Petrodollar — is the era really cracking? Yuan surge, IMF and CIPS numbers tell the real story for Korean investors

Trending · May 25, 2026 · DIR

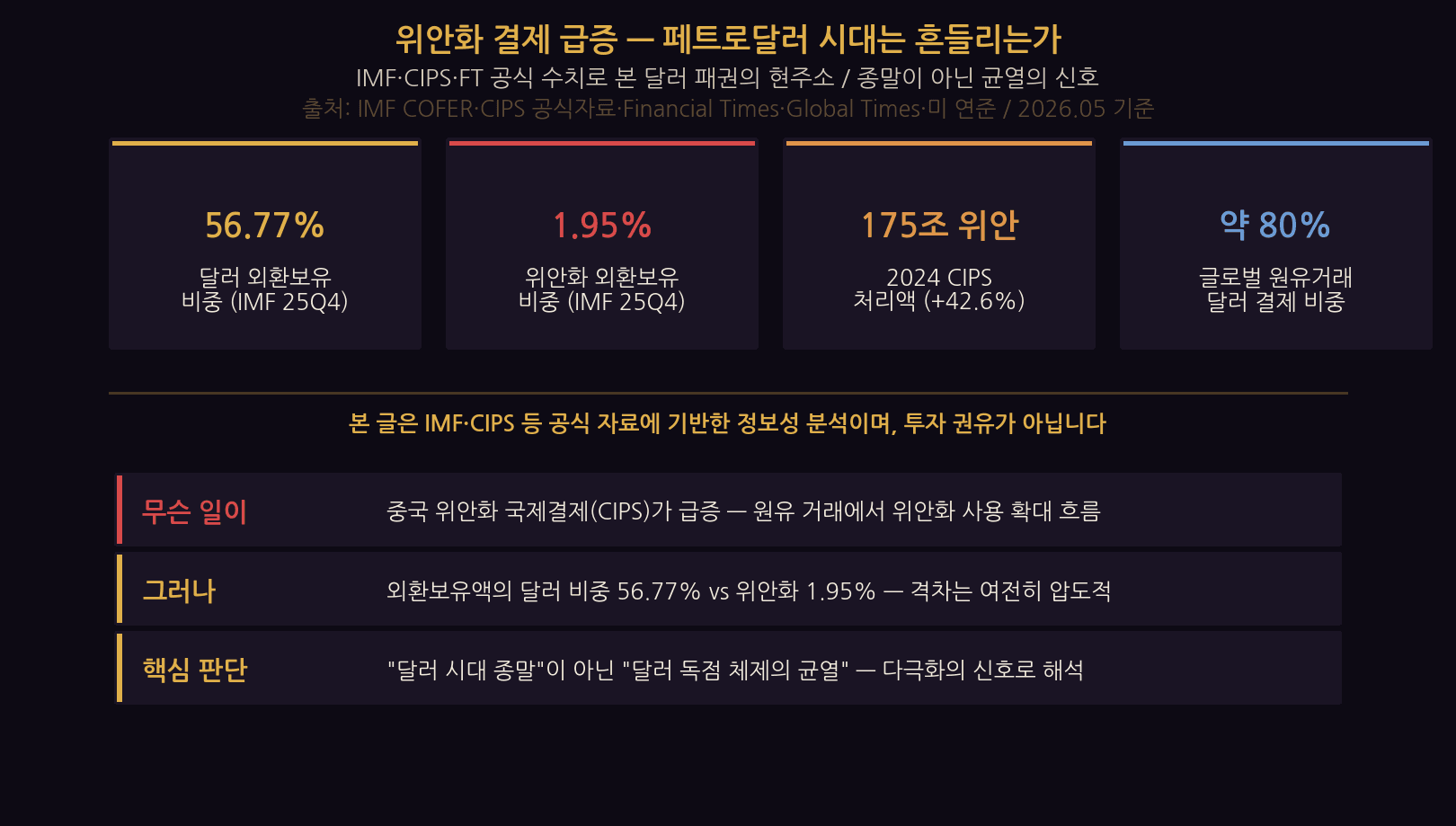

Is the Petrodollar era really cracking? We pressure-test the debate with hard numbers — surging yuan settlement, CIPS +42.6%, IMF reserves 56.77% USD vs 1.95% CNY — and lay out a calm view of dollar hegemony today, with implications for Korean investors.

A quiet but meaningful shift is taking place in global oil trade settlement: Chinese yuan use is rising fast. With the 2026 Iran war, geopolitical risk, US financial sanctions, and China’s yuan-internationalization push converging, analysts are calling cracks in the Petrodollar-only flow that has dominated for half a century.

This piece avoids vague forecasts and instead pressure-tests the Petrodollar debate with hard numbers from IMF, CIPS, and the Financial Times. The bottom line up top: today’s shift looks less like a “fall of the dollar” and more like “cracks in a dollar monopoly.” Primary sources: IMF COFER and Financial Times.

