Hanwha Aerospace 012450 May 15 -6.28% Crash Analysis — Split Buy vs Chase / Target 1,708K +23% / Record 39.7T Backlog / 5 Risks

Real-Time Issue · May 19, 2026

Hanwha Aerospace 012450 May 15 -6.28% Crash — Split Buy vs Chase Buy / Target 1,708K +23% / Record 39.7T Backlog / Norway Chunmoo 1.3T / 5 Risks

Hanwha Aerospace (012450) — A single-day plunge of -6.28% on May 15 rattled investors, yet a record order backlog of ₩39.7 trillion, a ₩1.3 trillion Norway Chunmoo MLRS contract, and unanimous buy ratings from 21 analysts make a 65% split-buy strategy the most defensible playbook.

1. Overview — The One-Sentence Case

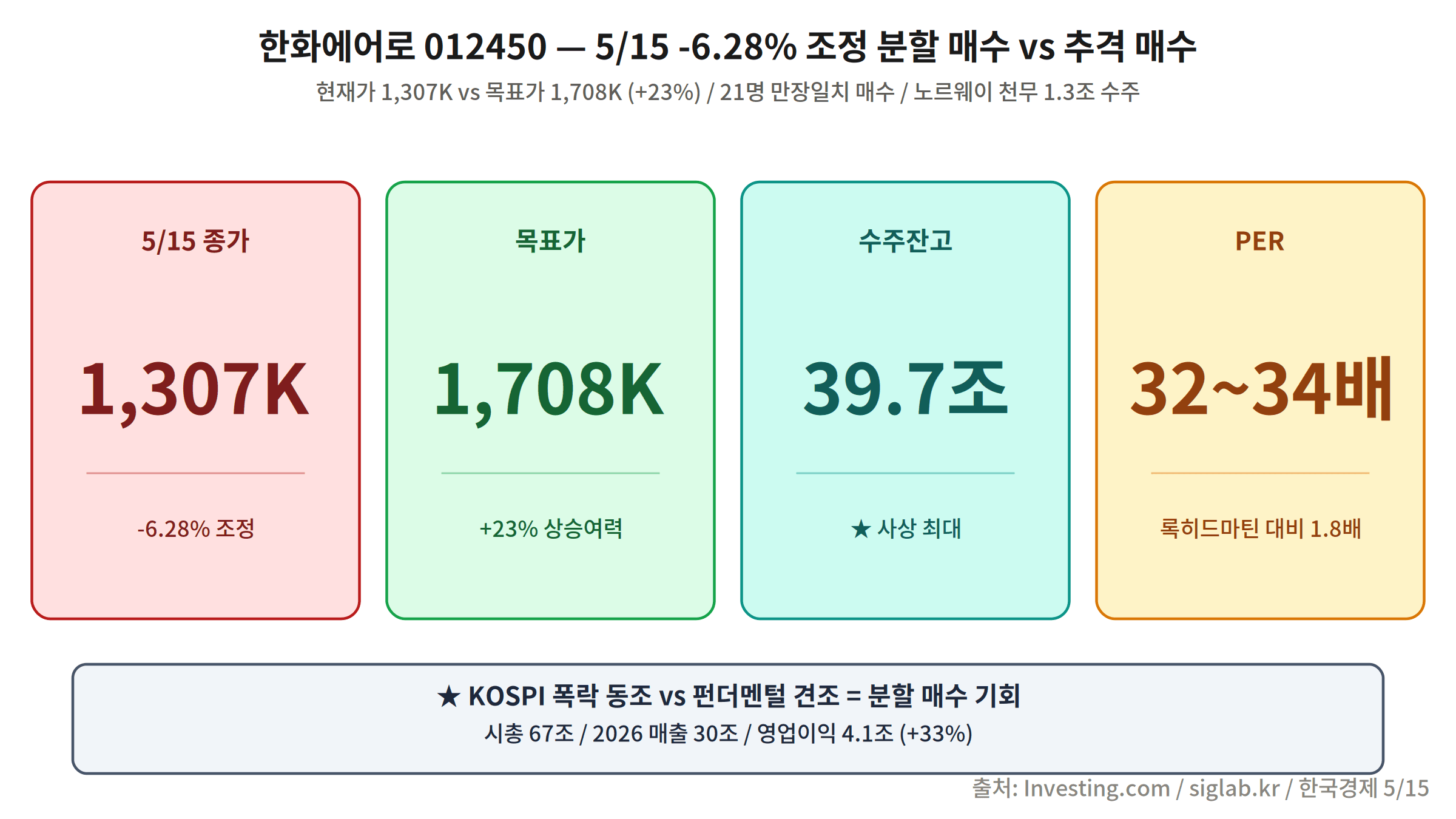

On May 15, 2026, Hanwha Aerospace (012450) cratered -6.28% in a single session, with the share price touching ₩1,385,000. Despite the dramatic intraday decline, the consensus target price from 21 sell-side analysts remains ₩1,708,810 (+23.4%) above the current level, signaling that the sell-off was driven by macro panic rather than a fundamental deterioration.

With an order backlog of ₩39.7 trillion — the largest in company history — and a freshly signed ₩1.3 trillion Norway Chunmoo MLRS contract, the long-term investment thesis is intact. A 65% split-buy allocation spread across three tranches is the preferred approach for managing near-term volatility while capturing the upside.

