Warsh Fed Chair sworn in — June FOMC, the rate path ahead, and a Warsh-era portfolio playbook

Trending · 2026.05.25

Warsh Takes Helm at the Fed — June FOMC Hold Likely, First Cut Eyed for September

Kevin Warsh was sworn in as Federal Reserve Chair on May 22, 2026. With inflation at 3.5%, a June FOMC hold looks all but certain, and markets are now watching whether Warsh signals a September cut.

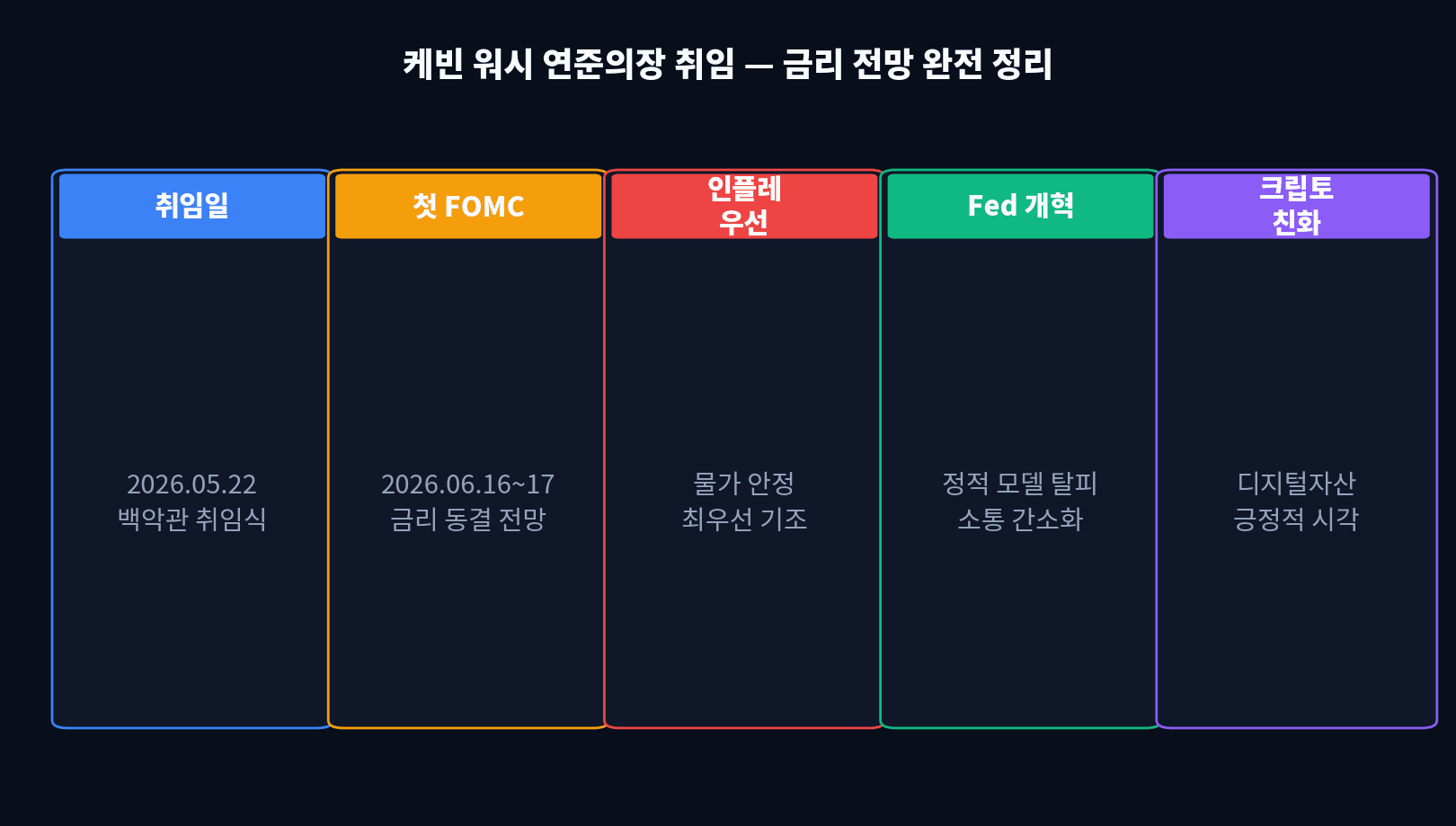

Kevin Warsh was officially sworn in as Chair of the U.S. Federal Reserve on May 22, 2026. Unlike his predecessor Jerome Powell, Warsh has placed inflation suppression at the very top of his agenda and pledged to overhaul the Fed’s communication style and policy models.

Despite intense pressure from President Trump to cut rates immediately, Warsh has insisted the Fed “will cut only when the data allows it,” underscoring central bank independence. With his first FOMC meeting set for June 16–17, global markets are watching every word Warsh utters.

| Item | Detail | Market Read |

|---|---|---|

| Sworn in | May 22, 2026 | Within expectations |

| First FOMC | June 16–17, 2026 | Cut probability ~10% |

| Current Fed funds rate | 3.75% | Down from 4.25% (Dec 2025) |

| CPI inflation | 3.5% (April) | Well above 2% target |

| Warsh’s core stance | Inflation suppression first | Read as hawkish |

“Price stability is the foundation of economic prosperity. We will restore it — methodically, transparently, and without political influence.”

01. Who Is Kevin Warsh — Crisis-Tested, Market-Friendly, Hawkish on Inflation

Warsh served as a Federal Reserve Governor from 2006 to 2011 under the George W. Bush administration, deeply involved in the 2008 financial crisis response. He later continued monetary policy research at Stanford’s Hoover Institution, building a reputation as market-friendly yet uncompromisingly hawkish on inflation.

President Trump nominated Warsh as Powell’s successor following the end of Powell’s term in May 2026, and the Senate confirmed him in February 2026. The market’s hawkish read on Warsh is well grounded — and the contrast with Powell is sharp.

