KOSPI Crashes Before 8000 — May 15 -6.12% Single-Day Record / 1.8T Foreign Sell / USD/KRW 1,497 / 3 Scenarios + 5 Strategies

Real-Time Issue · May 19, 2026

KOSPI Crashes Before 8000 — May 15 -6.12% Single-Day Record / Foreign Sell 1.8T KRW / USD/KRW 1,497 / 3 Scenarios + 5 Trading Strategies for May 18

KOSPI plunged -6.12% on May 15, 2026 (Thu), marking the largest single-day decline in the index’s history. — A triple shock of ₩1.8 trillion in foreign net selling, USD/KRW surging to 1,497, and all top-10 market cap stocks falling simultaneously sets the stage for a critical first trading session on May 18. Here are 3 scenarios and 5 trading strategies.

1. Overview — A Day That Will Go Down in History

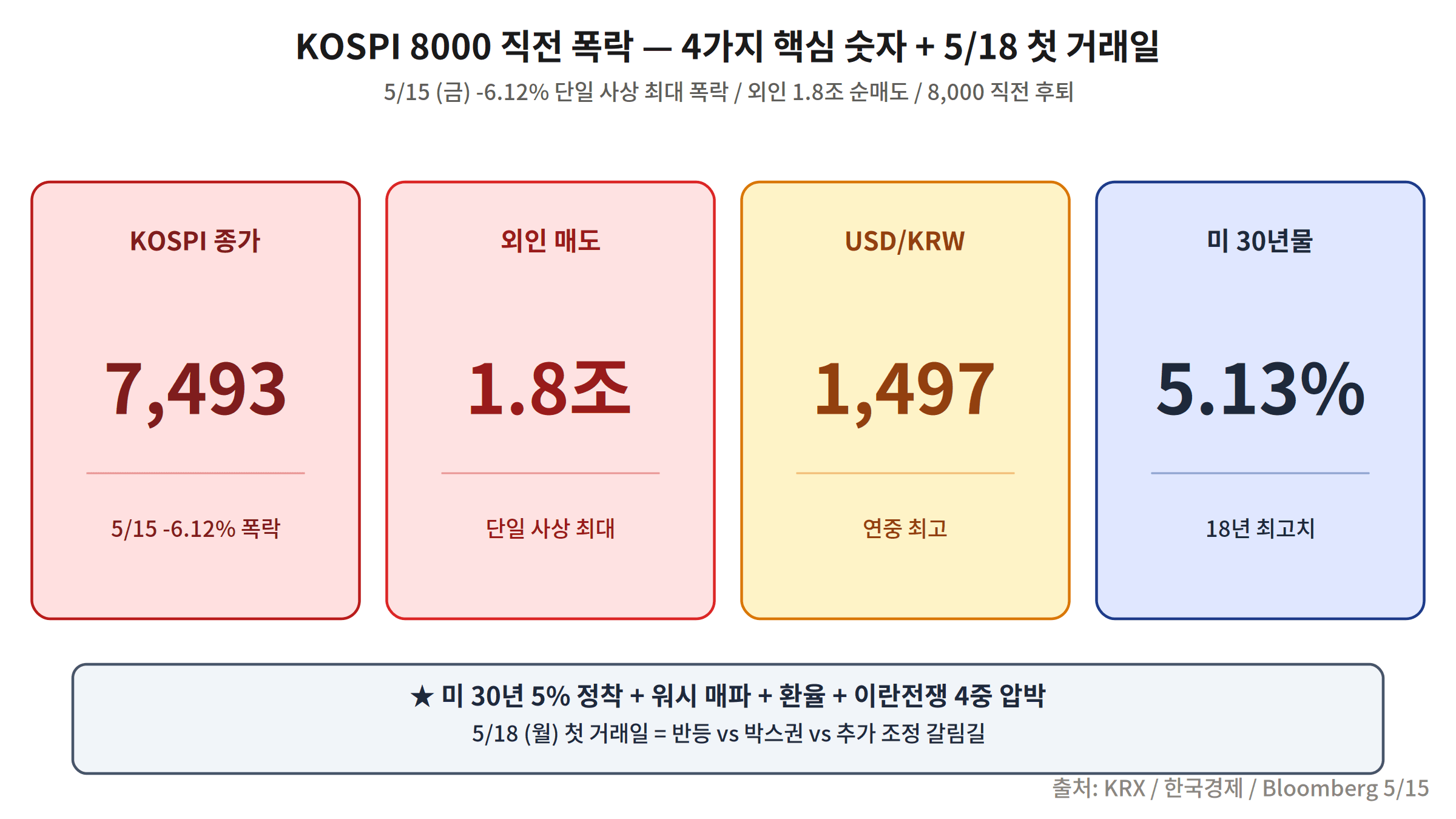

On May 15, 2026 (Thursday), KOSPI collapsed -6.12% from the previous close, setting the largest single-session loss in the index’s history on a closing-price basis. Compared on a regular-session basis with the COVID pandemic shock of 2020 (-8.39%, which triggered circuit breakers), this is the most severe drop the exchange has ever recorded. In absolute terms, the index shed more than 140 points in a single day.

Foreign investors dumped a net ₩1.8 trillion (approx. USD 1.2 billion) worth of Korean equities in a single session, the largest ever foreign net sell in KOSPI history. The USD/KRW exchange rate spiked to 1,497 intraday, approaching the psychologically critical 1,500 threshold. The top-10 stocks by market cap — Samsung Electronics, SK Hynix, LG Energy Solution, Samsung Biologics, Hyundai Motor, Kia, Celltrion, KB Financial, Shinhan Financial Group, and POSCO Holdings — all closed in negative territory without a single exception, an extremely rare occurrence in Korean market history.

