Nvidia Earnings Tonight — 3 Key Checkpoints + SK Hynix·Hanmi Semiconductor Beneficiaries / Scenario Strategy + Stop-Loss

Real-Time Issue · May 20, 2026

Nvidia Earnings Tonight — 3 Key Checkpoints + SK Hynix·Hanmi Semiconductor Beneficiaries / Scenario Strategy / Stop-Loss Included

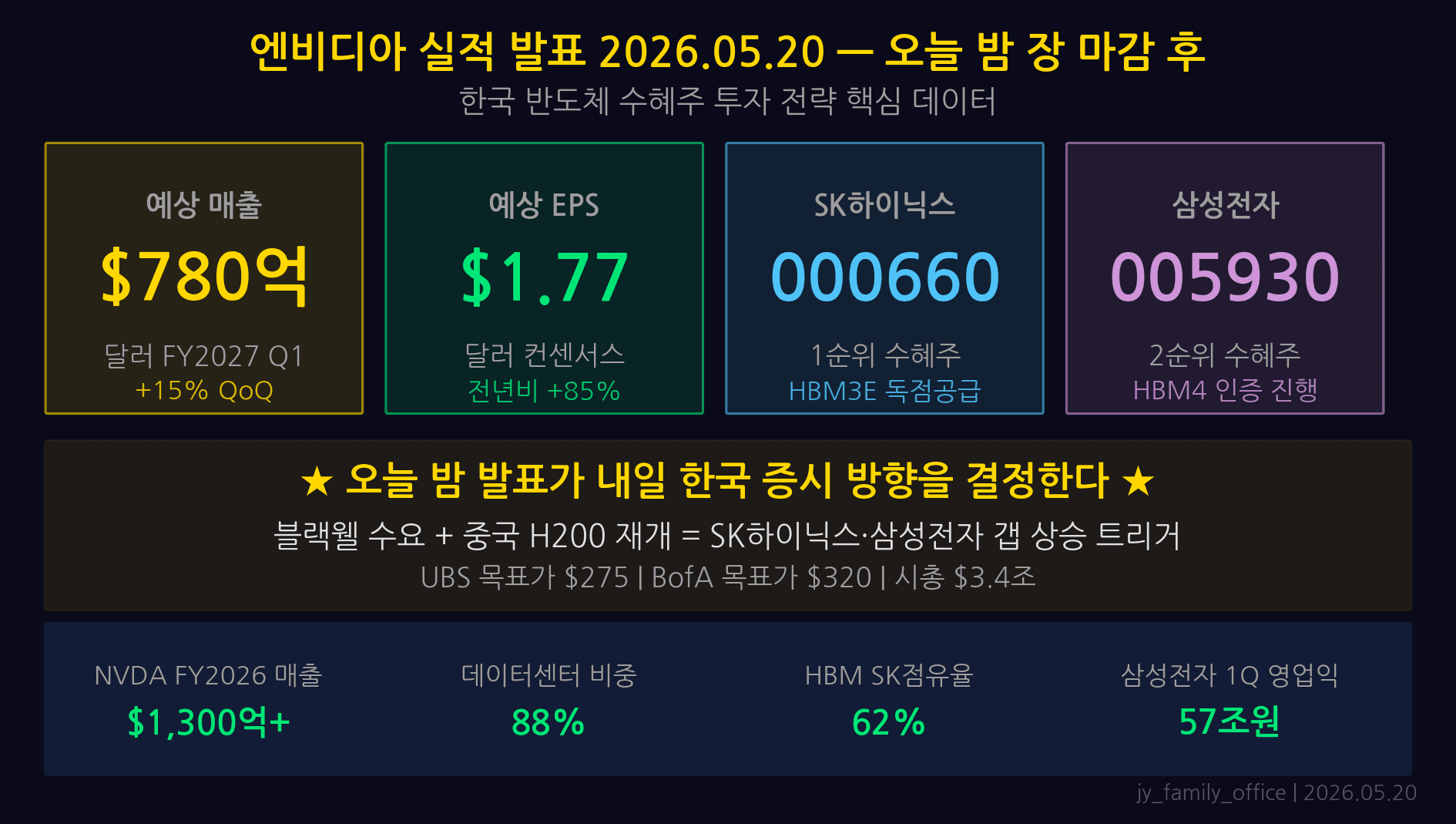

Consensus revenue $43.5B, EPS $0.93, guidance $46B+ — Nvidia’s Q1 FY27 earnings after today’s close will set the direction for Korean semiconductor beneficiary stocks. We’ve mapped out scenario-based strategies for surprise, in-line, and disappointment outcomes, including stop-loss levels for SK Hynix and Hanmi Semiconductor.

1. The Key Numbers — What the Market Expects

Wall Street’s expectations for Nvidia Q1 FY27 (February–April 2026) are crystal clear. The benchmark is consensus revenue of $43.5B and EPS of $0.93. The crucial metric is Data Center segment revenue of $38B, which is expected to represent approximately 87% of total revenue.

Gaming is projected at roughly $3.5B and Professional Visualization at $0.7B — neither carries significant weight with investors. The market’s entire focus sits on the data center number and whether next-quarter guidance clears $46B. In Q4 FY26, CEO Jensen Huang declared that “Blackwell demand exceeds supply.” Tonight’s report is the test of that claim.

For context: Nvidia’s most recent quarter (Q4 FY26) posted revenue of $39.3B, beating the then-consensus of $37.6B by 5%. If the same beat pattern repeats this quarter, actual revenue could reach $45–46B.

