Korea-Japan shuttle diplomacy and LNG cooperation — energy security and shipbuilding upside, a five-step playbook

Trending

Korea-Japan Shuttle Diplomacy & LNG Cooperation — Energy Security Investment Strategy (2026.05.25)

The revived Seoul-Tokyo channel built on shuttle diplomacy has produced a sweeping energy pact — joint LNG procurement, SMR cooperation, and a hydrogen supply chain. Here is a data-driven map of the beneficiaries (KOGAS, the Big-3 shipbuilders, SMR, hydrogen) and the five investment plays that follow.

By DIR Editorial · 2026.05.25

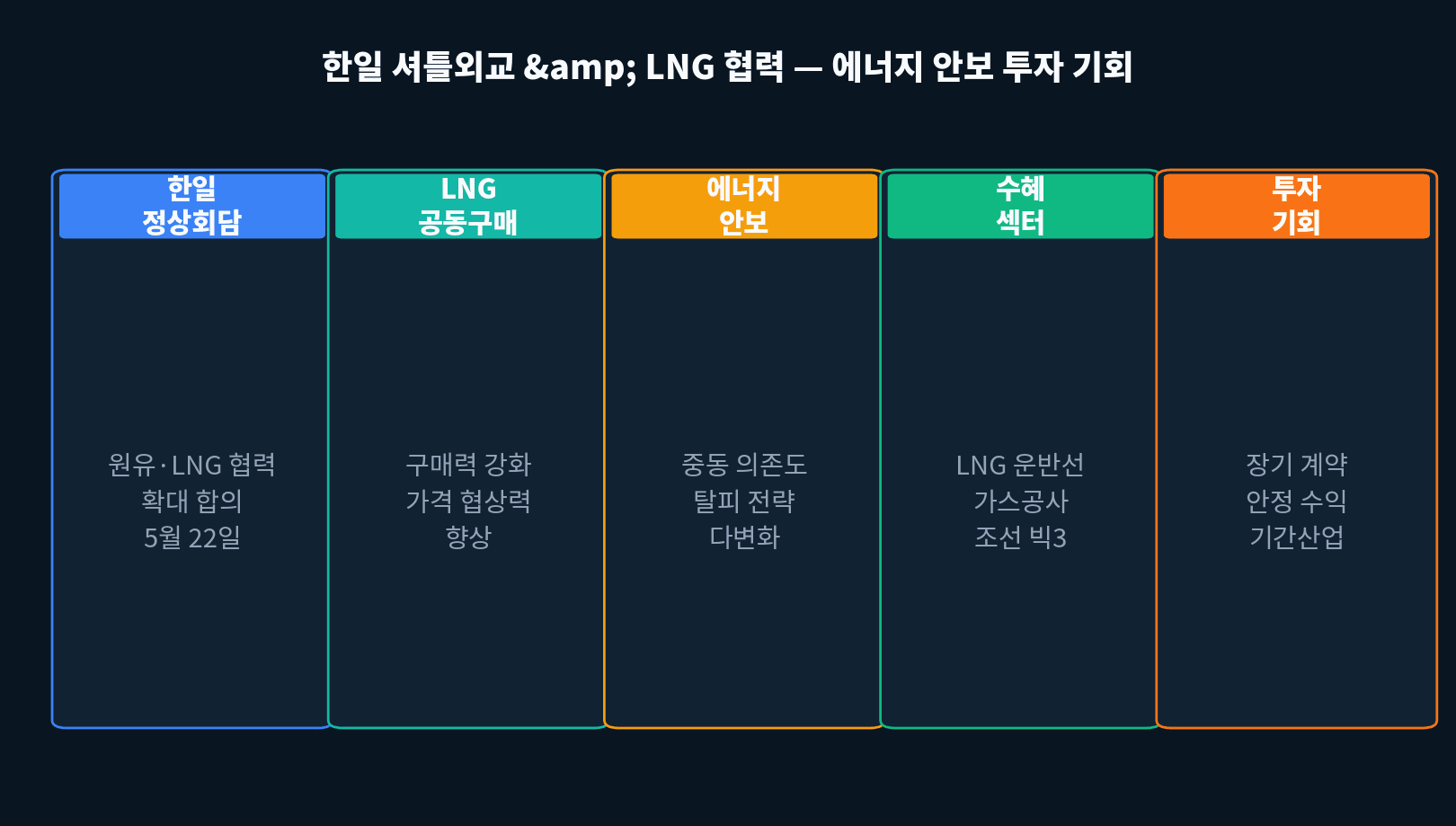

President Lee Jae-myung and Japan’s Prime Minister activated shuttle diplomacy on May 22 — combined with a hometown visit — and agreed on expanded crude oil and LNG cooperation as the centerpiece. With the Iran war pushing Middle East dependency into the danger zone, the two nations have effectively formed a joint energy front. Joint LNG procurement, nuclear cooperation, and a hydrogen supply chain are the main pillars. Background coverage is available via Reuters Energy.

The sectors most directly leveraged by this shuttle diplomacy are Korea Gas Corp., the Big-3 shipbuilders, small modular reactors (SMR), and the hydrogen-ammonia chain. This piece breaks down the agreement, the pricing math, and the five resulting investment plays.

| Pillar | Substance | Beneficiary | Expected Impact |

|---|---|---|---|

| Joint LNG Procurement | Combined Korea-Japan bargaining | Korea Gas Corp. | 5-10% price cut |

| Crude Diversification | Australia · US · Qatar | Big-3 (LNG carriers) | More LNGC orders |

| Nuclear Cooperation | Joint SMR development | Doosan Enerbility | SMR export momentum |

| Hydrogen Energy | Green hydrogen co-production | HD Hyundai | Ammonia logistics tie-up |

| Energy Finance | Joint Korea-Japan energy fund | KDB | Lower funding cost |

“Korea and Japan are a community of destiny in energy security. When we respond together, we secure energy that is both safer and cheaper.” (Joint press conference, 2026.05.22)

01 | Korea’s Energy Security Picture — Why Now?