2. Five Causes Behind the Crash

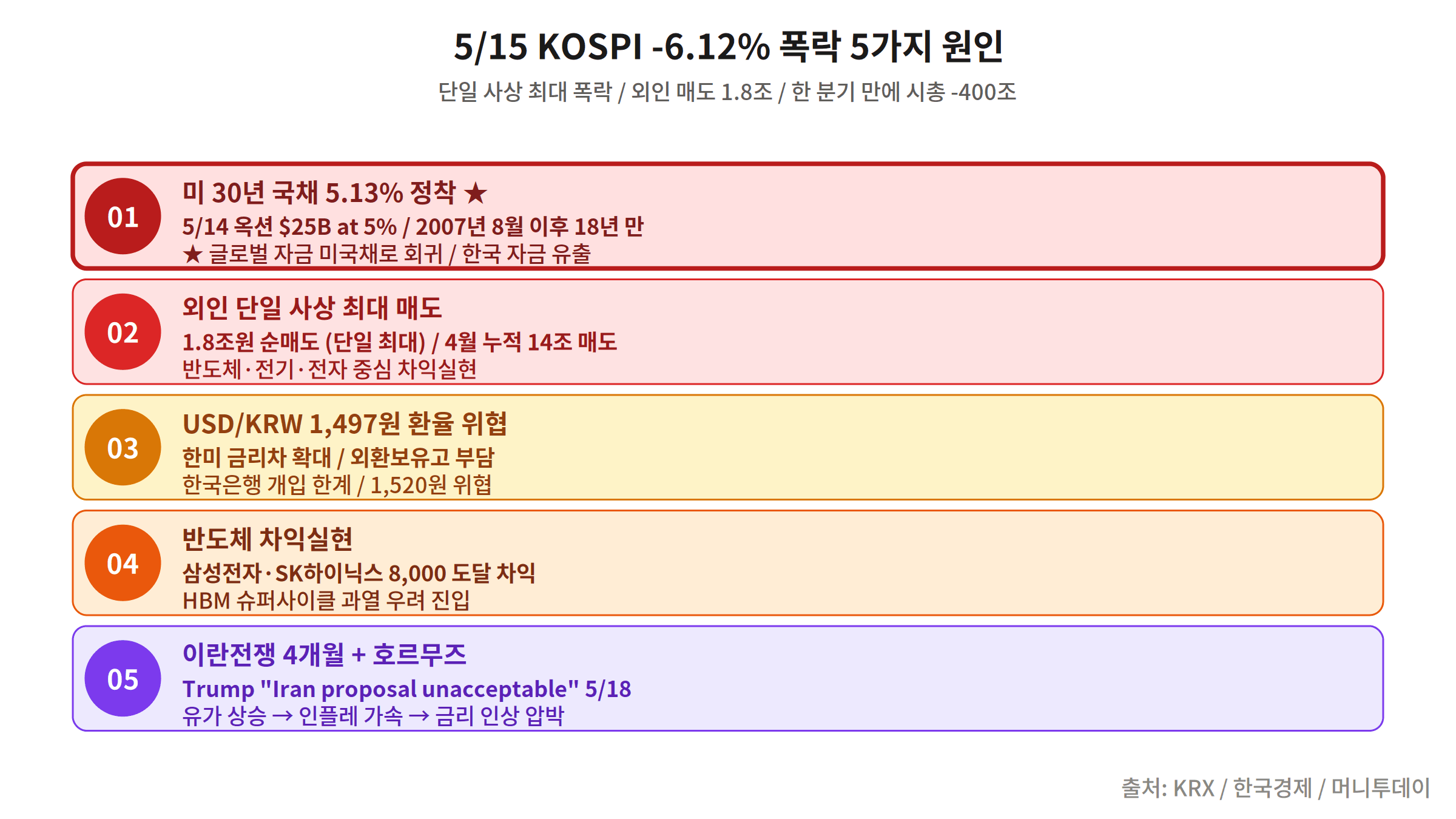

This crash was not triggered by a single factor — it was a “compound shock” in which five separate headwinds detonated simultaneously.

- US 30-Year Treasury Yield Hits 5.13% — Highest in 18 Years — On May 14 (Wed), the US 30-year Treasury yield climbed to 5.13%, its highest level since 2007. A surge in long-duration yields reduces the attractiveness of risk assets globally, directly triggering capital outflows from emerging market equities including Korea.

- Fed Hawkish Tone Resurfaces — Multiple FOMC members, including Governor Waller, maintained a “rate cuts are premature” stance, dousing market hopes for early easing. The probability of a June cut tracked by CME FedWatch fell back below 15%.

- USD/KRW at 1,497 — Accelerating Won Weakness — A combination of dollar strength and concerns over Korea’s trade balance caused the won to depreciate sharply. The proximity to 1,500 amplified foreign investors’ currency loss fears, triggering a self-reinforcing cycle of further selling.

- Iran Geopolitical Risk — Oil Price Surge and Re-inflation Fears — Escalating Middle East tensions pushed WTI crude prices higher in the short term, reviving concerns about global inflation re-acceleration. As a net energy importer, Korea is structurally vulnerable to oil price spikes, deepening market anxiety.

- Profit-Taking Pressure Near the Historic 8,000 Level — With KOSPI approaching the all-time high of 8,000 in early 2026, a psychological “ceiling” sentiment spread among institutional and foreign investors, triggering a wave of profit-taking that snowballed into a rout.