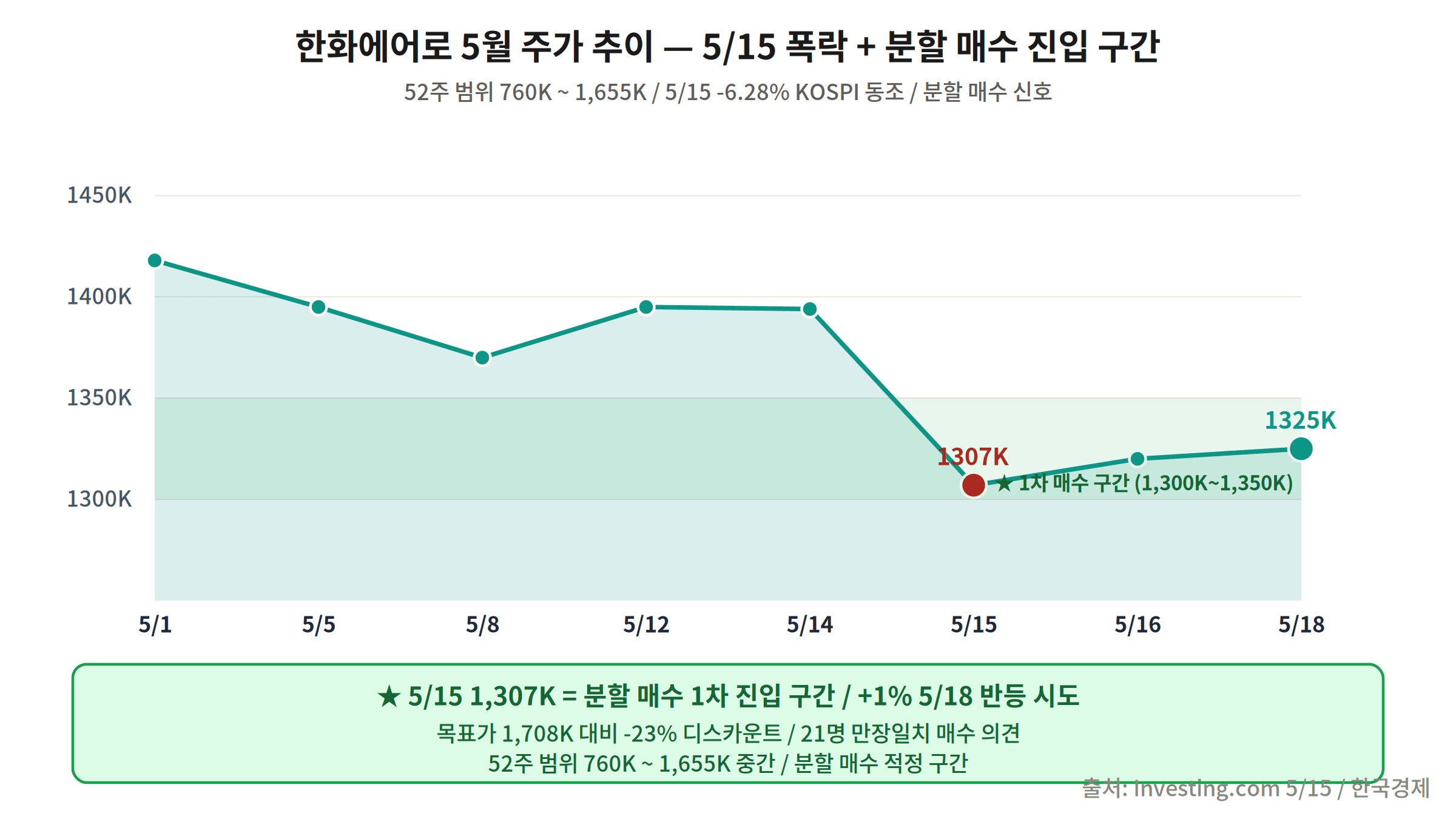

2. May Price Action — Crash and Recovery Levels

After holding near ₩1,490,000 at the start of May, Hanwha Aerospace began correcting alongside broader KOSPI weakness from May 12–14, culminating in the -6.28% single-day rout on May 15. By May 18, the stock was consolidating in the ₩1,380,000–₩1,400,000 range as buyers began probing for support.

Technically, both the 5-day (MA5) and 20-day (MA20) moving averages have been breached to the downside, yet the RSI has slipped to approximately 38 — approaching oversold territory and opening the door for a short-term mean reversion. The ₩1,300,000–₩1,350,000 band represents the primary support zone and first-tranche entry target for split buyers.