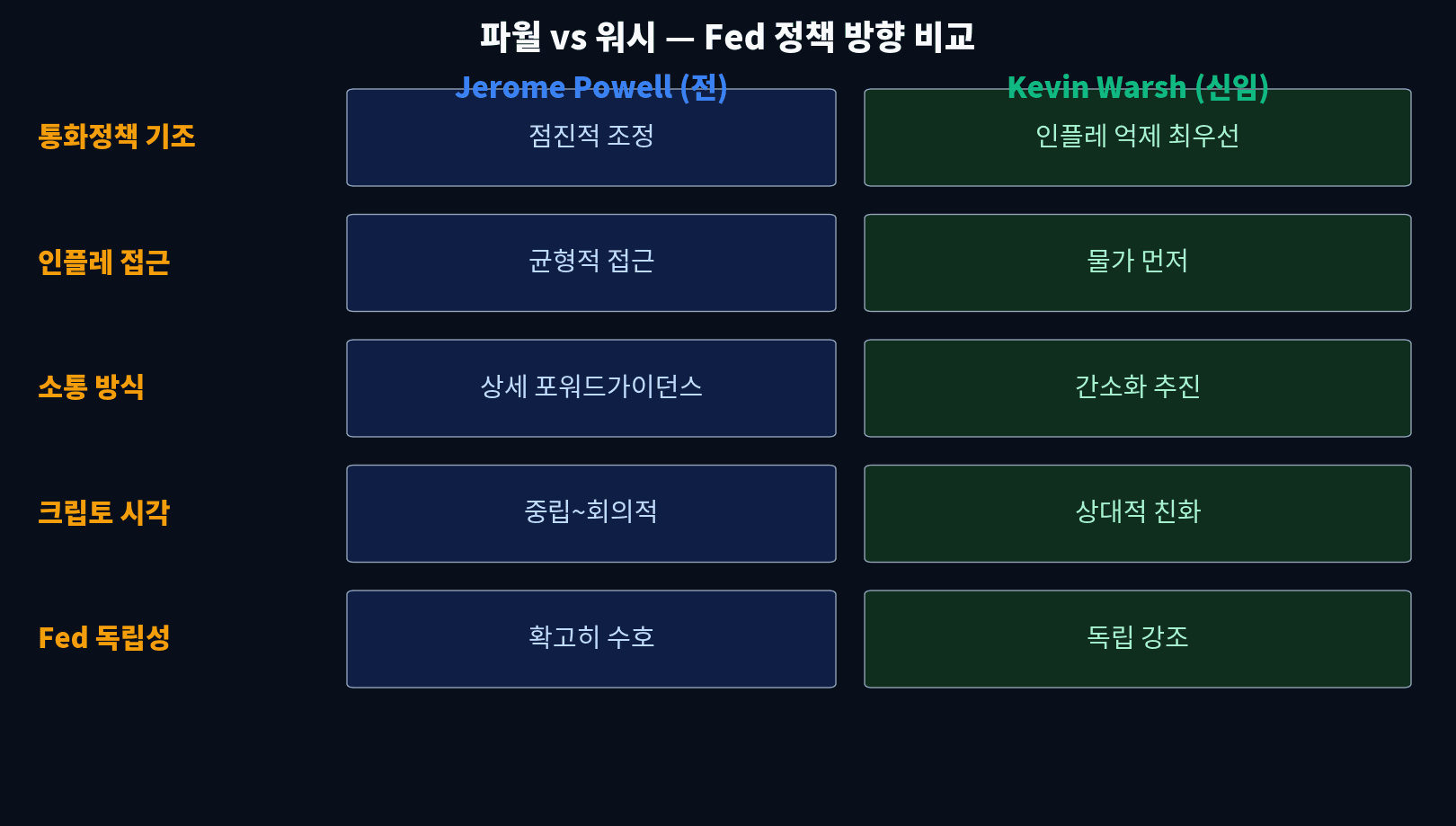

| Dimension | Powell (former) | Warsh (new) |

|---|---|---|

| Policy philosophy | Gradual, balanced | Inflation suppression first |

| Inflation approach | Balanced | Prices first, growth later |

| Communication | Detailed forward guidance | Simplified, proven by action |

| Crypto stance | Neutral to skeptical | Relatively friendly, pro-institutionalization |

| Fed independence | Firmly defended | Emphasized, openly rejects Trump pressure |

| Model usage | Static-model reliant | Diverse data + intuition |

“The Fed’s independence is not a luxury — it is a necessity. We will make decisions based on data, not on political pressure.” — Kevin Warsh, inaugural press conference, May 22, 2026.