2. Tonight’s Earnings — 3 Key Checkpoints

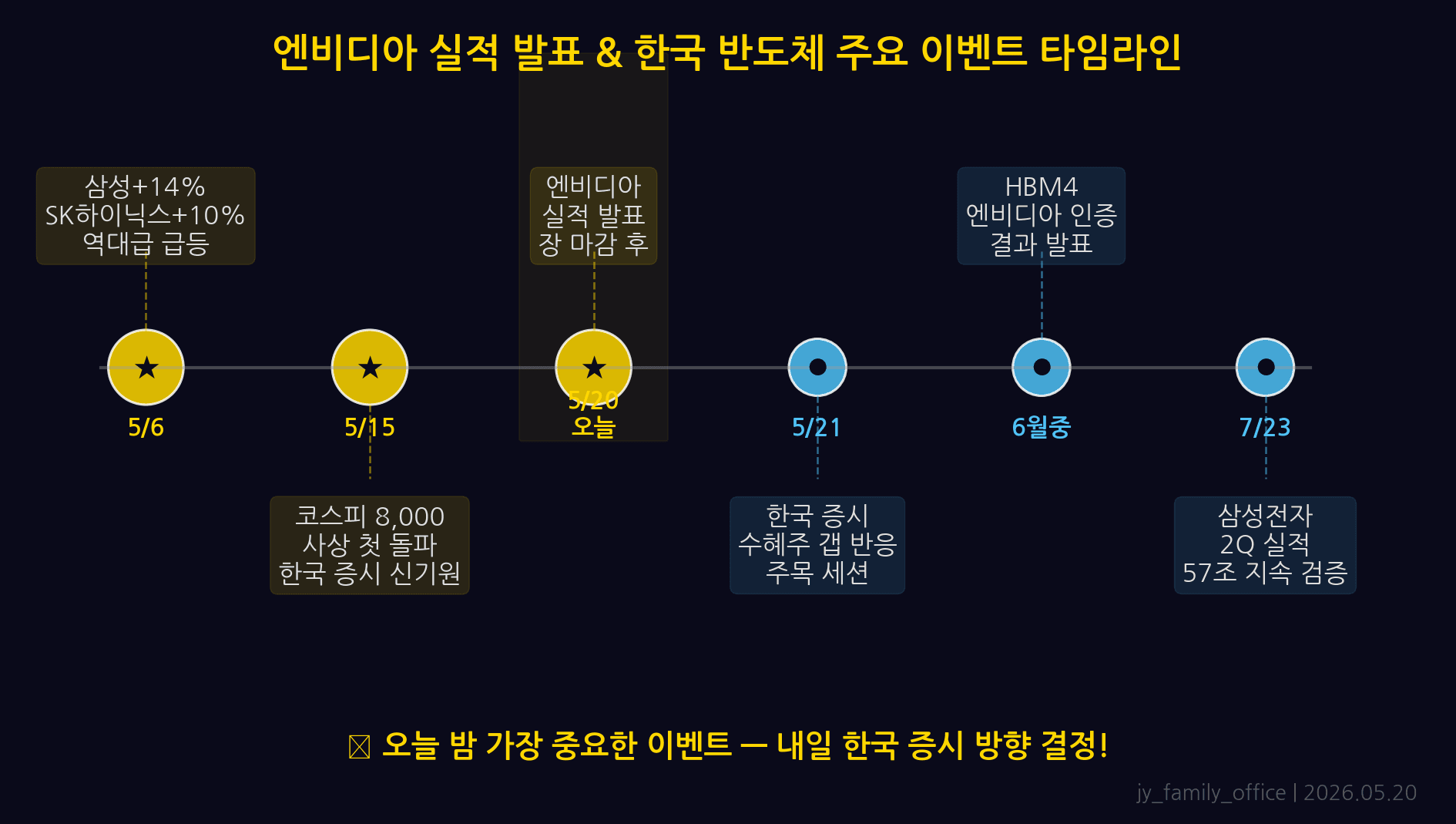

The earnings release goes live at 4:30 PM ET (9:30 AM KST May 21), followed by the conference call 30 minutes later. What Jensen Huang says matters more than the raw numbers. Focus on these three items:

- Data Center revenue vs. $38B consensus — A print above $40B would be treated as a clear beat. A print below $36B would trigger fears of a guidance cut and could cause a sharp sell-off.

- GB300 / Blackwell Ultra guidance and production timeline — Confirmation that GB300 (Blackwell Ultra) mass production is on track for H2 2026 is bullish. Any hint of delay will cause an immediate negative reaction. Watch closely for mentions of HBM4 adoption and the named supplier.

- HBM supply — any mention of a shift to Samsung — SK Hynix currently handles more than 70% of HBM3E supply. If Jensen Huang announces “Samsung HBM quality certification complete,” it would be a short-term negative for SK Hynix. Conversely, silence on the topic — or a statement reinforcing the SK Hynix partnership — is a bullish signal.