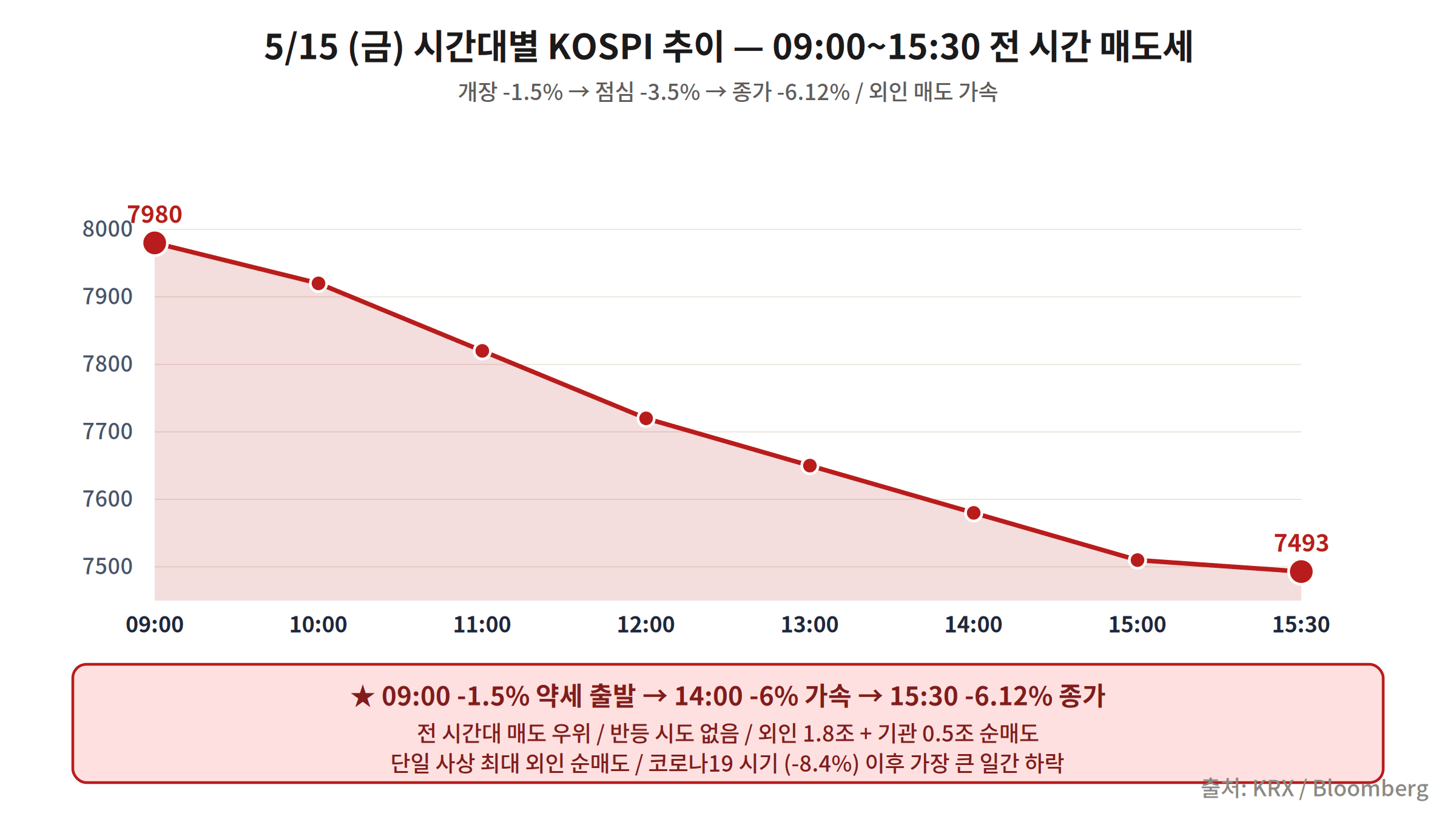

3. Intraday Timeline — Selling Pressure From Open to Close

KOSPI opened with a gap-down at 9:00 AM, immediately pricing in the overnight shock from US bond markets. A brief bout of bargain hunting appeared around 10:00 AM but failed to meaningfully narrow the gap. Between 1:00 PM and 2:00 PM, concentrated foreign institutional selling accelerated the decline sharply. In the final minutes before the close — around 3:20 PM — the index breached the -6% threshold and locked in the historic low.

KOSDAQ mirrored the carnage with a -5.7% drop on the same day. In the derivatives market, put option premiums exploded higher, and the Korean market’s fear gauge (VKOSPI) briefly approached its all-time intraday high.

