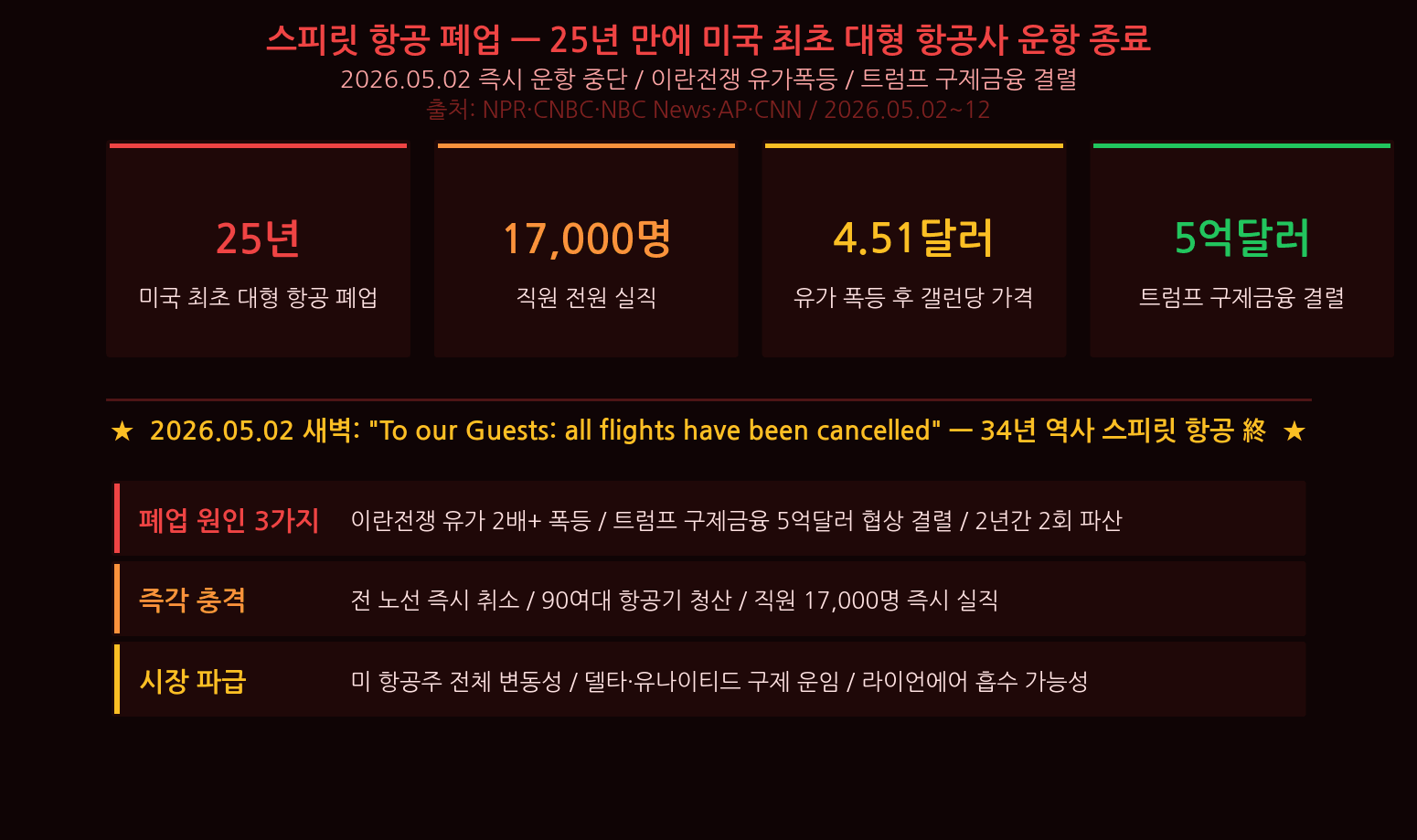

Spirit Airlines Shuts Down — First Major US Airline Collapse in 25 Years

Real-Time Issue · May 22, 2026

Spirit Airlines Shuts Down — First Major US Airline Collapse in 25 Years

Iran War Doubles Jet Fuel Costs · Trump Bailout Talks Fail · Airline Stock Investment Strategy

![[비비PICK] 리에티 LUNO RT 4056 선글라스](https://img1a.coupangcdn.com/image/affiliate/banner/8f965ee3220144b9189234e8256f5677@2x.jpg)