3. Revenue and Operating Income Trend — A History of Upside Surprises

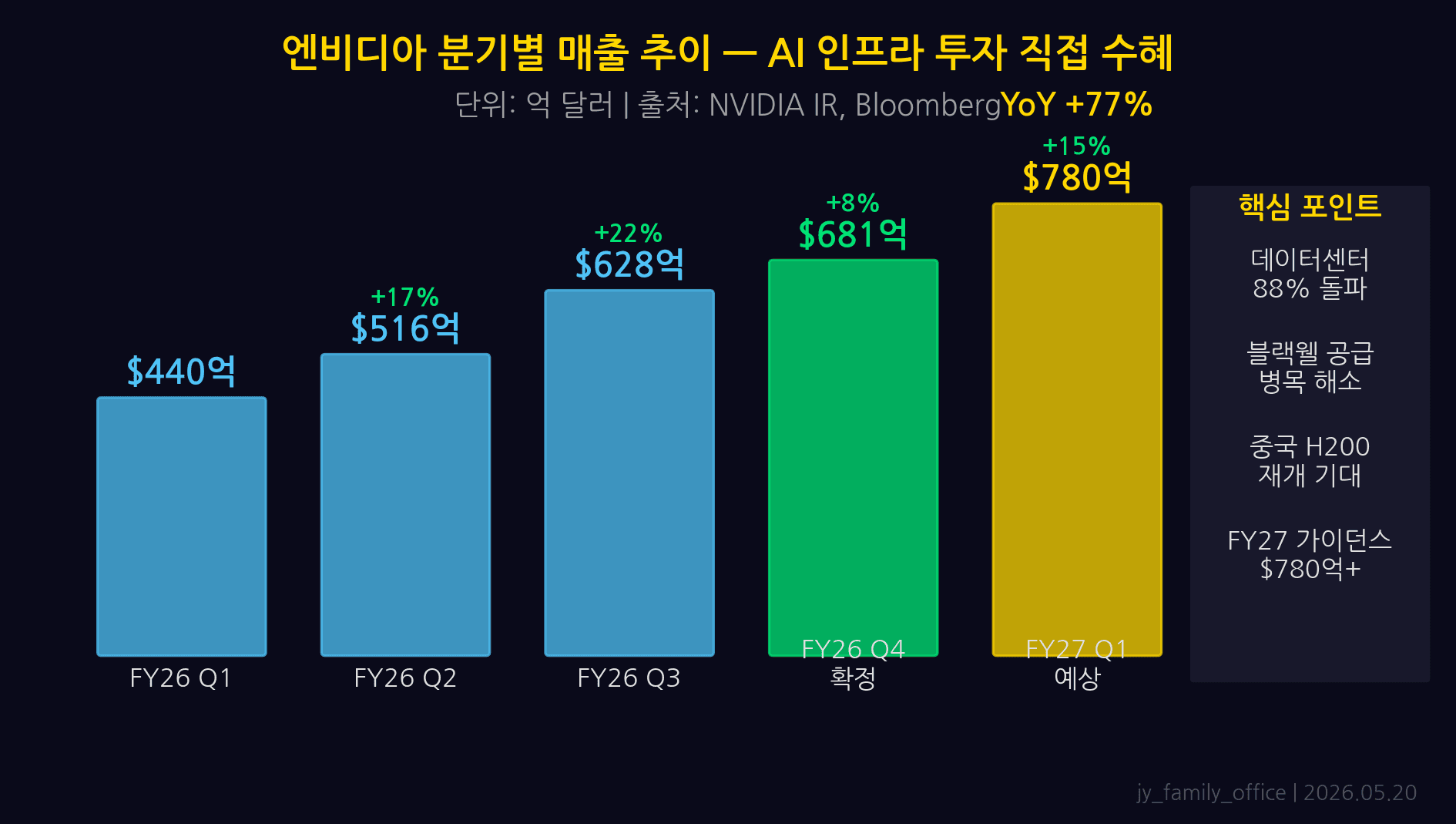

Nvidia has beaten Wall Street’s consensus estimate for eight consecutive quarters. The trajectory by the numbers:

- Q1 FY25: Revenue $26.0B (+10% vs. consensus), operating margin 66%

- Q2 FY25: Revenue $30.0B — data center strength despite Blackwell delays

- Q3 FY25: Revenue $35.1B — initial Blackwell shipments begin

- Q4 FY25: Revenue $39.3B (vs. consensus $37.6B, +4.5%)

- Q1 FY26 (tonight): Consensus $43.5B — surprise scenario targets $45–46B

Operating margins have held in the 65–68% range. With Big Tech’s AI infrastructure buildout accelerating across the board, Nvidia’s pricing power remains unmatched. The four hyperscalers — Meta, Microsoft, Google, and Amazon — are estimated to collectively spend roughly $300 billion on AI infrastructure in 2026, the overwhelming majority of which flows through Nvidia GPUs.