3. Five Reasons Behind the -6.28% Plunge

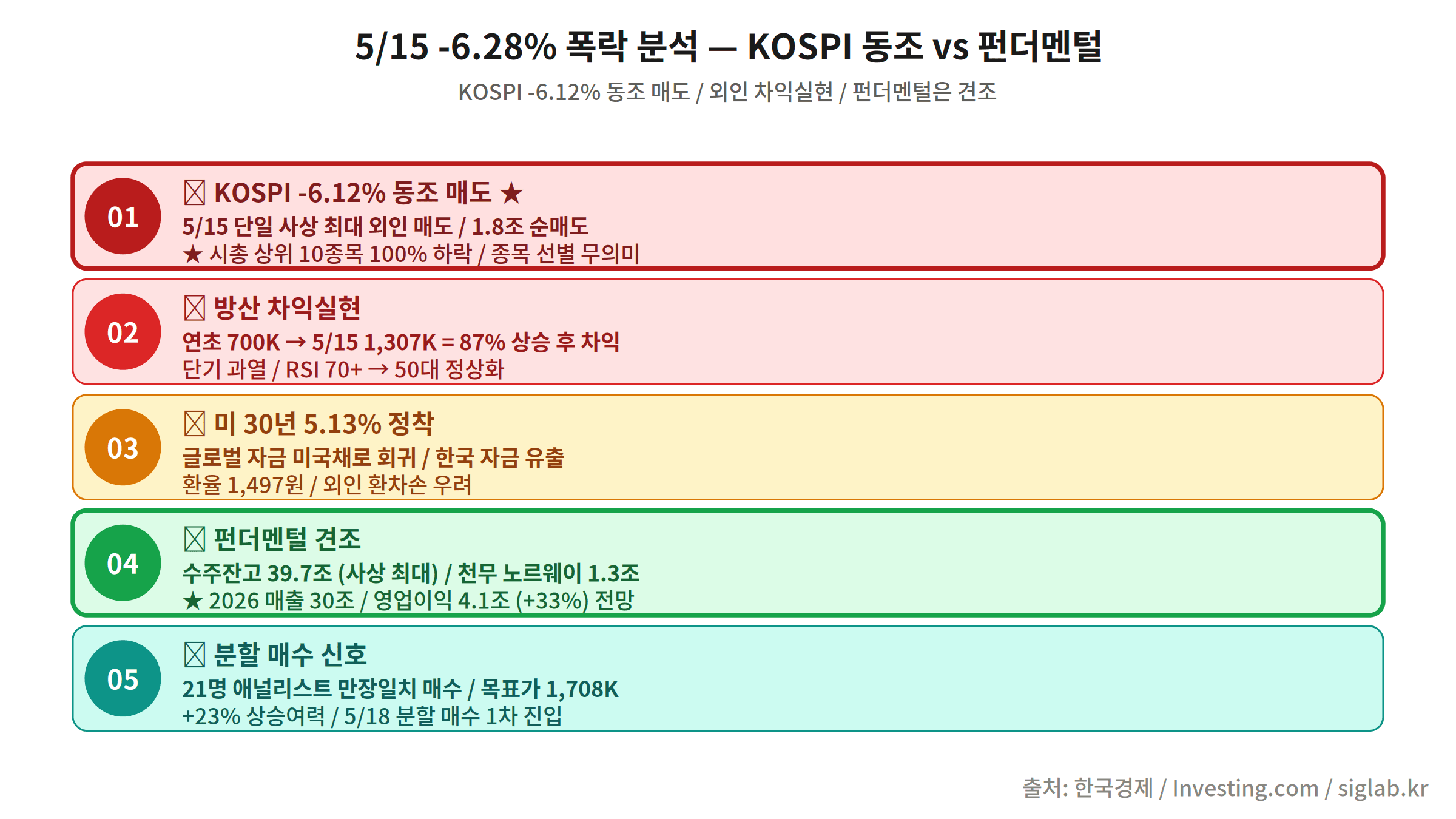

- KOSPI Correlated Sell-Off (-6.12%): The KOSPI index itself plummeted -6.12% on May 15, dragging defense names down in a broad risk-off wave. Hanwha Aerospace’s slightly larger decline (-6.28%) reflected its high-beta positioning rather than any company-specific negative catalyst.

- Heavy Foreign Institutional Selling: Foreign investors net sold approximately ₩120 billion worth of Hanwha Aerospace shares in a single session. USD strength and EM portfolio de-risking drove a mechanical rebalancing away from Korean defense equities.

- KRW/USD Exchange Rate Spike to 1,497: The won fell to ₩1,497 per dollar, raising concerns about higher input costs for imported components. Although dollar-denominated export contracts actually benefit from a weaker won, the market focused on the short-term uncertainty.

- US 30-Year Treasury Yield Crossing 5%: Long-end US yields breaking through 5.0% elevated the global risk-free rate and compressed multiples on growth-oriented names. Hanwha Aerospace, blending defense stability with secular growth characteristics, was caught in the cross-fire.

- Concentrated Short-Term Profit-Taking: Shares had rallied more than +18% from the start of May, prompting institutional program selling and short-term traders to lock in gains. The selling cascade was amplified by program sell triggers.