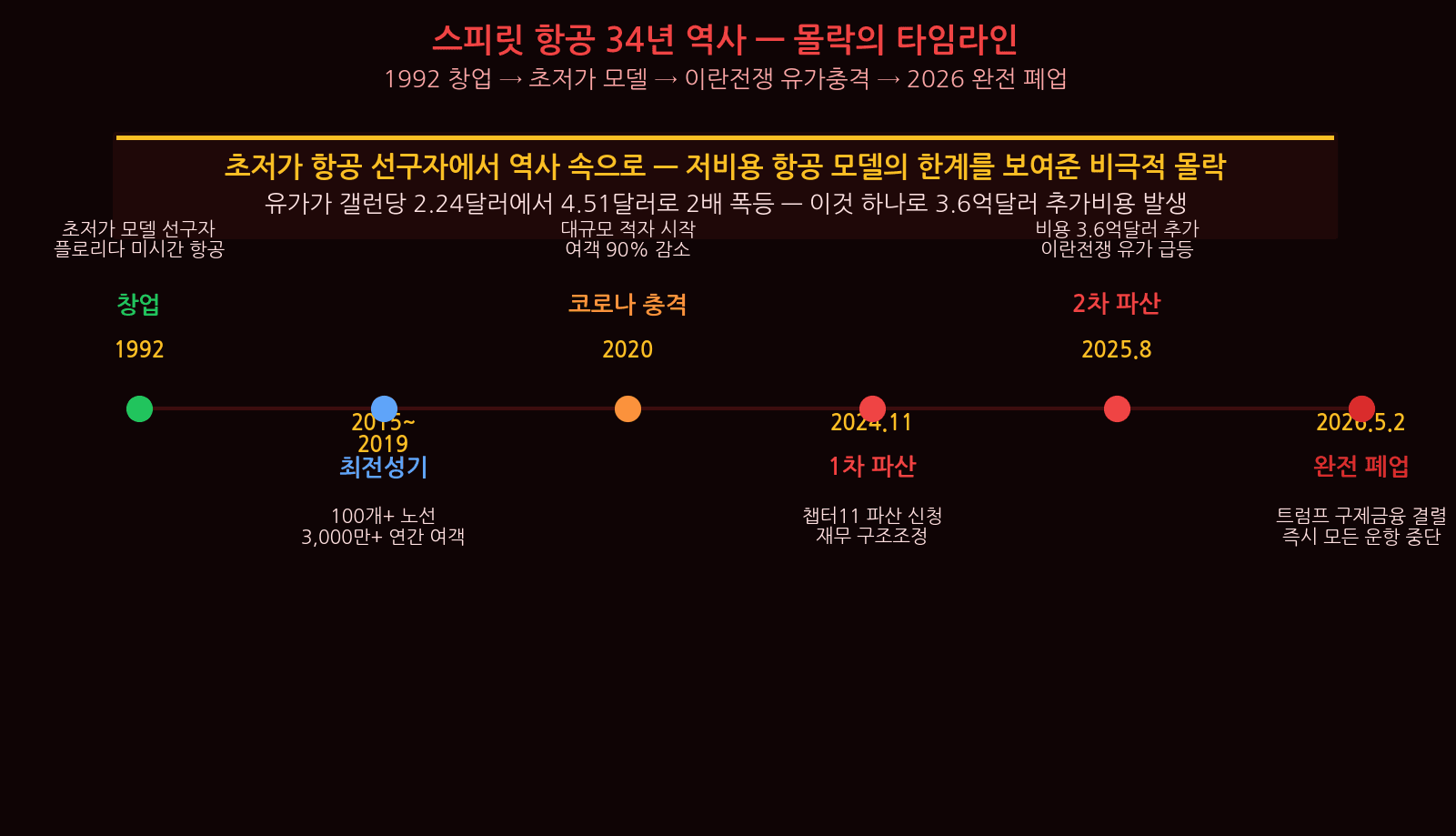

34-Year History — The Collapse Timeline

On the morning of May 2, 2026, Spirit Airlines cut power to every aircraft in its fleet. “To our Guests: all flights have been cancelled, and customer service is no longer available.” The last time a major US airline closed was in the aftermath of 9/11 — 25 years ago. Founded 1992 → peak 2015–2019 (100+ routes, 30M passengers) → COVID shock 2020 → Chapter 11 (November 2024) → second bankruptcy triggered by Iran-war jet fuel shock (August 2025) → full shutdown and liquidation May 2, 2026.