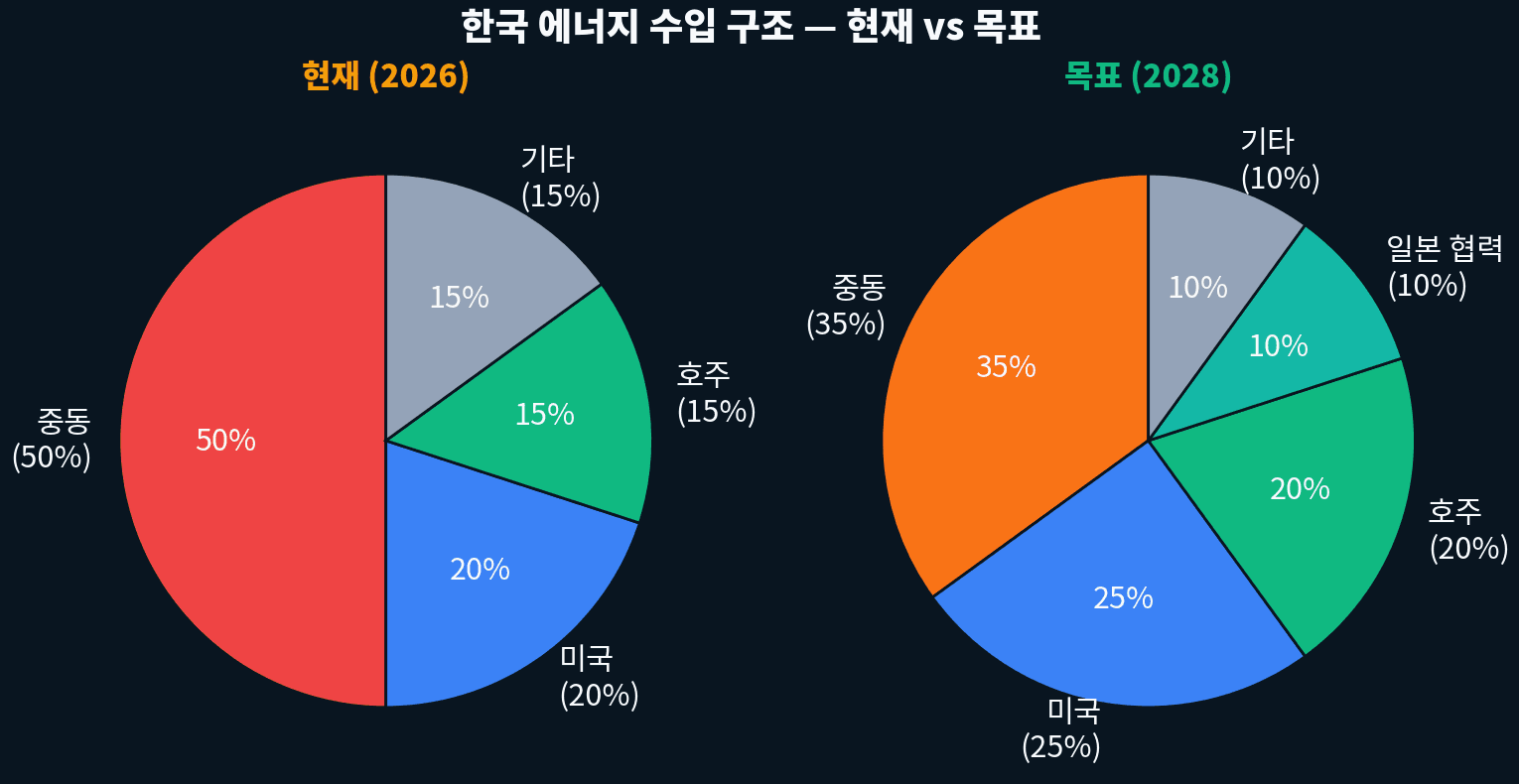

Korea’s energy self-sufficiency rate sits below 1% — among the lowest in the world. More than 95% of energy is imported, and the Middle East alone accounts for roughly 50%. With the Iran war effectively closing the Strait of Hormuz, securing alternative supplies has become an existential task.

| Energy | Current ME Share | Target ME Share | Alternative Supply |

|---|---|---|---|

| Crude oil | 53% | 35% | US · Canada · Australia |

| LNG | 45% | 30% | Qatar · US · Australia |

| Coal | 15% (no ME) | — | Australia · Indonesia |

| Total natural gas | 47% | 32% | Korea-Japan joint buy |

| Total energy | 50% | 35% | By 2028 |

— MOTIE Energy Security Roadmap (2026.04)

Of Iran’s roughly 3 million barrels of daily crude output, Korea imports about 200,000-250,000 barrels (post-2024 resumption basis). With Hormuz blocked, Korea’s LNG shipping costs have surged 70-80%, and some cargoes are being rerouted around the Cape of Good Hope.