02. The Inflation Picture — Why Warsh Cannot Cut Rates Yet

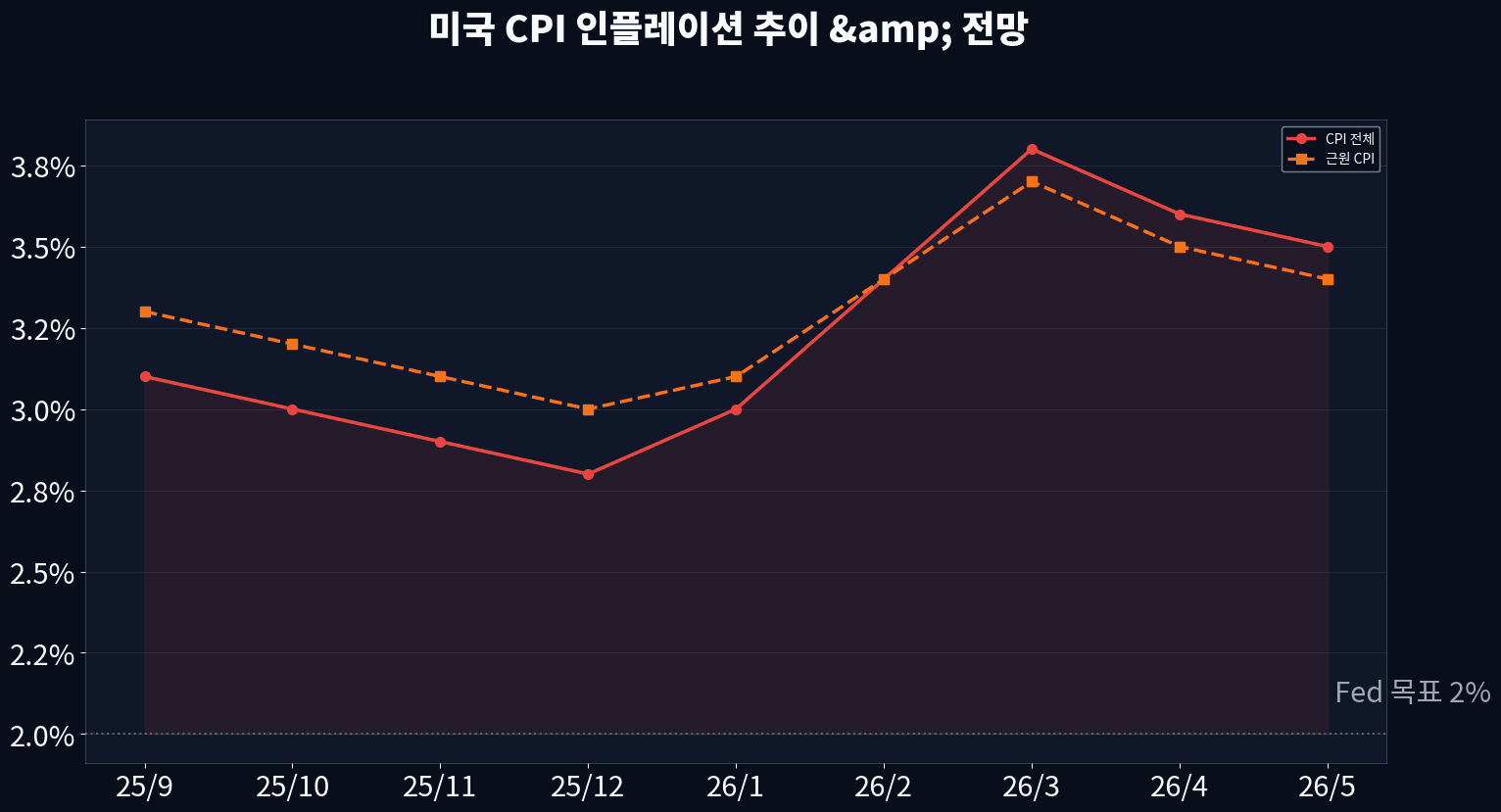

U.S. CPI had fallen to 2.8% by the end of 2025, but rebounded to 3.5% in April 2026 after the Iran war drove crude oil higher. That leaves a 1.5-percentage-point gap to the Fed’s 2.0% target — the structural reason Warsh cannot move to cut rates immediately.

| Indicator | Dec 2025 | Feb 2026 | Apr 2026 | Fed target | Gap |

|---|---|---|---|---|---|

| Headline CPI | 2.8% | 3.4% | 3.5% | 2.0% | +1.5pp |

| Core CPI | 3.0% | 3.4% | 3.4% | 2.0% | +1.4pp |

| PCE (Fed-preferred) | 2.5% | 3.1% | 3.2% | 2.0% | +1.2pp |

| Core PCE | 2.6% | 3.0% | 3.1% | 2.0% | +1.1pp |

| PPI (producer prices) | 2.2% | 3.5% | 3.8% | — | Re-acceleration risk |

Higher oil typically takes 2–4 months to feed through into CPI. Dubai crude is up roughly 30% since March, and that pass-through should hit CPI fully in May–June, adding fresh upside pressure to prices. This is the single biggest reason Warsh is expected to hold rates at the June FOMC.