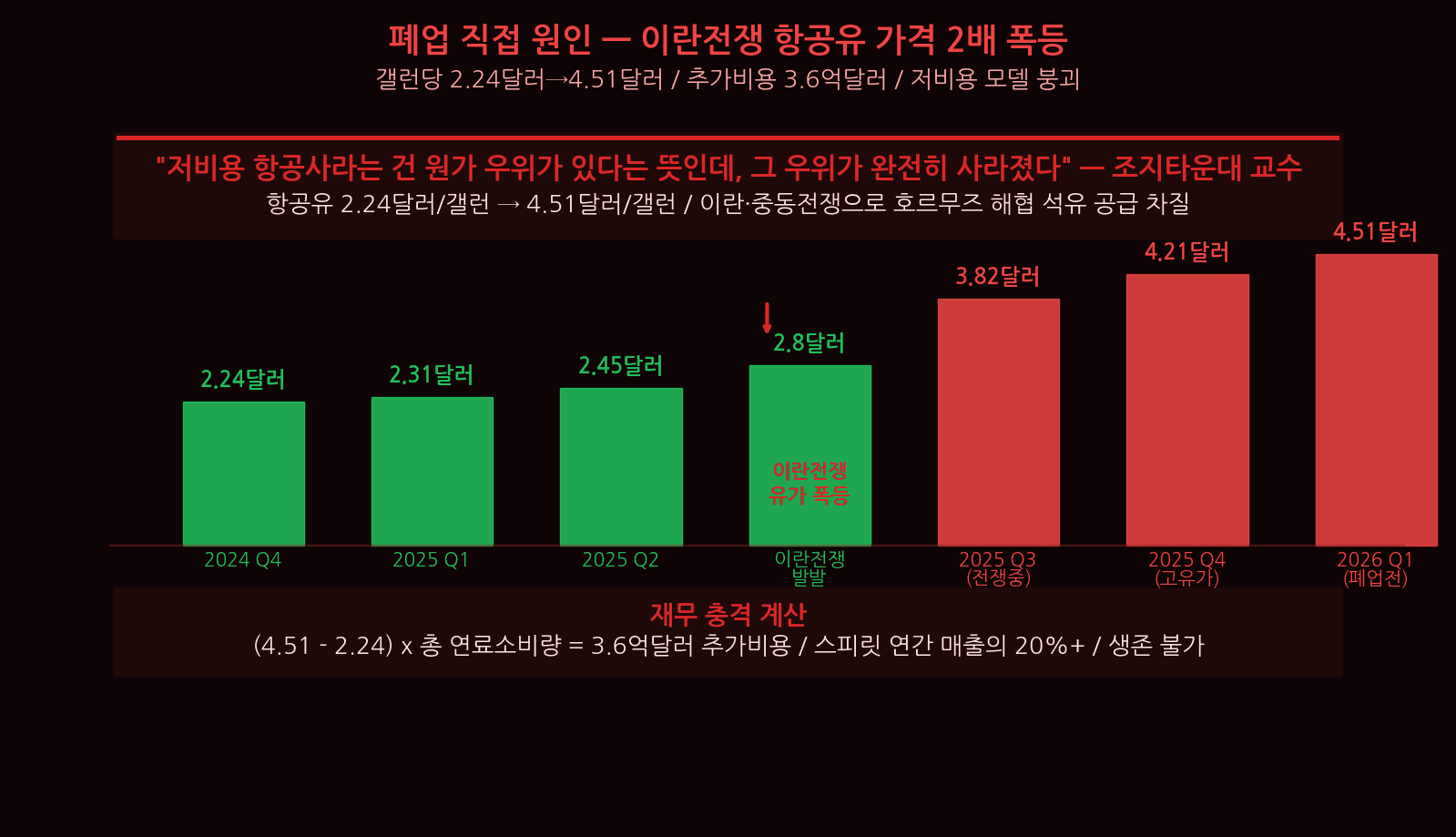

Why Spirit Failed — The Iran War Fuel Shock

The Iran war pushed jet fuel from $2.24/gallon to $4.51/gallon — a 101% increase. That single variable added $360M in costs Spirit could not absorb. Jet fuel is 30–40% of an ultra-low-cost carrier’s operating cost structure. Double the fuel price and the entire cost model collapses. Spirit had no fuel hedging — it bought on the spot market every time. A $500M Trump administration bailout was also pursued and rejected: Trump said there was “no good deal to be had.”

