Capital Gains Tax Surcharge Ends — 5 Strategies for Multi-Home Owners After May 9

Trending · May 17, 2026

South Korea’s capital gains tax surcharge on multi-home owners resumed May 10, 2026, after a 4-year moratorium. 2nd home: +20%p, 3rd home: +30%p above the standard rate. Contracts signed by May 9 qualify for a 4–6 month grace period. Here are 5 strategies for owners navigating the change.

On May 9, 2026, South Korea’s four-year moratorium on the capital gains tax surcharge for multi-home owners officially ended. President Lee Jae-myung declared there would be no further extensions, stating that “no market can beat the government.” Starting May 10, owners of two homes in designated adjustment zones face a surcharge of +20 percentage points on top of the standard progressive rate, while owners of three or more homes face +30 percentage points. The special long-term holding deduction — which could reduce taxable income by up to 30% — is also suspended for affected properties, effectively doubling or tripling the tax burden compared to the moratorium period. Whether you have a contract in hand or are still weighing your options, the time to act is now.

Section 01 — By the Numbers: How Much More Will You Pay?

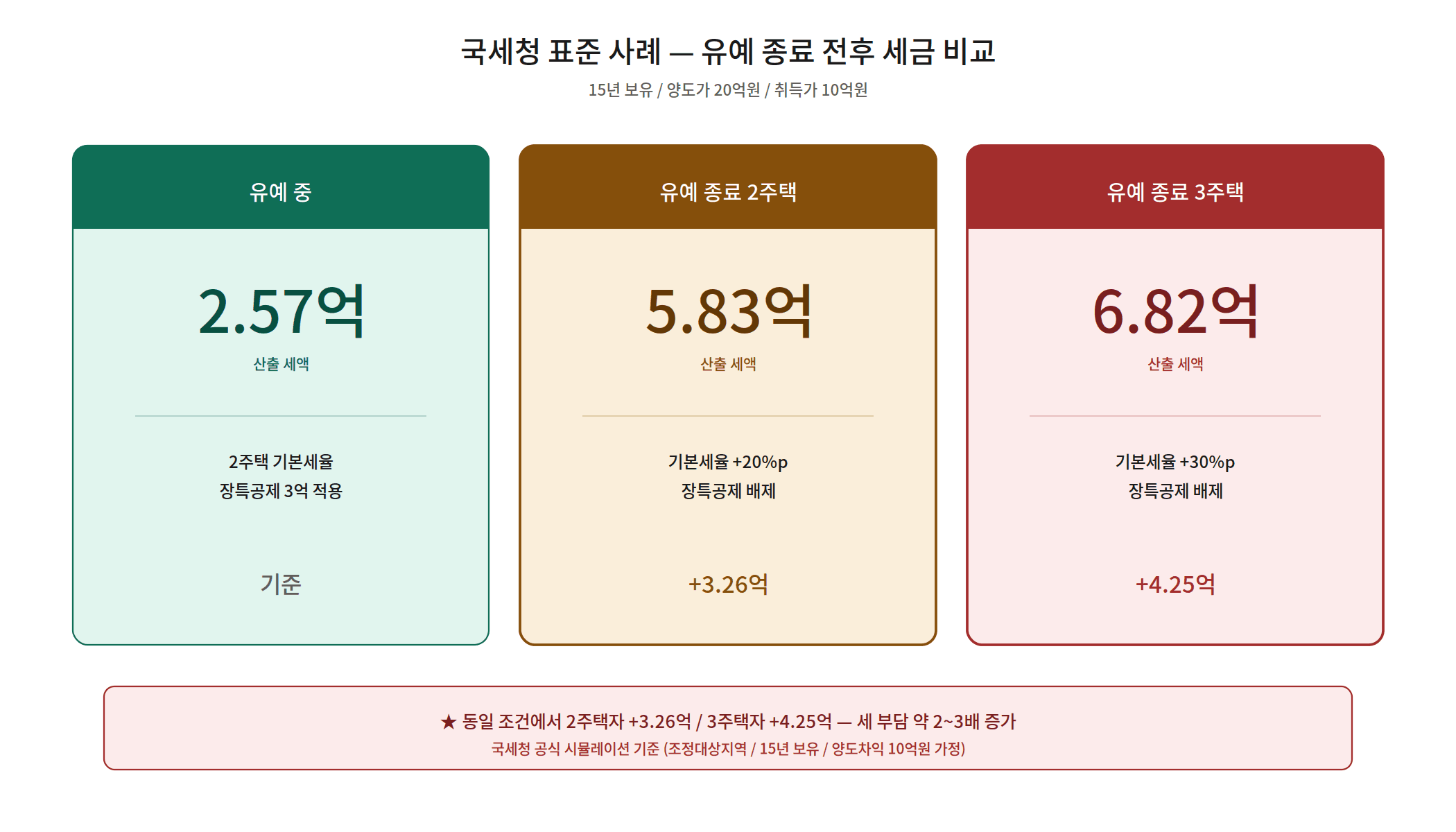