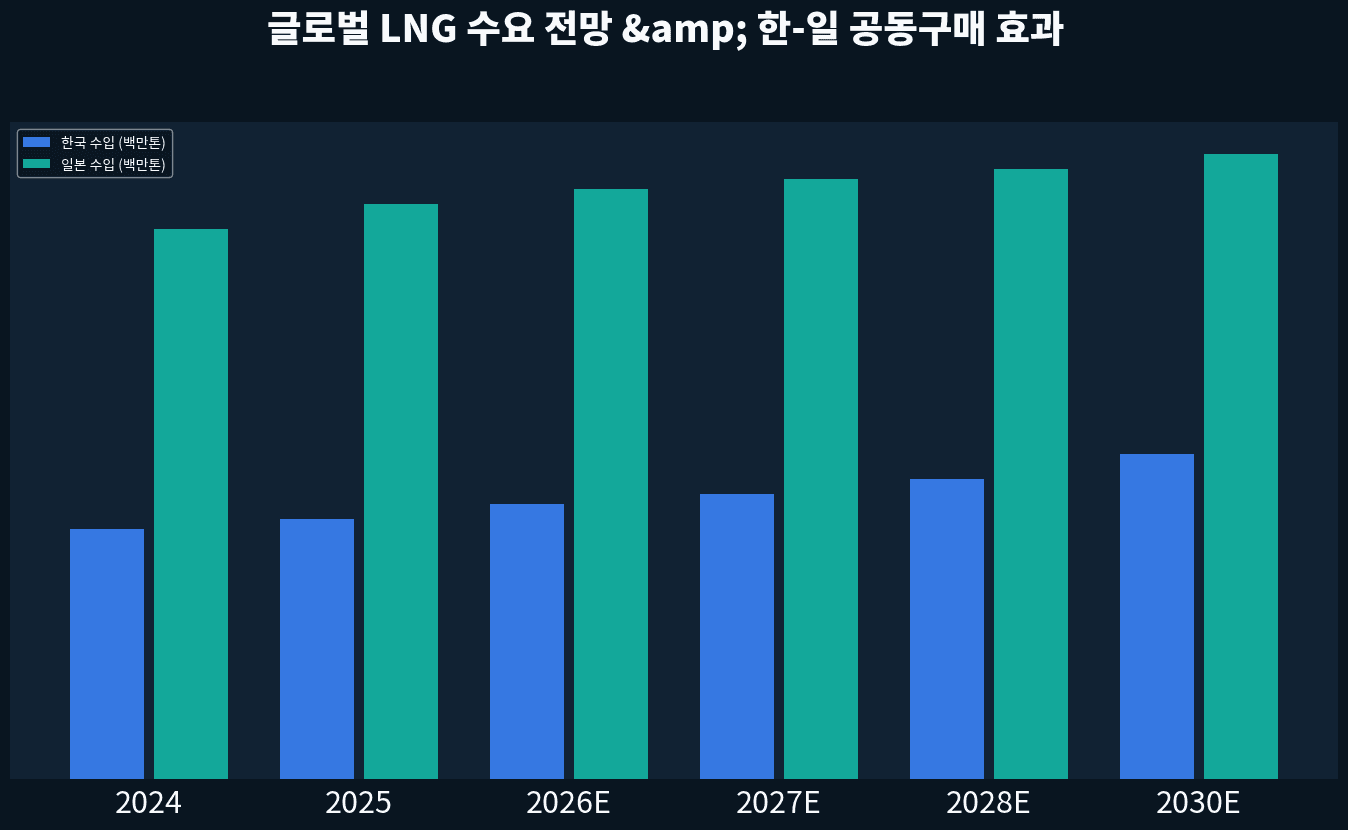

02 | Joint LNG Procurement — How Much Can It Save?

If Korea (~55 million tons LNG/year) and Japan (~70 million tons/year) buy jointly, they form the world’s largest LNG buying bloc — about 25% of global trade. The added bargaining power could deliver a 5-10% price discount.