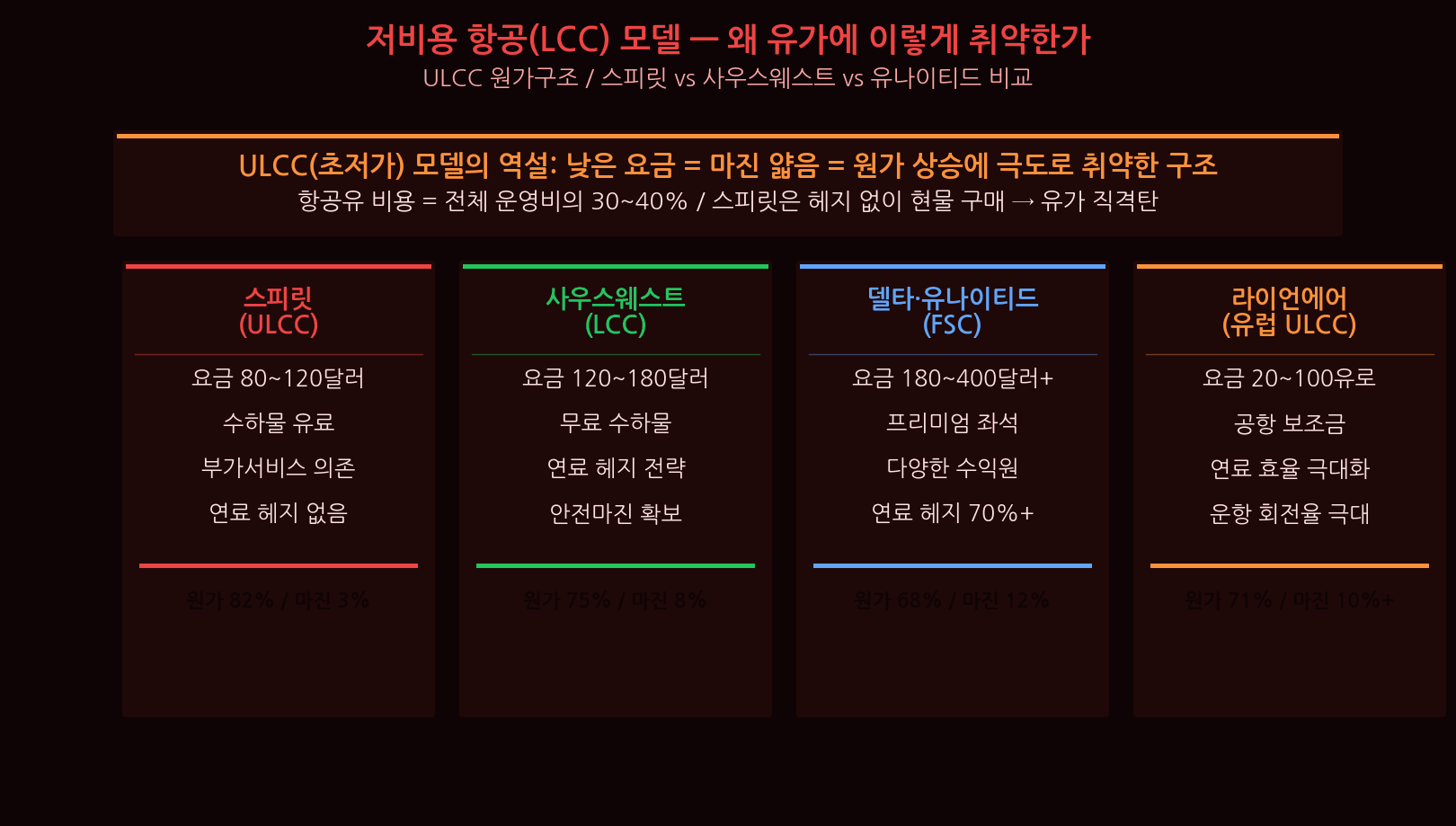

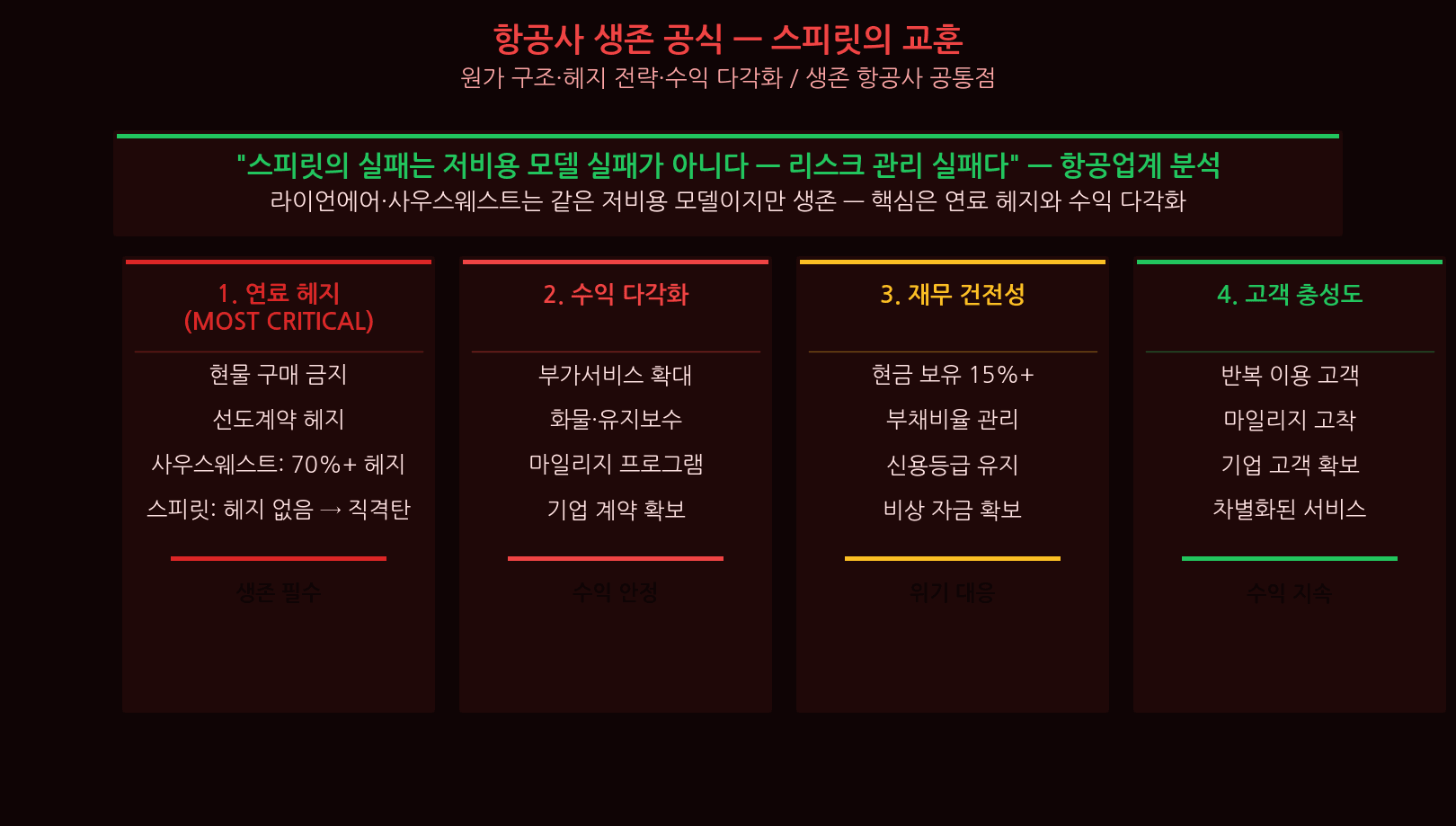

The Limits of the Ultra-Low-Cost Model

Airline comparison: Spirit (ULCC) — no hedging, 3% margin → two bankruptcies → shutdown. Southwest (LCC) — 70%+ hedged, 8% margin → profitable. Ryanair (EU ULCC) — forward contracts, 