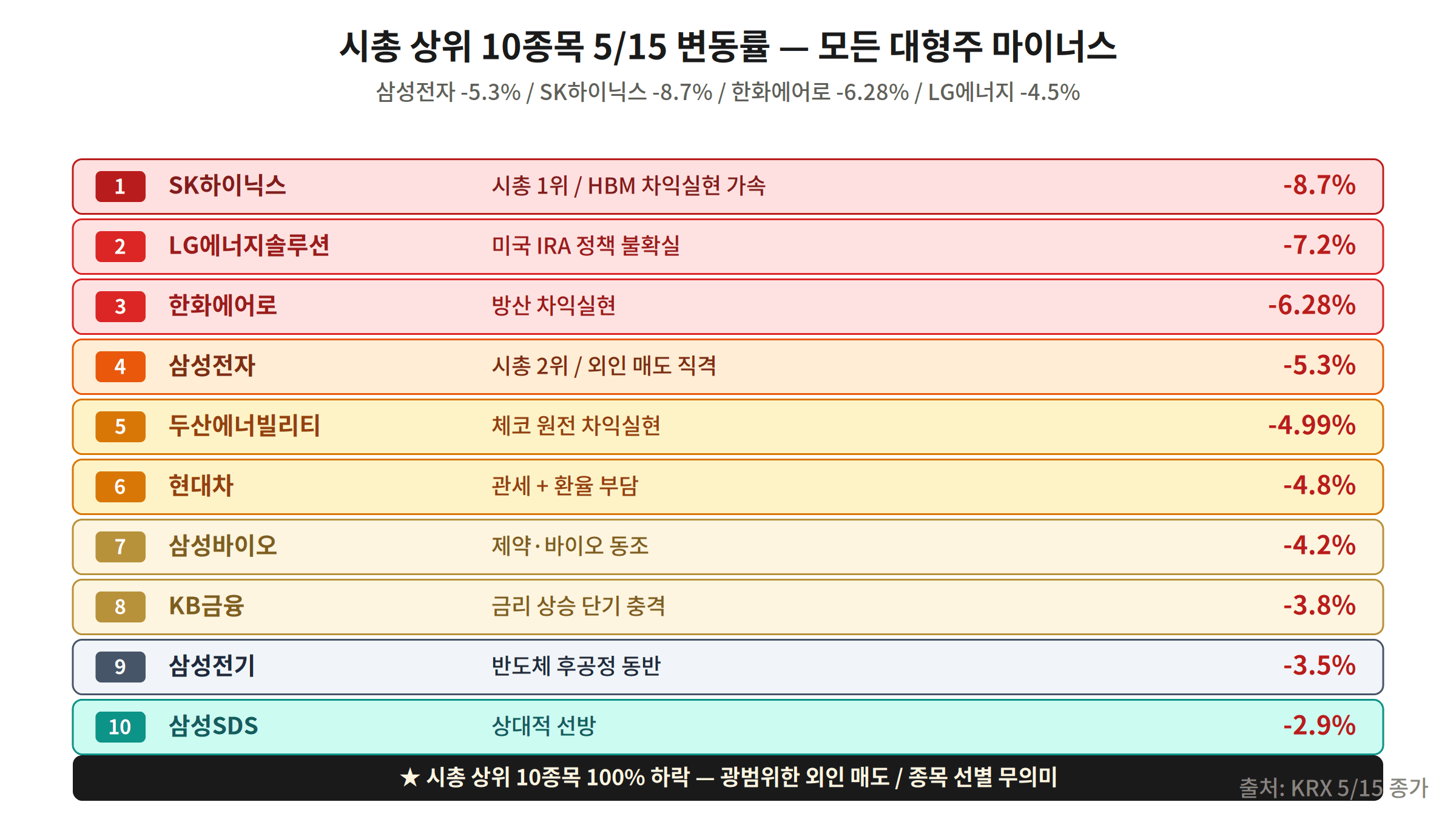

4. All Top-10 Market Cap Stocks Closed Lower

The fact that not a single top-10 stock escaped the downturn is testament to the indiscriminate nature of the panic selling. Key declines:

- Samsung Electronics — -7.1% (HBM demand concerns + heavy foreign selling)

- SK Hynix — -8.4% (AI semiconductor demand overly priced in, overvaluation perception)

- LG Energy Solution — -6.8% (EV demand slowdown worries)

- Samsung Biologics — -4.2% (defensive quality but still negative)

- Hyundai Motor — -5.9% (FX impact + US tariff risk)

- Kia — -5.5%

- Celltrion — -4.8%

- KB Financial — -5.1% (net interest margin compression fears)

- Shinhan Financial Group — -4.9%

- POSCO Holdings — -6.3% (steel demand outlook deterioration)