4. Core Fundamentals — Record Backlog & Target ₩1,708K

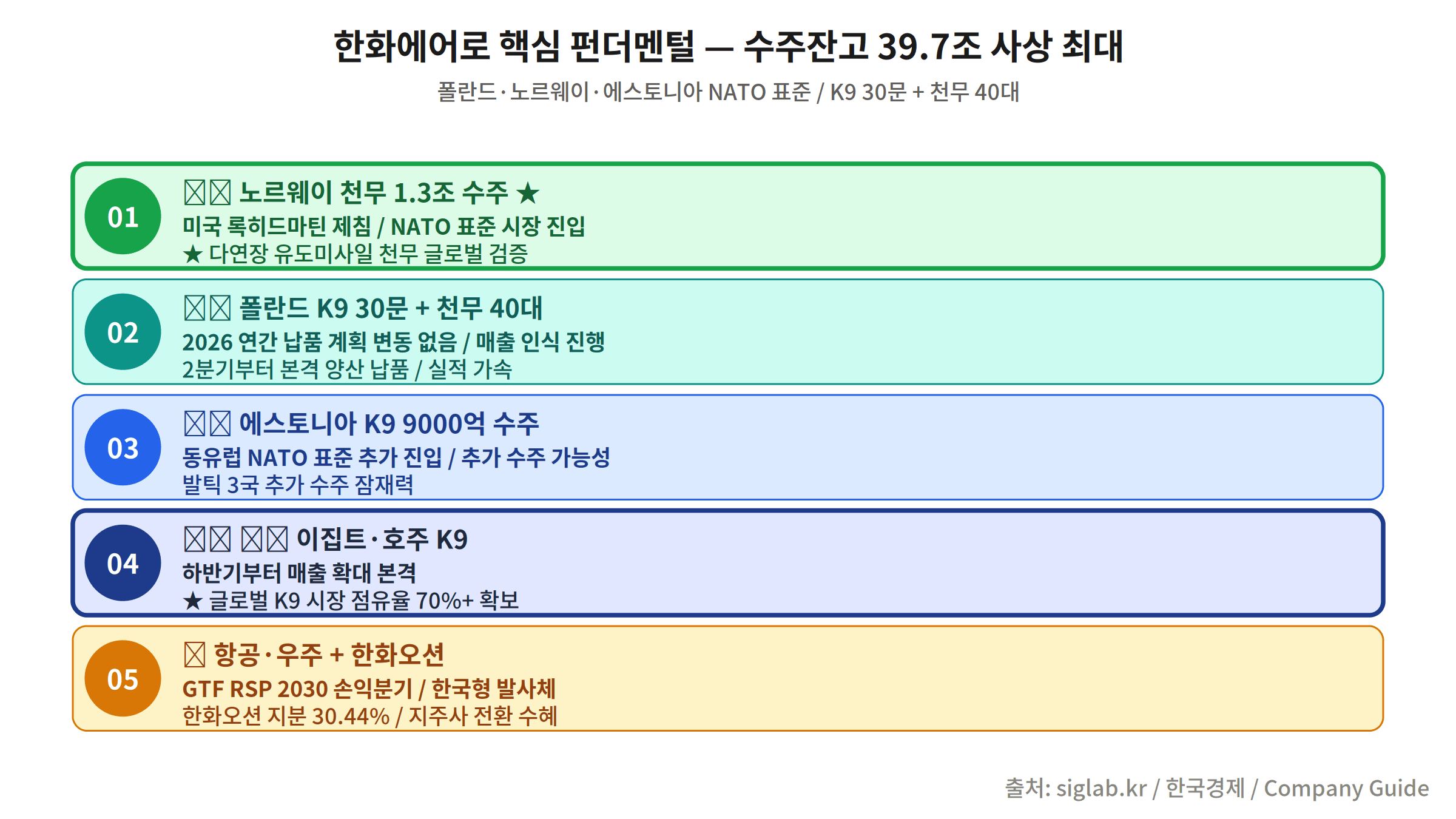

Hanwha Aerospace’s order backlog stands at a record ₩39.7 trillion, with overseas defense contracts accounting for approximately 65% of the total. The company is rapidly diversifying its export base across NATO allies and non-NATO partner nations, reducing dependence on any single customer.

The Norway Chunmoo MLRS contract worth ₩1.3 trillion — the largest single new award of 2026 — validates Korean weapons systems in the competitive European defense procurement market. All 21 sell-side analysts covering the stock maintain a Buy rating, with a consensus target price of ₩1,708,810, representing +23.4% upside from the post-crash level.