What the Petrodollar is — the root of 50 years of dollar hegemony

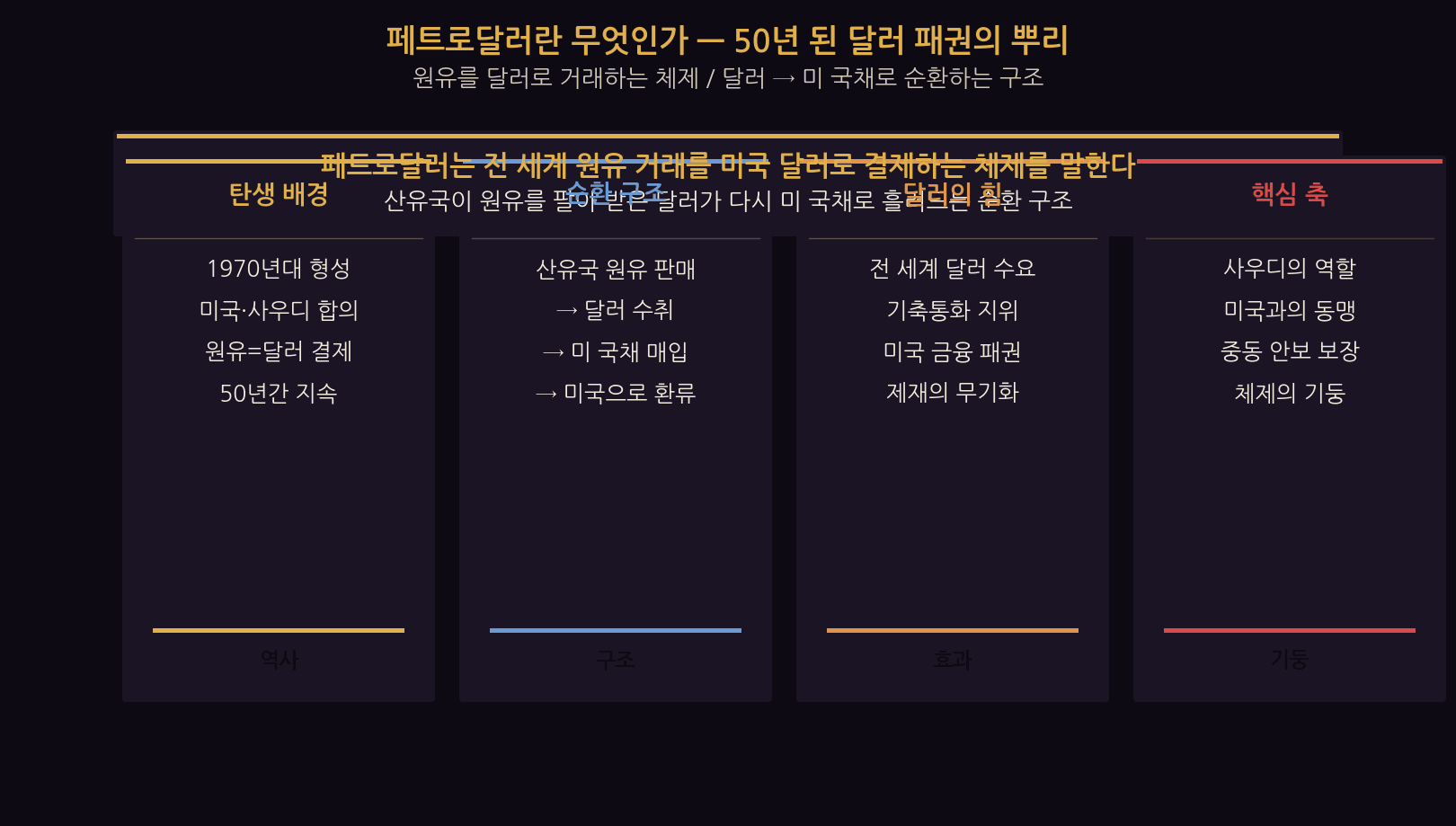

Before yuan, the Petrodollar itself needs defining. It refers to the system under which global oil trade is settled in US dollars — forged in the 1970s around US-Saudi understandings and durable for roughly 50 years.

The core is a recycling loop. Oil producers receive dollars for crude; those dollars flow back into US Treasuries and US capital markets. The world needs dollars to buy oil, dollars accumulate reserve status, and the US gains financial primacy — including the leverage of sanctions. Saudi’s role and the US alliance were pillars of this architecture.

