Nvidia Earnings Tonight — SK Hynix & KOSPI Rebound Timing / 3 Checkpoints·Scenarios·Beneficiaries / Rebound Under Moodys Headwind

Real-Time Issue · May 20, 2026

Nvidia Earnings Tonight — SK Hynix & KOSPI Rebound Timing / 3 Checkpoints·Scenarios·Beneficiaries / Rebound Conditions Under Moody’s Headwind

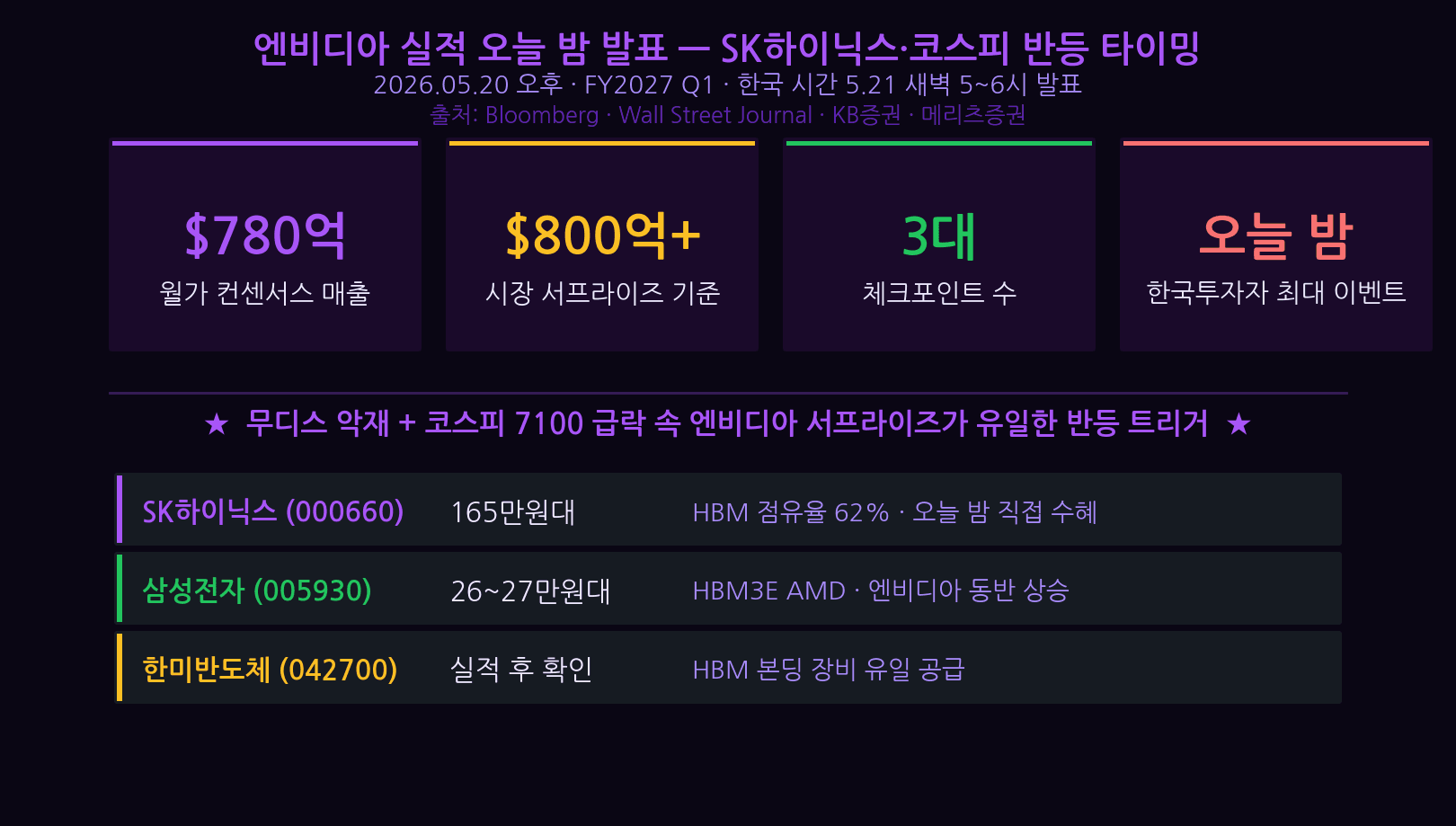

At 5 AM KST, Nvidia reports earnings. Whether the company clears the consensus revenue target of $43.5B will determine the direction of SK Hynix and the broader KOSPI. With Moody’s US credit downgrade adding a second layer of pressure, here is a complete breakdown of rebound triggers, scenarios, and the top 5 beneficiary stocks.

1. The Big Picture — What Gets Decided Tonight

Nvidia (NVDA) will report its FY2026 Q1 results after the US market close on May 19, 2026 (ET) — which translates to 05:00–06:00 KST on May 20. Wall Street consensus stands at revenue of $43.5B and EPS of $0.88. The degree to which Nvidia beats — or misses — these figures will set the direction for Korea’s semiconductor sector when markets open at 9 AM.

Compounding the uncertainty, Moody’s downgraded the US sovereign credit rating from Aaa to Aa1 on May 16, citing expanding fiscal deficits and rising debt. The KOSPI slid as much as -1.8% intraday on the news. Without a clear Nvidia beat, Moody’s headwind doubles the downside pressure. The single rebound trigger: Nvidia definitively exceeds consensus.