10%+ margin → record profits. Delta/United (FSC) — 60–70% hedged, 12% margin → stable. The verdict: the low-cost model isn’t dead. The unhedged low-cost model is dead. Ryanair is printing record earnings right now.

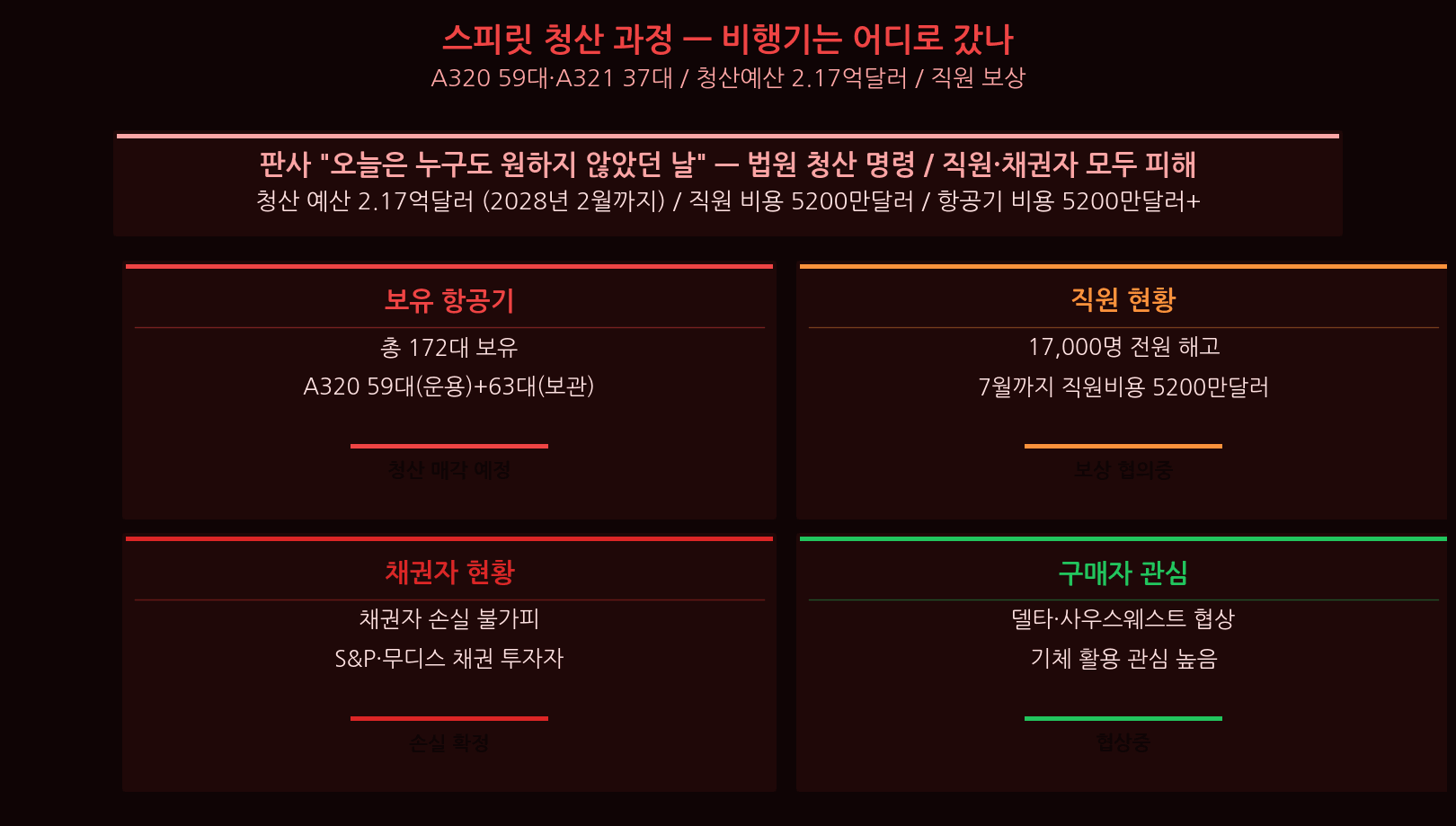

Liquidation — Where Did the Planes Go?