| Metric | Solo (Current) | Joint (Target) | Savings |

|---|---|---|---|

| Bargaining volume | Korea 55Mt | Korea+Japan 125Mt | Top buyer status |

| Average LNG price | ~$30/MMBtu | ~$27-28/MMBtu | 5-10% cut |

| Annual savings | — | ~KRW 2-4 tn est. | National energy bill |

| Contract tenor | Short-term spot | Long-term contracts | Price stability |

| Supply diversification | ME-heavy | Australia · US · Qatar | Risk dispersion |

→ Top-buyer pricing leverage secured

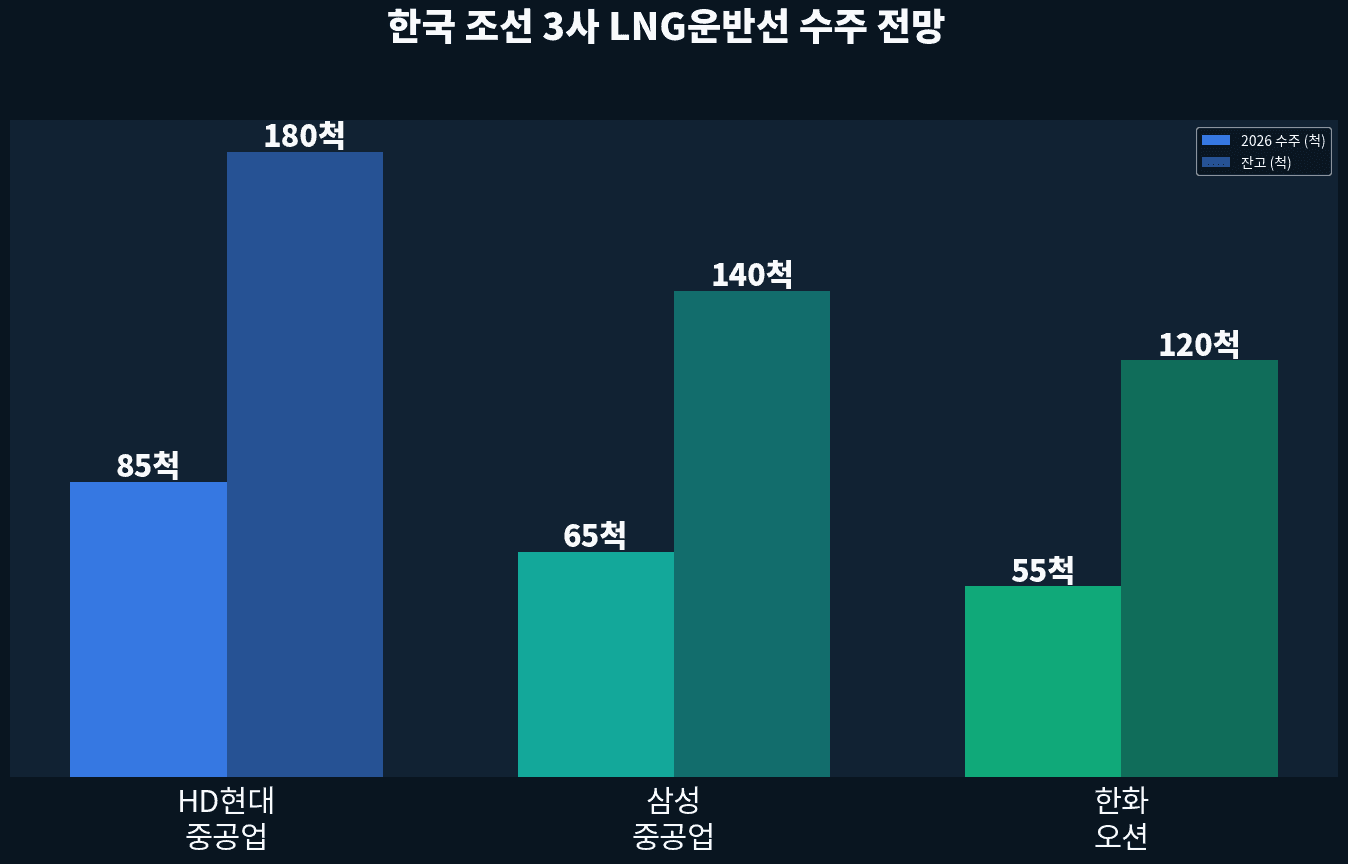

03 | Shipbuilding Windfall — LNG Carrier Orders Set to Explode

Supply diversification fuels demand for LNG carriers (LNGC). Shipping Australian or US LNG to Asia means voyages 2-3x longer than the Middle East route. Korea’s Big-3 (HD Hyundai Heavy, Samsung Heavy, Hanwha Ocean) build more than 75% of the world’s LNG carriers.

| Shipyard | Backlog | 2026 New-Order Target | Price per Vessel | Investment Angle |

|---|---|---|---|---|

| HD Hyundai Heavy (329180) | 180 ships | 85 ships | ~KRW 300bn | World #1 backlog |

| Samsung Heavy (010140) | 140 ships | 65 ships | ~KRW 290bn | Tech + margin lift |

| Hanwha Ocean (042660) | 120 ships | 55 ships | ~KRW 280bn | Defense crossover |

| Japan (JMU et al.) | 60 ships | 30 ships | ~KRW 270bn | KR-JP partner |

| China | 200+ ships | 120 ships | ~KRW 220bn | Price-war risk |

Margin per LNG carrier is now about 8-12% — sharply improved versus the prior cycle. Order backlogs span 4-5 years, locking in earnings visibility through 2028-2030. Hanwha Ocean also stacks defense (naval ship + submarine) orders on top.