| Item | Detail |

|---|---|

| Origin | 1970s — US-Saudi understandings |

| Core loop | Oil sold → USD received → US Treasuries bought |

| Effect | Global USD demand → reserve currency status |

| Duration | ~50 years |

Yuan settlement surges — CIPS in the official numbers

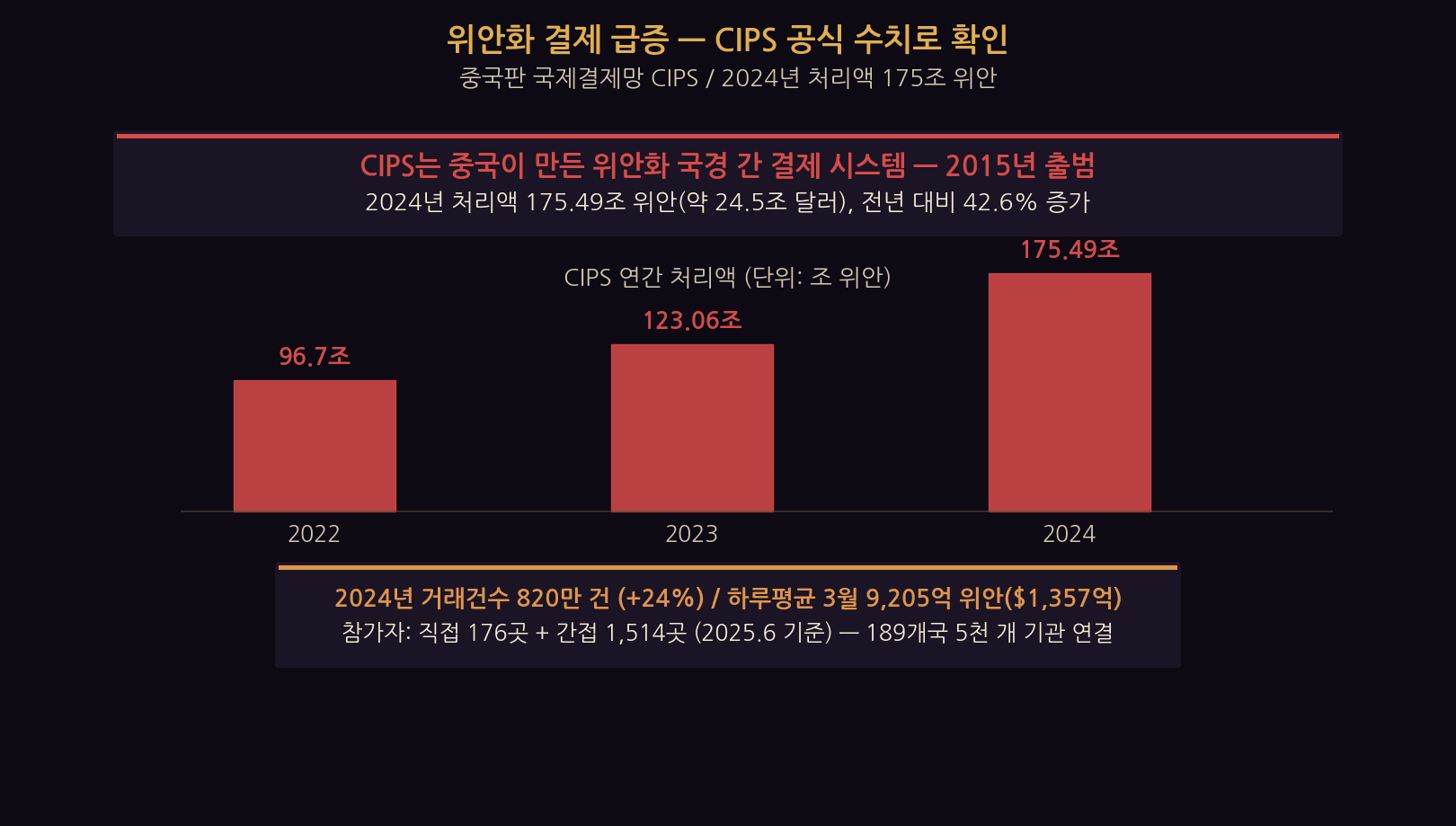

Now the heart of the shift. Yuan settlement is rising fast in global flows. At the center is CIPS — the Cross-Border Interbank Payment System — launched by China in 2015 as a yuan cross-border settlement rail.

The numbers back it up. 2024 CIPS throughput was RMB 175.49 trillion (~$24.5T), a +42.6% YoY jump, with 8.2 million transactions (+24%). FT reports CIPS daily-average value at RMB 920.5B (~$135.7B) in March 2026. Participants total 176 direct + 1,514 indirect (as of June 2025), reaching ~5,000 banks across 189 countries.

| Item | Value | Source |

|---|---|---|

| 2024 CIPS throughput | RMB 175.49T (+42.6%) | CIPS / Shanghai gov |

| 2024 transactions | 8.2M (+24%) | CIPS official |

| Daily avg (Mar 2026) | RMB 920.5B (~$135.7B) | Financial Times |

| Participants | 176 direct + 1,514 indirect | CIPS (Jun 2025) |

In 2024 CIPS processed RMB 175 trillion of cross-border yuan settlement, up 43% year-on-year.

