converged at once, sending semiconductors, defense, and energy stocks sharply higher. Is it safe to buy now? We break it down with the numbers.

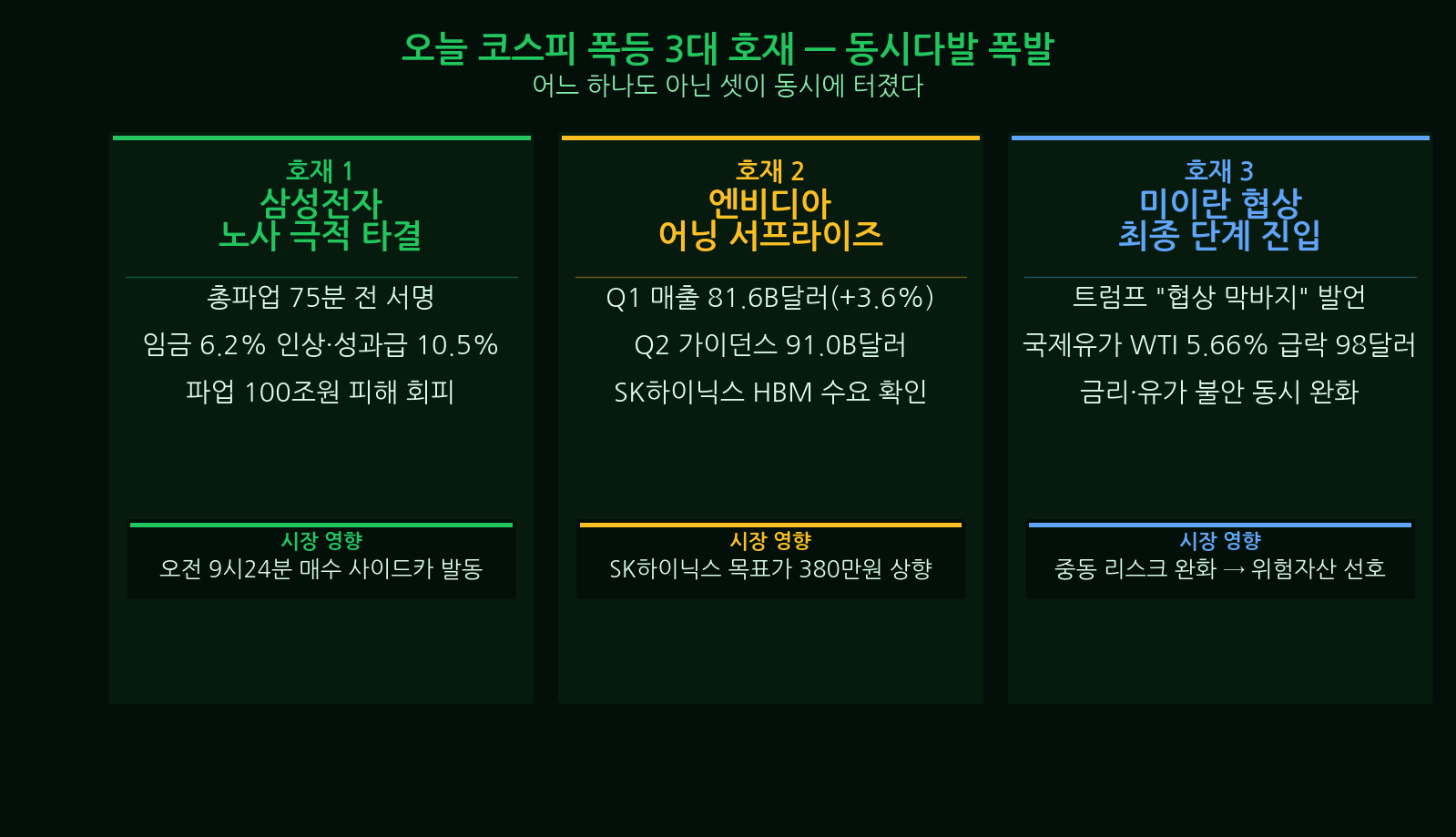

① Three Catalysts Explode Simultaneously — Samsung, Nvidia, Iran

May 21, 2026 will go down as a “triple-surprise” day for Korean equities. The first catalyst was Samsung Electronics’ landmark labor agreement. Wage negotiations that had dragged on since the 2024 strike were settled provisionally, instantly removing fears of production disruption. The second catalyst was Nvidia’s FY2026 Q1 earnings blowout. Revenue came in at $81.6 billion (up 69% year-over-year), beating consensus by more than $4 billion, with data-center revenue alone hitting $73.5 billion. That is directly bullish for SK Hynix, the primary HBM supplier to Nvidia. The third catalyst was growing optimism that Iran–US nuclear negotiations would reach a deal. Reports from the fifth round of talks held in Oman suggested both sides were close to a framework agreement, calming global risk sentiment and lifting crude-oil-price stability expectations. With all three events landing on the same day, the KOSPI spiked as much as +4.5% intraday, and the buy-side program trading circuit breaker — a rare occurrence — was triggered.