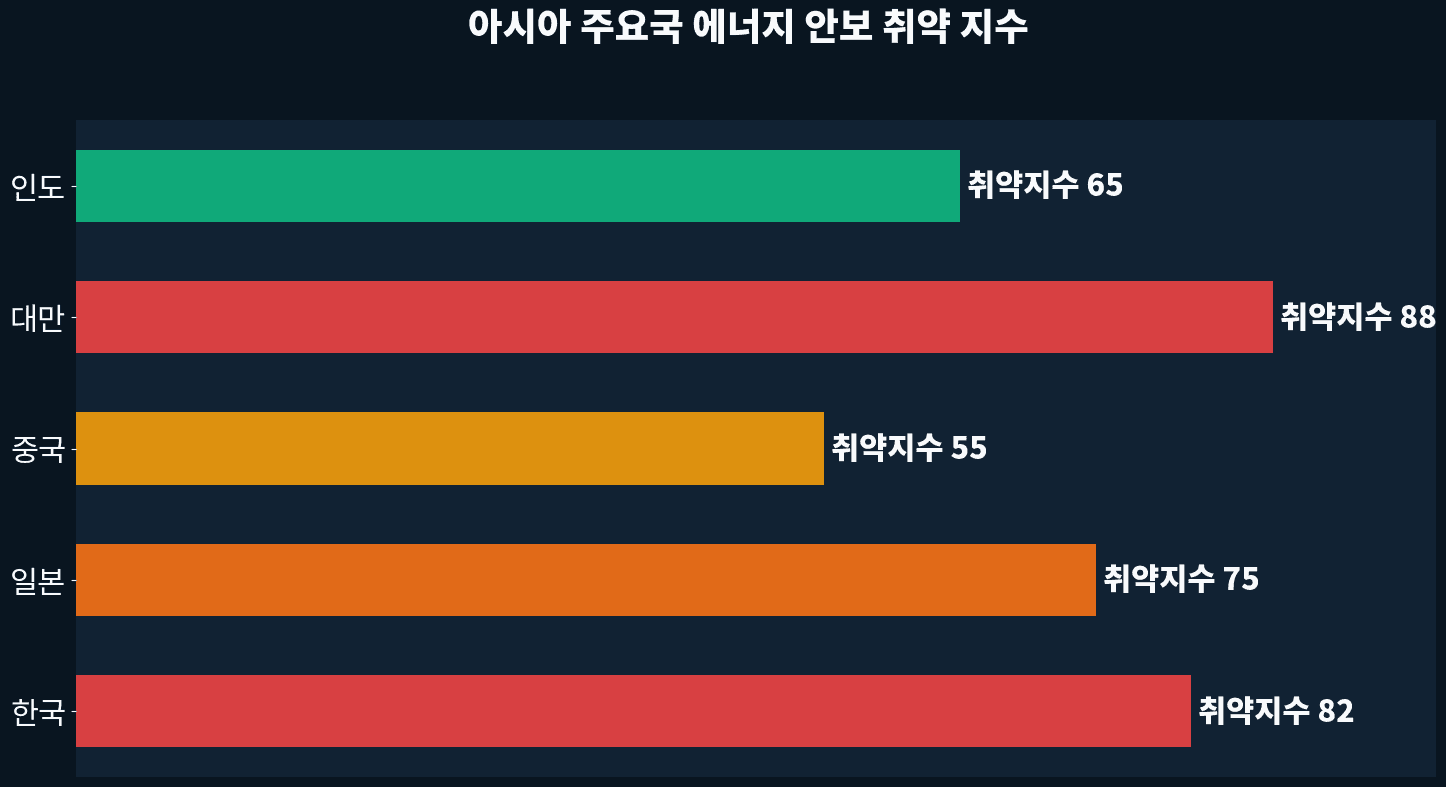

04 | Energy Security Index — Korea’s Vulnerability

According to IEA analysis, Korea’s energy security vulnerability index is among the highest of major Asian economies. With self-sufficiency under 1%, Middle East share at 50%, and strategic petroleum reserves at just 90 days, crisis-response capacity is thin. For Korea-Japan cooperation to be a structural fix, long-term contracts and stockpile expansion must run in parallel.

| Country | Self-Sufficiency | ME Dependency | SPR (days) | Grade |

|---|---|---|---|---|

| Korea | <1% | 50% | 90 | Vulnerable (worst) |

| Japan | 5% | 40% | 170 | Vulnerable |

| China | 60% | 45% | 90 | Moderate |

| Taiwan | 2% | 55% | 80 | Very vulnerable |

| Australia | 65% | 0% | 50 | Strong |

| United States | 100%+ | 0% | SPR 90 | Strongest |

Korea’s SPR sits at roughly 90 days (~97 million barrels). That barely clears the IEA’s 90-day recommendation. If the Iran war drags on, expansion to 150 days is under discussion.

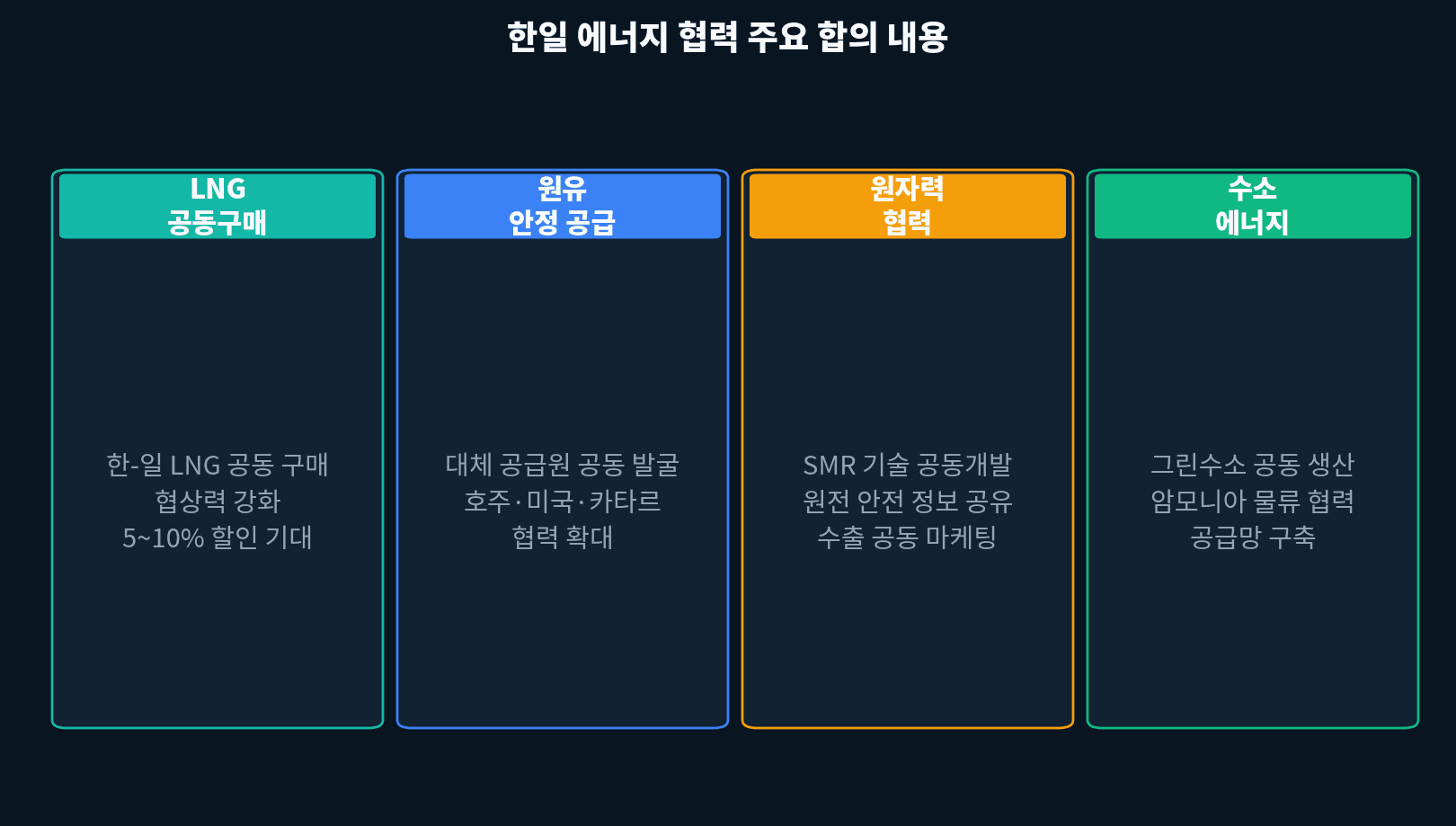

05 | Four-Pillar Agreement Born from Shuttle Diplomacy

The energy cooperation produced by this round of shuttle diplomacy extends beyond joint LNG buying to nuclear power, hydrogen, and carbon neutrality. The long-term intent is for Korea and Japan to jointly hold Asia’s energy leverage.