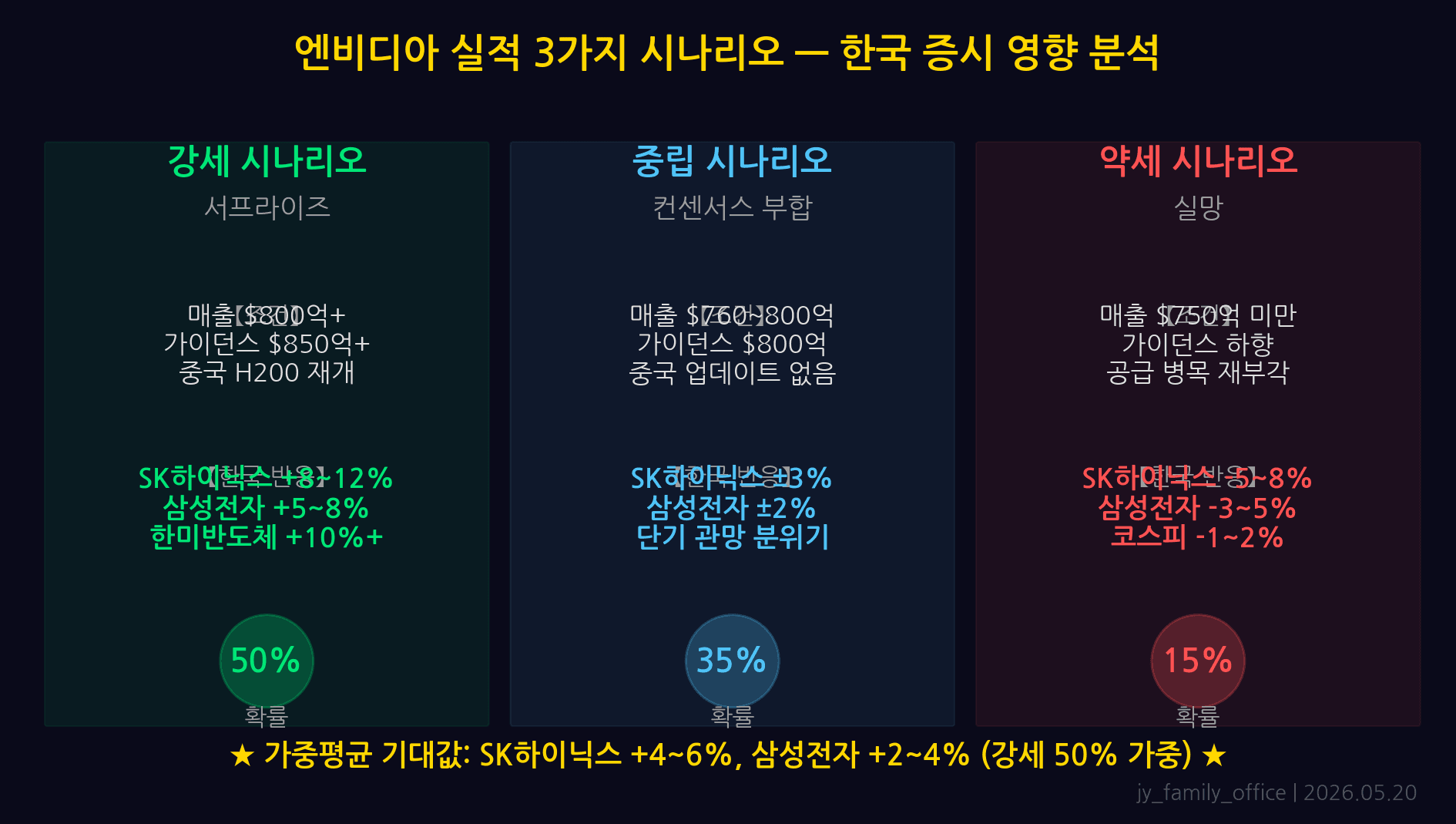

4. Three Scenarios — Probability and Market Reaction

The options market is currently pricing an earnings-day implied move of ±9% for NVDA. Our editorial team’s three-scenario framework:

-

Surprise Scenario (40% probability)

Conditions: Revenue $45B+ + Guidance above $46B + No Samsung HBM shift announcement

Expected reaction: NVDA +8–12%, SK Hynix +5–8%, Hanmi Semiconductor +6–10%

Likely gap up in after-hours, then continued gains at the open — watch for short-term overbought conditions -

In-Line Scenario (40% probability)

Conditions: Revenue $43–45B + Guidance around $46B

Expected reaction: NVDA ±2–3%, muted response from Korean beneficiaries

Classic “buy the rumor, sell the news” dynamic — profit-taking may weigh on the stock short-term -

Disappointment Scenario (20% probability)

Conditions: Revenue below $41B OR guidance below $44B OR Samsung HBM supply announcement

Expected reaction: NVDA -8–15%, SK Hynix -6–10%, Hanmi Semiconductor -10–15%

Mechanical stop-loss execution is essential — do not hold through stops

One critical asymmetry: even though the disappointment scenario carries the lowest probability, the downside magnitude tends to exceed the upside in a surprise. Hedging via put options or raising cash ahead of the print is a rational precaution.

