Nvidia +85% record earnings and HBM4 — how much will SK Hynix benefit, full analysis

Trending · May 25, 2026

Nvidia Posts Record +85% Quarter — How Big Is SK Hynix’s HBM4 Windfall?

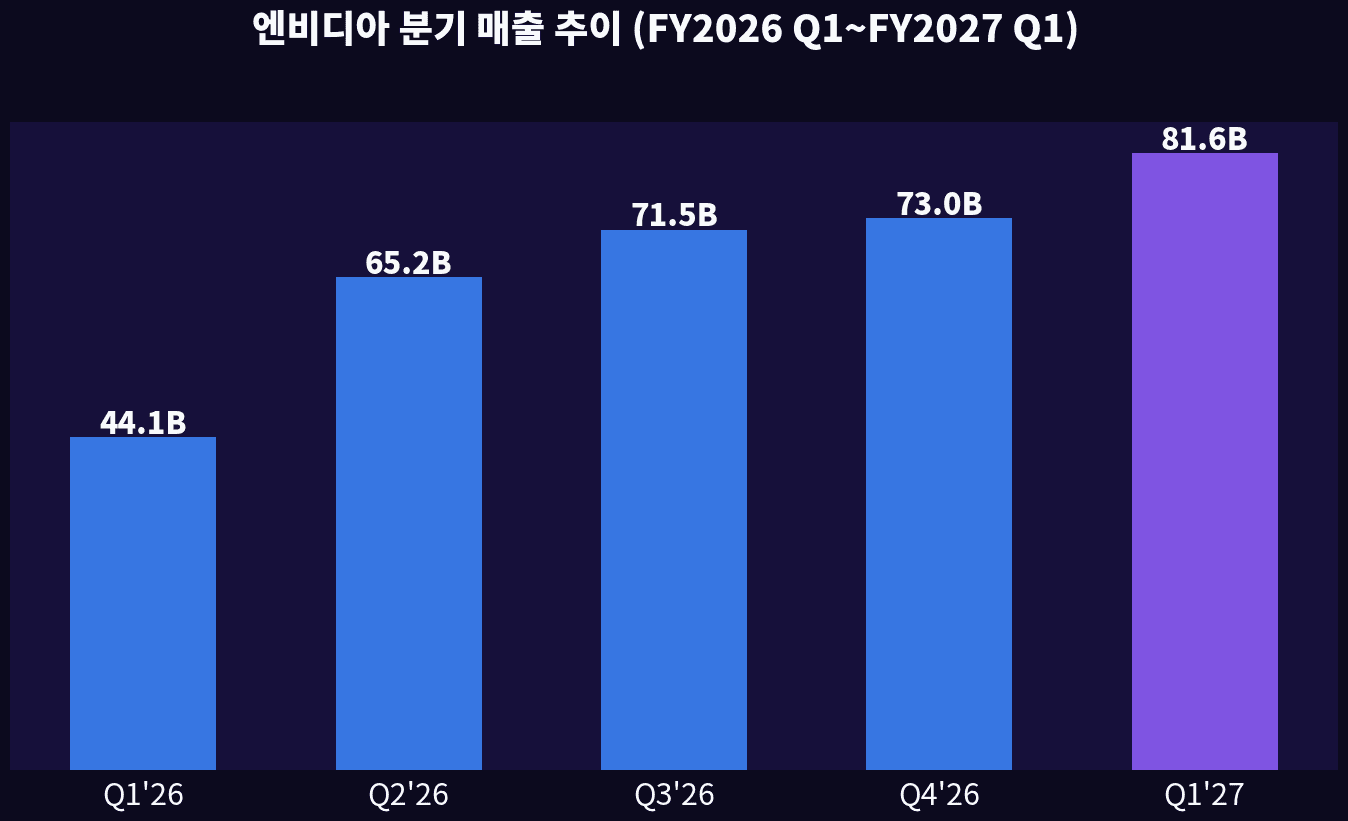

Nvidia Q1 FY2027 revenue hit $81.6B, up +85% YoY. We break down what HBM4 sole supplier SK Hynix actually wins — order book, earnings, and price targets.