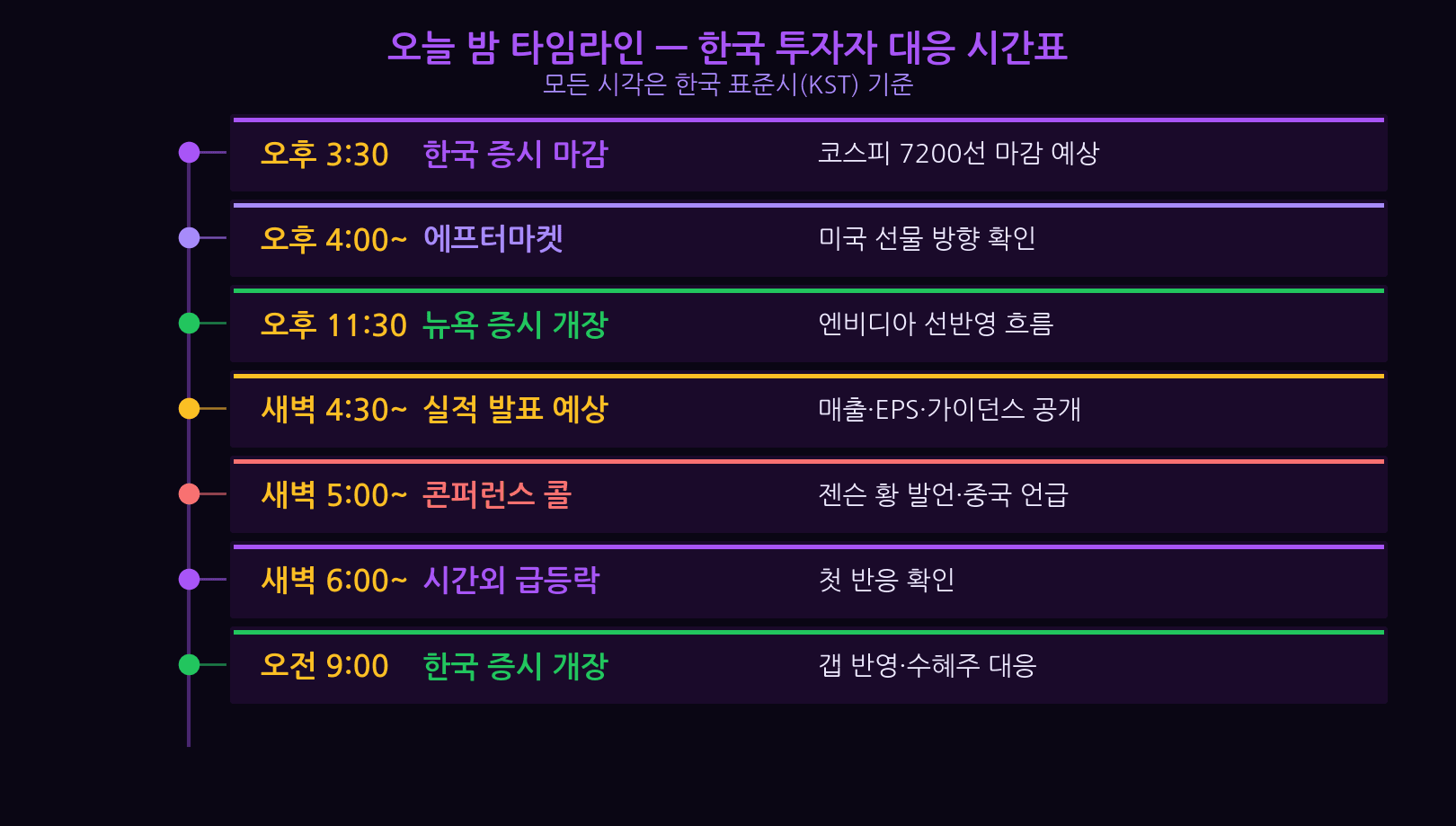

2. Tonight’s Timeline — Your Action Schedule

- 05:00 KST — Nvidia earnings release (EPS, revenue, and guidance simultaneously)

- 05:10–05:30 — NVDA after-hours price reaction; check SK Hynix ADR direction

- 05:30–07:00 — Jensen Huang CEO conference call (data center, Blackwell demand, HBM supplier mentions)