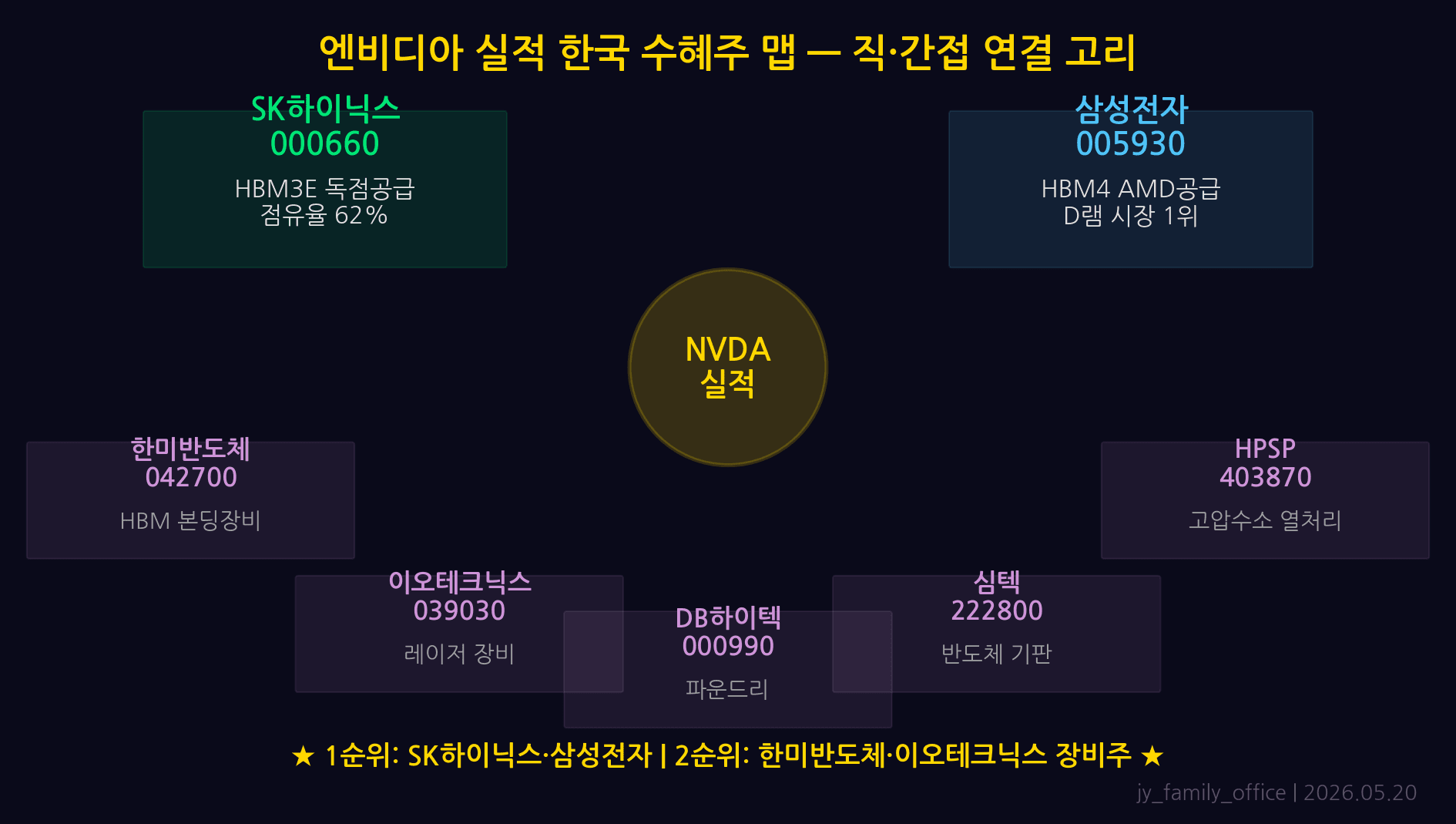

5. Beneficiary Map — Korea’s Semiconductor Ecosystem

An Nvidia earnings surprise ripples through Korea’s entire semiconductor supply chain. Here are the key names and the investment thesis for each:

- SK Hynix (KRX: 000660) — The dominant HBM3E supplier. Each new Nvidia data center GPU requires more HBM capacity than its predecessor. If SK Hynix secures HBM4 design wins, share gains could accelerate further. Top direct beneficiary.

- Hanmi Semiconductor (KRX: 042700) — Sole supplier of TC bonders (thermal compression bonders), the critical packaging equipment for HBM. More SK Hynix HBM volume = direct equipment order growth for Hanmi. Highest leverage play in the group.

- HPSP (KRX: 403870) — High-pressure hydrogen annealing equipment. Essential for improving HBM yield; supplies both SK Hynix and Samsung. Indirect beneficiary.

- Iotechvision (KRX: 039030) — Laser systems used in HBM stacking and dicing processes. Benefits from SK Hynix capacity expansion decisions.

- PSK (KRX: 319660) — Semiconductor cleaning and etching equipment. Gains from rising HBM process step counts, though more indirectly than the names above.

Note: in the disappointment scenario, all names above are likely to fall together. Hanmi Semiconductor carries the highest volatility given its direct HBM cycle exposure.