Spirit’s fleet: 59 A320s (in service) + 63 A320s (stored); 37 A321s (in service) + 13 A321s (stored). All are being returned to lessors or sold. Total liquidation budget: $217M (distribution to creditors through February 2028). Employee compensation: $52M (priority payment by July). 17,000 workers lost their jobs. Passengers holding Spirit tickets should dispute charges through their credit card company — that is the fastest route to a refund.

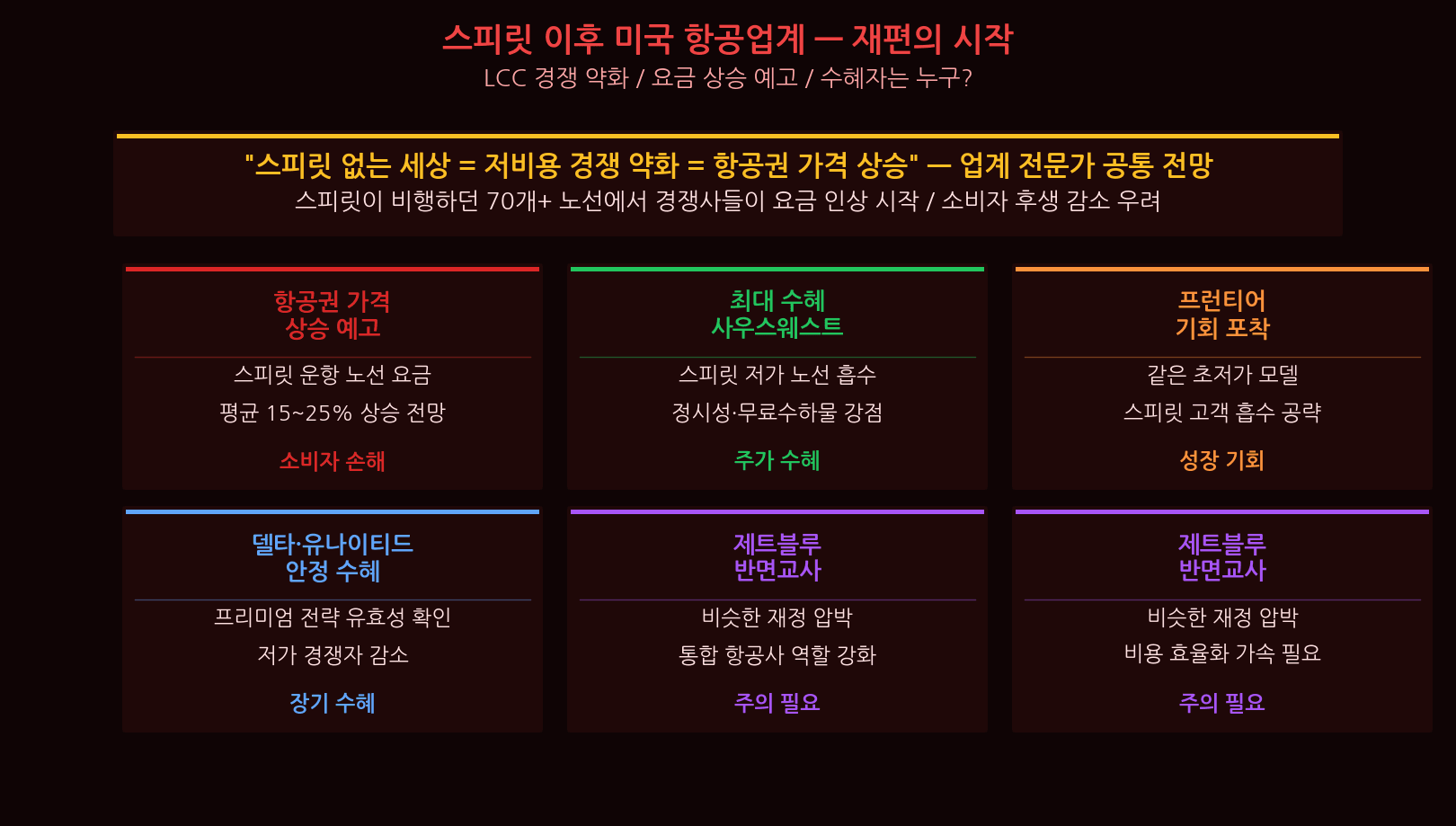

US Aviation Industry Reshapes

Competition has vanished on 70+ Spirit routes. Average airfares on those routes are expected to rise 15–25%. Florida, Caribbean, and Midwest routes will be hit hardest. Winners: Southwest (LUV) absorbs the most Spirit routes — the primary beneficiary. Delta and United reaffirm the premium-strategy thesis. Challengers: Frontier and Alaska Air will compete for some of Spirit’s vacated low-fare routes.