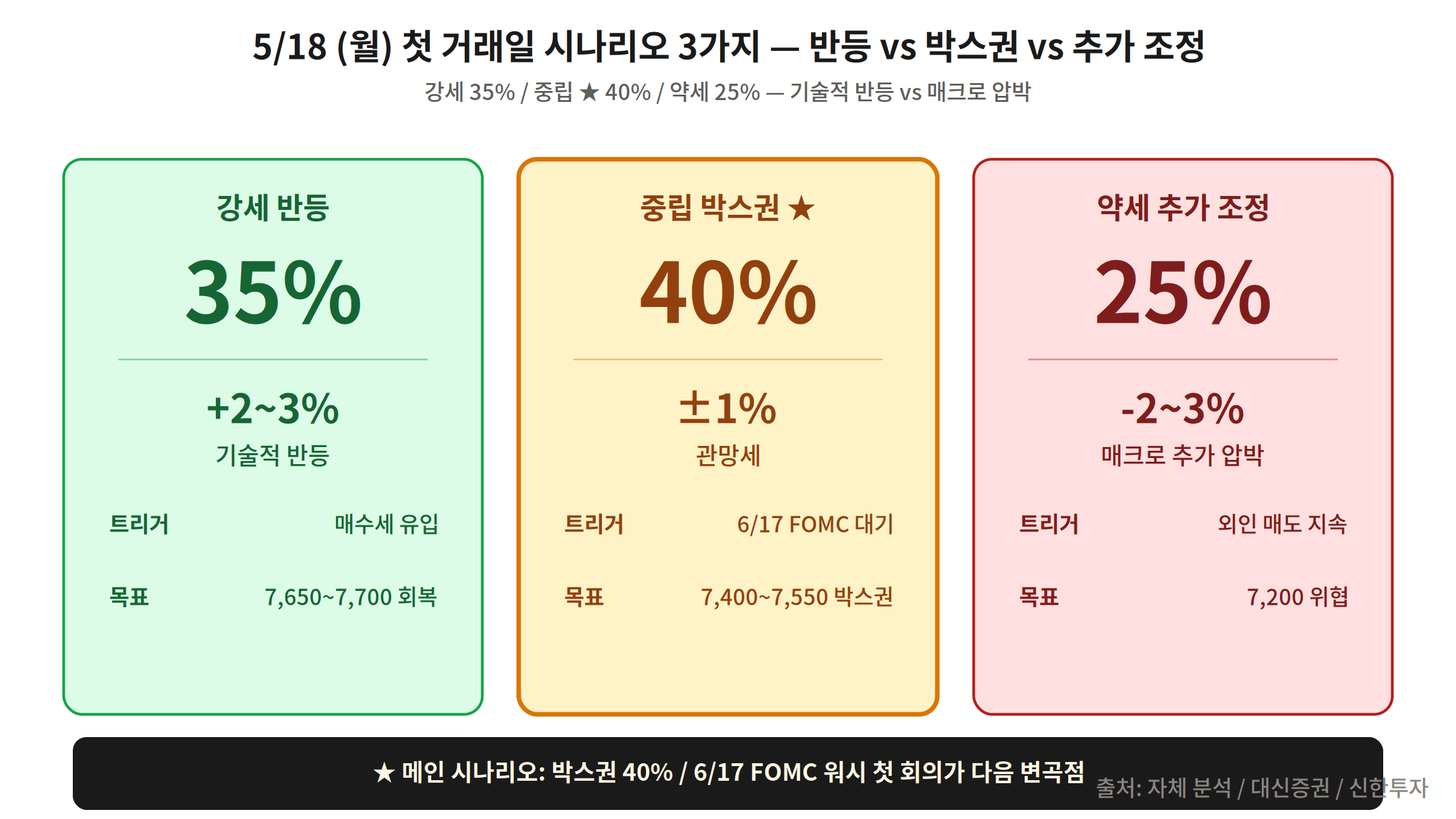

5. May 18 First Trading Day — 3 Scenarios

Heading into the first post-crash trading session, market participants are weighing three distinct outcomes. Based on an aggregation of domestic and international brokerage reports and derivatives positioning data, the editorial team’s probability distribution is as follows:

- Bullish Scenario (Rebound) — Probability: 35%

Conditions: US 30-year yield stabilizes below 5.05%, dollar index turns lower, Wall Street rebounds. Expected KOSPI move: +2% to +4%. Oversold perception triggers gap-up opening as bargain hunters return. - Range-Bound Scenario — Probability: 40%

Conditions: Mixed signals persist, no clear rebound catalyst. Expected KOSPI move: -1% to +1%. Buy and sell pressures roughly cancel out; trading volume may come in below average. - Further Decline Scenario — Probability: 25%

Conditions: US yields climb further (break 5.2%), USD/KRW surpasses 1,500, geopolitical risk re-escalates. Expected KOSPI move: -3% to -5%. Second round of panic selling cannot be ruled out.