— Shanghai government / CIPS official · Jan 2025

Why yuan is in focus for oil trade

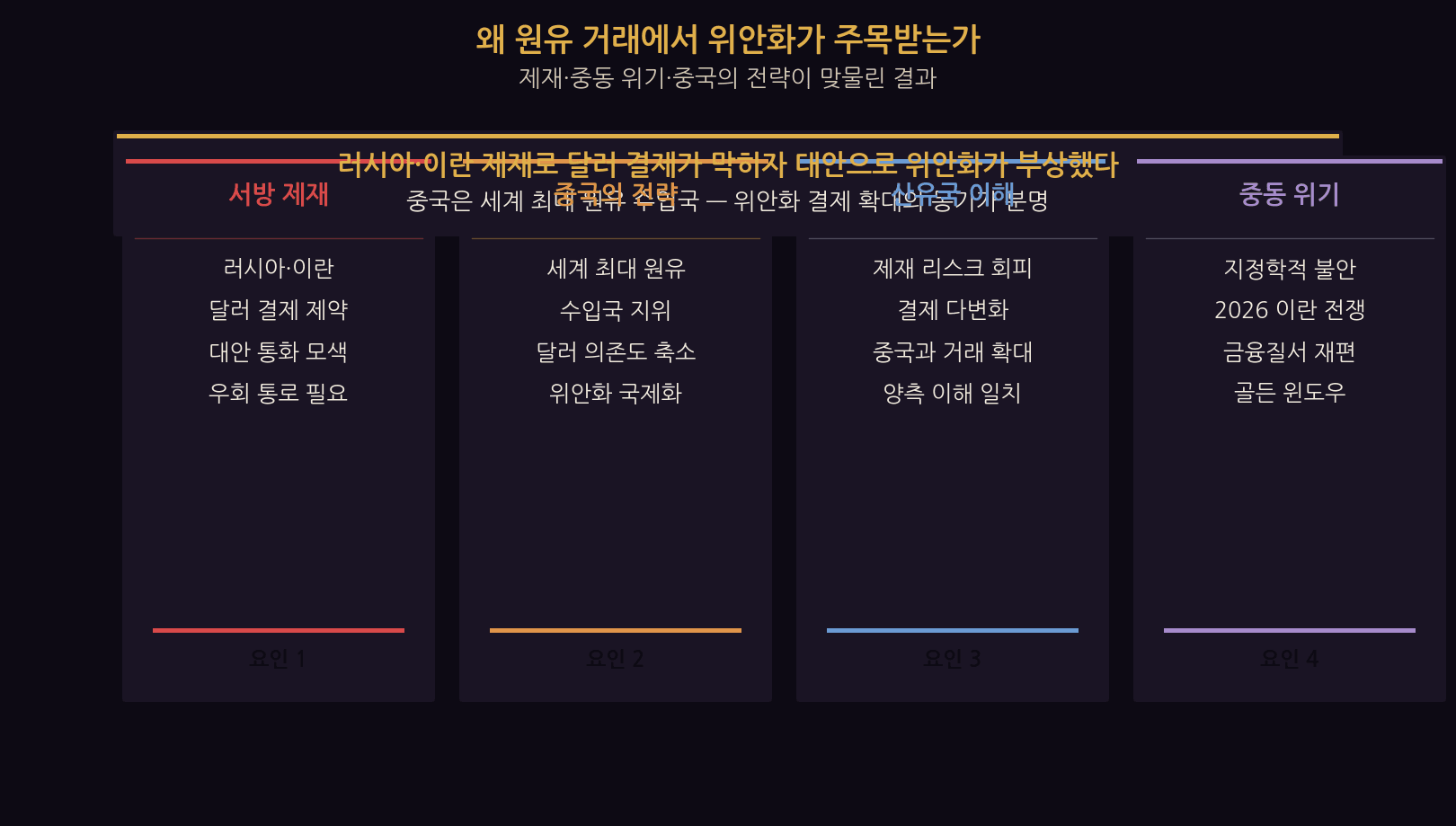

Why is oil trade the place where yuan suddenly draws attention? International oil pricing was almost entirely in US dollars. Several converging factors have changed the picture.

The biggest driver is Western sanctions. Russia and Iran face heavy USD-settlement constraints, pushing counterparties to alternatives — and yuan has stepped in. China is among the world’s largest crude importers, so paying in yuan lowers its dollar dependence. Oil exporters get a way to dodge sanctions risk. The 2026 Iran war added urgency to that financial-order rebalancing.