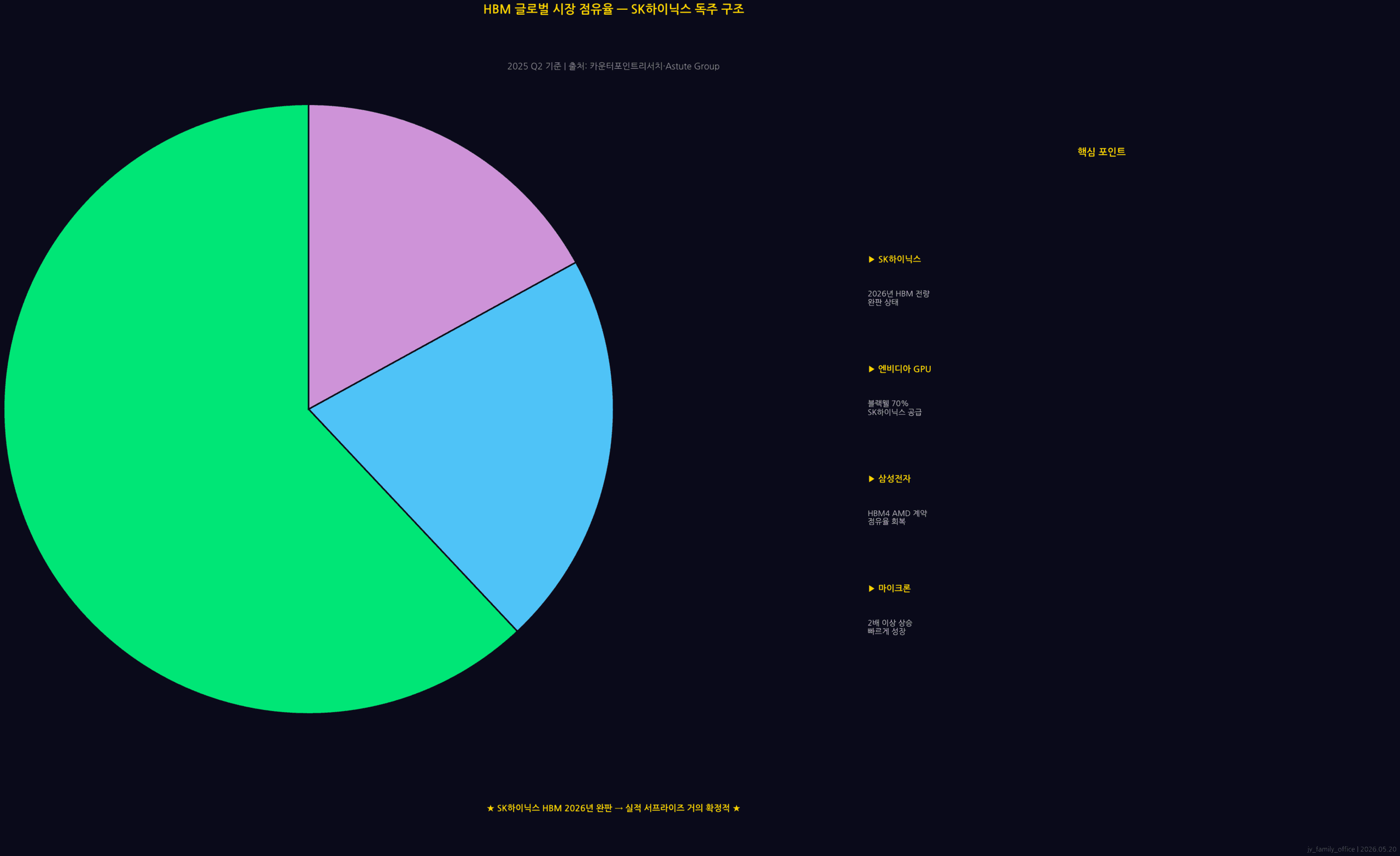

6. HBM Market Share — SK Hynix’s Structural Moat

SK Hynix’s position in the HBM (High Bandwidth Memory) market goes well beyond a simple No. 1 ranking. At over 70% market share, it represents a structural oligopoly. The company is effectively the sole supplier of HBM3E for Nvidia’s H100, H200, and B200 GPUs.

Samsung Electronics has not yet fully passed HBM3E quality certification with Nvidia. Micron holds less than 20% share, servicing primarily non-Nvidia customers. The market expects SK Hynix to maintain its lead in next-generation HBM4 (mass production targeted H2 2026) as well.

There is essentially one scenario that could shake this structural moat: Jensen Huang directly announcing “Samsung HBM supply expansion” on tonight’s conference call. That is precisely why Checkpoint 3 is so important.

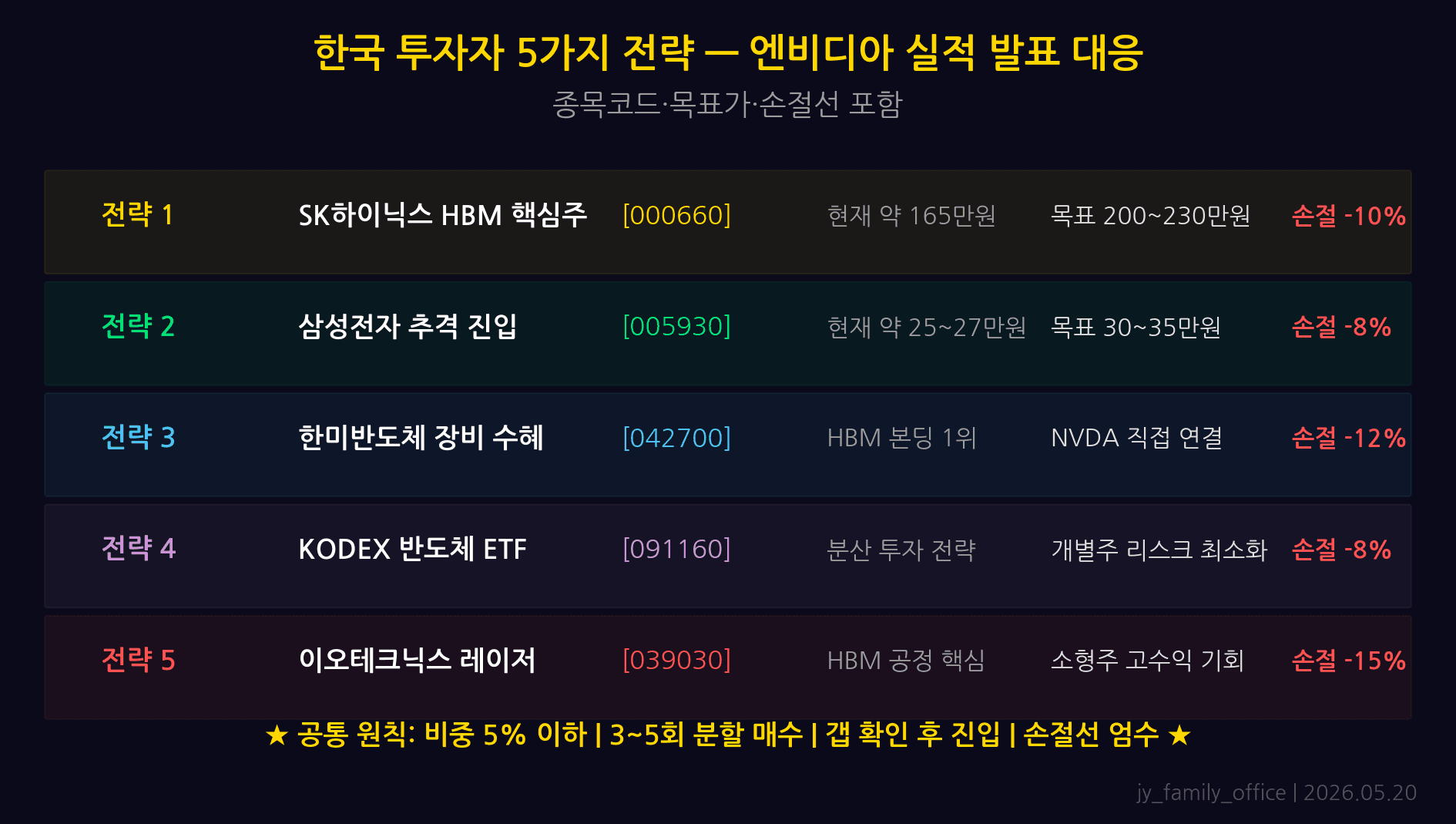

7. Five Strategies for Korean Investors — With Stop-Loss Levels

These five principles are recommended for navigating the earnings event:

-

Pre-earnings: Hold existing SK Hynix positions

Within a consensus-range outcome, SK Hynix remains the lowest-risk beneficiary. Selling ahead of the print is unnecessary profit realization. New entries, however, are better initiated after the result is confirmed. -

Post-surprise: Add to Hanmi Semiconductor

If Data Center revenue exceeds $40B and guidance clears $46B+, increase Hanmi Semiconductor weight by 10–15 percentage points from current allocation. TC bonder order momentum is likely to be reflected immediately in share price. -

Disappointment scenario: Apply SK Hynix stop-loss at KRW 1.4 million mechanically

This represents roughly -8–10% from current levels. Execute the stop without hesitation and observe for a re-entry opportunity — emotional overrides are the most common source of loss in earnings-event trading. -

NVDA direct buy: Only after confirming a gap up post-earnings

Entering NVDA fresh ahead of earnings is high-risk. The valid tactical entry is on a pullback from the opening gap, after after-hours trading confirms a +5% or better move. -

Maintain 20% cash reserve at all times

Regardless of scenario outcome, keep 20% of the portfolio in cash. This is dry powder for buying the dip in the disappointment scenario — and discipline insurance against chasing in the surprise scenario.

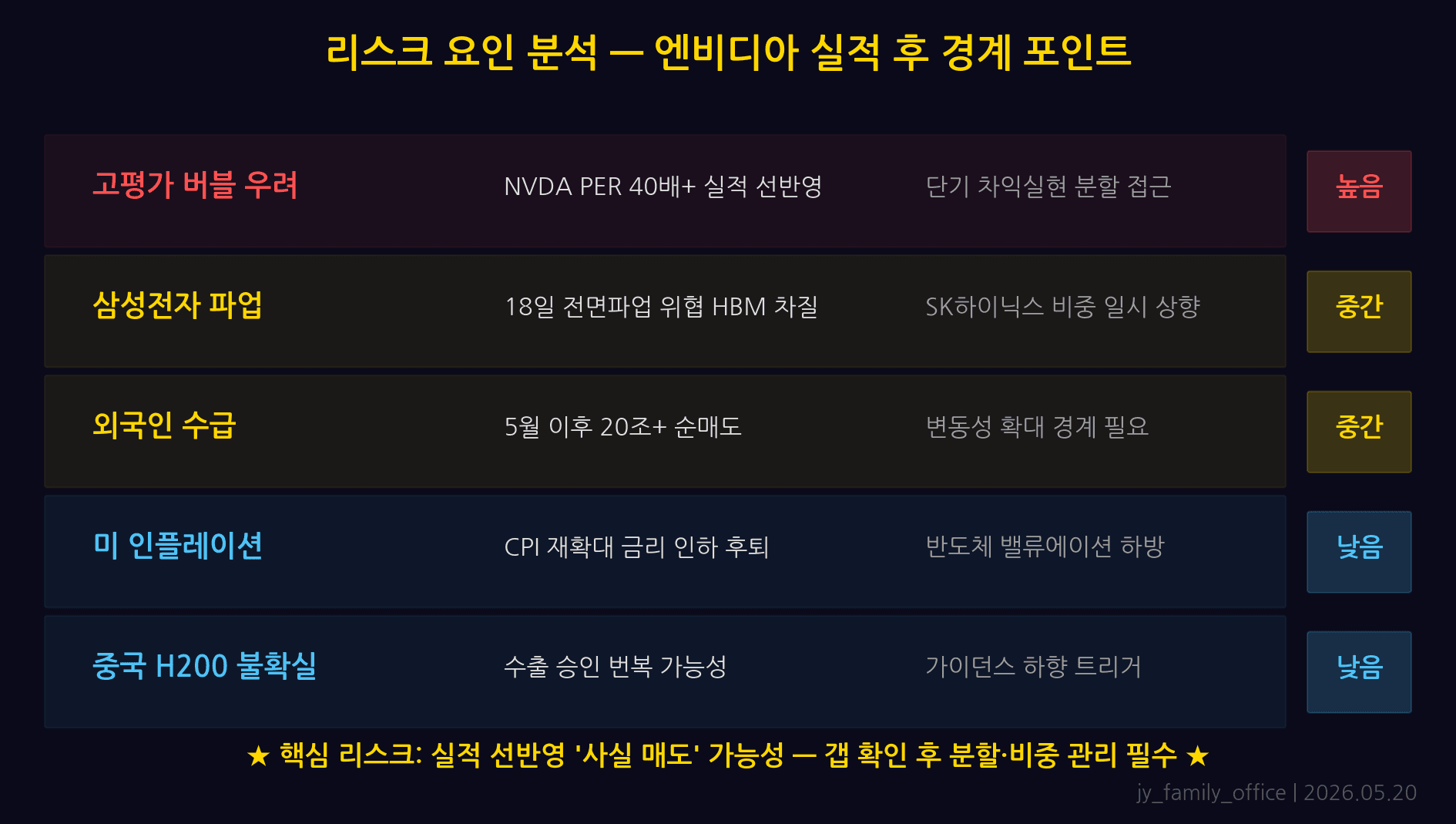

8. Five Risks — The Variables Most Investors Miss

Strong headline numbers are no guarantee of a strong stock price reaction. These five risks require explicit monitoring:

- Conservative guidance — Even if reported revenue beats, guidance at or below $45B will trigger “peak growth” concerns and selling pressure. “Strong print, weak guide” is a recurring Nvidia pattern that has caused sharp post-earnings drops before.