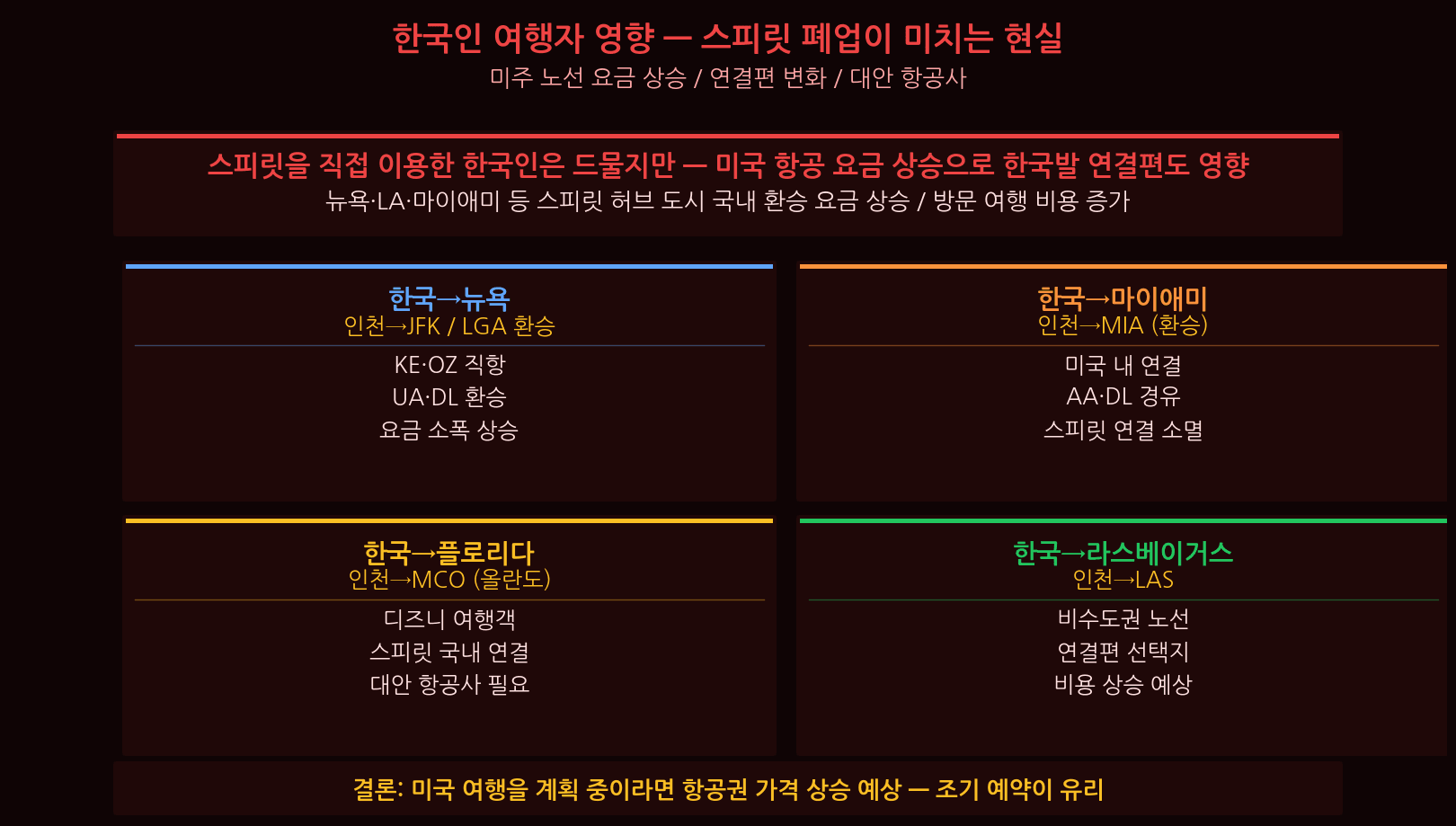

Impact on Korean Travelers

How Spirit’s collapse affects Korean travelers: Incheon→New York connections (reduced domestic competition at JFK/LGA → Delta/United fare uptick), Incheon→Miami (American/Delta alternatives, fares rising), Incheon→Orlando (Disney trip costs up, Southwest as alternative), Incheon→Las Vegas (Southwest/Alaska as alternatives, fares rising). If you’re planning a US trip this summer, book now. Fares on affected routes are expected to climb further before the season peaks.

The Airline Survival Formula — Spirit’s Legacy

Five lessons from Spirit’s collapse: ① Cost advantage without fuel hedging is a ticking clock, not a strategy. ② Two bankruptcies without fixing the underlying business model are meaningless. ③ Government bailouts cannot fix a structurally broken cost model. ④ Every surviving low-cost carrier — Southwest, Ryanair — has rigorous cost management AND hedging. ⑤ Black swan events (Iran war) expose the unhedged. No airline is safe without a fuel risk management program.