| Factor | Detail |

|---|---|

| Western sanctions | USD-settlement constraints on Russia/Iran |

| China strategy | Largest crude importer; lower USD dependence |

| Producer incentive | Avoid sanctions risk; diversify settlement |

| Mideast crisis | 2026 Iran war accelerates financial reshuffling |

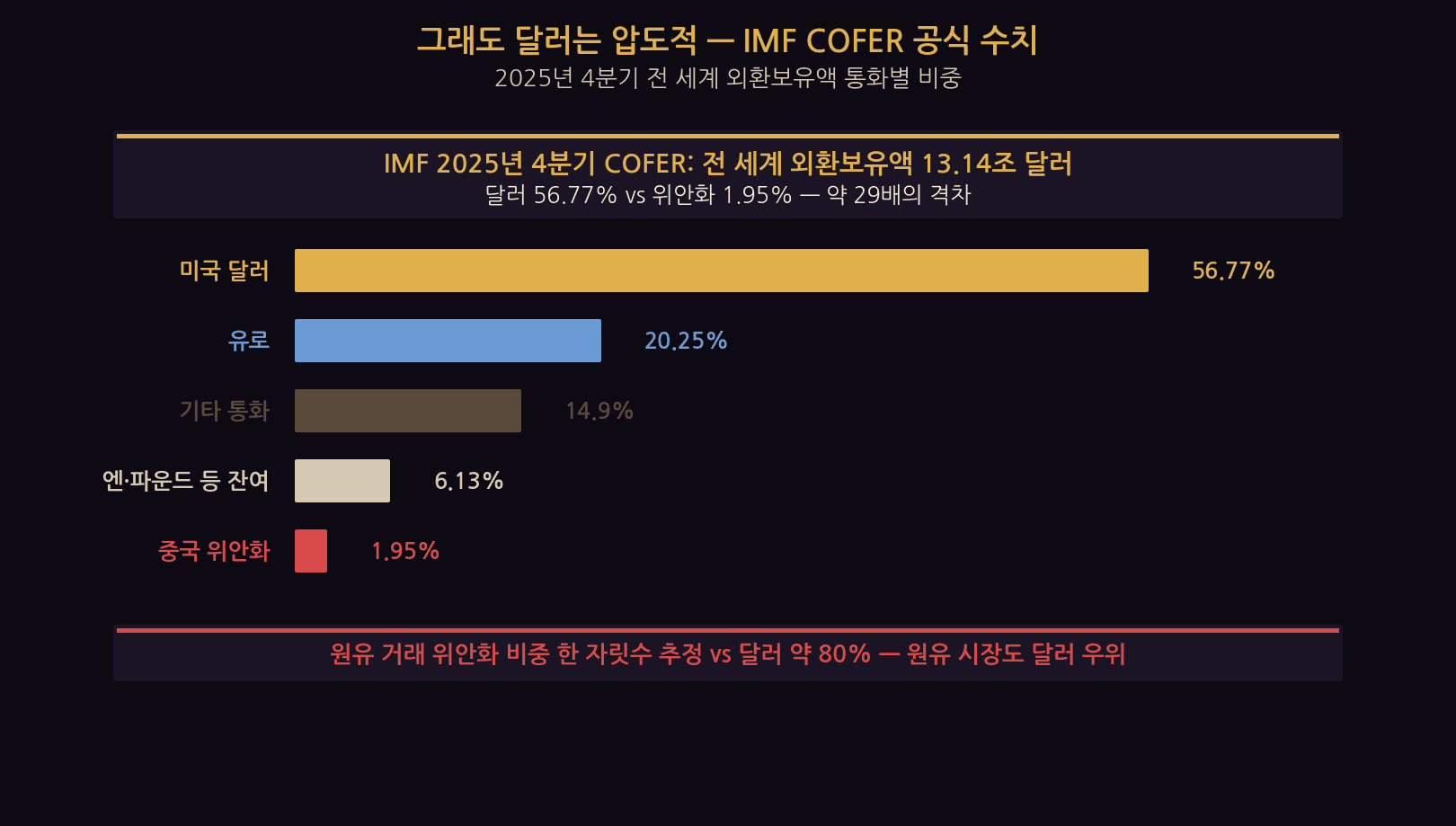

Yet the dollar dominates — IMF COFER in numbers

Yuan settlement is rising — that is real. But the gap is too wide to call “the Petrodollar era over.” IMF data makes this concrete.

The IMF’s March 2026 release of 2025 Q4 COFER shows global reserves of $13.14T allocated 56.77% to USD vs just 1.95% to CNY — a ~29x gap. Even adding euro (20.25%) and yen/pound, yuan stays marginal. In oil trade, USD is estimated near 80% versus a single-digit yuan share.

| Currency | Reserves share (2025Q4) | Note |

|---|---|---|

| USD | 56.77% | down from 56.93% prior quarter |

| EUR | 20.25% | down from 20.36% |

| CNY | 1.95% | up from 1.92% |

| Oil-trade USD | ~80% | CNY estimated single digits |

In 2025 Q4 the USD share of global reserves was 56.77%, slightly down from 56.93% in the prior quarter.