- China export restriction commentary — If the call includes references to tightened restrictions on H20 or new export controls, the market will reprice the China revenue contribution (estimated $3–4B) downward immediately.

- Samsung HBM supply shift announcement — As noted above, the single most impactful possible statement for SK Hynix. Watch for it in the supply chain section of the call.

- Currency risk — A surprise outcome typically strengthens the dollar and weakens the Korean won (KRW). However, in a disappointment-driven risk-off environment, won weakness could push up import prices and create secondary pressures. Check hedging status on any USD-denominated holdings.

- After-hours volatility trap — A spike in after-hours trading followed by a gap fill at the regular session open is a well-established pattern with Nvidia. Chasing after-hours highs is one of the most consistent ways to lose money on an earnings trade.

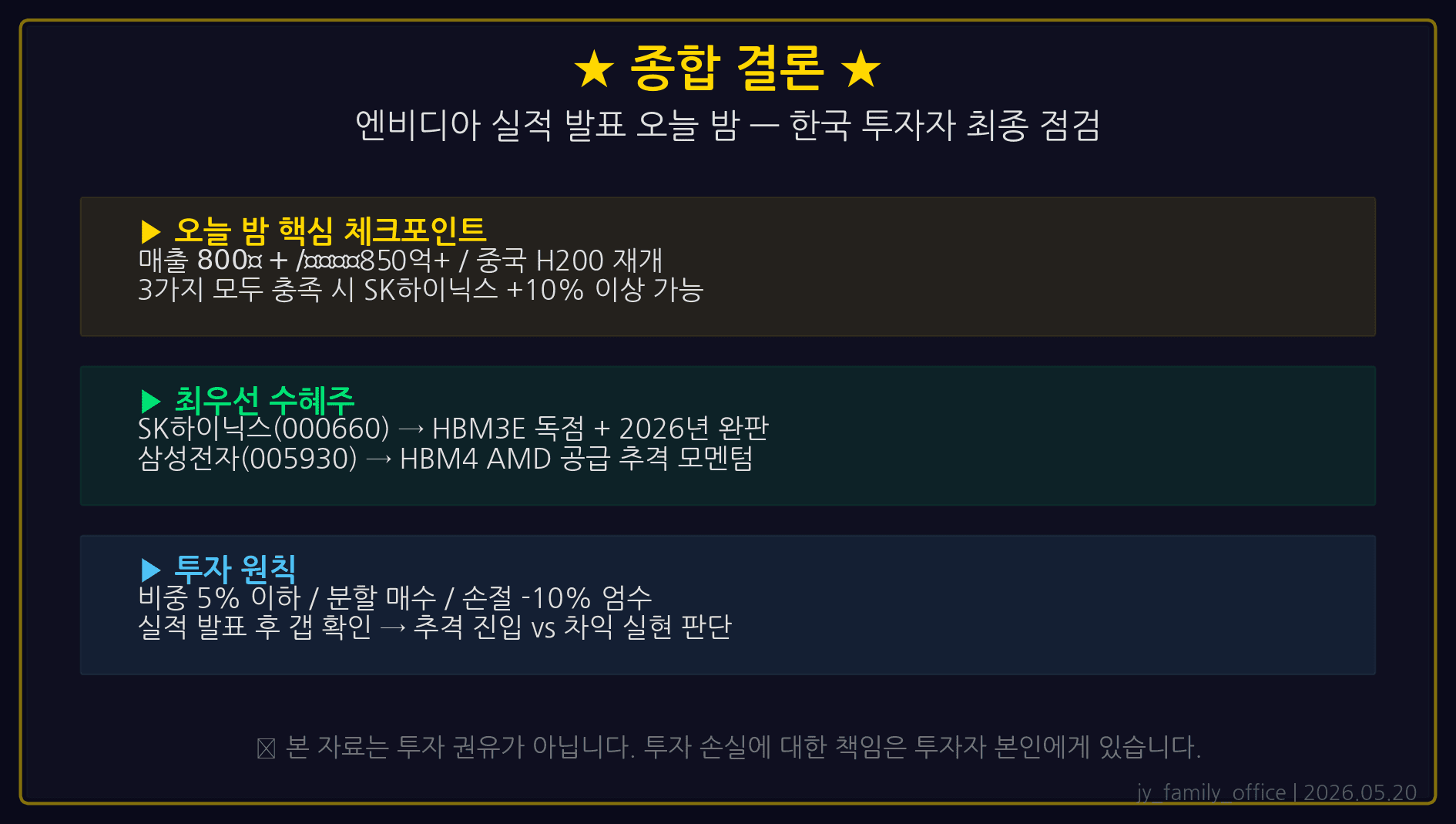

9. Bottom Line — Tonight’s Checklist

Our editorial team’s base case is the Surprise scenario at 40% probability. Continued strength in Blackwell demand, sustained Big Tech AI investment, and stabilized HBM3E supply dynamics collectively point toward another consensus beat. But even on that foundation, risk management is what converts a correct call into realized profit.

At 9:30 AM KST on May 21, the moment the results are released, check these three items in sequence:

- Data Center revenue figure → confirm whether it exceeds $38B

- Guidance number → $46B+ confirms the surprise scenario

- Key conference call statements → capture any mention of HBM supplier changes

SK Hynix remains the safest and most essential core holding among Korean beneficiaries. Applying the KRW 1.4 million stop-loss in a disappointment scenario, adding Hanmi Semiconductor on a confirmed surprise, and keeping 20% cash in reserve at all times is the optimal positioning for this earnings season. Discipline on the cash reserve applies under every outcome.