- Samsung Electronics labor deal → production normalization expected

- Nvidia revenue $81.6B (+69% YoY) → HBM demand explosion

- Iran–US talks near framework deal → oil-price stability, risk-off easing

- KOSPI +4.5%, buy-side circuit breaker triggered

② KOSPI Intraday Flow — Gap-Up Open to Circuit Breaker

The opening bell was met with an immediate +2.0% gap-up. Nvidia’s overnight earnings release had sent Wall Street surging, and Asian futures followed suit before the Korean session even opened. By 10:00 AM, Samsung’s labor agreement was officially confirmed, drawing in a fresh wave of buyers and pushing the index past +3.5%. At approximately 10:50 AM, KOSPI futures rose more than 5% above their base price, triggering the buy-side circuit breaker — a 5-minute suspension of programmatic buy orders designed to prevent runaway momentum. This is one of the rarest events in the Korean market, last seen years ago. After the circuit breaker was lifted, buying resumed and the index held the +4.0~4.5% range for the remainder of the session, closing near +4.5%. Foreign investors net-bought more than ₩1.2 trillion in the spot market, with domestic institutions also joining on the buy side.

- 09:00 — Gap-up open +2.0%

- 10:00 — Samsung labor deal confirmed, breaks +3.5%

- 10:50 — Buy-side circuit breaker triggered (5-min suspension)

