Polred (487580) IPO Analysis: +300% Day-1 Surge, ₩80B Revenue, Japan 84% Risk & Entry Checklist

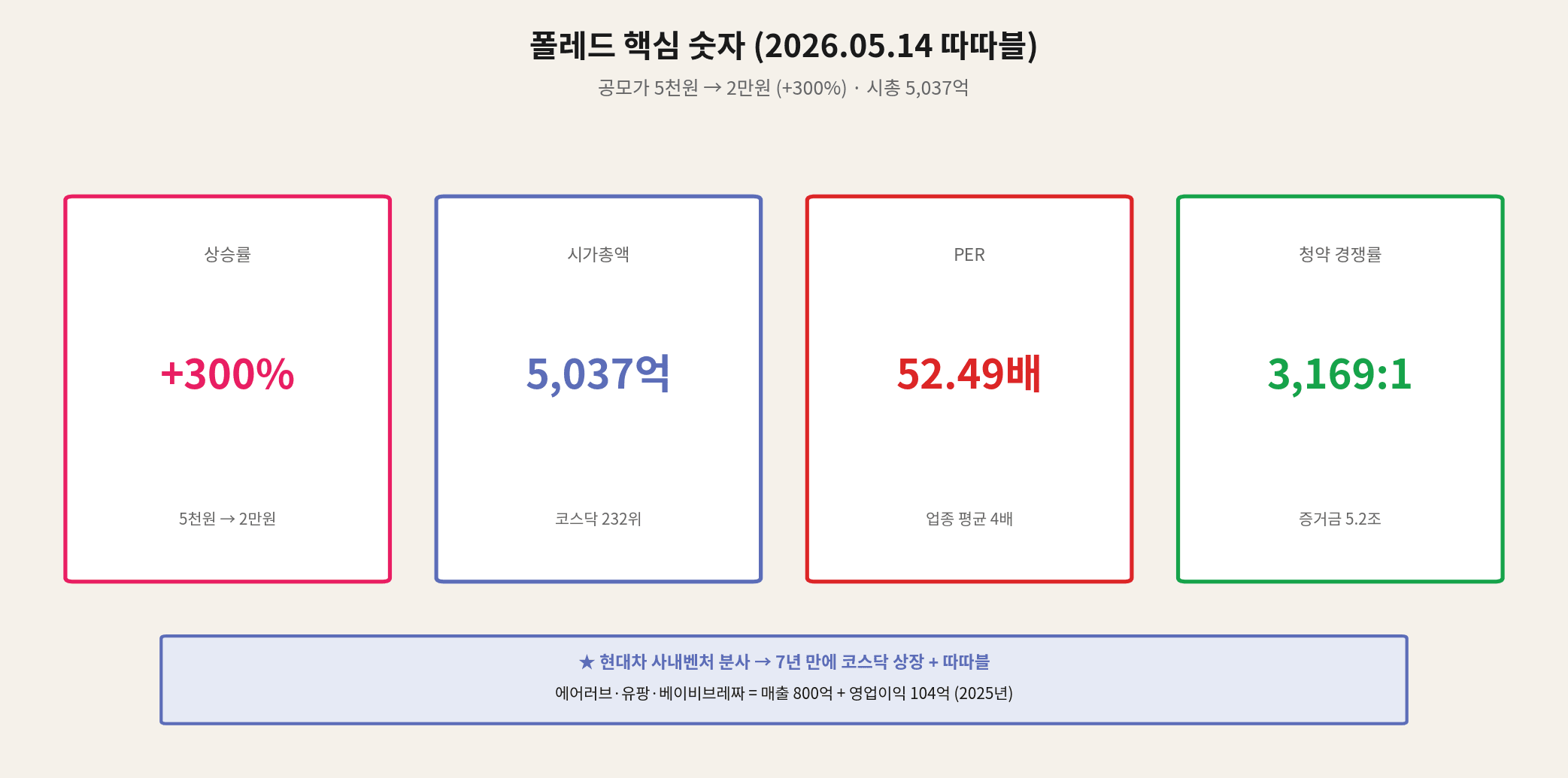

On May 14, 2026, Polred (487580) surged +300% on its KOSDAQ debut — hitting the daily price limit of ₩20,000 from an IPO price of ₩5,000. Market cap topped ₩504 billion in a single session.

The company began as a Hyundai Motor in-house venture in 2016 and spun off in 2019, building a profitable baby products business with ₩79.9B revenue and ₩10.4B operating profit in 2025. On the same day, Cosmo Robotics (listed May 11) hit +778% over 4 trading days — both are labeled Korea’s top 2026 new listings.

This analysis covers: company overview, the ₩80B growth story, 4 core products, 4 structural strengths, 5 risks (84% Japan dependency, PER 52x, 67% lockup), and an entry checklist for investors.