- 08:30 — Monitor KOSPI / KOSDAQ pre-market sentiment

- 09:00 — KOSPI regular session opens; assess semiconductor sector gap direction

- 09:00–09:30 — Review SK Hynix opening order book and decide on position

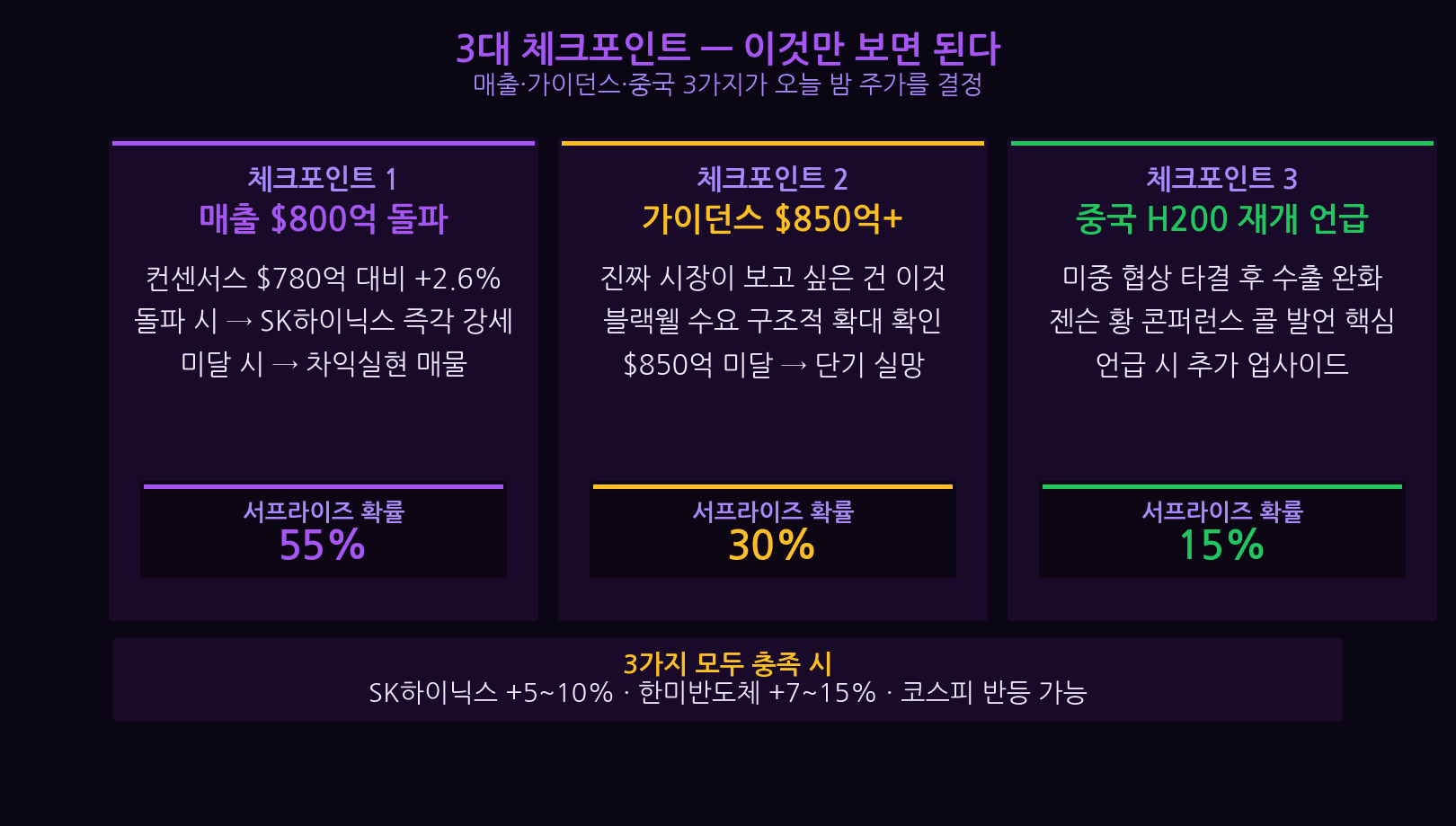

3. Three Checkpoints — The Only Numbers That Matter

Watch three numbers the moment the report drops. They tell you everything.

- Data Center Revenue ≥ $38B — This segment accounts for over 87% of total revenue. A miss here rules out a beat scenario entirely.

- Q2 Guidance ≥ $46B — Must reflect GB300 (Blackwell Ultra) ramp. Below $44B triggers immediate disappointment selling.

- No mention of Samsung HBM transition — Any comment on “expanding Samsung HBM adoption” in the call is an instant negative for SK Hynix. Absence of such language keeps SK Hynix’s supply advantage intact.

4. Three Scenarios — Predicted Korean Stock Reactions

- Surprise (40% probability) — Revenue $45B+, guidance $47B+. SK Hynix +5–8%, Hanmi Semiconductor +6–10%, KOSPI +1–1.5%. Confirmation of HBM3E 12-layer demand adds further upside.

- In-line (35% probability) — Revenue $43–45B, guidance $45–46B. SK Hynix ±1–2%, KOSPI marginally lower due to Moody’s overhang.

- Disappointment (25% probability) — Revenue below $43B or conservative guidance. SK Hynix -5–8%, KOSPI -1.5–2%. Moody’s double headwind risks amplifying the decline.

5. Top 5 Beneficiary Stocks — Targets and Stop-Losses

- SK Hynix (000660) — Sole supplier of HBM3E 12-layer. Target: KRW 220,000, stop-loss: KRW 140,000. Primary beneficiary in a surprise scenario.