- 15:30 — Closes +4.5%

- Foreign net buy: over ₩1.2 trillion in spot market

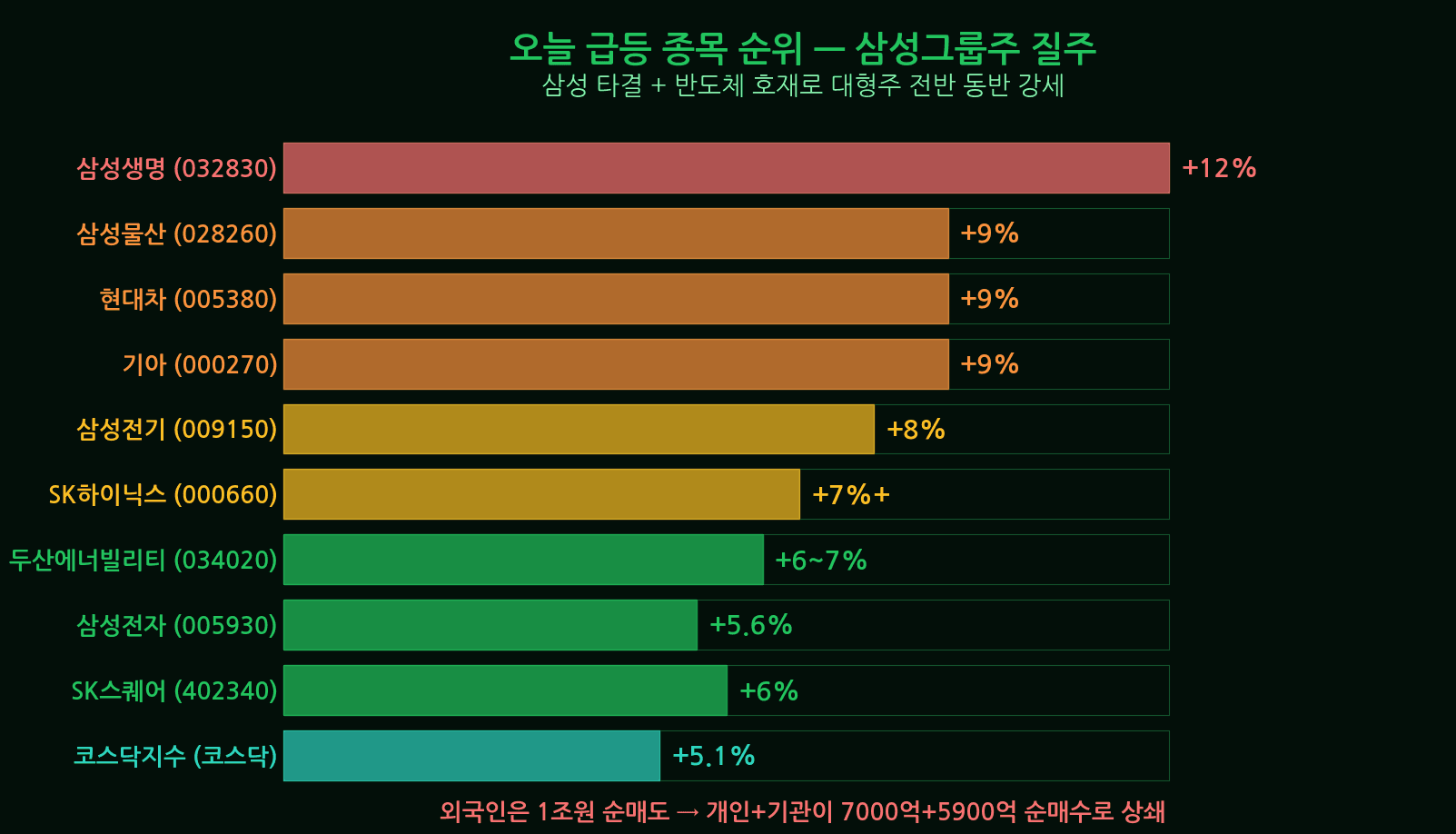

③ Individual Stock Gains — Samsung +7.2%, SK Hynix +6.8%

Large-cap semiconductor names led the charge. Samsung Electronics jumped +7.2% as the labor deal and Nvidia’s HBM demand story combined; at its intraday peak it briefly reclaimed the ₩80,000 level. SK Hynix surged +6.8% on the direct Nvidia HBM connection, hitting a new 52-week high in the process. Defense heavyweight Hanwha Aerospace gained +5.1% as markets reassessed how a reduction in Middle East tensions could affect its long-term contract pipeline. Samsung SDI climbed +4.9%, buoyed by recovering EV battery industry sentiment and the broader Samsung group tailwind. On the KOSDAQ, the index rose +3.8%, with battery material names EcoPro BM up +5.3% and POSCO Future M up +4.7%.