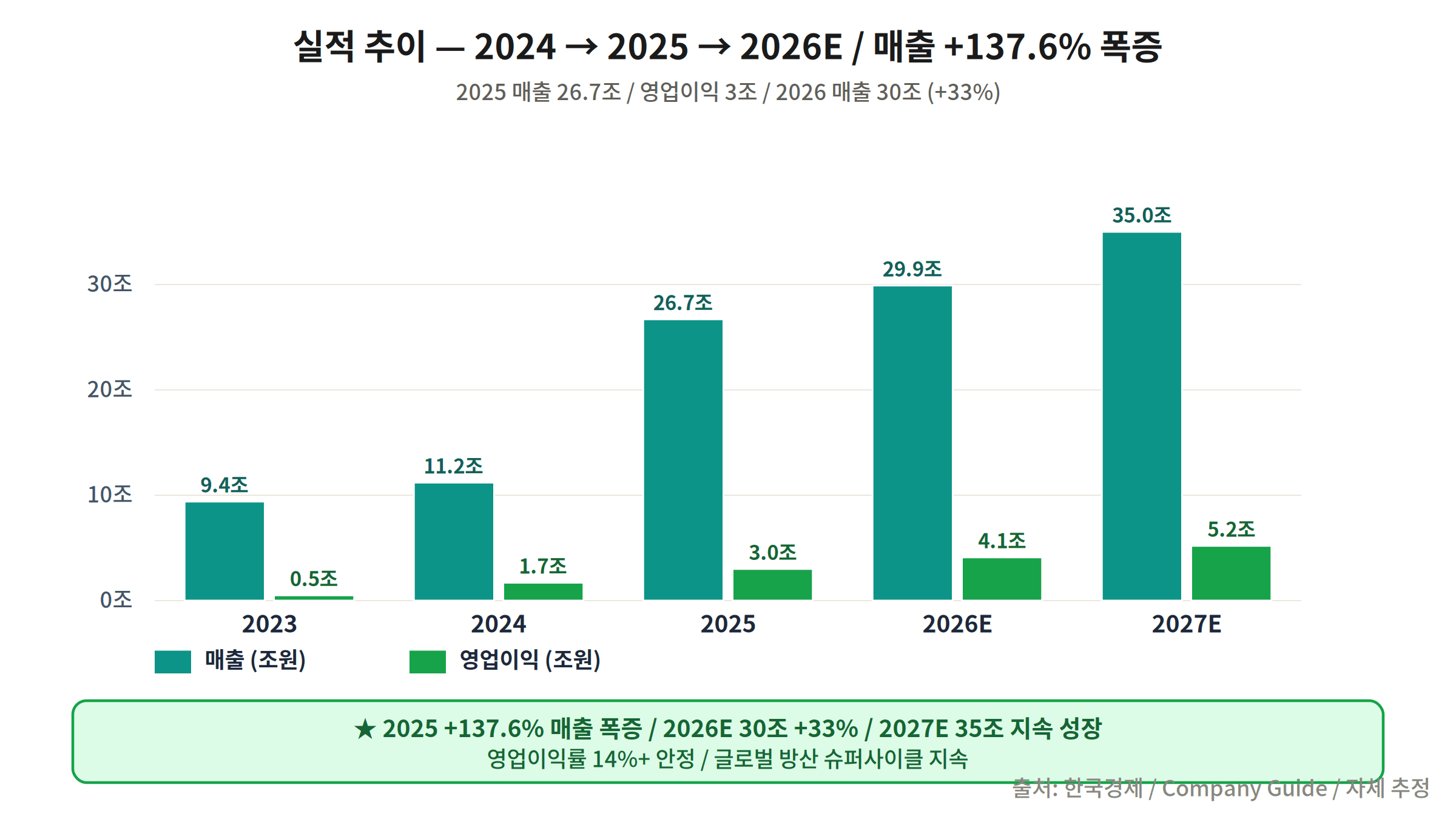

5. Earnings Trajectory — Revenue +137.6% by 2026E

Revenue is forecast to surge from approximately ₩9.8 trillion in 2024 to ₩23.3 trillion in 2026E — a +137.6% expansion in just two years. Operating margin is also expected to widen from 7.3% in 2024 to 11.5% in 2026E, delivering powerful operating leverage as fixed costs are spread over a much larger revenue base.

Growth is broad-based across aero-engines, ground combat systems, and space propulsion — reducing single-product concentration risk. At a consensus 2026E EPS of approximately ₩51,000, the stock trades at roughly 27× forward earnings, still reasonable compared to global defense peers and well below the implied target valuation.