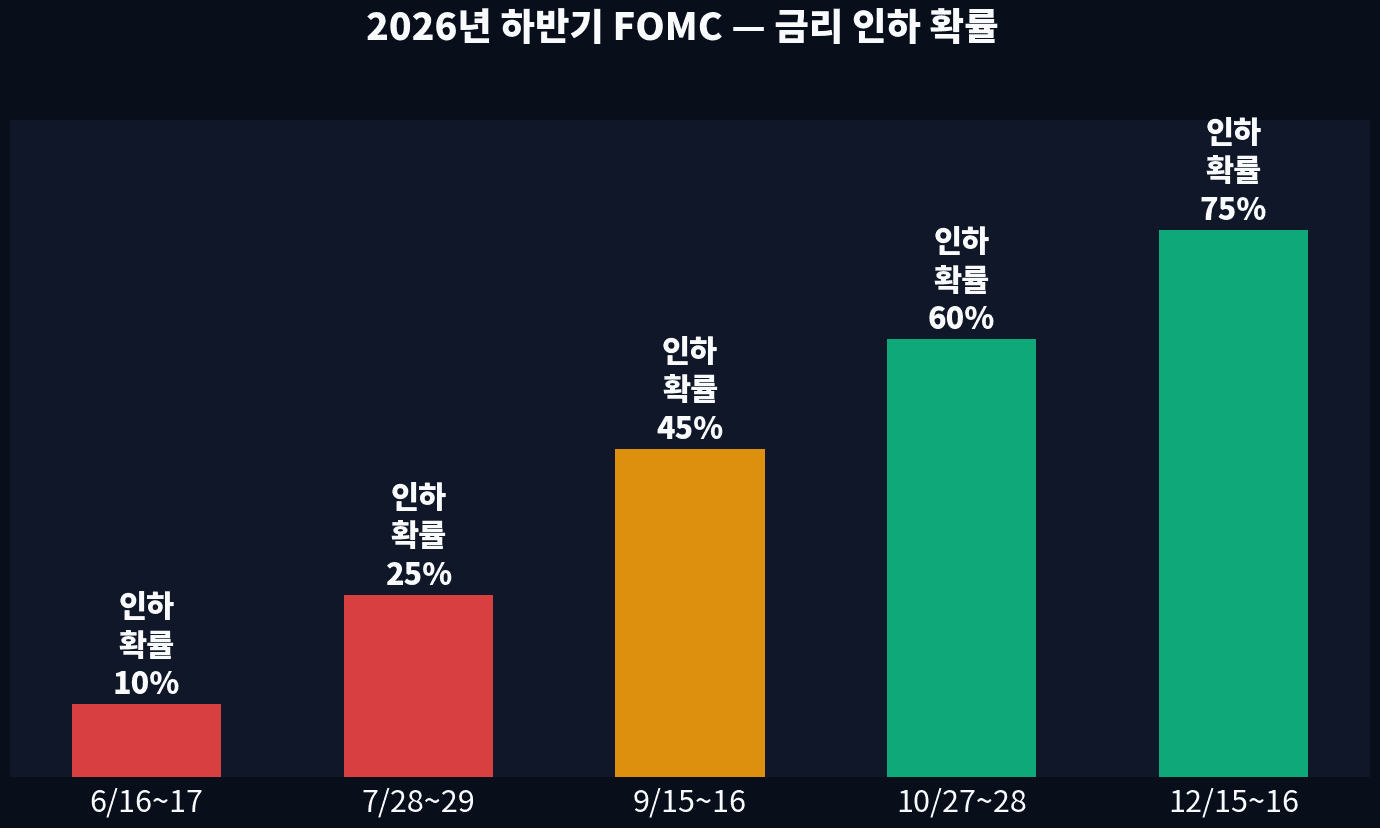

03. Rate Path Outlook — Warsh Holds in June, First Cut in September

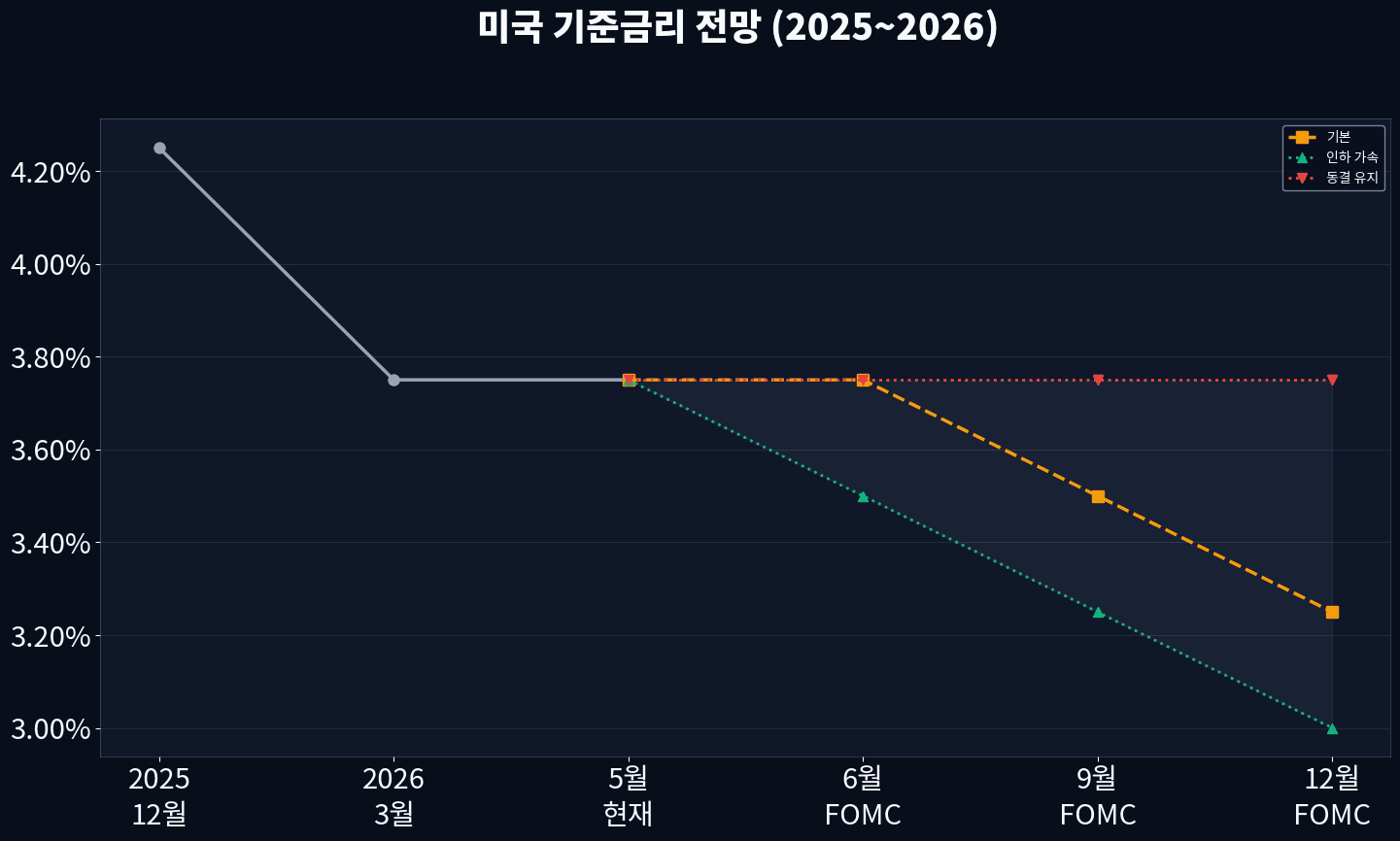

Market consensus heavily favors a rate hold at the June FOMC. CME FedWatch puts the probability of a June cut at under 10%. A first cut is more likely in September or December, with 1–2 cuts of 25 basis points each as the base scenario through year-end.

