2026 Korea Tax Reform: 7 Key Changes — Dividend Separate Tax, ISA Expansion, Securities Transaction Tax Return, Rental Income 1.2B

Breaking News · May 17, 2026

2026 Korea tax reform is a watershed moment for investors, business owners, and landlords alike. Seven major changes — from dividend separate taxation and ISA overhaul to the abolition of the financial investment income tax — reshape the tax landscape starting this year. Here is everything you need to know in one place.

2026 Korea Tax Reform: 7 Changes at a Glance

The South Korean government has overhauled the tax code to simultaneously boost financial investment and improve tax equity. The seven changes below take effect in 2026 and have immediate implications for individuals and businesses.

- ① Dividend separate taxation introduced

- ② ISA non-taxable limit expanded + 9.9% preferential tax

- ③ Securities transaction tax restored to 0.20%

- ④ Financial Investment Income Tax (FIIT) officially abolished

- ⑤ Rental income threshold set at assessed value KRW 1.2 billion

- ⑥ False invoice penalty raised from 3% to 4%

- ⑦ Business account mandate + company car insurance requirement

① Dividend Separate Taxation — High-Yield Investors Get a Break

Previously, dividend income was aggregated with other income and could be taxed at up to 49.5% (including local income tax) under the global income tax system. Starting 2026, taxpayers can elect separate taxation, meaning dividend income is taxed at a flat rate without being combined with other income.

This is especially advantageous for high-dividend investors and those whose financial income exceeds the KRW 20 million threshold for global income taxation. Taxpayers in the top bracket (taxable income over KRW 1 billion, 45% rate) stand to benefit the most. However, electing separate taxation generally forecloses refunds of withheld taxes, so individual circumstances must be assessed carefully.

Dividend separate taxation is not about paying less tax — it’s about choosing the rate structure that fits your income profile.