— IMF COFER data brief · Mar 27, 2026

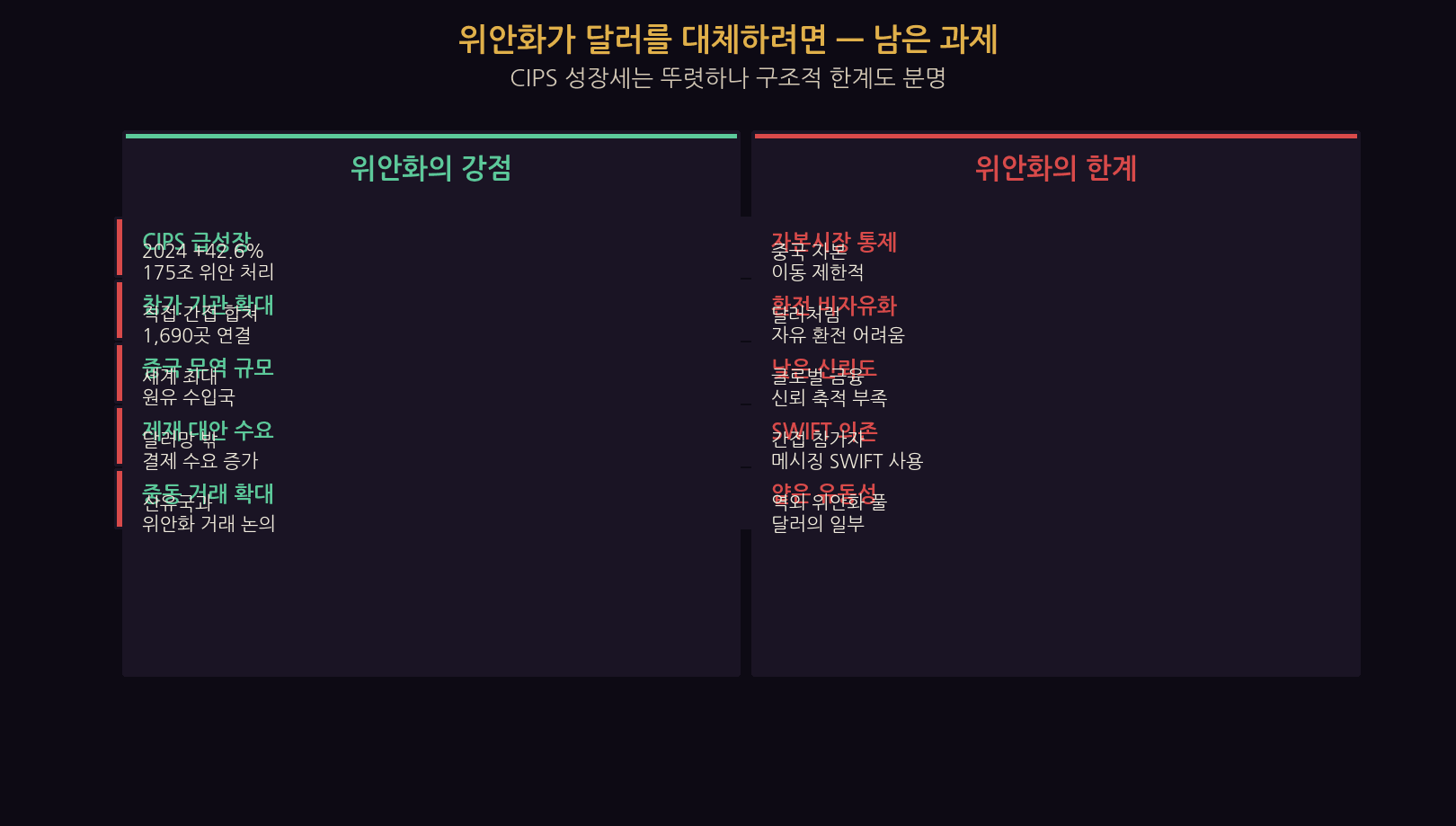

For yuan to replace the Petrodollar — outstanding issues

CIPS growth is real and visible. Yet for yuan to actually replace the dollar, much remains to be solved.

The biggest hurdle is China’s capital controls. Unlike USD, yuan is not freely convertible everywhere, and China restricts capital movement. Global financial trust has not accumulated the way it has for the dollar. Many CIPS overseas participants are indirect — still relying on SWIFT messaging. Offshore yuan liquidity pools are small versus USD pools. Replacement would require capital-market opening, convertibility, and global financial credibility together.

| Yuan strengths | Yuan limitations |

|---|---|

| CIPS 2024 +42.6% growth | Capital controls and restrictions |

| ~1,690 participants | Non-free convertibility |

| Largest crude importer | Limited global trust |

| Sanctions-alternative demand | Indirect users still on SWIFT |

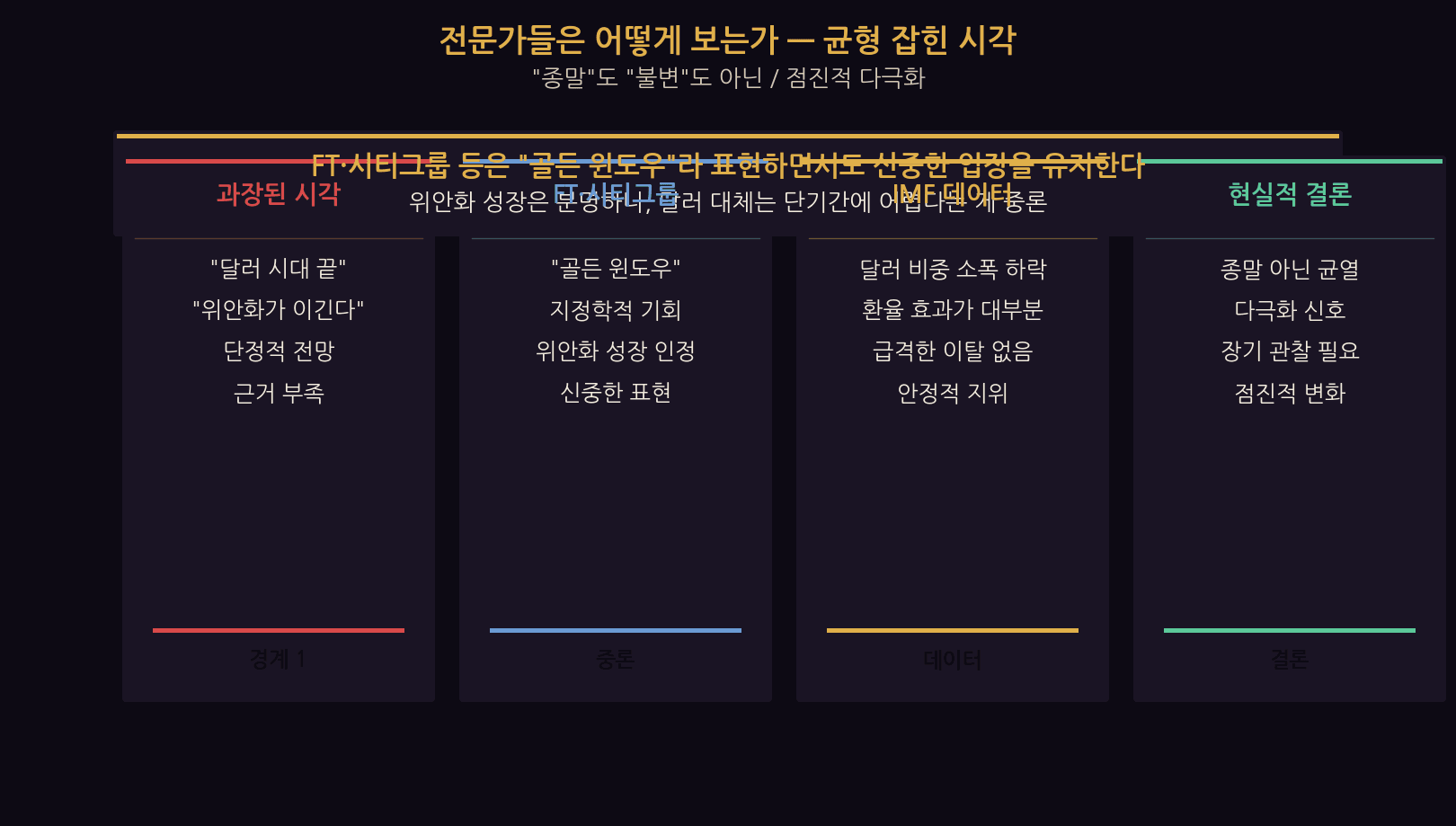

Expert views — a balanced read

How should this shift be read? Expert opinion lands between “the end” and “no change”.