| FOMC date | Current rate | Cut probability | Scenario |

|---|---|---|---|

| Jun 16–17, 2026 (1st) | 3.75% | 10% | Hold likely |

| Jul 28–29, 2026 (2nd) | 3.75% | 25% | Hold or possible cut |

| Sep 15–16, 2026 (3rd) | 3.75–3.50% | 45% | First cut likely |

| Oct 27–28, 2026 (4th) | 3.50–3.25% | 60% | Back-to-back cuts possible |

| Dec 15–16, 2026 (5th) | 3.25–3.00% | 75% | Year-end 3.00–3.25% |

President Trump has repeatedly posted on social media demanding that Warsh “cut rates right now.” Warsh has explicitly responded that the Fed “does not react to political pressure,” cementing its independence. The longer this standoff drags on, the more market volatility it is likely to inject.

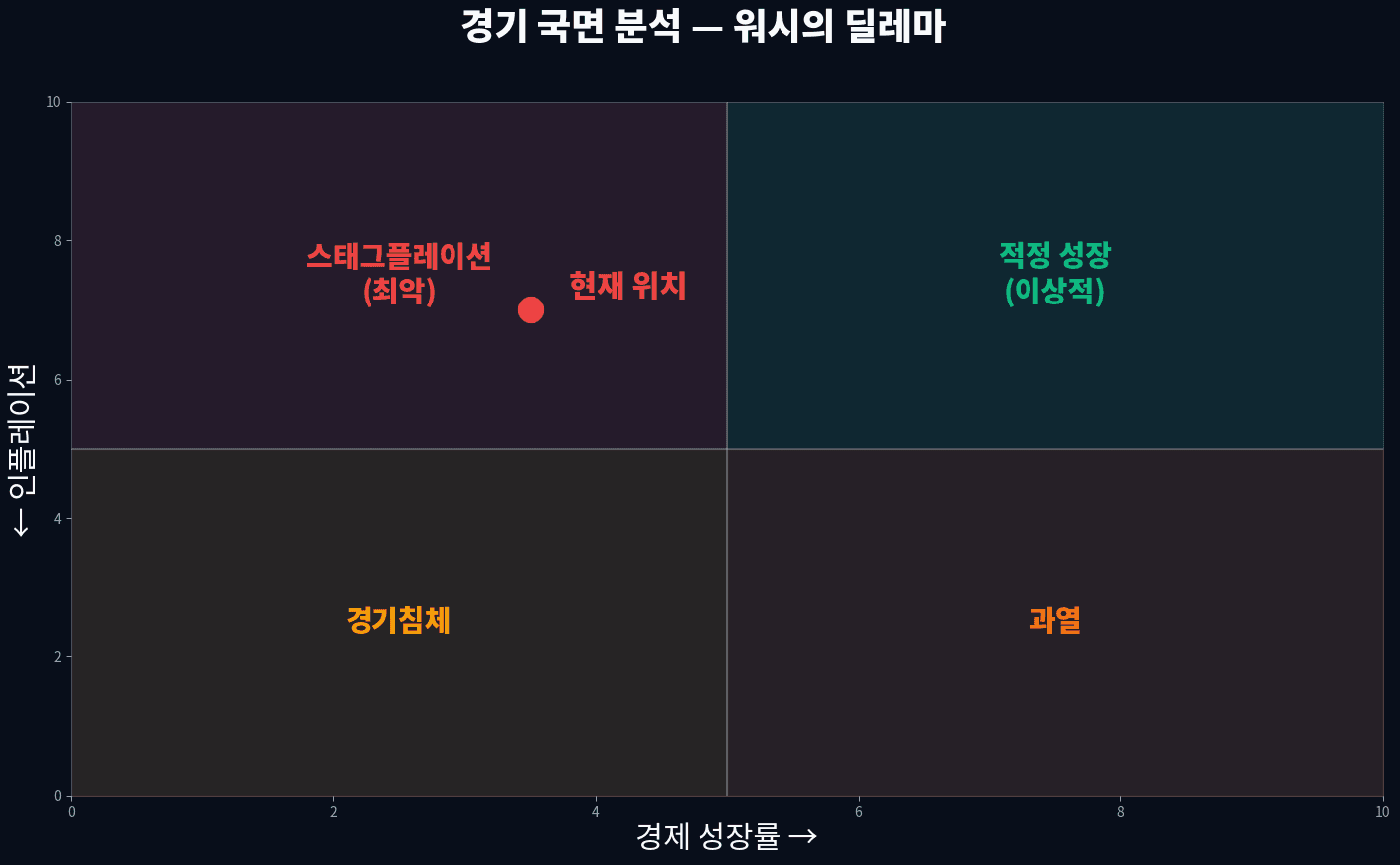

04. Stagflation Risk — Warsh’s Biggest Dilemma

The biggest challenge facing Warsh is stagflation — high inflation combined with weak growth. The Iran war is pushing oil prices up, lifting headline inflation while simultaneously slowing the economy. Hiking would kill growth further; cutting would re-ignite inflation. It is a textbook policy trap.

| Scenario | Growth | Inflation | Rate path | Investment posture |

|---|---|---|---|---|

| Soft landing | 2.0–2.5% | 2.5–3.0% | First cut in September | Balanced stocks + bonds |

| Stagflation | 0.5–1.0% | 3.5–4.5% | Hold or hike | Gold, USD, commodities |

| Recession | Negative | Below 2.0% | Emergency cuts | Bonds + cash |

| Overheating | 3.0%+ | Below 2.0% | Further hikes | Stocks + real estate |

| Current base case | 1.5–2.0% | 3.0–3.5% | Hold maintained | Diversified portfolio |

- Sticky prices: May–June CPI above 3.5% would sharply raise stagflation risk.