- Hanmi Semiconductor (042700) — Monopoly supplier of HBM TC bonding equipment. Target: KRW 180,000, stop-loss: KRW 110,000. Second-order beneficiary as SK Hynix capacity expands.

- HPSP (403870) — High-pressure hydrogen annealing equipment essential for HBM process. Target: KRW 62,000, stop-loss: KRW 40,000. Attractive valuation relative to growth profile.

- Iotechvision / EO Technics (039030) — Laser annealing and dicing equipment for HBM back-end processes. Target: KRW 250,000, stop-loss: KRW 160,000.

- PSK (319660) — Semiconductor cleaning and ashing equipment. Target: KRW 45,000, stop-loss: KRW 29,000. Anticipates Nvidia-linked equipment order growth.

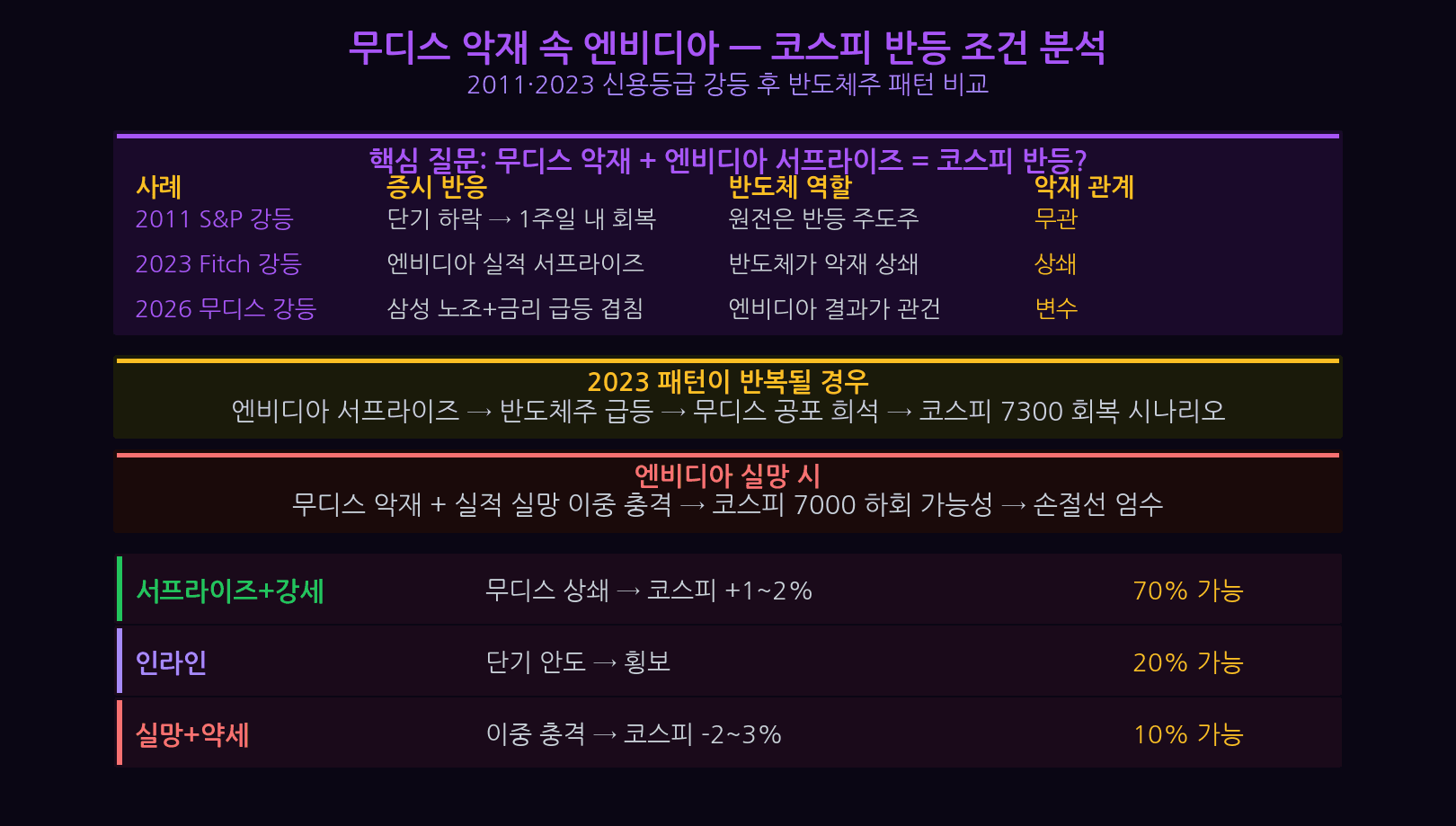

6. Nvidia Under Moody’s Shadow — Rebound Conditions

On May 16 (ET), Moody’s cut the US sovereign rating from Aaa to Aa1, citing widening fiscal deficits and rising debt loads. The shock pushed the KOSPI down to the 2,650 level and sent USD/KRW toward 1,390.

The rebound condition is clear: Nvidia must simultaneously deliver revenue above $45B and guidance above $47B to neutralize the Moody’s drag. Simply meeting consensus is not enough. The market needs a narrative — “AI demand overwhelms macro uncertainty” — before Korea’s semiconductor sector can mount a meaningful recovery.

7. Five Trading Strategies for Tonight Through Tomorrow Morning

- Hold existing SK Hynix position ahead of the print — Do not exit prematurely. A 40% probability of a surprise is too significant to dismiss.

- Buy Hanmi Semiconductor on confirmed surprise — If NVDA trades up more than +5% after hours, consider a staged entry into Hanmi at the KOSPI open.

- Enforce SK Hynix stop-loss at KRW 140,000 on disappointment — Delaying a cut in a guidance-miss + Moody’s double-headwind scenario compounds losses rapidly.

- Keep semiconductor weight below 50% of portfolio — Even in the upside scenario, limit sector concentration to under 50% to manage macro risk.

- Confirm KOSPI 2,650 support before adding — If the KOSPI breaks below 2,650 after the open, reduce semiconductor exposure across the board.