| Pillar | Substance | Expected Impact | Korean Beneficiary |

|---|---|---|---|

| Joint LNG Procurement | 125Mt joint negotiation | 5-10% price cut | Korea Gas Corp. |

| Nuclear (SMR) | Joint SMR development | Wider export market | Doosan Enerbility |

| Hydrogen · Ammonia | Green hydrogen co-production | Net-zero foundation | Hyundai Motor, HD Hyundai |

| Energy Finance | Joint infrastructure fund | Lower funding cost | KDB, Eximbank |

· First joint energy-security response since the 1965 normalization treaty

· An Asian energy alliance set against the China-Russia bloc

· Korea’s nuclear tech + Japan’s hydrogen tech = complementary synergy

· Aligned with US LNG-export expansion → room to cooperate with the Trump administration

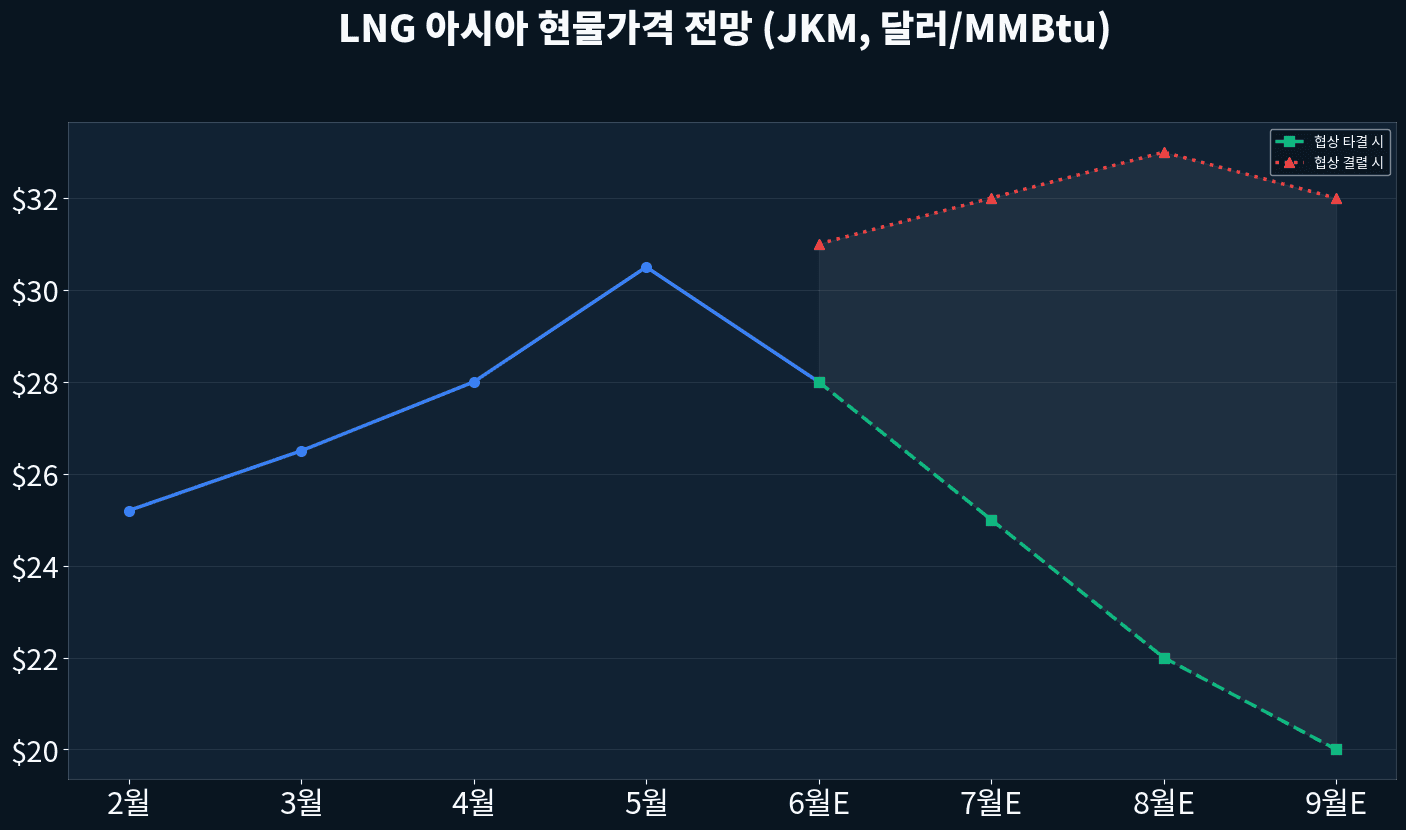

06 | LNG Price Outlook — How Far Could Prices Fall on a Deal?

Asian LNG spot (JKM) is around $30/MMBtu — up 67% from the pre-Iran-war level (~$18). If Iran negotiations succeed, the reopening of Hormuz normalizes supply and JKM could slide to $22-25. Layer on Korea-Japan joint procurement and another 5-10% discount drags the effective import price down to $20-22.

| Scenario | JKM Spot | Korea Landed Price | Power Tariff | Annual Savings |

|---|---|---|---|---|

| Current (war continues) | $30/MMBtu | $33 | Unchanged | — |

| Iran deal lands | $20-23 | $22-25 | -15 to -20% | ~KRW 5-8 tn |

| + Joint procurement | $18-20 | $20-22 | -25 to -30% | ~KRW 8-12 tn |

| War drags / talks fail | $35-40 | $38-43 | +15 to +20% | Added losses |

| Target (2028) | $15-18 | $17-20 | Normalized | Pre-ME-stress level |

A sharp LNG drop can dent KOGAS’s near-term profitability. But the heavy weight of long-term contracts limits direct spot-price damage. The likelier path is a virtuous cycle: price stability → tariff relief expectations → KOGAS normalization.