- Slowing growth: Q2 GDP under 1.0% would be a clear warning.

- Rising unemployment: May nonfarm payrolls (June 5) below 200k would be a weak-side signal.

- Warsh’s tone: July FOMC commentary is pivotal — does Warsh stay hawkish or pivot dovish?

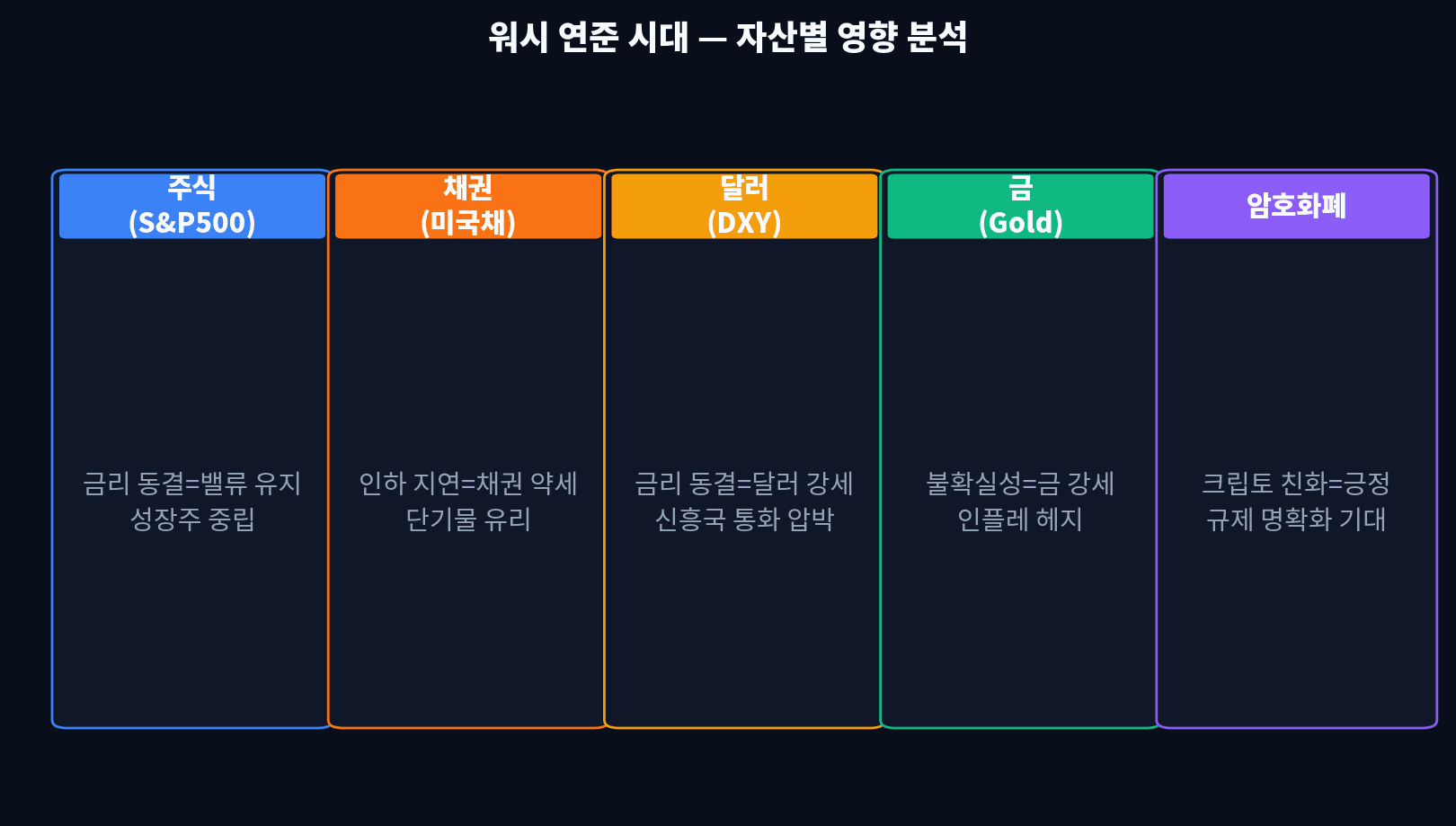

05. Asset Class Impact — Rebuilding Portfolios for the Warsh Era

The longer rates stay on hold, the more portfolio construction has to shift. Short-duration bonds and gold offer stability, while growth equities face continued valuation pressure. Crypto stands to benefit from Warsh’s relatively friendly stance and institutionalization momentum.

| Asset class | If rates stay on hold | If Fed cuts | Warsh-specific note |

|---|---|---|---|

| S&P 500 equities | Valuations steady, growth-stock neutral | Upside expected | AI growth premium coexists |

| U.S. 10Y Treasuries | Prices weak, yields at peak | Sharp rally expected | Front-run cuts via futures |

| U.S. dollar (DXY) | Stronger for longer | Pivot to weakness | Pressure on USD-pegged currencies |

| Gold | Stronger on uncertainty hedge | Strength continues | Inflation-hedge demand sticky |

| Cryptocurrencies | CLARITY Act tailwind | Upside leverage | Warsh-friendly = positive catalyst |

The U.S. Senate recently passed the CLARITY Act, the long-awaited crypto regulation framework. It classifies Bitcoin and Ethereum as commodities, separating them from SEC oversight. Combined with Warsh’s crypto-friendly stance, this gives digital assets a clear positive momentum.