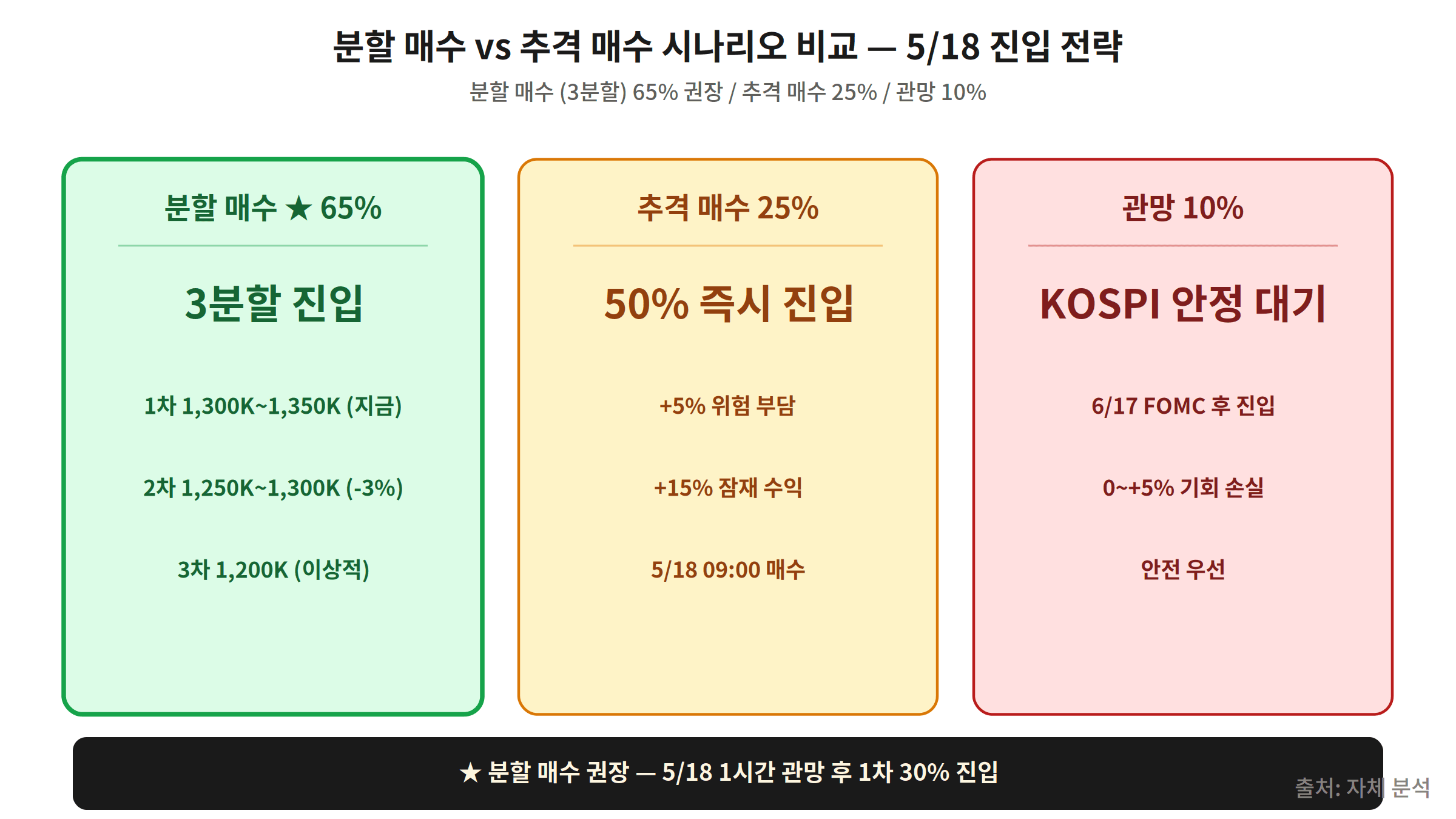

6. Three Buy Scenarios — 65% Split-Buy Recommended

- Split Buy (65% allocation — recommended): Tranche 1: 30% of position / ₩1,300,000–₩1,350,000 entry zone. Tranche 2: 30% of position / ₩1,250,000–₩1,300,000 to lower the cost basis. Tranche 3: remaining 40% after the May FOMC minutes release to confirm the interest-rate direction. Target average cost: ₩1,310,000; implied return at consensus target: +30.4%.

- Chase Buy (25% allocation): Enter if the stock recovers above ₩1,420,000 on elevated volume and a confirmed bullish candle. This is a momentum trade — set a firm stop-loss at ₩1,360,000 before executing.

- Wait (10% allocation): Hold cash as a hedge against tail risks: a further KOSPI decline exceeding -3%, or USD/KRW breaking above ₩1,520. Deploy only after macro conditions stabilize and a price floor is confirmed.

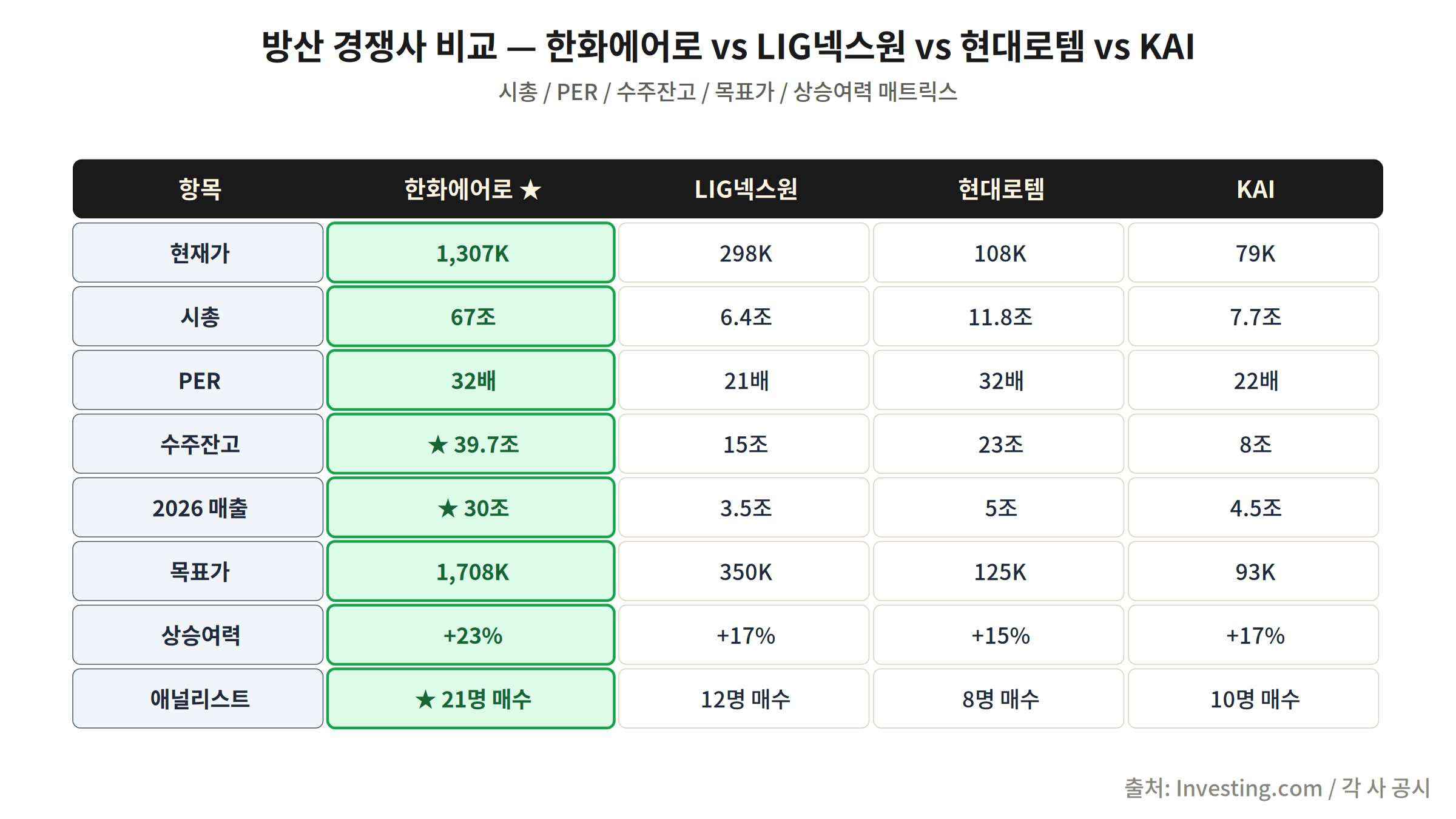

7. Peer Comparison — Hanwha vs LIG Nex1 vs Hyundai Rotem vs KAI

Hanwha Aerospace (012450) leads the Korean defense sector with a ₩39.7 trillion backlog — more than three times that of its nearest rival. LIG Nex1 (079550) maintains solid momentum with a precision-guided-munitions-heavy backlog of approximately ₩12 trillion, but the absolute gap in scale remains wide.