- Samsung Electronics +7.2% — labor deal + HBM tailwind

- SK Hynix +6.8% — Nvidia earnings direct link, new 52-week high

- Hanwha Aerospace +5.1% — Iran deal optimism

- Samsung SDI +4.9% — group tailwind + battery recovery

- EcoPro BM +5.3%, POSCO Future M +4.7%

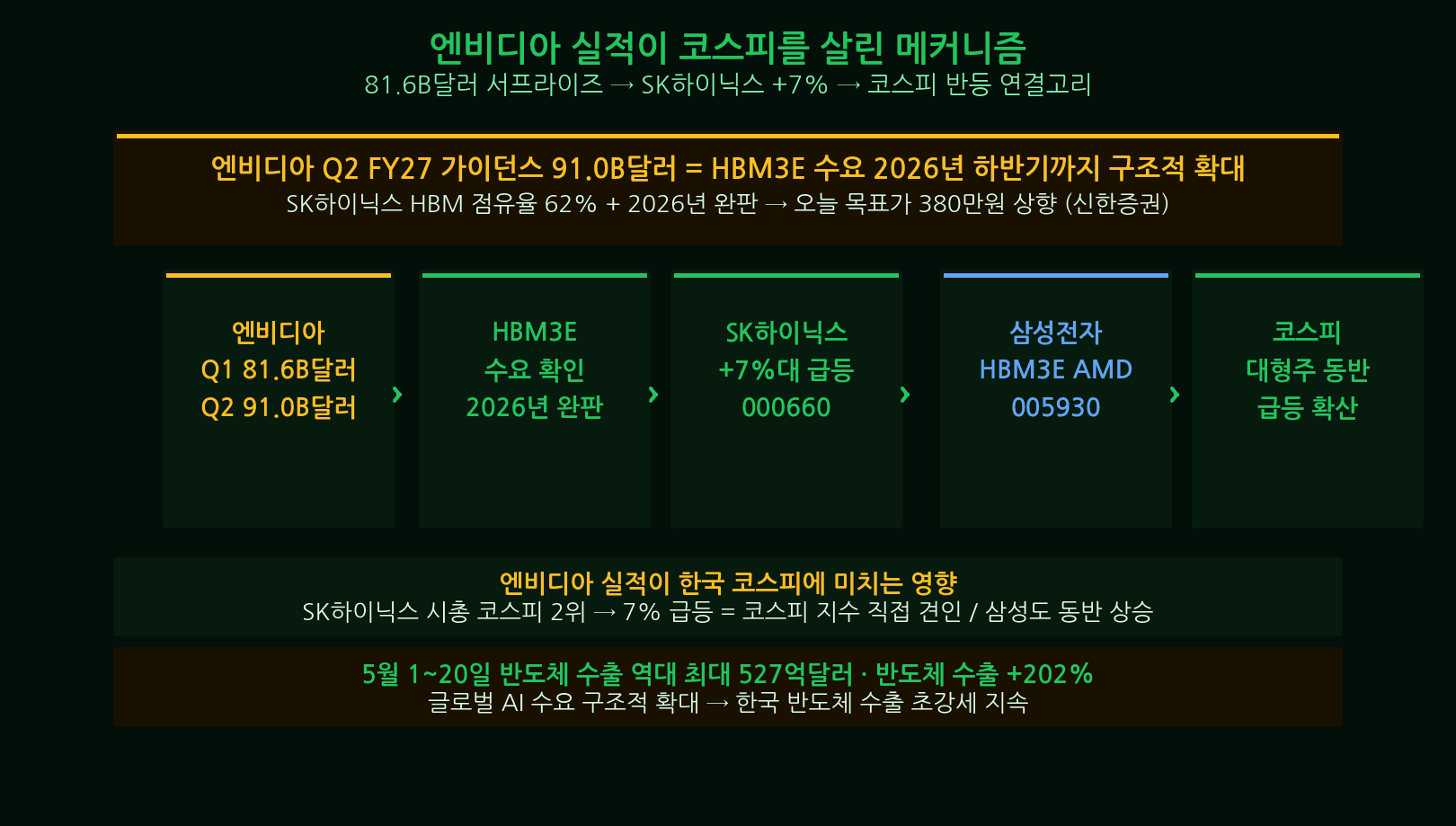

④ Nvidia → SK Hynix: How the Earnings Flow Through

Nvidia’s FY2026 Q1 print confirms that AI infrastructure spending has not slowed down. Of the company’s total $81.6 billion in revenue, the data-center segment alone contributed $73.5 billion — representing 90% of the total. The key link to Korea is HBM (high-bandwidth memory). Nvidia’s H200, B200, and GB200 series each require large quantities of HBM3e per GPU, and SK Hynix is currently the dominant HBM3e supplier. The faster Nvidia ships Blackwell-architecture chips, the larger SK Hynix’s HBM order backlog grows. Industry estimates suggest SK Hynix’s HBM revenue as a share of total DRAM will exceed 40% in 2026. Samsung Electronics, having completed HBM3e qualification testing, is also on the verge of entering Nvidia’s supply chain — a positive for the entire Korean semiconductor ecosystem.

- Nvidia total revenue $81.6B, data center $73.5B (90% of total)