06. H2 FOMC Calendar — Tracking Warsh’s Rate-Cut Probabilities

Five rate decisions remain between the June and December FOMC meetings. The outcome of Iran negotiations and the May–June CPI prints will be the key variables shaping the back-half rate path. If oil falls on a diplomatic breakthrough, Warsh could pull the first cut forward to September.

| FOMC | Date | Expected outcome | Cut probability | Key leading indicators |

|---|---|---|---|---|

| 1st (Warsh’s first) | Jun 16–17 | Hold | 10% | May CPI (6/11), payrolls (6/5) |

| 2nd | Jul 28–29 | Hold or -25bp | 25% | Q2 GDP, June CPI |

| 3rd | Sep 15–16 | -25bp likely | 45% | Jackson Hole hint (late Aug) |

| 4th | Oct 27–28 | -25bp | 60% | Q3 GDP, Iran situation |

| 5th | Dec 15–16 | -25bp | 75% | Annual inflation target progress |

Warsh will likely use the Jackson Hole economic symposium in late August to telegraph the back-half rate direction. If a September cut is on the table, expect his late-August remarks to land as a clear “ready to cut” signal.

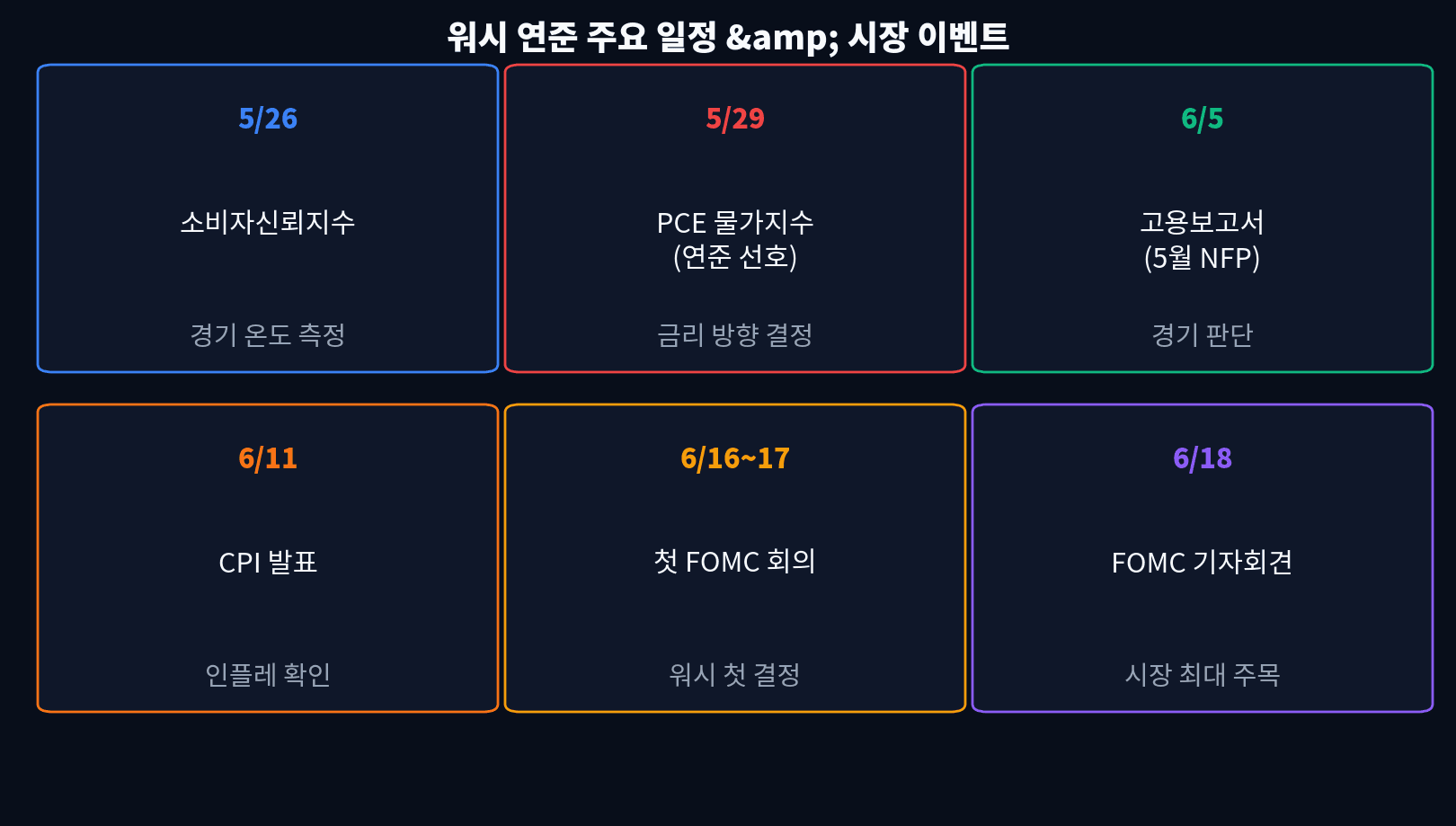

07. This Week’s Key Data — The Inputs Behind Warsh’s First FOMC

The economic data hitting this week and next month will largely dictate Warsh’s first FOMC decision. The May 29 PCE inflation print and the June 5 nonfarm payrolls report stand out as the two most decisive data points.

| Date | Indicator | Consensus | Meaning |

|---|---|---|---|

| 5/26 (Mon) | U.S. Consumer Confidence (Conference Board) | 98 | Gauge of consumer resilience |