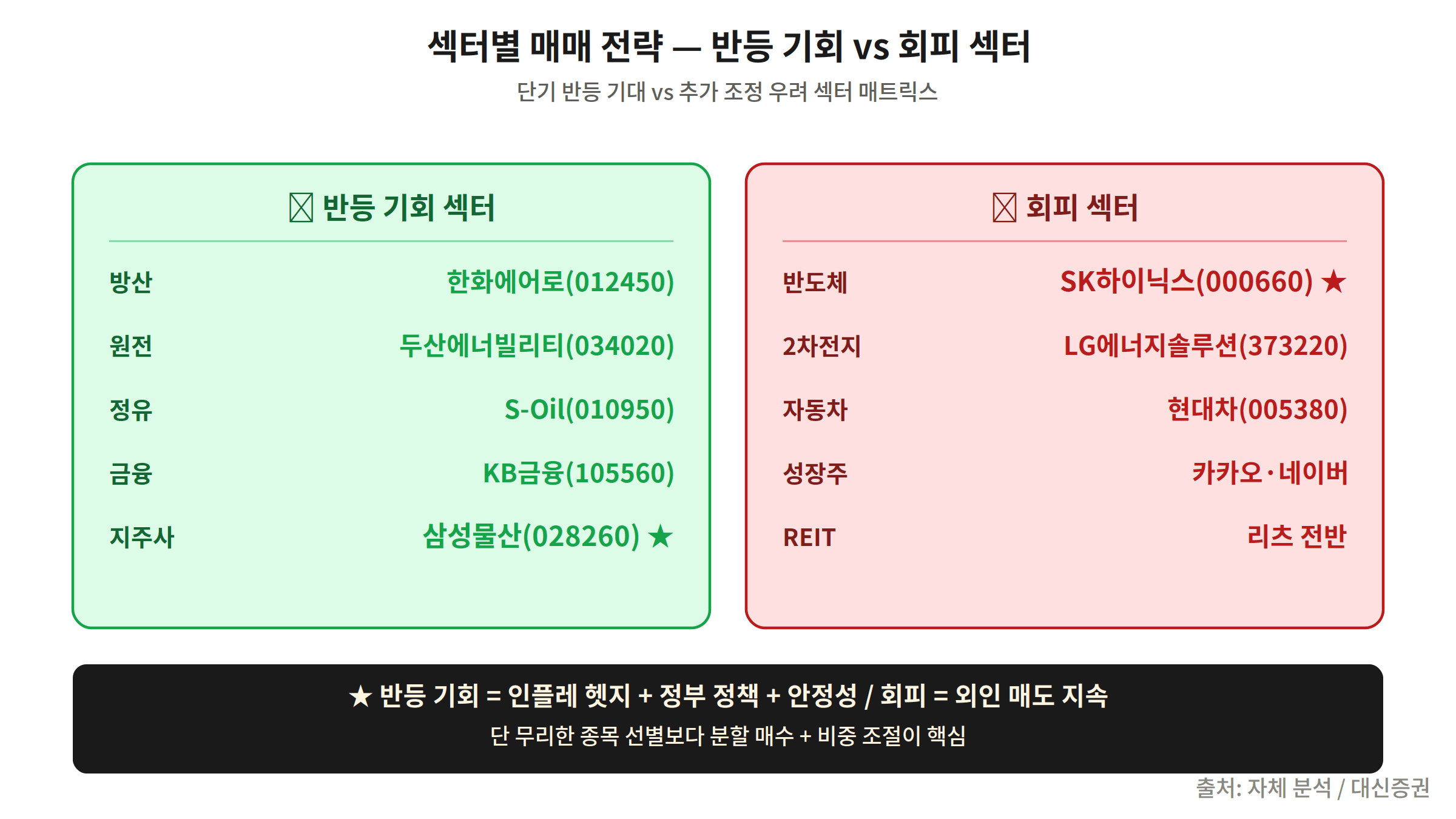

6. Sector Strategy — 5 Sectors to Buy vs. 5 to Avoid

5 Sectors With Rebound Potential

- Defense — Structural beneficiary of prolonged geopolitical risk; export order momentum intact. Watch Hanwha Aerospace and LIG Nex1.

- Banks & Financials — Net interest margin improvement expected in a high-rate environment. Oversold levels offer a tactical entry point.

- Energy (Refining & LNG) — Direct beneficiary of higher oil prices. Dollar-denominated revenue provides a natural hedge against won weakness.

- Bio & Pharma — Insulated from global drug pricing negotiations; domestic demand base is stable. Selective approach focused on export-oriented biotech firms.

- Semiconductors (Memory & HBM) — Short-term oversold. AI demand as a long-term structural driver remains intact; dollar-cost averaging recommended.

5 Sectors to Avoid for Now

- REITs — Dividend appeal diminishes as rates stay high; asset valuation pressure persists.

- Real Estate-Related Stocks — Dual headwind of domestic property market slump and elevated borrowing costs.

- High-PER Growth Stocks — Rising discount rates compress future cash flow valuations; valuation burden resurfaces.

- Utilities — Defensive role is weakened in the current macro environment; yield appeal is limited.

- Consumer Staples (Domestic) — Rising FX and falling real purchasing power weigh on consumer sentiment.