The National Tax Service (NTS) released a standard example to illustrate the impact of the capital gains tax surcharge. Assumptions: property held 15 years, sale price KRW 2 billion (approx. USD 1.45M), acquisition price KRW 1 billion. The gap between what owners paid during the moratorium and what they will owe now is stark. More detailed calculation tools are available on the NTS official website.

| Scenario | Taxable Base | Rate | Tax Payable | Increase |

|---|---|---|---|---|

| Moratorium (2nd home) | KRW 697.5M | 42% | KRW 257.01M | — |

| Post-moratorium (2nd home) | KRW 997.5M | 62% | KRW 582.51M | +KRW 325.5M |

| Post-moratorium (3rd home) | KRW 997.5M | 72% | KRW 682.26M | +KRW 425.25M |

Section 02 — Six Capital Gains Tax Rate Categories at a Glance

South Korea’s capital gains tax surcharge system applies different rates depending on property count, holding period, and zone designation. Understanding all six categories is essential before making any transaction decision.

| Category | Rate | Notes |

|---|---|---|

| RATE 1 — 1st home exemption | Tax-exempt | Requires 2+ years of ownership and residency |

| RATE 2 — 2nd home (non-adjustment zone) | Standard (6–45%) | Located outside designated zones |

| RATE 3 — 2nd home surcharge | Standard +20%p | In adjustment zones, moratorium ended May 10 |

| RATE 4 — 3rd home+ surcharge | Standard +30%p | In adjustment zones, moratorium ended May 10 |

| RATE 5 — Short-term sale | Up to 70% | Held less than 1 year |

| RATE 6 — Pre-sale rights (분양권) | Up to 70% | Pre-sale rights in adjustment zones |