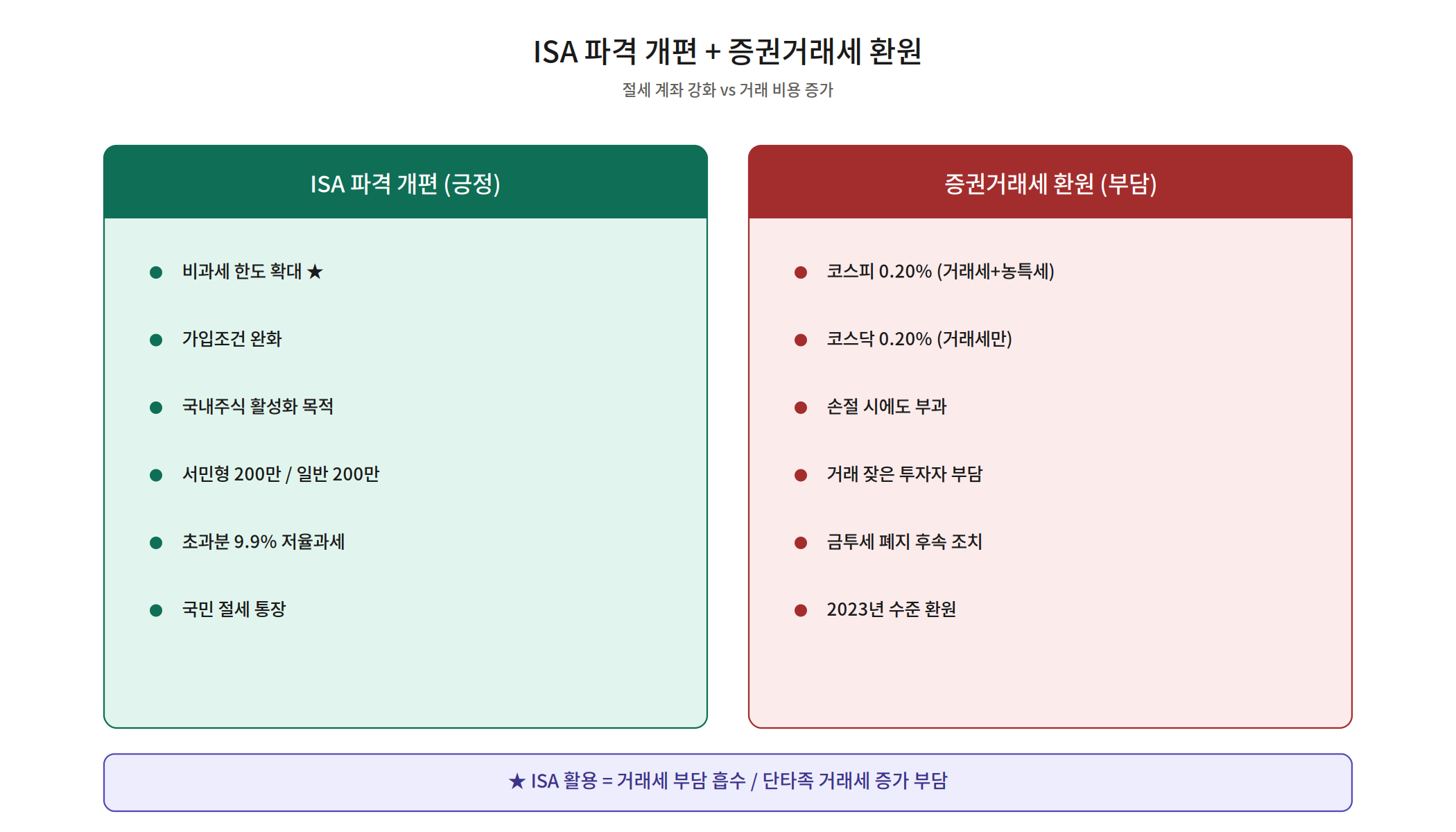

② ISA Overhaul — Bigger Non-Taxable Limit + 9.9% Preferential Tax

The Individual Savings Account (ISA) scheme receives a major upgrade in 2026. Two key improvements stand out:

- Expanded non-taxable limit: Raised above the previous KRW 2 million (KRW 4 million for low-income earners)

- 9.9% separate tax on gains above the limit: Instead of global income tax rates, excess returns are taxed at a preferential 9.9% flat rate

Investors who hold stocks, funds, bonds, and deposits all in one ISA account can now maximize tax savings with greater flexibility. If you do not yet have an ISA, opening one now is strongly advisable. ISA-related deduction details are available on the National Tax Service Hometax portal.

③ Securities Transaction Tax Restored + ④ FIIT Abolished

After a phased reduction in 2024–2025, the securities transaction tax returns to 0.20% for both KOSPI and KOSDAQ in 2026. Simultaneously, after years of debate, the Financial Investment Income Tax (FIIT) has been officially abolished before it ever took effect. FIIT would have taxed stock, bond, and fund gains exceeding KRW 50 million at 22–27.5%.

Frequent traders will see slightly higher transaction costs due to the restored securities tax. Long-term investors, on the other hand, benefit from the elimination of FIIT risk on large gains. Taken together, the two changes favor a buy-and-hold strategy over active trading.