| 5/29 (Thu) | PCE Price Index (April) | 3.0–3.2% | Fed’s preferred gauge |

| 6/5 (Fri) | Nonfarm Payrolls (May NFP) | 170k | Labor market strength |

| 6/11 (Wed) | CPI (May) | 3.3–3.6% | Captures May oil pass-through |

| 6/16–17 | FOMC meeting | Hold expected | Warsh’s first official decision |

| 6/18 (Wed) | FOMC decision & press conference | — | Top market focus |

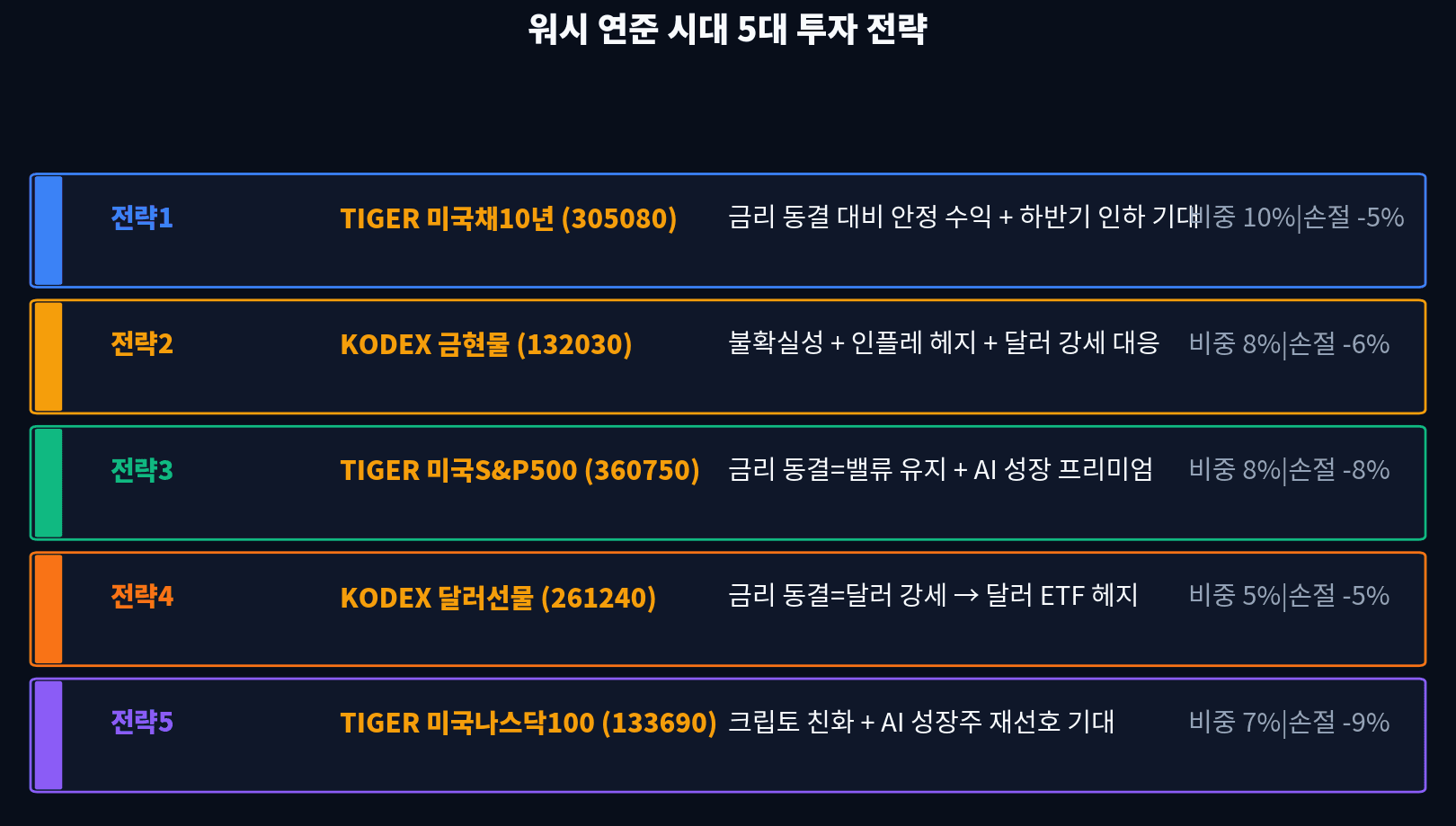

08. Five Investment Strategies for the Warsh Era — Bonds, Gold, USD Mix

Here is a portfolio playbook tuned for an extended Warsh-era hold. The core idea: short-duration bonds, gold and dollar hedges, and selective exposure to the AI growth premium — all balanced together.

| # | Strategy | Ticker (KRX) | Code | Stop | Weight | Core thesis |

|---|---|---|---|---|---|---|

| 1 | Front-run bond cuts | TIGER U.S. 10Y Treasury | 305080 | -5% | 10% | H2 cut expectations |

| 2 | Gold hedge | KODEX Gold Spot | 132030 | -6% | 8% | Inflation + uncertainty |

| 3 | S&P 500 core | TIGER U.S. S&P 500 | 360750 | -8% | 8% | Growth premium intact |

| 4 | USD hedge | KODEX USD Futures | 261240 | -5% | 5% | Rate hold = USD strength |

| 5 | Nasdaq growth | TIGER U.S. Nasdaq 100 | 133690 | -9% | 7% | Crypto + AI tailwind |

A successful Iran deal would push oil lower, drag CPI down, and could pull Warsh’s first cut into September. In that case, consider scaling the bond bucket from 10% to 15% and trimming the dollar ETF allocation.

□ 6/5 — Nonfarm payrolls (May NFP, consensus 170k)

□ 6/11 — May CPI release (consensus 3.3–3.6%)

□ 6/16–17 — Warsh’s first FOMC: confirm the hold

□ 6/18 — Watch Warsh’s press conference for September cut signals

□ Late August — Jackson Hole: H2 rate-direction hint

□ Monitor Iran negotiations for oil and CPI impact

Sources

- Federal Reserve — Kevin Warsh Confirmation & Inaugural Statement (2026.05.22)

- CME FedWatch — June FOMC Probability (2026.05.25)

- Bloomberg — Kevin Warsh takes helm at Federal Reserve (2026.05.22)

- Wall Street Journal — Warsh signals patience on rate cuts (2026.05.23)

- BLS — CPI April 2026 Report

- TheStreet — Stock Market Today: Dow hits record 50,580 (2026.05.22)

This article is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any specific security. All content is based on public information as of May 25, 2026. All investments involve risk of loss; please consult a licensed financial advisor before making decisions.