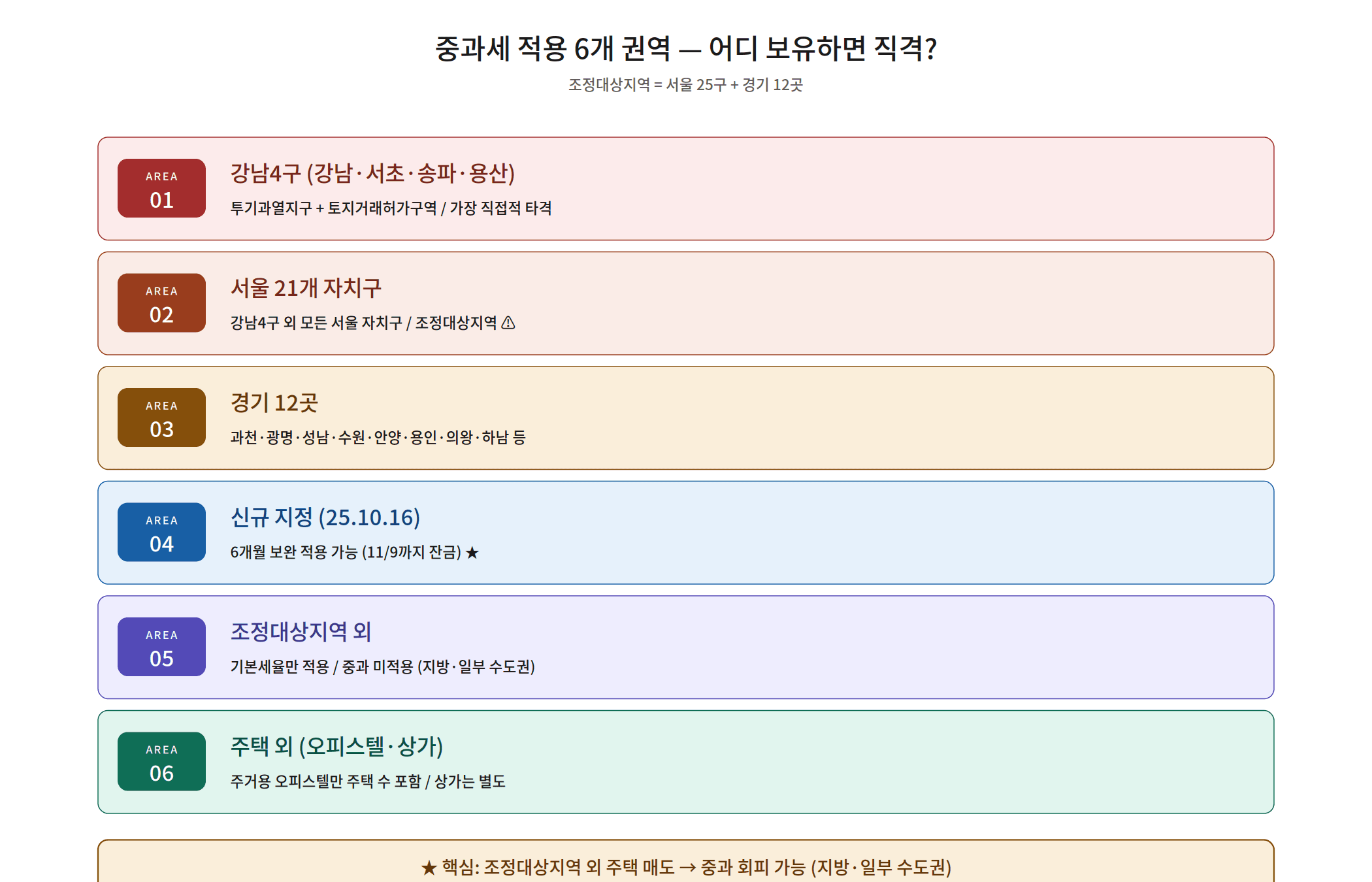

Section 03 — Which Areas Are Affected? Six Designation Zones

The capital gains tax surcharge applies only to properties in officially designated adjustment zones. A new wave of designations in October 2025 expanded the coverage, so owners should verify current status before proceeding.

| Zone | Key Areas |

|---|---|

| Gangnam 4 Districts | Gangnam, Seocho, Songpa, Yongsan |

| Seoul (21 districts) | All Seoul districts except Gangnam 4 |

| Gyeonggi (12 cities) | Gwacheon, Gwangmyeong, Seongnam, Suwon, Anyang, Yongin, Uiwang, Hanam, etc. |

| Newly Designated (Oct 16, 2025) | Additional areas added in Oct 2025 designation round |

| Non-adjustment Zones | Standard rate only — no surcharge |

| Non-residential Property | Land, commercial — separate rules apply |

Section 04 — Government Relief: Grace Period Rules

To cushion the abrupt reinstatement of the capital gains tax surcharge, the government announced six relief measures. The key takeaway: if you signed a purchase-sale contract and paid a deposit before May 9, you may qualify for a multi-month grace period on the final payment.