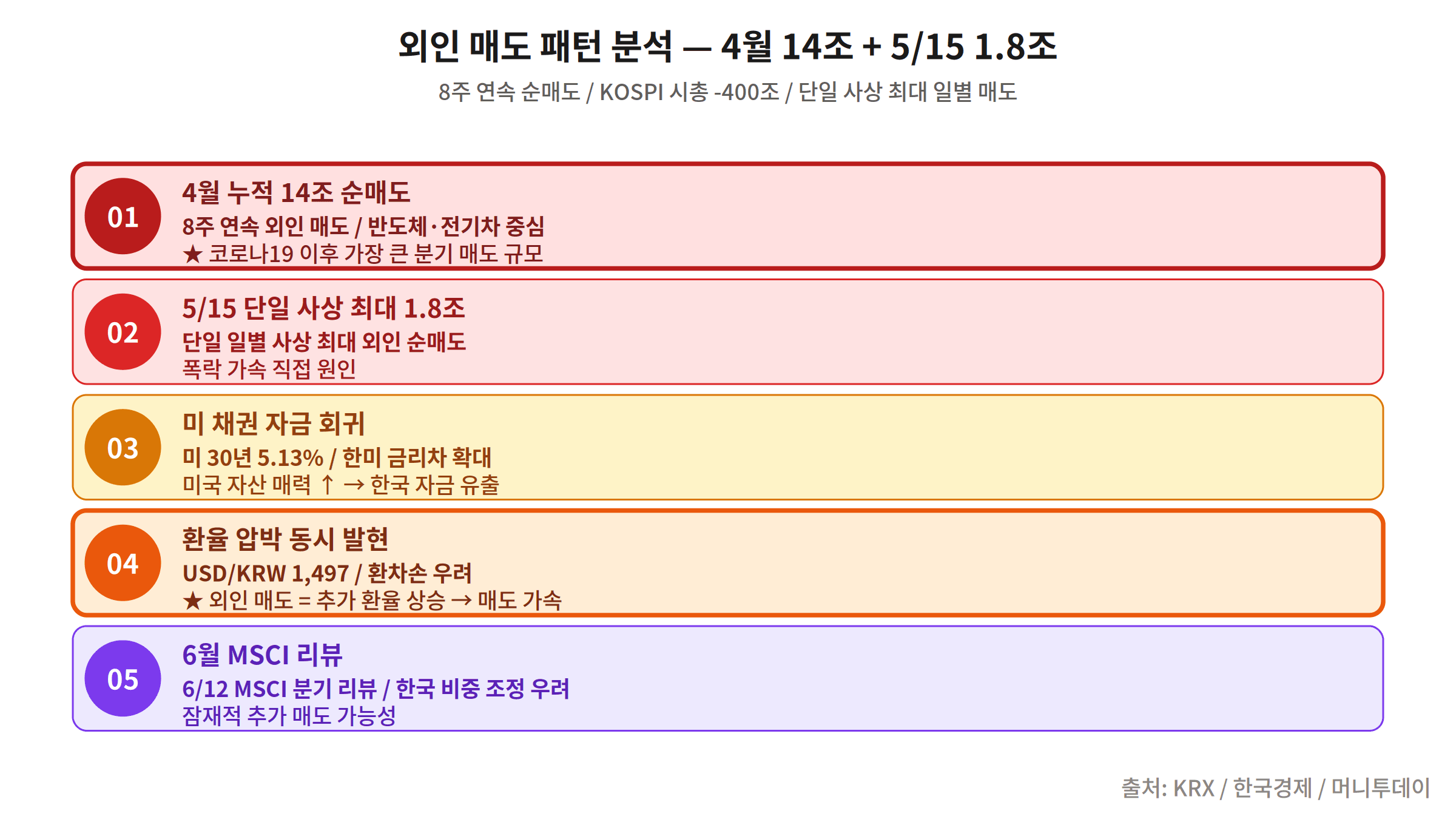

7. Foreign Selling Pattern — 8 Consecutive Weeks, ₩14T Outflow Since April

The ₩1.8 trillion foreign net sell on May 15 is not an isolated event. Foreign investors have been net sellers of KOSPI for 8 consecutive weeks since late March 2026, draining more than ₩14 trillion from the market in April alone.

This structural outflow is not simple profit-taking. It reflects the compound effect of dollar strength, rising US long-term yields, and a global risk-off shift away from emerging markets. Large-cap IT and semiconductor stocks with high foreign ownership have borne the brunt. Market consensus holds that a reversal of this trend requires at least one of two catalysts: a turn lower in the dollar index or a clear Fed rate-cut signal.

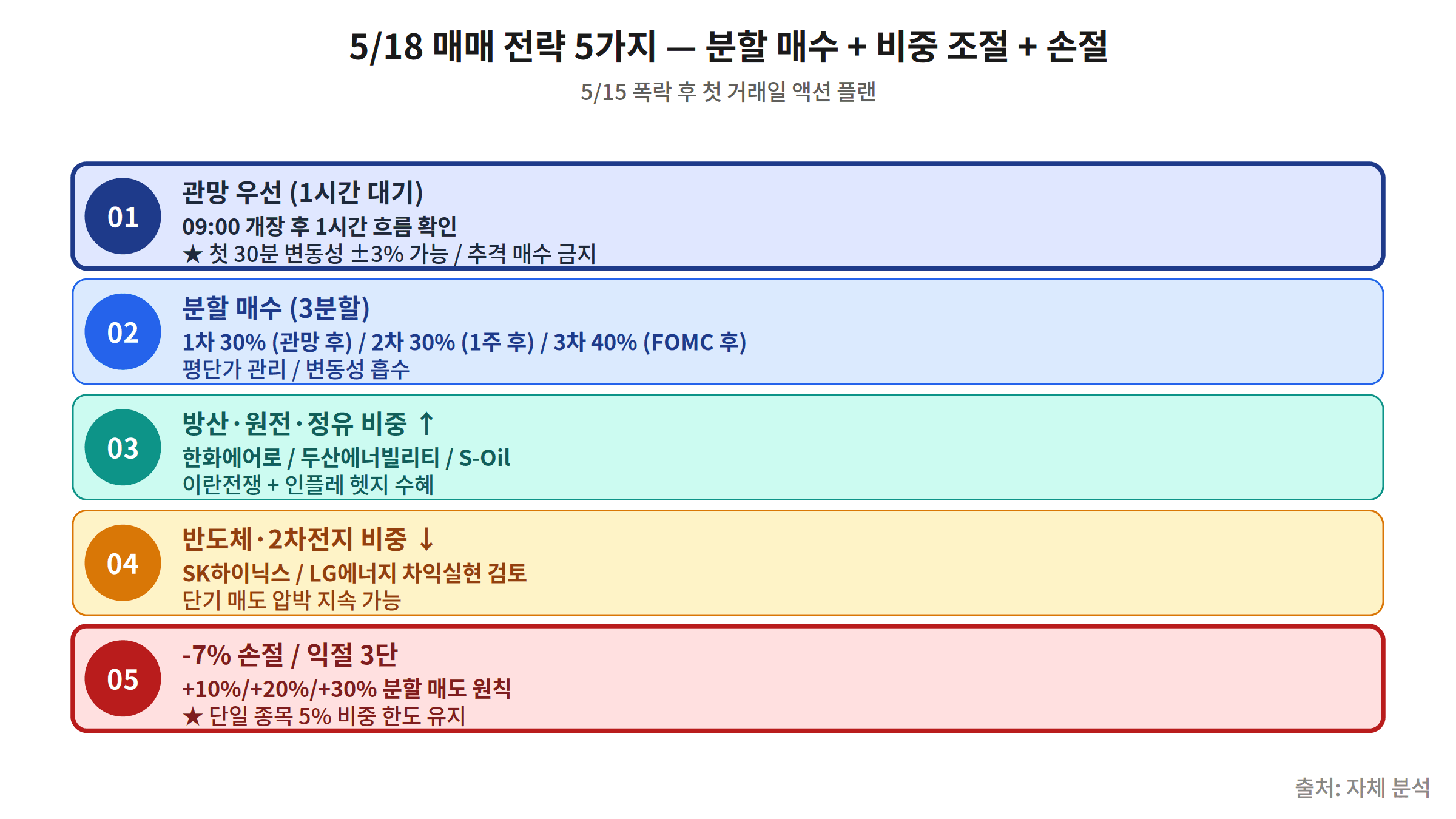

8. Five Trading Strategies — An Actionable Checklist

- Wait the First Hour After Open — The 09:00–10:00 window on May 18 will be characterized by maximum volatility as the prior session’s shock is digested. Avoid initiating new buy or sell positions until market direction becomes clearer.

- Scale Into Positions in Three Tranches — If targeting a rebound entry, divide your total intended purchase into three separate tranches. Example: Tranche 1 at -3% from reference, Tranche 2 at -5%, Tranche 3 on any further weakness. This approach reduces average cost and limits damage if the market falls further.