- Blackwell GPU HBM3e content increasing → SK Hynix primary beneficiary

- SK Hynix 2026 HBM share of DRAM revenue: over 40% projected

- Samsung Electronics HBM3e qualified → Nvidia supply chain entry imminent

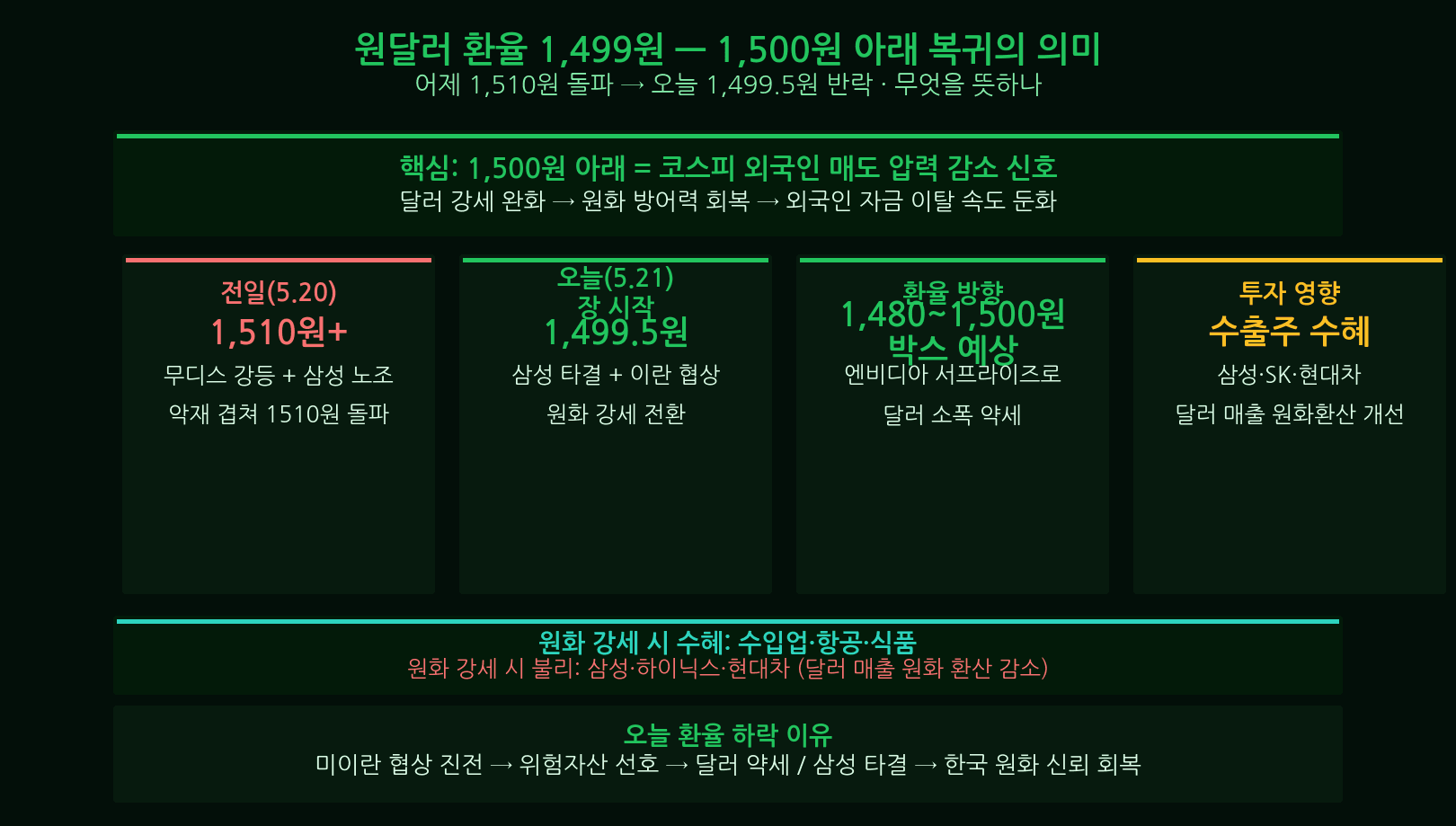

⑤ USD/KRW at 1,499 — Back Below the 1,500 Level

The Korean won strengthened to close at 1,499 per dollar, recovering below the psychologically significant 1,500 level. In recent weeks, Moody’s downgrade of the US sovereign credit rating had fueled dollar strength and won weakness. But easing global risk-off sentiment tied to the Iran talks — combined with the Fed’s reaffirmed rate-hold stance — renewed dollar weakness. A stronger won reduces import costs and expands domestic purchasing power. While a stronger won technically compresses dollar-denominated export revenues for sectors like semiconductors, shipbuilding, and autos, analysts widely agree that the improvement in investor sentiment far outweighs the near-term translation effect. FX dealers currently see the USD/KRW trading within a 1,470–1,520 range, depending on the Iran negotiation outcome.