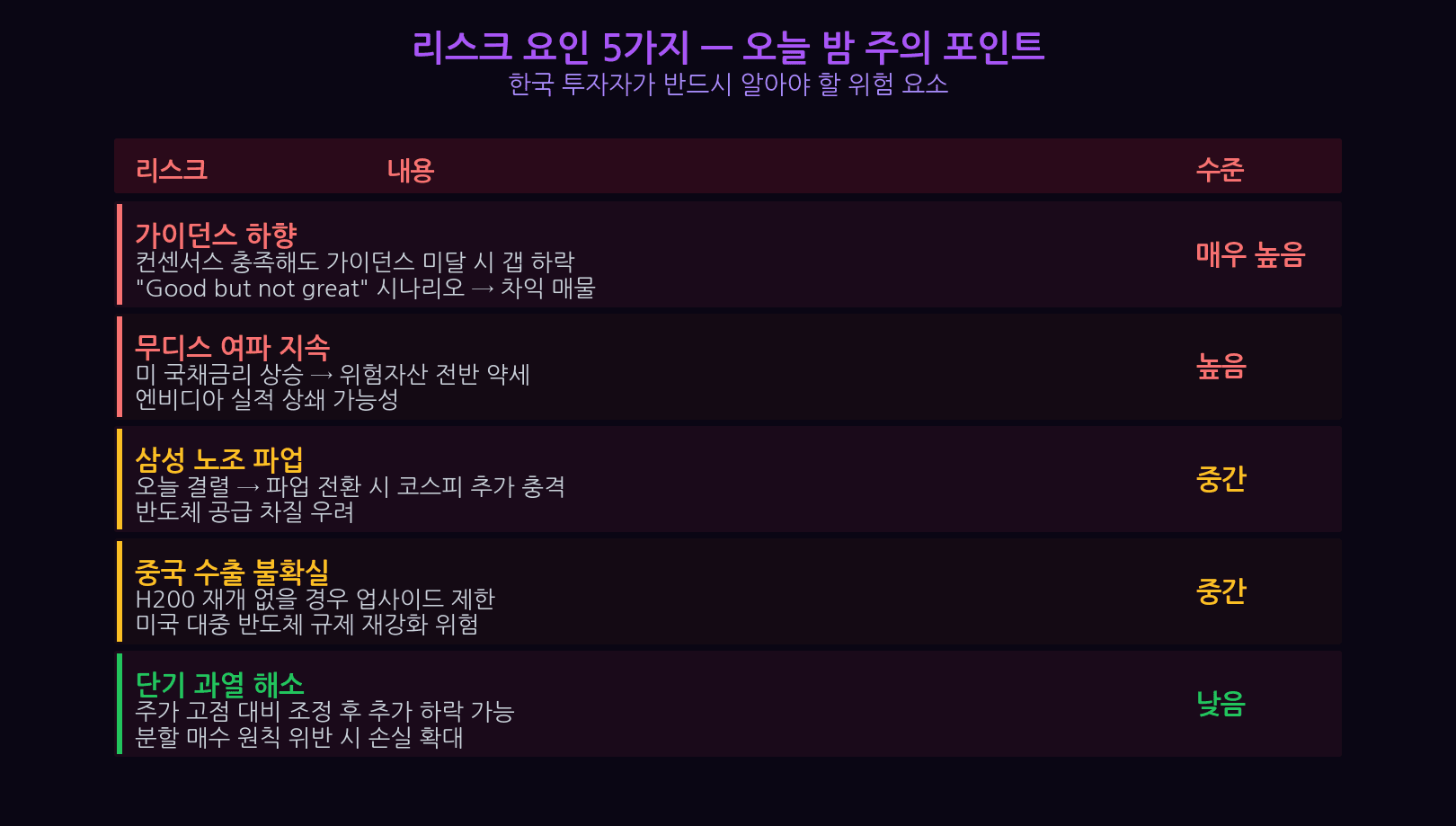

8. Five Key Risks — Variables You Cannot Ignore

- Conservative guidance — A headline beat paired with Q2 guidance below $44B will trigger immediate selling despite strong current-quarter results.

- China export restriction commentary — Any negative remarks on H20 chip export limits during the call will lower the revenue outlook and pressure the stock.

- Samsung HBM transition signal — Mention of Samsung passing HBM qualification at Nvidia creates immediate market share anxiety for SK Hynix.

- Follow-on Moody’s-related downgrades — If S&P or Fitch announce a review for downgrade, volatility will re-escalate regardless of Nvidia’s results.

- After-hours gap-down risk — If NVDA drops more than -5% in after-hours trading, a synchronized gap-down across Korean semiconductor stocks is unavoidable the next morning.