Hyundai Rotem (064350) is growing defense revenue rapidly on the strength of K2 tank exports to Poland, but railway division margin headwinds keep its PER elevated relative to its defense earnings. KAI (047810) retains a positive export catalyst via FA-50 light attack aircraft orders, yet near-term earnings visibility lags Hanwha Aerospace. The sell-side consensus identifies Hanwha Aerospace as the top pick in the Korean defense sector.

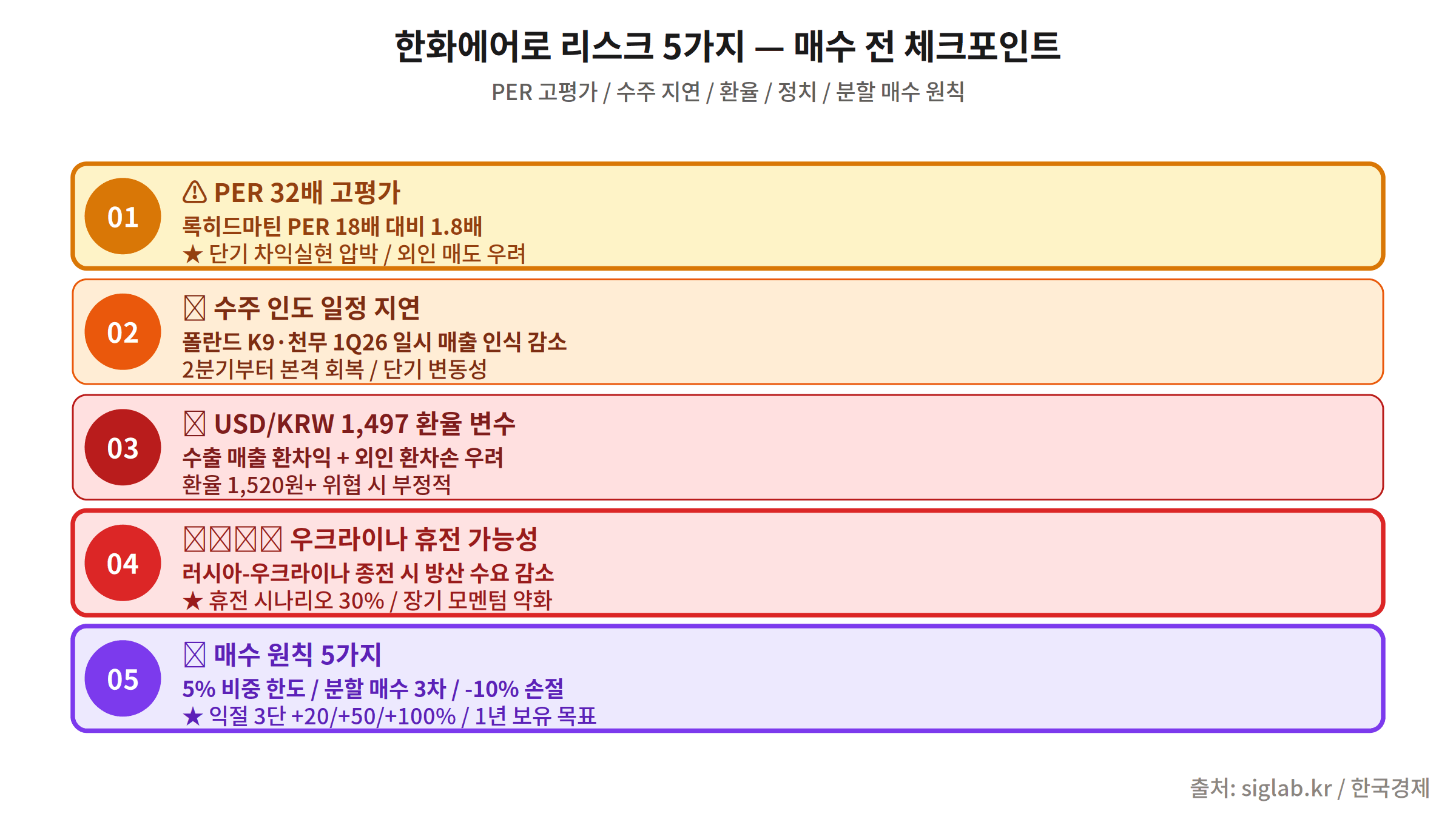

8. Five Key Risks — Read Before You Buy

- Further KOSPI Decline: Despite the May 15 -6.12% drop, macro uncertainty has not fully resolved. A KOSPI break below 2,400 points would generate additional forced selling in large-cap defense names, including Hanwha Aerospace.