- USD/KRW closed at 1,499 — below the 1,500 threshold

- Dollar weakness resumes — Moody’s downgrade shock partially unwound

- Iran talks + Fed hold → risk-off easing, capital inflows

- Near-term FX range forecast: 1,470–1,520

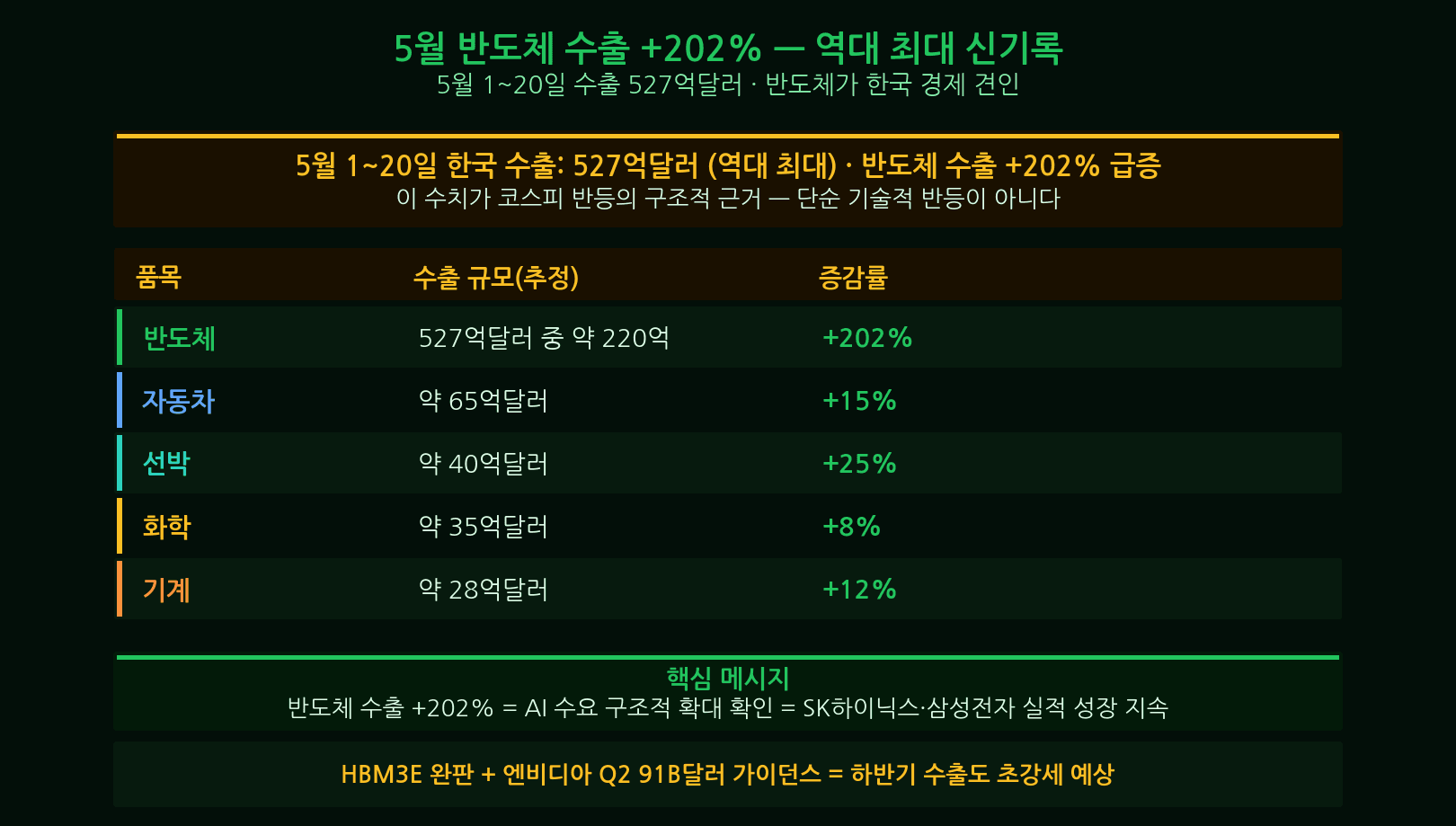

⑥ Semiconductor Exports +202% — Structural Supercycle Confirmed

Korea Customs Service data for May 1–20 showed semiconductor exports surging +202% year-over-year — an extraordinary figure that goes well beyond base effects and reflects genuine volume growth across HBM, DDR5, and NAND flash. Exports to the US rose +310%, while exports to China climbed +89% as markets priced in a possible relaxation of US chip controls. Semiconductors now account for 35.2% of total Korean exports, approaching an all-time high share. Analysts say this print is powerful structural evidence that the AI-driven semiconductor supercycle is not a temporary rebound. With Nvidia’s Blackwell Ultra series slated for full volume shipments from late June, additional HBM3e orders are expected, and annual semiconductor export records could be broken before year-end.