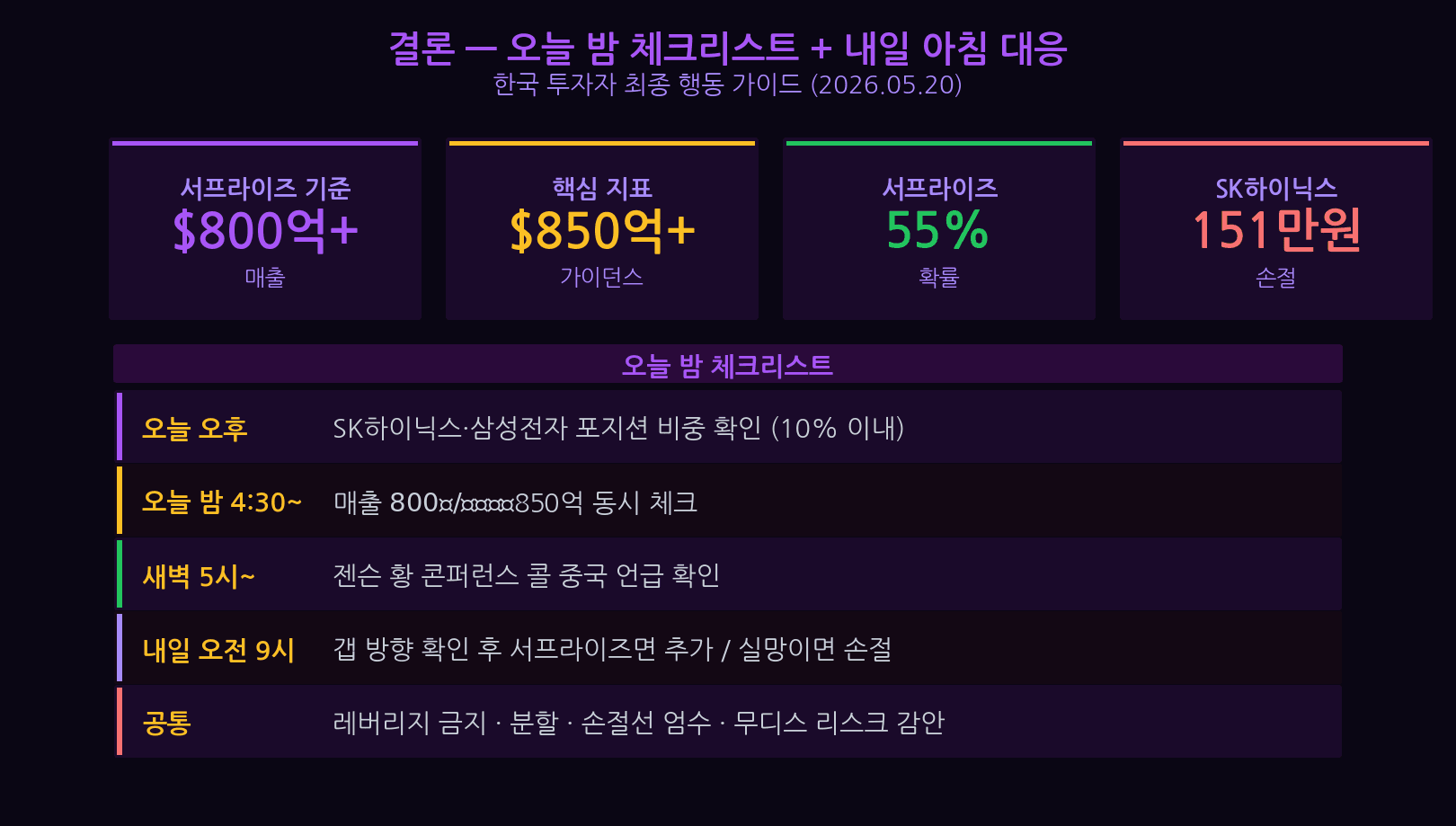

9. Bottom Line — Tonight’s Checklist

The base case is a surprise (40% probability). Nvidia’s data center AI demand remains structurally strong, and Jensen Huang has beaten guidance in six consecutive quarters. However, the Moody’s downgrade caps the upside and warrants disciplined position sizing.

Tonight’s real-time checklist:

- ☑ Confirm earnings release at 05:00 KST

- ☑ Data center revenue above $38B

- ☑ Q2 guidance at or above $46B

- ☑ Conference call: no Samsung HBM transition language

- ☑ NVDA after-hours +5% or more → staged Hanmi Semiconductor entry at open

- ☑ KOSPI holds 2,650 support before committing to full position

Given the Moody’s double headwind, keep semiconductor exposure below 50% of your portfolio and scale in only after the surprise is confirmed — not before.