The Financial Times described a “golden window” for yuan internationalization after the Iran war. Citi analysts agreed the geopolitical reshuffle opens an opportunity for broader yuan use. None argue yuan will replace USD imminently. IMF data shows much of the USD share decline reflects FX-valuation effects, not aggressive reserve diversification. The realistic read: today’s shift is not the fall of the Petrodollar but cracks in dollar monopoly.

| View | Detail | Read |

|---|---|---|

| Overstated | “Dollar era is over” | Weak evidence |

| FT / Citi | “Golden window” — opportunity | Yuan growth acknowledged |

| IMF data | USD drop reflects FX effects | No sharp exit |

| Realistic | Cracks, not collapse | Gradual multipolarity |

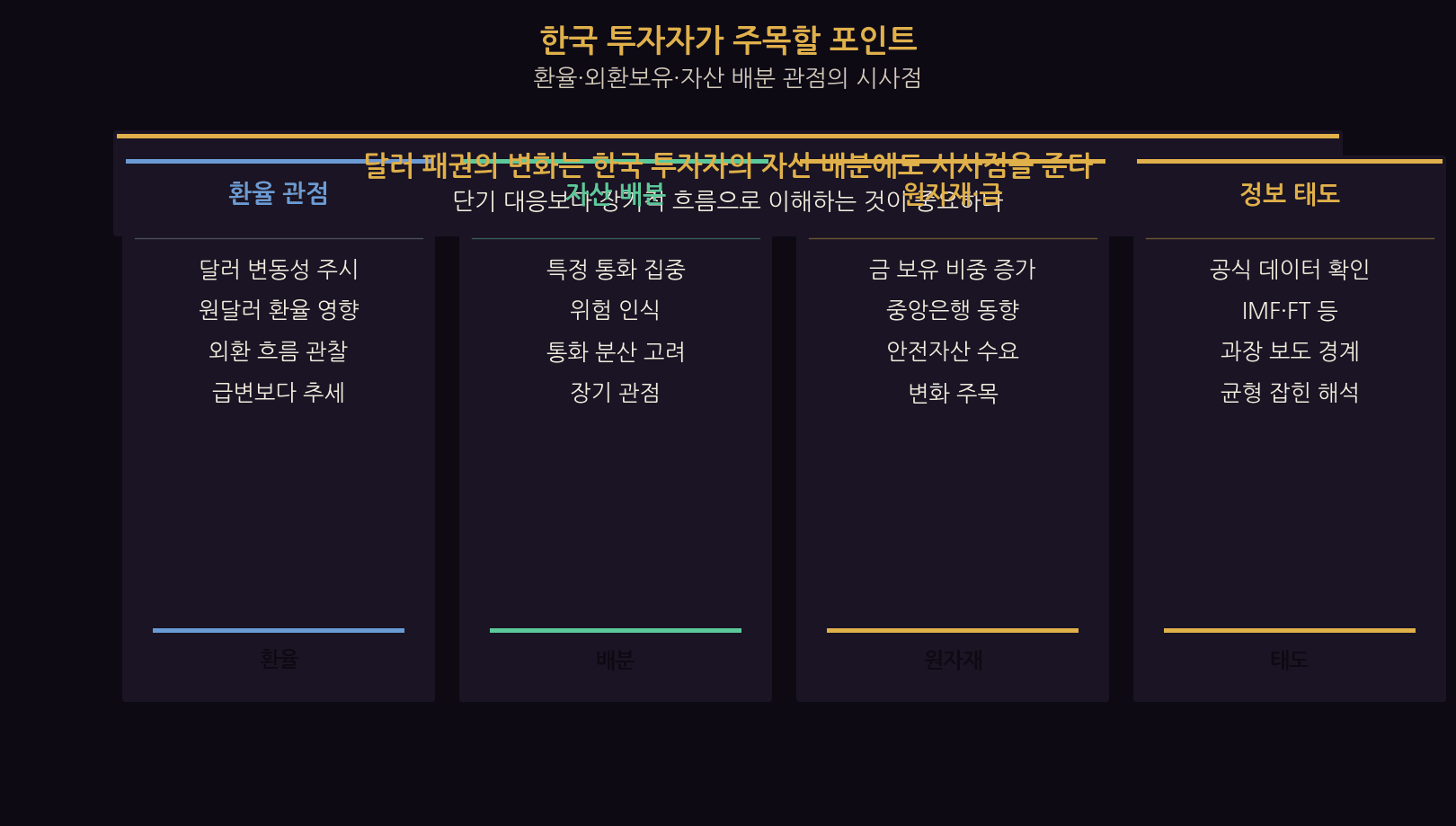

What Korean investors should watch

The broad shift carries implications for Korean investors too — better framed as a long-horizon trend than a short-term trade.