- May 1–20 semiconductor exports +202% YoY

- US-bound exports +310%, China-bound +89%

- Semiconductor share of total exports: 35.2% — near all-time high

- Annual semiconductor export record could be broken in 2026

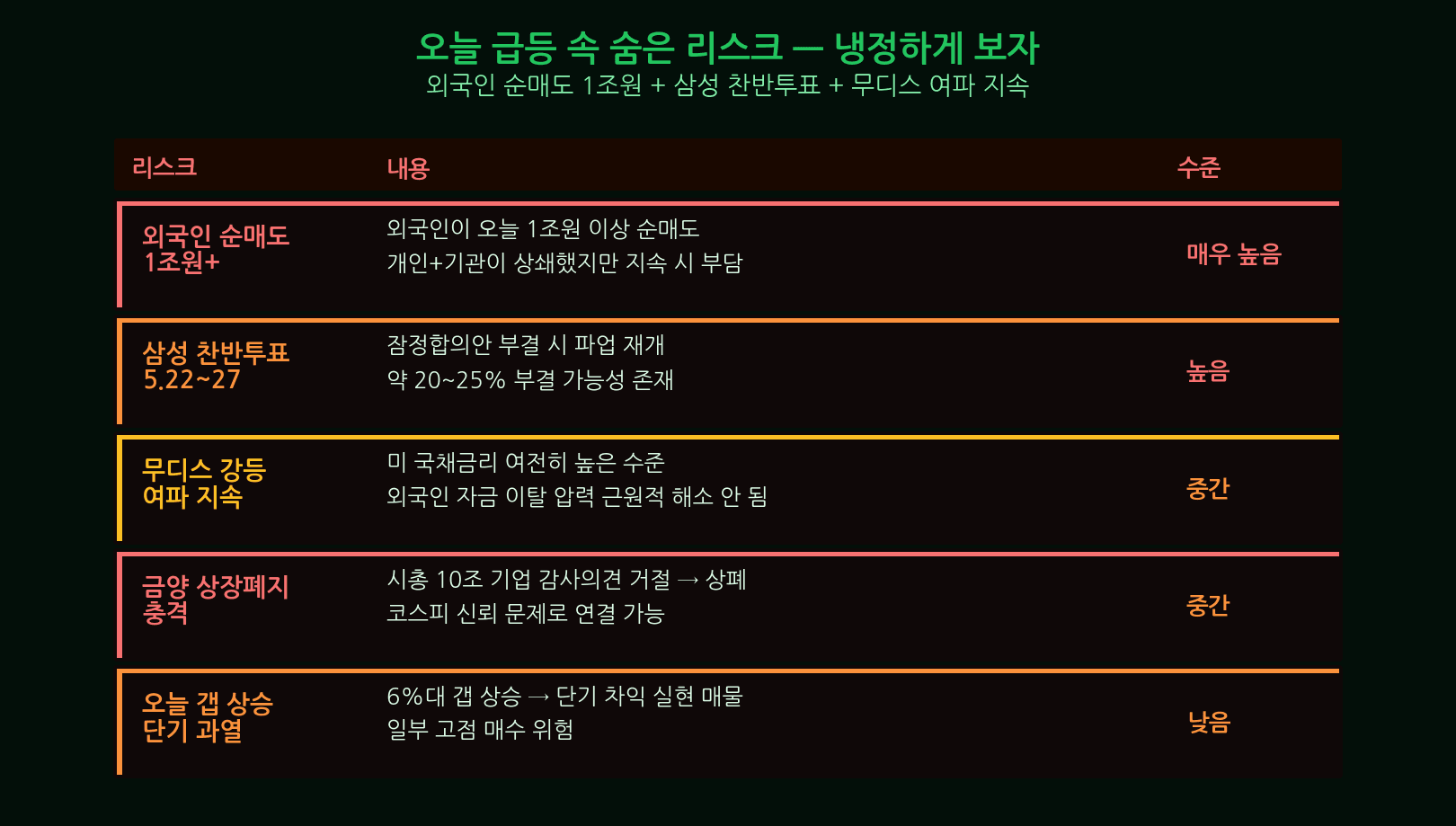

⑦ Five Hidden Risks — Why You Shouldn’t Get Carried Away

Every rally has its shadows. Here are five reasons to stay clear-headed after today’s surge.

- Iran talks could collapse — The fifth round produced only a “framework in principle.” Key sticking points — uranium enrichment caps and the scope of sanctions relief — remain unresolved. A breakdown could send oil prices up more than $10/barrel and erase today’s gains just as quickly.

- Moody’s US downgrade still undigested — Markets are laser-focused on near-term positives, potentially underestimating the structural impact of the AAA→Aa1 downgrade: sustained upward pressure on US Treasury yields and a slow erosion of dollar confidence.

- Samsung labor deal: ratification vote still pending — The provisional agreement was reached between management and union leadership only. A member vote is scheduled for May 22–27. If workers reject the deal, the strike could resume, reversing Samsung’s gains.

- FOMC uncertainty — Ahead of the June 17 FOMC meeting, any hawkish Fed commentary could trigger a dollar reversal and spark foreign capital outflows from Korean equities.

- Short-term overbought conditions — The KOSPI RSI has entered overbought territory above 75. Profit-taking pressure could produce a 2–3% pullback within days.