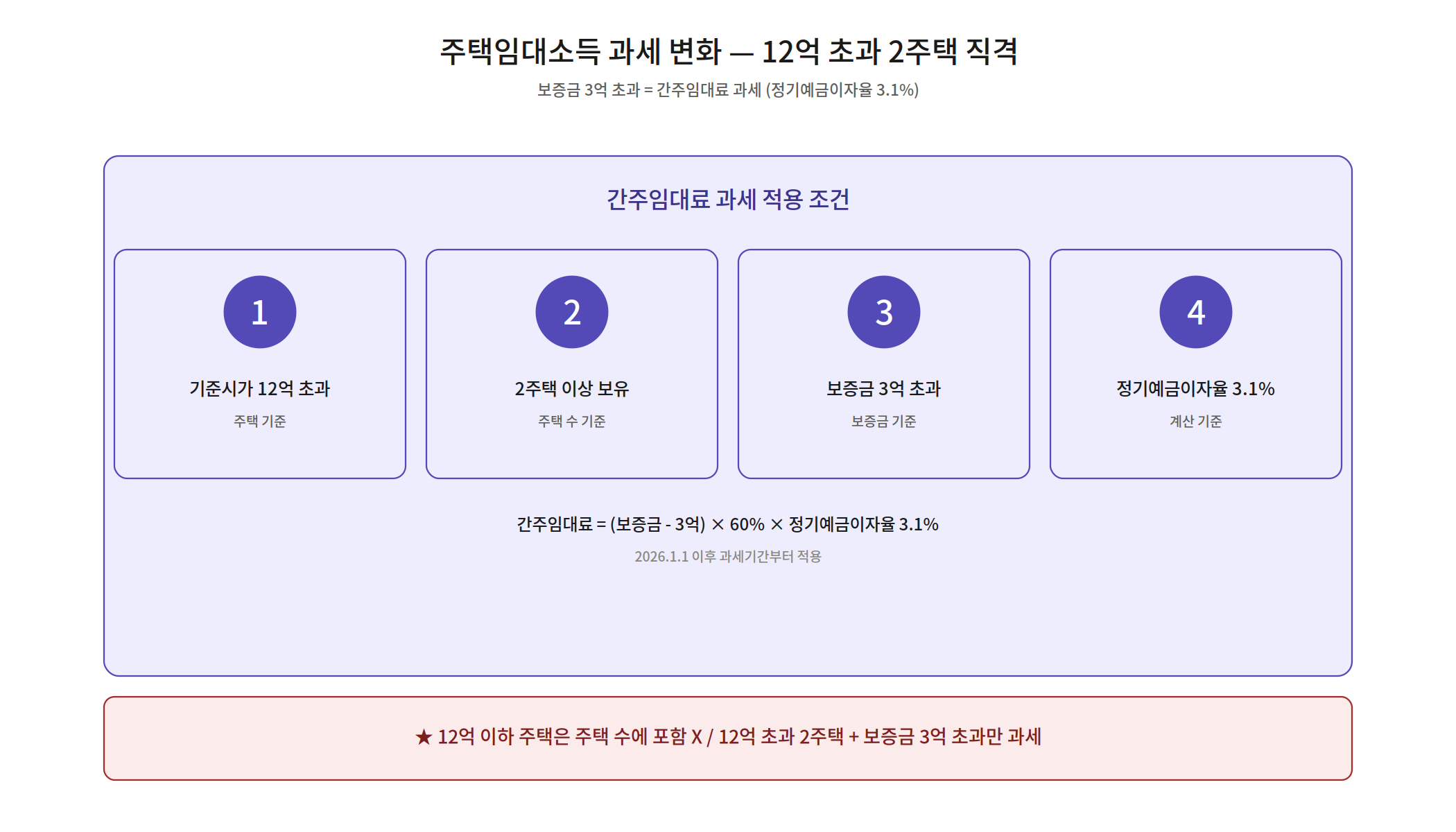

⑤ Rental Income — The KRW 1.2 Billion Threshold That Changes Everything

From 2026, landlords who own two or more homes with an assessed value exceeding KRW 1.2 billion and hold deposits totaling more than KRW 300 million will be subject to deemed rental income taxation. The formula is:

Deemed Rental Income = (Total Deposit − KRW 300M) × 60% × 3.1%For example, if total deposits amount to KRW 800 million: (800M − 300M) × 60% × 3.1% = approximately KRW 930,000 is treated as taxable deemed rental income. Critically, this applies even without collecting monthly rent — a jeonse (lump-sum deposit) arrangement alone can now trigger a tax liability. Landlords must verify the assessed values of their properties immediately.

⑥⑦ Business Owner Rules — False Invoice 4%, Mandatory Accounts & Insurance

Business owners face a tighter regulatory environment in 2026 across six areas:

- False invoice penalty raised to 4%: Issuing or receiving fraudulent tax invoices now triggers a penalty equal to 4% of the supply value (up from 3%). Deliberate tax evasion carries additional criminal exposure.

- Mandatory business account: Businesses required to maintain double-entry bookkeeping must process all revenue and expenses through a designated business bank account. Non-compliance triggers a 0.2% surcharge on gross revenue.

- Business car insurance mandate: Businesses operating two or more company cars must carry business-exclusive auto insurance for those vehicles to deduct related expenses. Uninsured vehicles lose all associated deductions.