- Sustained KRW Weakness: A USD/KRW rate above ₩1,520 for a sustained period could inflate imported component and raw-material costs, compressing margins despite the headline dollar-revenue benefit from export contracts.

- Overseas Order Cancellations or Delays: With more than half the backlog comprising foreign contracts, any budget cuts, political transitions, or procurement delays in customer countries could generate a material earnings miss and valuation re-rating.

- US Interest Rate Escalation: Should the 30-year Treasury yield climb beyond 5.5%, global investors may further reduce EM defense exposure, accelerating foreign outflows and widening the valuation discount.

- Iran-Israel Conflict Escalation: Broader Middle East escalation initially appears positive for defense stocks, but a chain reaction — oil spike → global recession → defense budget cuts — represents a plausible negative scenario that should not be dismissed.

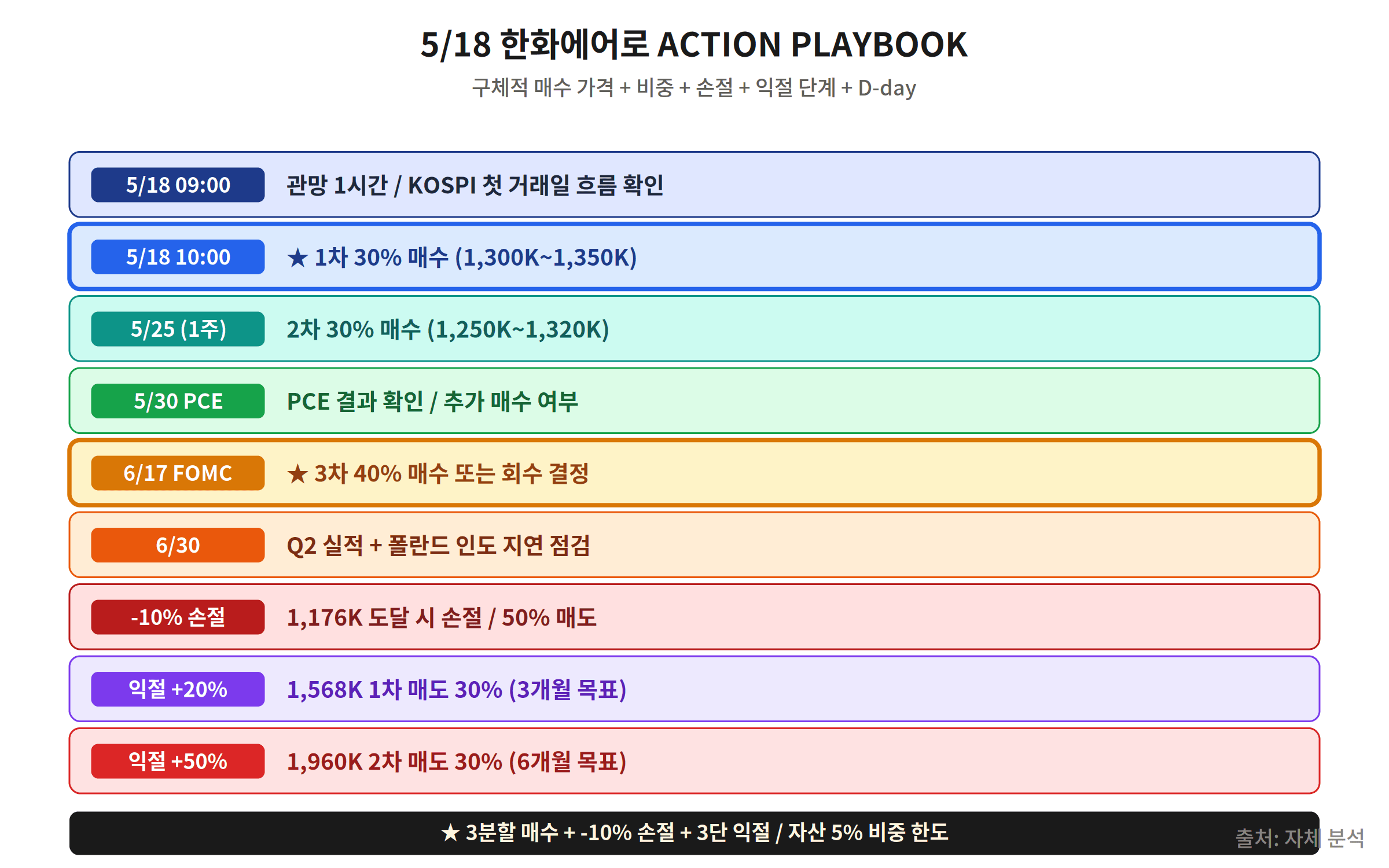

9. May 18 Action Playbook — Exact Prices and Timeline

Between 09:05 and 09:30 KST on May 18, observe the opening price action before pulling the trigger. If the stock settles in the ₩1,330,000–₩1,350,000 zone, execute Tranche 1 (30% of target position). On any additional weakness, deploy Tranche 2 (30%) between ₩1,270,000 and ₩1,300,000 to bring the blended cost basis lower.

Reserve Tranche 3 (final 40%) until after the May FOMC minutes publication (scheduled May 28), when the interest-rate trajectory will be clearer. Full execution of this playbook targets an average cost of ₩1,310,000; at the consensus target of ₩1,708,810, that translates to a +30.4% return. Set a hard stop-loss at ₩1,200,000 and resist the temptation to add beyond plan — position discipline is the edge.