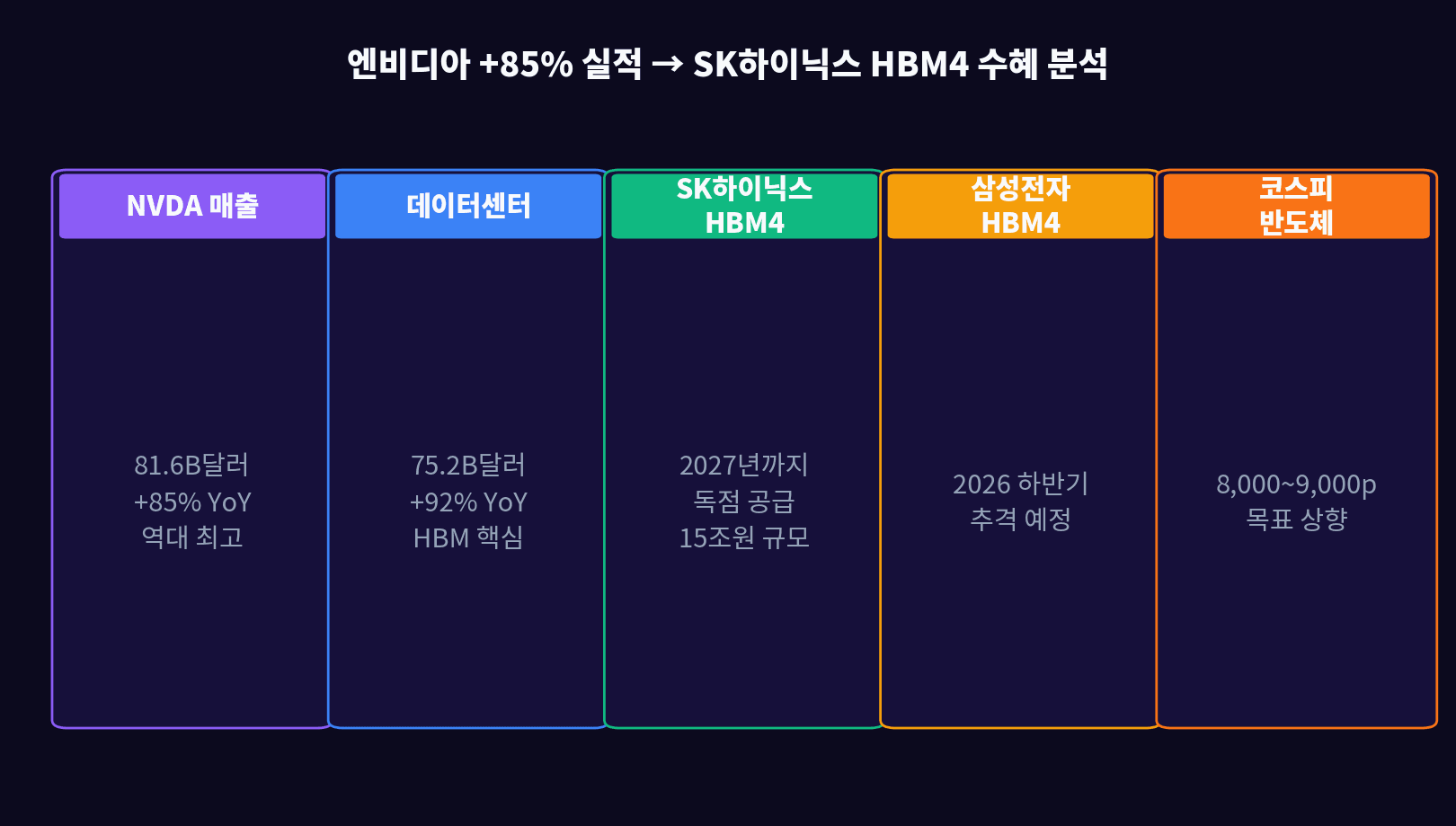

Nvidia just posted its biggest quarter ever — Q1 FY2027 revenue of $81.6 billion (about KRW 112 trillion), up +85% year over year. CEO Jensen Huang declared “a new era of AI infrastructure investment” and pointed to a $1.7 trillion AI data center market opportunity. The single most critical component powering this growth is SK Hynix’s HBM4 (High Bandwidth Memory). The official release is available on the NVIDIA Newsroom.

| Item | Figure | Meaning |

|---|---|---|

| NVDA Q1 FY2027 revenue | $81.6B | All-time high, +8% above consensus |

| YoY growth | +85% YoY | AI demand still exploding |

| Data center revenue | $75.2B (+92%) | Core driver of HBM demand |

| SK Hynix HBM4 supply | Sole supplier through 2027 | Est. KRW 15T order book |

| KOSPI semiconductor index outlook | 8,000–9,000pt | Sell-side target upgrade wave |

“The age of AI has arrived. The next wave is physical AI — robots, autonomous systems, and digital twins powered by our Grace Blackwell platform.”