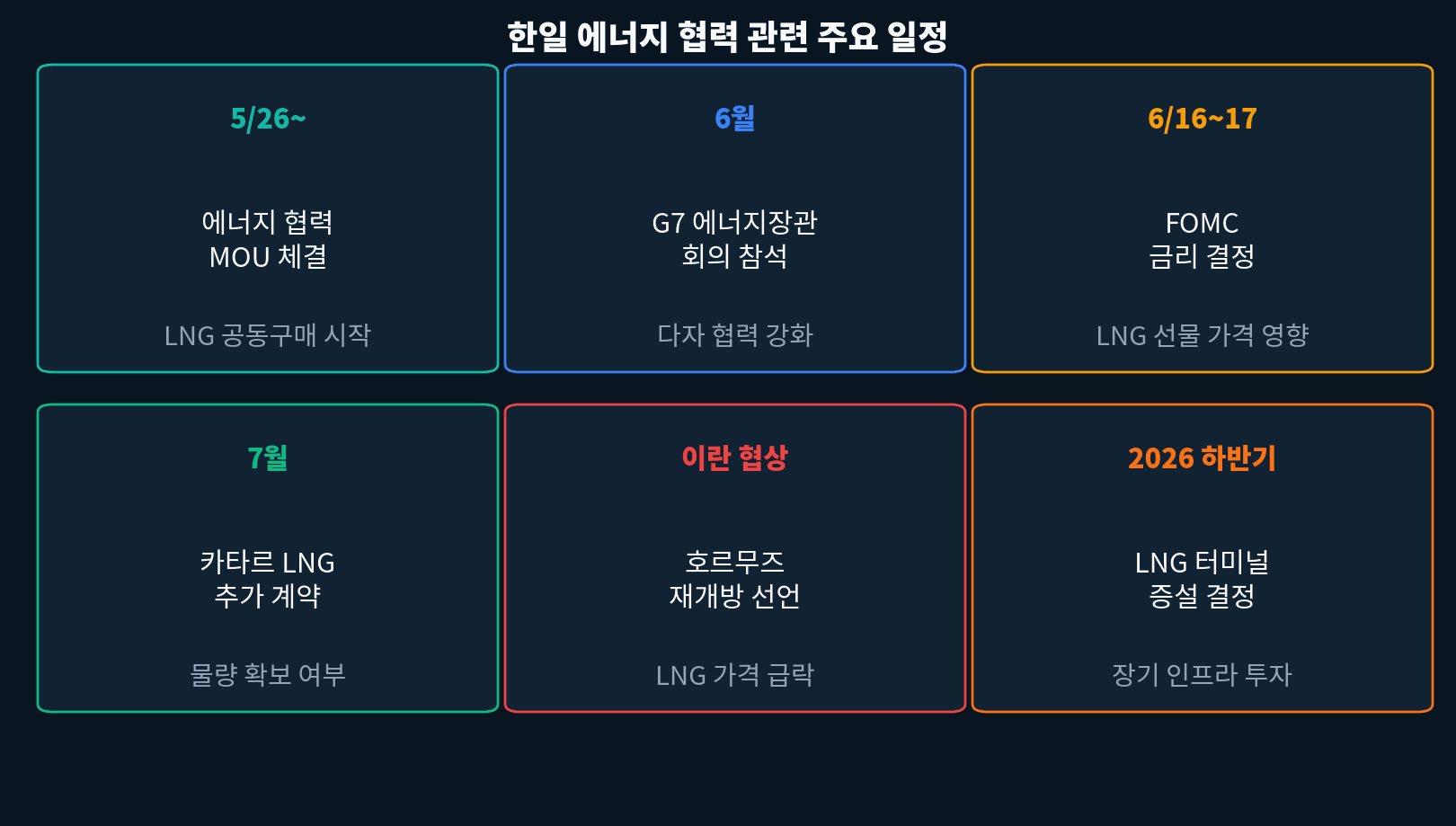

07 | Key Calendar & Monitoring Points

The pace of Korea-Japan energy cooperation and the outcome of Iran negotiations will dictate energy-sector prices. Watch especially the timing of the joint LNG procurement MOU and long-term contract news with Qatar and Australia.

| Date | Event | Beneficiary Sector | Watch Item |

|---|---|---|---|

| After 5/26 | Korea-Japan energy MOU signing | KOGAS · Shipbuilders | Joint procurement volume |

| June | G7 Energy Ministers’ Meeting | All energy names | Additional US LNG supply |

| 6/16-17 | FOMC — rates on hold | Shipbuilders · KOGAS | Stable funding costs |

| July | Qatar LNG add-on contracts | Korea Gas Corp. | Long-term volume lock-in |

| Iran deal | Hormuz reopens | Lower LNG prices | Landed-price relief |

| H2 2026 | LNG terminal expansion | HD Hyundai · Samsung | Long-cycle infra wins |

Each LNG carrier takes about 18-24 months to build, and current backlogs stretch 4-5 years. Vessels ordered today deliver in 2028-2030 — mid-to-long-term earnings are effectively pre-booked.