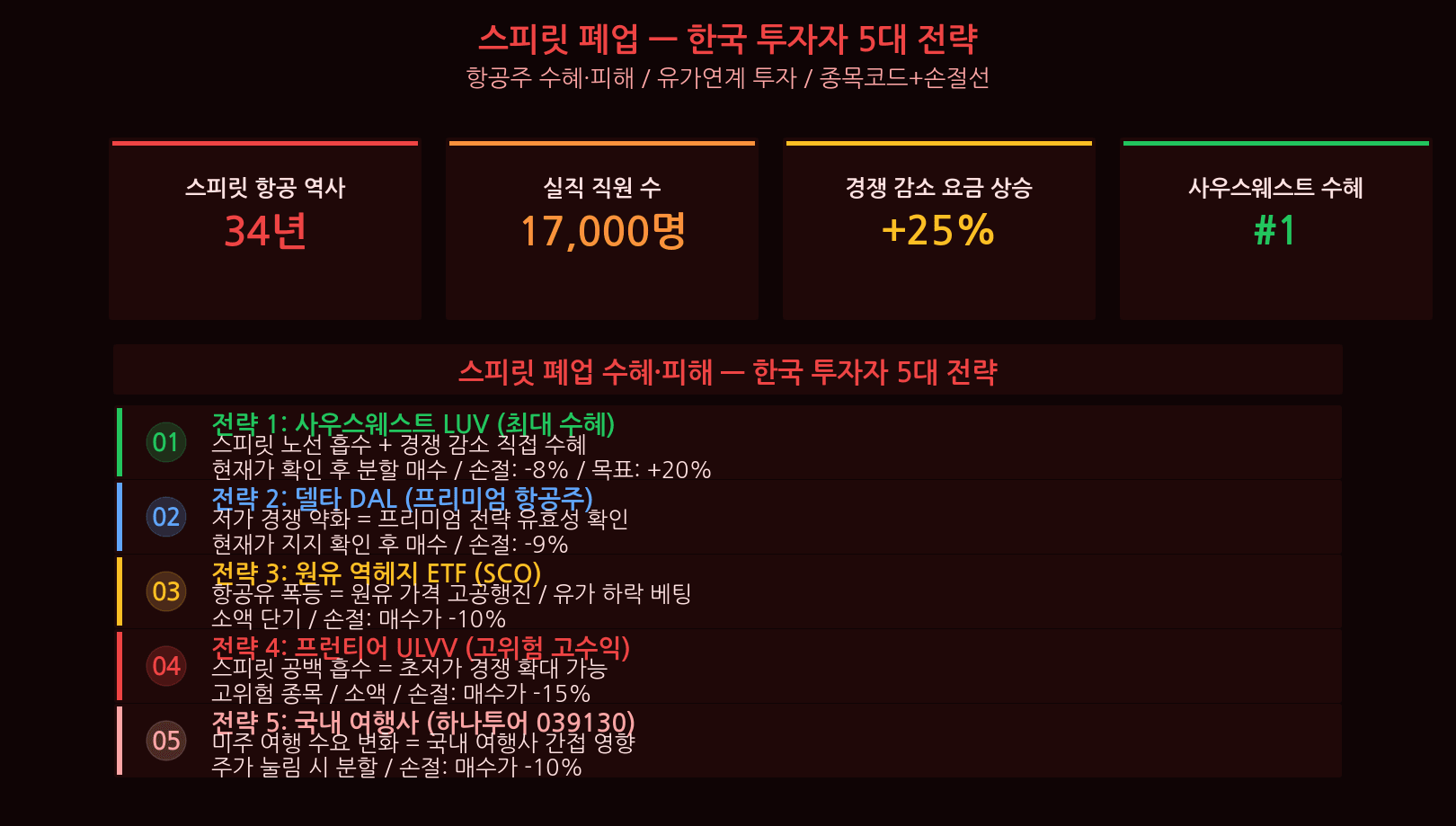

5 Investment Strategies for Korean Investors

Five strategies after Spirit’s collapse: ① Southwest (LUV) — top beneficiary absorbing Spirit routes; confirm support, stop-loss -8%; weight 8–10%. ② Delta (DAL) — premium strategy reaffirmed; split entry on support, stop-loss -9%; weight 8%. ③ ProShares UltraShort Crude (SCO) — inverse oil play when fuel prices turn down; stop-loss -10%; weight 3%. ④ Frontier (ULVV) — high-risk, small position only; stop-loss -15%; weight 3%. ⑤ Hanatour (039130, Korea) — monitor US travel cost impact; buy dips, stop-loss -10%; weight 5%.

Conclusion — The Future of Low-Cost Aviation

Spirit’s shutdown is not the end of low-cost aviation — it is the end of low-cost aviation without risk management. Ryanair is posting record profits. Southwest is growing into Spirit’s routes. The model works when executed properly. Final investor checklist: book US travel now (15–25% fare increases ahead) / watch Southwest (LUV) as the route-absorption winner / confirm Delta/United premium thesis / monitor oil direction — Iran war resolution is the key variable / track Hanatour (039130) for US travel cost exposure.

Sources: CNBC Reuters Korea JoongAng Daily