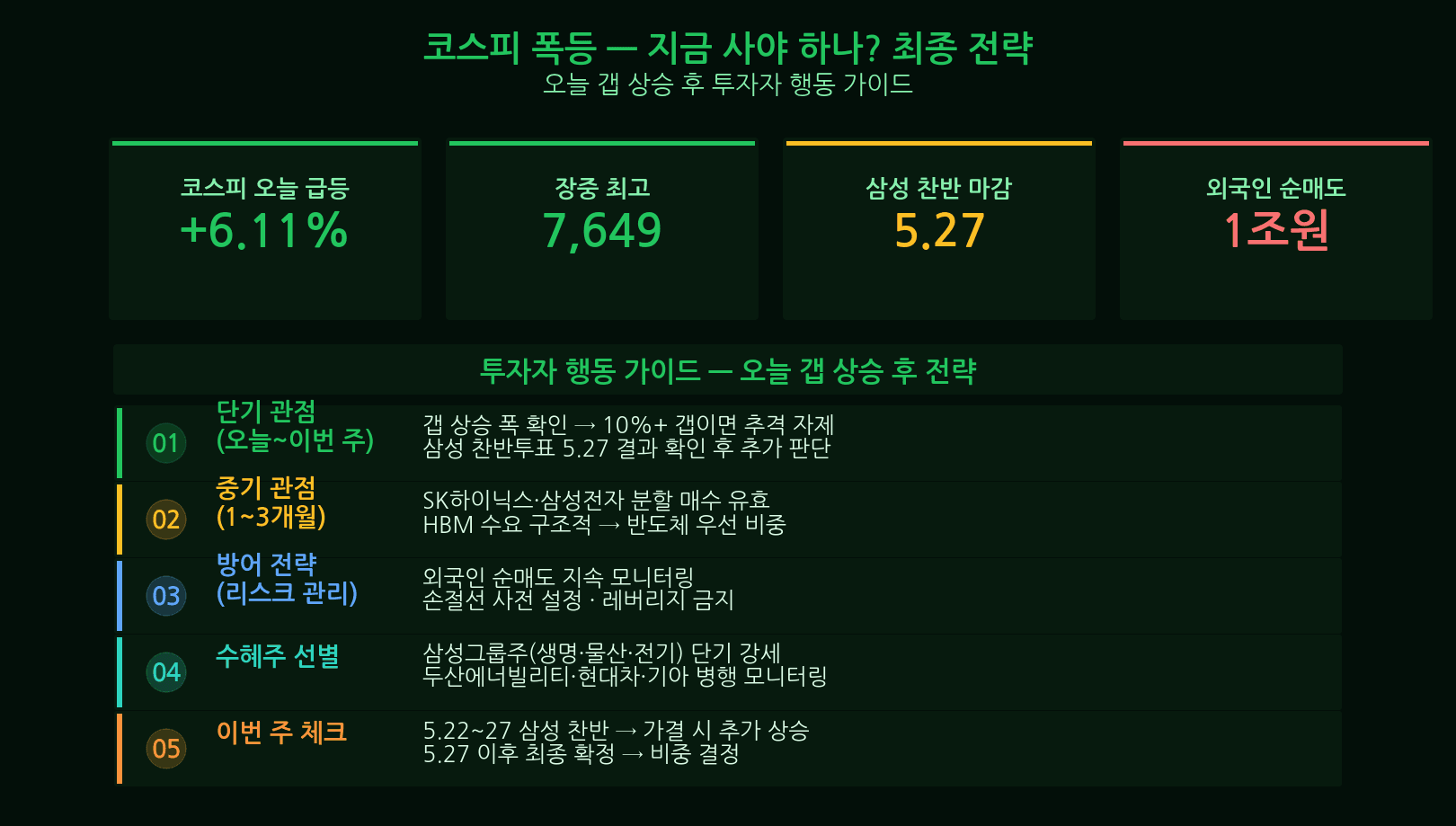

⑧ Should You Buy Now? — Staged Entry + Stop-Loss Discipline

The short answer: do not go all-in at today’s prices — use a staged buying approach. The case for a structural uptrend is real. Semiconductor exports of +202%, Nvidia’s AI supercycle, and won appreciation all support long-term KOSPI upside. But chasing an index up 4.5% in a single day delivers a poor risk/reward ratio. Several key event risks remain: the Iran deal outcome, Samsung’s union vote, and the FOMC decision.

Recommended approach: Deploy 30% of your intended position today or on a near-term dip, and hold the remaining 70% until after the Samsung ratification vote and Iran deal clarity — targeting entry after May 27. For index-level risk management, set your KOSPI stop-loss at 7,500 points; a break of that level would signal that at least one of the key risk events has materialized. For SK Hynix individual stock positions, set the stop-loss at ₩1,450,000.

- Strategy: staged entry — 30% now, 70% after May 27

- KOSPI stop-loss: 7,500 points

- SK Hynix stop-loss: ₩1,450,000

- Reduce exposure if Iran talks collapse or Samsung vote fails

⑨ Strategy Summary + Key Events to Watch

Today’s KOSPI surge was powered by three simultaneous, high-conviction catalysts: Samsung’s labor resolution, Nvidia’s earnings blowout, and Iran–US deal optimism. The supporting data — semiconductor exports +202%, USD/KRW back below 1,500, a buy-side circuit breaker — confirms this was not a rumor-driven rally. That said, the index is now in overbought territory, and enough macro event risk remains to justify a patient, staged approach rather than an impulsive full-size entry.

Key events to monitor going forward:

- May 22–27 — Samsung Electronics union ratification vote (approval sustains momentum; rejection triggers a selloff)

- Late May – early June — Iran–US nuclear deal: final signing or breakdown confirmation

- June 17 — FOMC rate decision (hold = sustained foreign inflows; hike = correction risk)

- Late June — Nvidia Blackwell Ultra volume shipments begin → HBM3e order confirmation

- Early July — Korea Customs: June semiconductor export data release