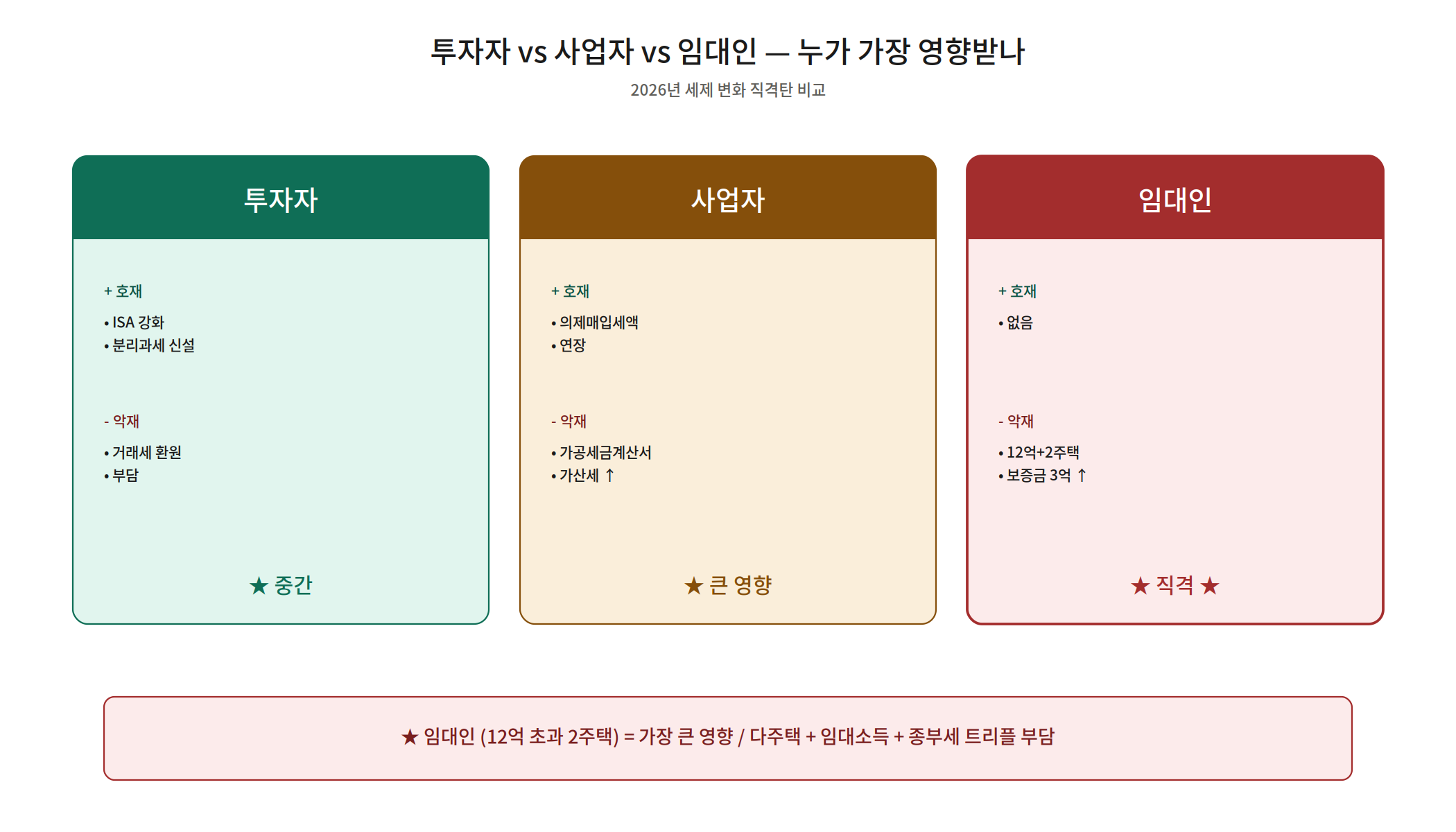

Who Is Affected Most? Investors vs. Business Owners vs. Landlords

| Group | Positive Changes | Negative Changes |

|---|---|---|

| Investors | FIIT abolished, ISA upgrade, dividend tax election | Securities tax restored to 0.20% (higher short-term costs) |

| Business owners | None | 4% false invoice penalty, account mandate, car insurance rule |

| Landlords | None | KRW 1.2B threshold — deemed rental income on jeonse deposits |

Landlords face the most direct hit. Those holding two high-value properties on jeonse contracts may owe income tax even without a single won of monthly rent. Investors, by contrast, gain new tools for tax optimization through the combination of FIIT abolition and ISA expansion.

5 Action Strategies + 3 Scenarios

Five strategies to act on now:

- Open an ISA account immediately — maximize the expanded non-taxable allowance.

- Run a dividend tax simulation — calculate whether global income tax or separate taxation is more favorable for your situation.

- Review deposit terms — landlords should consider whether restructuring jeonse deposits below KRW 300 million is feasible.

- Separate business accounts — double-entry bookkeeping businesses should segregate accounts now to avoid the 0.2% surcharge.

- Audit company car insurance — verify coverage for all business vehicles to protect your deduction eligibility.

Three scenarios:

- High-dividend investor: Elect dividend separate taxation + maximize ISA for a significantly lower effective tax rate.

- Two-home landlord: Check assessed values, then adjust deposit terms or consider a sale strategy before year-end.

- Self-employed / SME owner: Eliminate false invoice risk, segregate accounts, and secure business car insurance immediately.

Conclusion — The 2026 Korea Tax Reform Window Is Open Now

The 2026 Korea tax reform moves in two simultaneous directions: expanding choice for investors while tightening compliance requirements for business owners and landlords. Long-term investors benefit from the FIIT abolition and ISA upgrade; landlords and businesses must navigate new obligations and higher penalties.

Tax planning done early translates directly into savings. Review your asset structure and business setup today — and consult a licensed tax advisor if needed. Official guidance is available on the National Tax Service English portal (nts.go.kr).