FX first: changes in Petrodollar dominance can translate into USD volatility, so watch USD/KRW trends. In asset allocation, recognize single-currency concentration risk and consider diversification. The trend of central banks raising gold holdings is worth attention from a safe-haven angle. Most of all, verify with primary sources like IMF and FT and watch for overstated coverage.

| Lens | Takeaway |

|---|---|

| FX | Watch USD volatility and USD/KRW trends |

| Allocation | Recognize single-currency risk; consider diversification |

| Commodities / gold | Note rising central-bank gold holdings |

| Information | Verify with primary data; guard against overstated coverage |

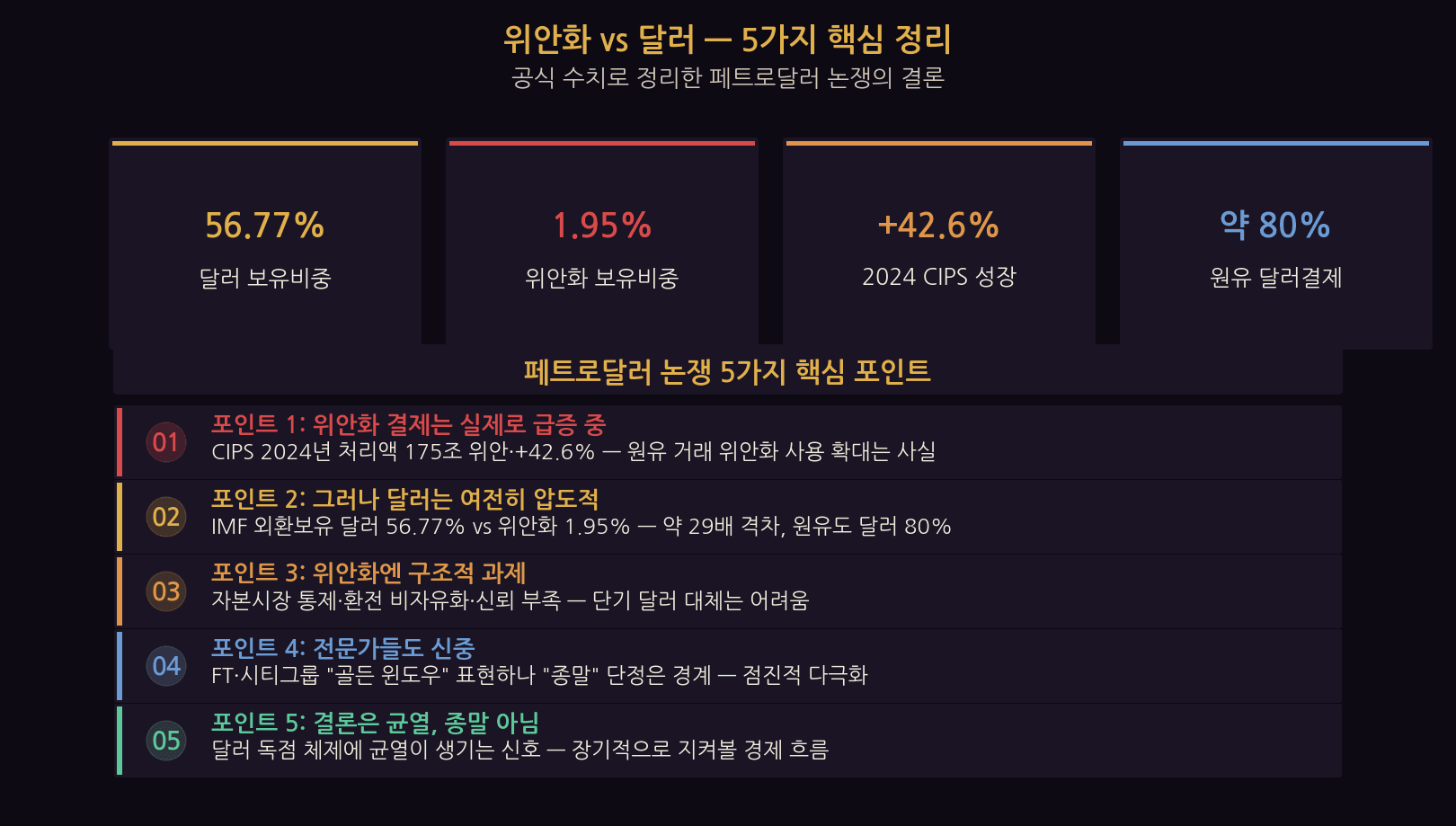

Petrodollar debate — five key points

| Point | Detail |

|---|---|

| 1. Yuan surges | CIPS 2024 throughput RMB 175T (+42.6%) — fact |

| 2. Dollar dominates | Reserves: USD 56.77% vs CNY 1.95% (~29x gap) |

| 3. Yuan hurdles | Capital controls, non-convertibility, limited trust |

| 4. Expert view | FT “golden window” — but “end” is overstated |

| 5. Conclusion | Not the end of the Petrodollar — cracks and multipolarity |

□ Reserves: USD 56.77% vs CNY 1.95% — IMF 2025Q4

□ Oil-trade USD ~80%; CNY estimated single digits

□ Yuan hurdles — capital controls, non-convertibility, trust

□ FT “golden window” — yuan growth acknowledged, “end” overstated

□ Conclusion — cracks and multipolarity, not the Petrodollar’s end

□ Currency-order change is a long-horizon trend — track official data

Sources

- IMF — Currency Composition of Official Foreign Exchange Reserves (COFER) data brief (Mar 27, 2026)

- CIPS / Shanghai gov — RMB globalization grows with expanding CIPS business (Jan 2025)

- Financial Times — Iran war opens ‘golden window’ for China’s renminbi (May 21, 2026)

- Global Times — PBC to enhance cross-border yuan payment (Oct 2025)

- US Federal Reserve — The International Role of the U.S. Dollar 2025 Edition

- CIPS official — participants and volume statistics (as of Jun 2025)

This article is for informational purposes based on official data from IMF, CIPS, and the Financial Times. It does not recommend any specific currency or asset. International monetary statistics depend on release date and methodology and can shift; FX markets move continuously. Investors bear sole responsibility for their decisions.