= a three-step energy-equity rally scenario

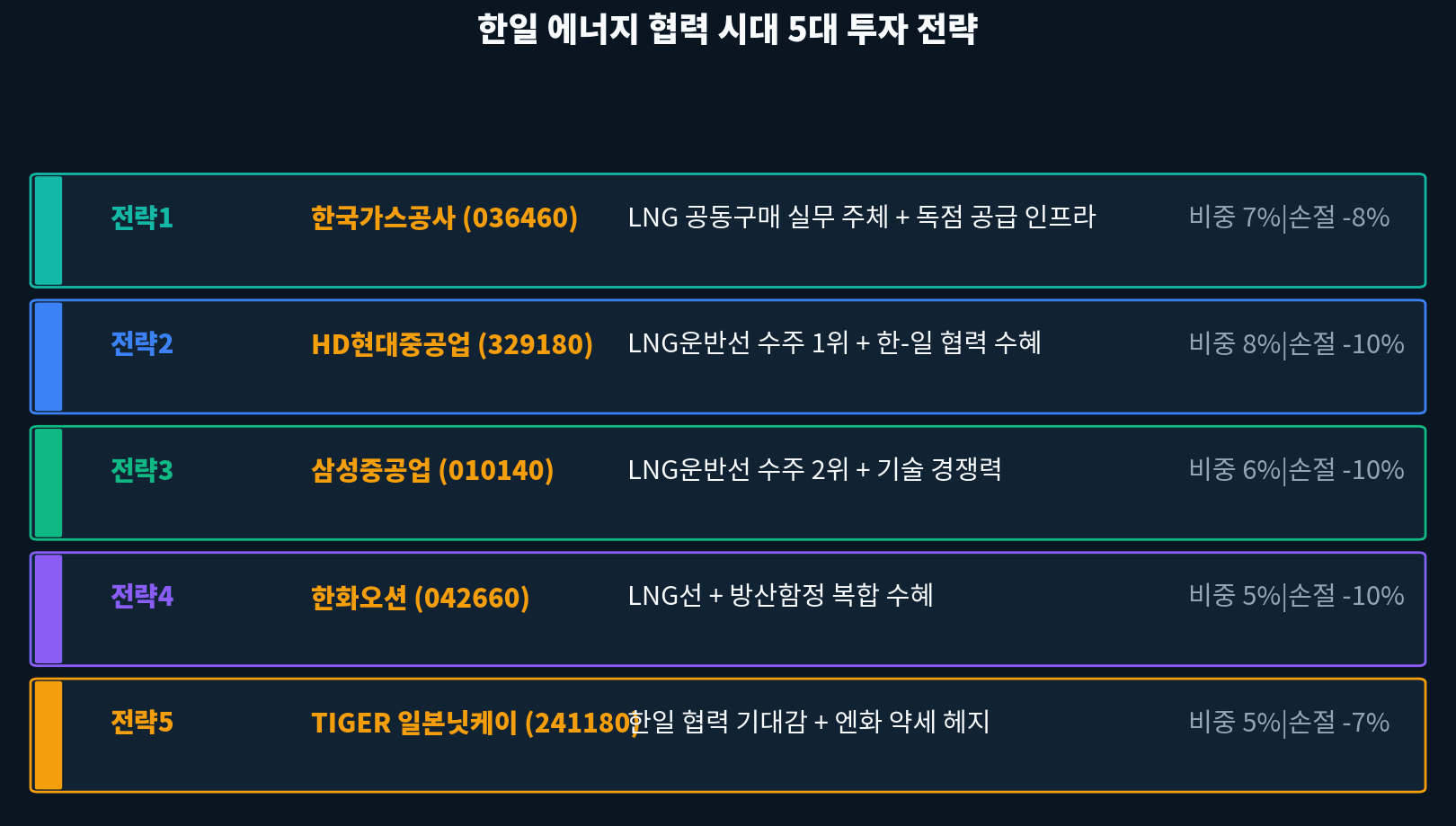

08 | Five Investment Plays for the Korea-Japan Energy Era

This portfolio reflects both Korea-Japan energy cooperation and the hope of an Iran-talks breakthrough. The core is LNG infrastructure (KOGAS, shipbuilders) and energy-security beneficiaries (nuclear, hydrogen), prioritizing names with long-contract-backed cash flow.

| Play | Name | Ticker | Stop | Weight | Core Thesis |

|---|---|---|---|---|---|

| ① LNG Core | Korea Gas Corp. | 036460 | -8% | 7% | Joint-buy executor |

| ② LNGC #1 | HD Hyundai Heavy | 329180 | -10% | 8% | World-leading backlog |

| ③ LNGC #2 | Samsung Heavy | 010140 | -10% | 6% | Tech + premium specs |

| ④ LNG + Defense | Hanwha Ocean | 042660 | -10% | 5% | Hybrid order book |

| ⑤ Japan Momentum | TIGER Nikkei ETF | 241180 | -7% | 5% | KR-JP cooperation play |

· Doosan Enerbility (034020): Beneficiary of joint Korea-Japan SMR development; KRW 20,000 target-price upgrade under review.

· Hyundai Motor (005380): Beneficiary of hydrogen-ammonia supply-chain build-out; Korea-Japan hydrogen logistics tie-up expected.

02. Korea+Japan 125Mt = 25% of global LNG trade, 5-10% price cut expected

03. Big-3 LNGC backlogs of 4-5 years lock in 2028-2030 earnings visibility

04. Korea self-sufficiency under 1%, ME 50% — SPR expansion to 150 days in play

05. Triggers: 5/26 MOU → July Qatar deal → Iran negotiations

06. Portfolio: KOGAS 7% · HD Hyundai 8% · Samsung 6% · Hanwha Ocean 5% · TIGER Nikkei 5%

Sources

- Korea Policy Briefing — Korea-Japan summit shuttle diplomacy crude & LNG agreement (2026.05.22)

- MOTIE — Energy Security Roadmap 2026-2028 (2026.04)

- Korea Gas Corp. IR — LNG Import Status & Joint Procurement Plan (2026.05)

- Kyunghyang Shinmun — Korea-Japan leaders’ energy agreement (2026.05.22)

- IEA — Energy Security in Asia-Pacific (2026.04)

- Bloomberg — Japan South Korea LNG joint purchase talks (2026.05.23)

This article is for informational purposes only and does not constitute a recommendation to buy or sell any specific security. Content reflects publicly available information as of 2026.05.25 and may not remain accurate as conditions evolve. All investments carry principal-loss risk; final responsibility rests with the investor.