01 Company Overview: From Hyundai Spin-off to ₩500B

| Item | Detail |

|---|---|

| Ticker | 487580 (KOSDAQ) |

| Listing Date | May 14, 2026 (NH Investment & Securities) |

| IPO Price | ₩5,000 (top of ₩4,100–₩5,000 range) |

| IPO Size | ₩13B (2.6M shares) |

| CEO | Lee Hyeong-mu (former Hyundai Namyang R&D automotive designer) |

| Largest Shareholder | Lee Hyeong-mu 12.47% |

| Shares Outstanding | 25,182,861 |

| May 14 Result | Open ₩16,500 → Double-limit ₩20,000 (+300%) |

02 ₩80B Revenue: 3.5x Growth in Two Years

| Year | Revenue (₩B) | Op. Profit | Key Event |

|---|---|---|---|

| 2022 | ~₩23B | -₩0.5B | Losses continue |

| 2023 | ₩52.8B | ₩0.2B | First profitable year |

| 2024 | ₩52.8B | ₩6.2B | Ufang & IVG acquisition impact |

| 2025 | ₩79.9B | ₩10.4B | +51.4% / +68.1% ★ |

03 Revenue Mix: The Japan 84% Trap

| Category | Revenue Share | Key Products |

|---|---|---|

| Baby Appliances | 53.3% | Ufang (sterilizer) + Baby Brezza (formula maker) |

| AIRLUV | 25.6% | Ventilated/heated seat cushions |

| Hygiene Products | 10.0% | Baby cosmetics etc. |

| Safety | 5.1% | Car seats (COVID impact contraction) |

| Other | 6.0% | Accessories |

| Market | % of Total Revenue | % of Overseas Revenue |

|---|---|---|

| Japan | 16.4% | 84% |

| Taiwan | 1.4% | 7% |

| Other (US, SE Asia) | 1.8% | 9% |

04 Four Core Products — Category #1 Brands

| Product | Category | Key Metric |

|---|---|---|

| AIRLUV | Ventilated/heated baby seat | 1M+ units sold / 25.6% revenue |

| Ufang | Baby bottle sterilizer | 90%+ market share / ₩24B revenue (2025) |

| Baby Brezza | Formula maker | Korea & Japan exclusive / ₩18.5B revenue |

| Pixel / Franklin | Bottle washer / hygiene | Proprietary brand lineup |

05 Four Structural Strengths

- Multi-Category #1 Brand Portfolio — AIRLUV, Ufang, Baby Brezza, Pixel each lead their category. Diversified, not single-product dependent.

- Fully Vertically Integrated — In-house: product planning, design, manufacturing, logistics, CS/AS. Own mold design differentiates from Chinese import resellers.

- Bolt-on M&A Playbook — 100% acquired Ufang + IVG in 2024. Within one year, acquisitions represent 47.5% of revenue.

- VIB (Very Important Baby) Trend Alignment — Fewer babies but more spending per child. The premium baby products market is actually growing.

06 Five Risks — Honest Assessment

| Risk | Detail |

|---|---|

| ① PER 52.49x | 4x sector average of 12.84x. Limits further upside after +300% debut. |

| ② 84% Japan Dependency | 84% of overseas revenue from Japan alone — yen FX, policy, tariff exposure. |

| ③ Korea + Japan Birth Rate Decline | Both key markets shrinking — premium pricing strategy must offset volume decline. |

| ④ 67% Lockup | 67.24% of institutional shares locked — concentrated sell pressure at 1/3/6-month release. |

| ⑤ M&A Revenue Dependency | 47.5% of revenue from 2024 acquisitions — organic growth rate needs separate validation. |

07 Polred vs Cosmo Robotics — Same Day, Different Story

| Item | Polred (487580) | Cosmo Robotics (439960) |

|---|---|---|

| Listing | May 14, 2026 | May 11, 2026 |

| May 14 Close | ₩20,000 (+300%) | ₩52,700 (+778%) |

| Pattern | Day-1 double-limit | Double-limit + 3 consecutive limit-ups |

| Revenue (2025) | ₩79.9B (profitable) | ₩8.9B (loss-making) |

| Investment Type | Stability + Japan exposure | Growth + short-term frenzy |

08 Entry Checklist — Five Signals

- STEP 1: Lockup Release Schedule — 67% institutional lockup. First major sell pressure arrives ~mid-September 2026 (18 weeks post-listing)

- STEP 2: PER 52x vs Sector 12x Justification — Can the 4x premium hold? Track overseas revenue growth rate continuity

- STEP 3: Japan Revenue FX & Policy Risk — 84% Japan exposure = yen, tariff, consumption tax, Korea-Japan relations all in play

- STEP 4: Organic Growth vs M&A Effect Separation — Strip out the 47.5% acquisition contribution; what does the underlying business grow at?

- STEP 5: US & Taiwan Expansion Progress — Ufang US launch / geographic diversification away from Japan dependency

09 Conclusion: How to Frame Polred

Polred has genuine structural appeal: profitable at scale (₩80B/₩10.4B), four category-leading brands, fully vertically integrated operations. These are durable competitive advantages, not just IPO hype.

But entering immediately after a +300% surge demands caution. PER 52.49x is 4x the sector average, and 84% Japan concentration creates single-market risk. The September lockup expiry is the next major test.

② Risks: PER 52x vs 12x sector / Japan 84% / birth rate decline / 67% lockup

③ Key Variable: US/Taiwan geographic diversification / organic growth rate / Ufang global

④ Watch Dates: Mid-September lockup release / H1 2026 earnings / Japan revenue share

⑤ Entry Strategy: No chasing / scale-in approach / verify lockup schedule first

🏠 Recommended Products

This post is part of the Coupang Partners program. A commission may be earned from qualifying purchases.

![[Breaking 21:30 KST] US April CPI 3.8% — oil spike kills Fed rate-cut bets](https://getdir.app/wp-content/uploads/2026/05/01_cpi_trend-768x380.png)