| Measure | Details |

|---|---|

| EXTEND 1 | Contracts signed before May 9 → eligible for moratorium-era tax rates |

| EXTEND 2 | Gangnam 4 Districts → 4-month final payment extension (deadline: Sep 9) |

| EXTEND 3 | Newly designated zones → 6-month extension (deadline: Nov 9) |

| EXTEND 4 | Land transaction permit zones → permit application period counted separately |

| EXTEND 5 | Bank transfer records proving deposit payment are mandatory |

| EXTEND 6 | Verbal agreements are not recognized — written contracts required |

Section 05 — Too Late vs. Still in Time

Owners who signed after May 9 cannot avoid the full capital gains tax surcharge. But depending on your situation, different strategies remain available.

| Too Late (contracts after May 9) | Still in Time (contracts before May 9) |

|---|---|

| Split sales across tax years to reduce progressive rate | Complete final payment by Sep 9 (Gangnam 4) |

| Consider encumbered gift (부담부 증여) | Complete final payment by Nov 9 (new zones) |

| Check 1-household 1-home exemption eligibility | Use land transaction permit process for additional time |

| Consider rental business registration | Preserve all bank transfer records as proof |

| Prioritize selling non-adjustment-zone properties first | Consult a tax accountant on optimal settlement schedule |

| Wait for motivated buyer rather than accepting discounts | Negotiate final payment date with buyer |

Section 06 — Encumbered Gift vs. Outright Sale

When the capital gains tax surcharge cannot be avoided, an encumbered gift (부담부 증여) may significantly reduce taxable gains. In this structure, the property is transferred to a family member along with its associated debt (e.g., lease deposit or mortgage). Only the debt portion is treated as a taxable sale, while the remainder is subject to gift tax. However, the recipient’s gift tax liability must be factored into the total family tax picture.

“Because capital gains tax follows a progressive rate structure, selling multiple properties in the same tax year can generate a large combined gain. Distributing sales across multiple tax years can materially reduce the applicable rate.”

Samil PwC, Real Estate Tax Guide

Section 07 — 5 Action Strategies for Multi-Home Owners

Here are five concrete strategies for navigating the reinstated capital gains tax surcharge. Each situation is different — simulate your own numbers with a certified tax accountant before acting.

| Strategy | Core Action | Key Caveat |

|---|---|---|

| ACTION 1 — Verify May 9 contract status | Secure signed contract and deposit transfer records immediately | Verbal agreements invalid |

| ACTION 2 — Non-adjustment zones first | Prioritize selling properties outside designated zones | Confirm current zone status |

| ACTION 3 — Split sales | Sell multiple properties across different tax years | Leverage progressive rate structure |

| ACTION 4 — Encumbered gift | Transfer property with debt to reduce taxable gain | Simulate recipient gift tax too |

| ACTION 5 — Consolidate to one home | Use temporary 2-home exemption or meet 1-home criteria before selling | Check 2-year ownership/residency rules |

Section 08 — Three Market Scenarios

What happens next to South Korea’s housing market following the capital gains tax surcharge reinstatement? Expert consensus points to three distinct scenarios.

| Scenario | Probability | Key Driver |

|---|---|---|

| ① Short-term supply freeze ★ | 50% | Tax shock causes owners to hold — fewer listings, prices hold short-term |

| ② Gradual normalization | 35% | Properties trickle to market over time — prices stabilize |

| ③ Market shock | 15% | Flood of distressed listings + rate headwinds — price correction |

Conclusion — The One Thing to Do Right Now

A contract signed before May 9, backed by bank transfer proof = up to KRW 325 million in tax savings. That one document is the entire story of the capital gains tax surcharge reinstatement in a nutshell. If you have it, secure it today and coordinate your settlement schedule with your buyer. If you missed the deadline, an encumbered gift combined with staggered sales across tax years is your most realistic remaining option. Either way, a pre-transaction simulation with a licensed tax accountant is not optional — it is the single most important financial decision you can make this year.

![[Breaking 21:30 KST] US April CPI 3.8% — oil spike kills Fed rate-cut bets](https://getdir.app/wp-content/uploads/2026/05/01_cpi_trend-768x380.png)