01. Nvidia Earnings Breakdown — What Sold and How Much?

The headline of Q1 FY2027 is $75.2B in data center revenue, accounting for 92% of the total. Gaming, automotive, and pro visualization all grew, but AI infrastructure dominated. Demand for the Grace Blackwell platform has far exceeded expectations, leaving the supply side in a sustained shortage.

| Segment | Q1 FY2027 revenue | QoQ | YoY |

|---|---|---|---|

| Data Center | $75.2B | +12% | +92% |

| Gaming | $3.8B | +5% | +13% |

| Professional Visualization | $0.5B | +8% | +17% |

| Automotive | $0.6B | +10% | +88% |

| OEM & Other | $1.5B | +3% | +6% |

Nvidia guided next quarter’s revenue to $88–90B, signaling yet another record-breaking print. HBM4 demand is expected to run 2–3x higher than HBM3E.

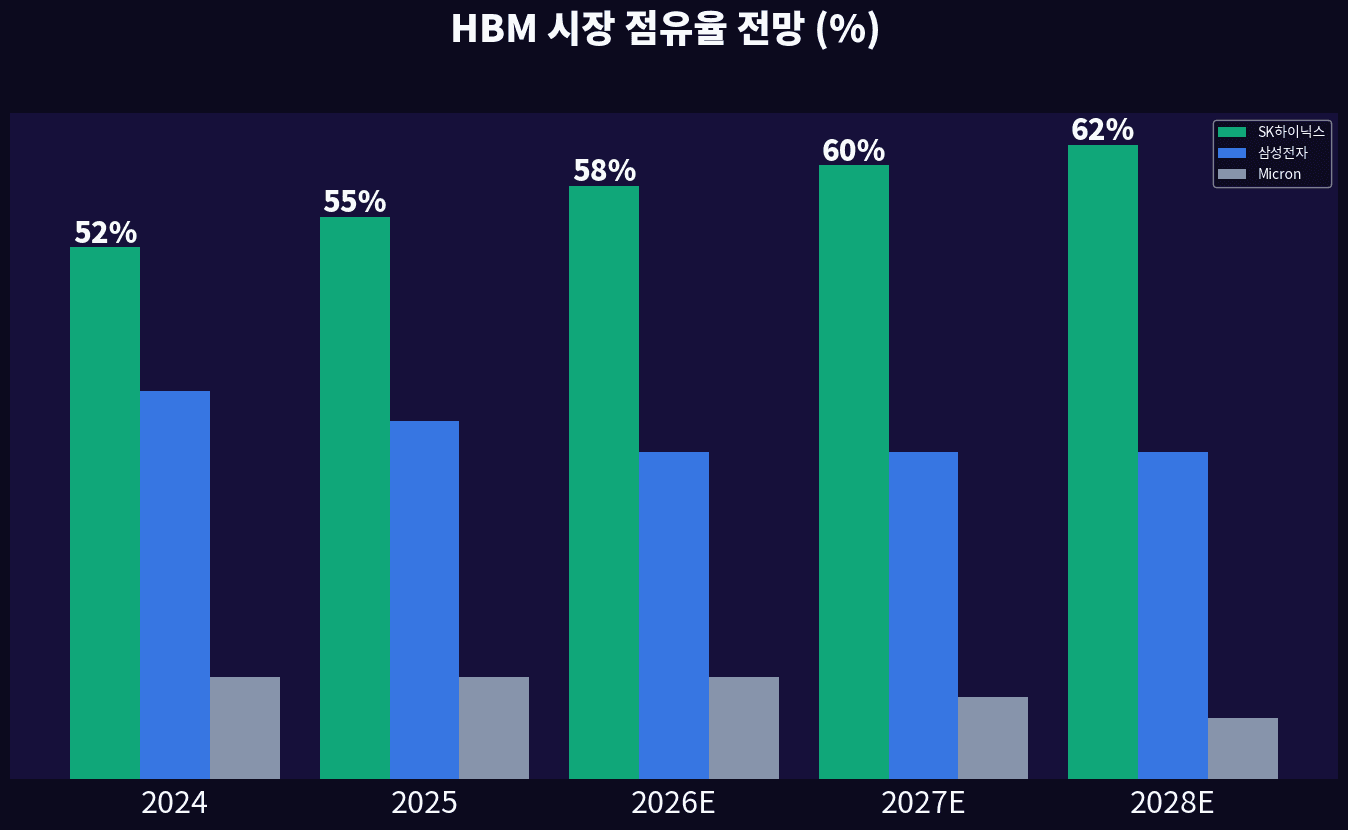

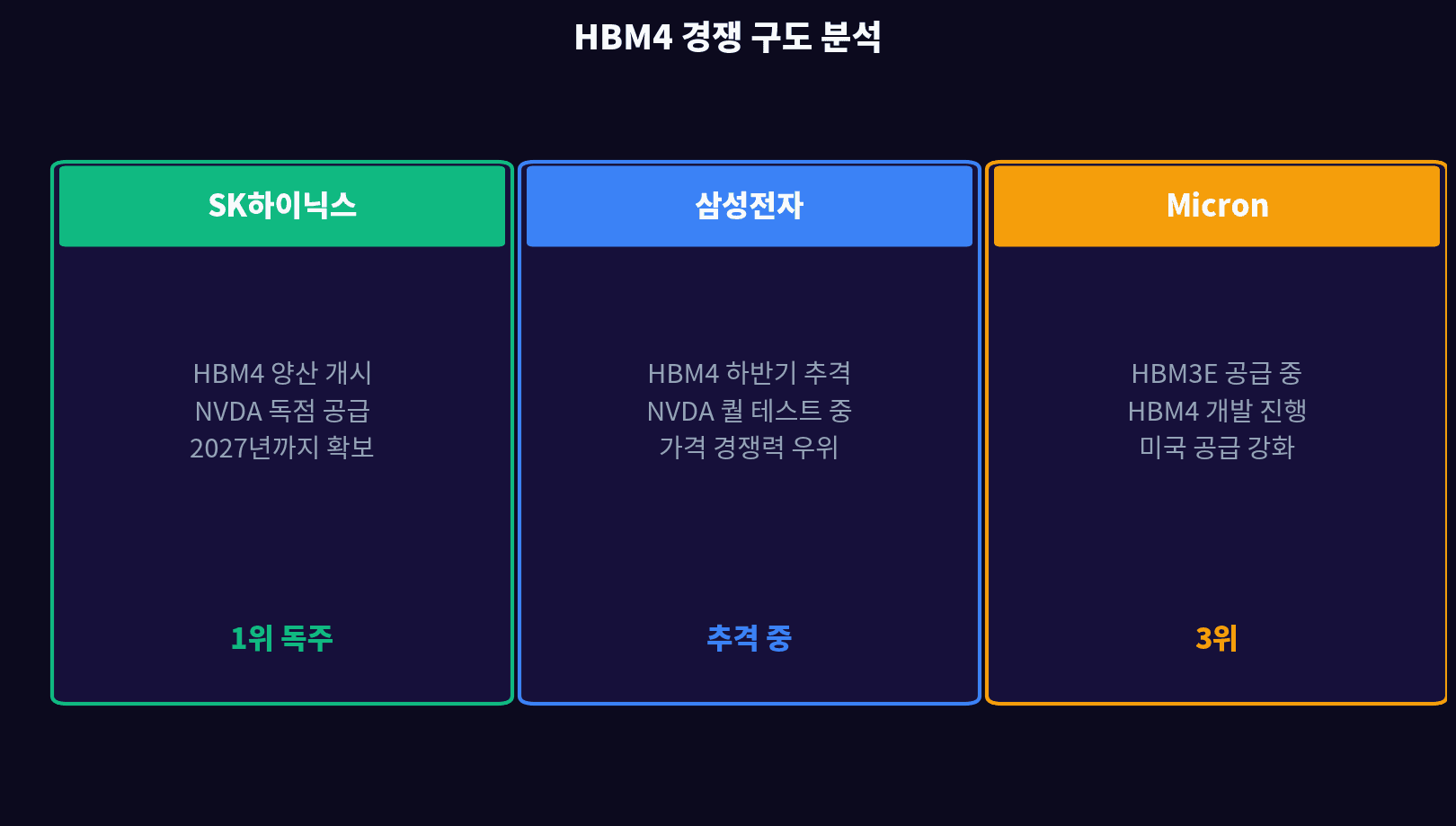

02. The HBM4 Market — Why SK Hynix Is Running Away With It

HBM (High Bandwidth Memory) is the critical memory stack inside AI accelerators, delivering 10–20x the bandwidth of conventional DRAM. SK Hynix currently holds 55–58% of the global HBM market and continues to lead alone. In HBM4, an exclusive supply contract with Nvidia locks in volumes through 2027.