- Keep Equity Exposure Below 30% of Portfolio — In the current high-volatility regime, cap equity holdings at 30% of total assets as a risk management baseline. The remainder should be held in cash, short-duration bonds, or dollar-denominated assets.

- Apply a Hard -7% Stop-Loss Rule — For any position entered, execute a mechanical stop-loss at -7% from the purchase price without exception. The most dangerous psychology in a crash environment is “I’ll wait for it to recover.”

- Maintain Elevated Cash Until FOMC (June 17) — Uncertainty persists until the June 17 FOMC decision. With the May 30 PCE and June 11 CPI releases still ahead, near-term volatility remains elevated. Hold a higher-than-normal cash position and wait for clarity before deploying capital aggressively.

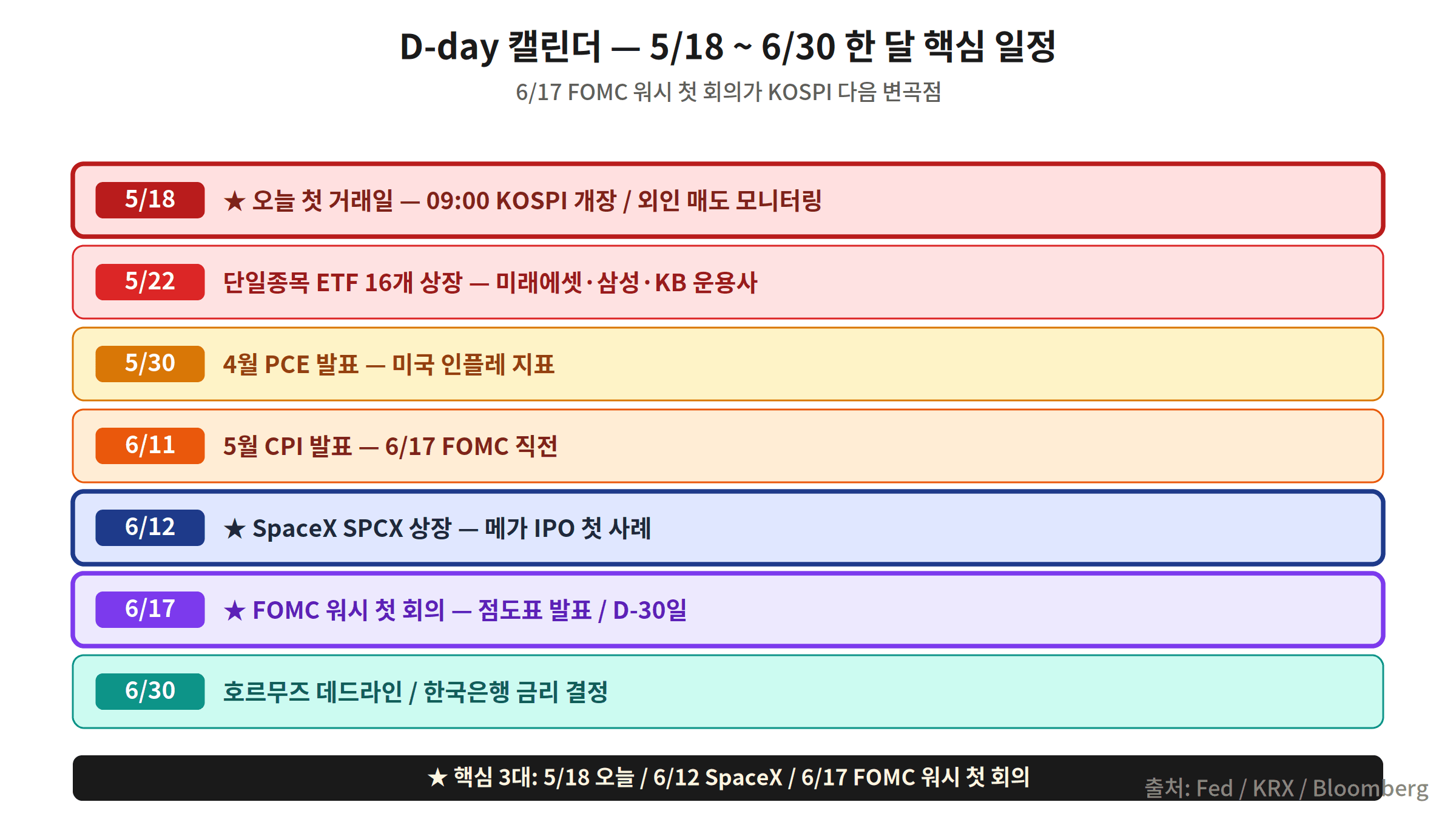

9. D-Day Calendar — The Next 5 Weeks Are the Inflection Point

Four pivotal events that will determine KOSPI’s trajectory are clustered within the next five weeks.

- May 27 — Nvidia Earnings (Q1 FY2027)

The clearest real-time gauge of AI semiconductor demand. A strong beat could serve as a rebound catalyst for SK Hynix and Samsung Electronics. A miss could trigger another leg down. - May 30 — US April PCE (Personal Consumption Expenditures Price Index)

The Fed’s preferred inflation gauge. A reading above consensus would push rate-cut expectations further out and add fresh downward pressure to KOSPI. - June 11 — US May CPI (Consumer Price Index)

The critical inflation data point released immediately before the June FOMC. A reading at or below 2.7% could revive rate-cut expectations and provide a much-needed market lift. - June 17 — FOMC Rate Decision + Updated Dot Plot

The single most important market event of this cycle. A hold accompanied by a second-half cut signal could trigger a global risk-on rotation. A continued hawkish tone risks sending KOSPI to new lows.