| Item | SK Hynix | Samsung | Micron | Others |

|---|---|---|---|---|

| HBM3E status | 55% leader | 38% chaser | 7% | 0% |

| HBM4 outlook | ~60% | ~30% | 8% | 2% |

| NVDA supply status | Sole supplier | Qual in progress | Partial | None |

| Tech standing | First to mass-produce | 6–9 month gap | Chasing leaders | N/A |

| Order value | ~KRW 15T (est.) | Undetermined | ~KRW 2T | N/A |

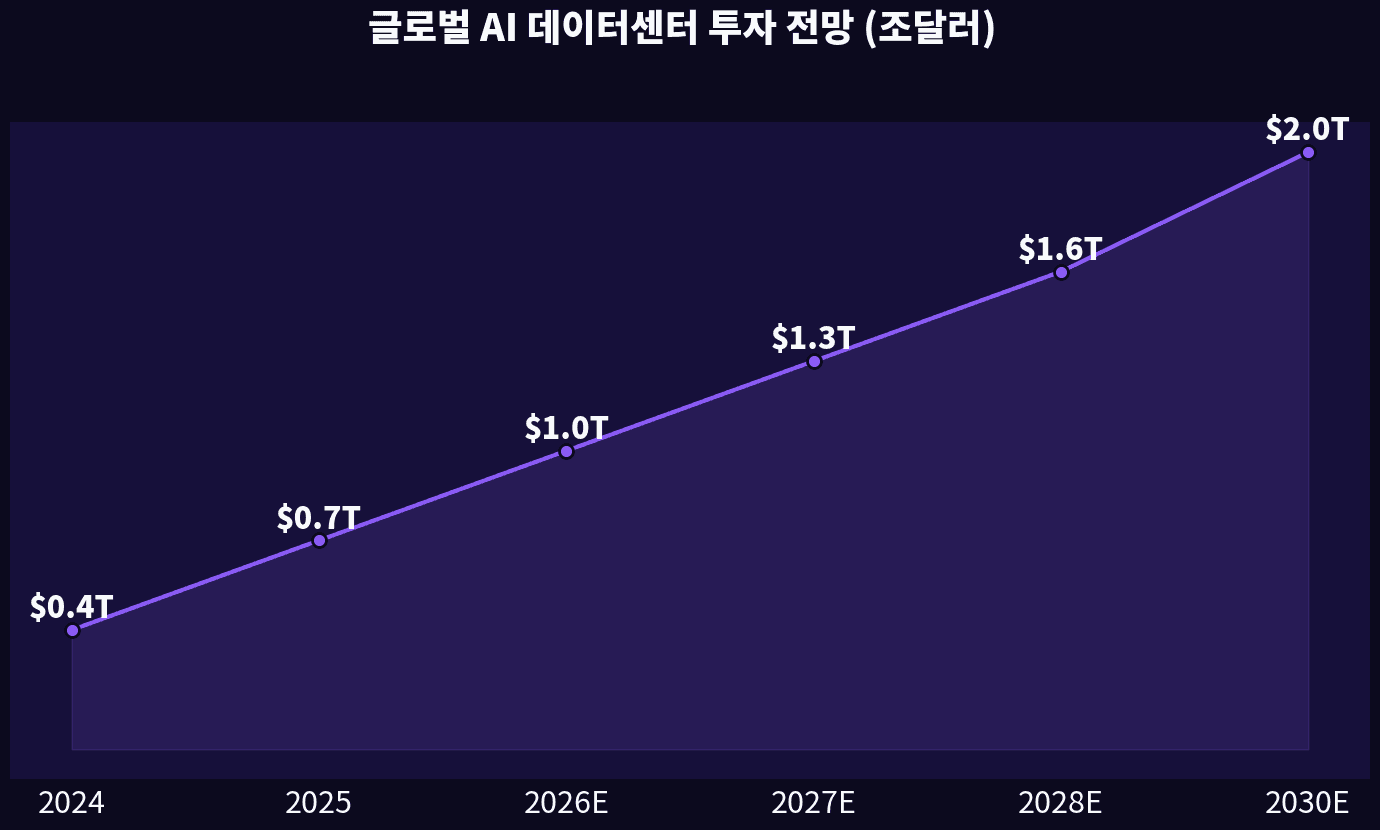

03. AI Data Center CapEx — The Supercycle Isn’t Over

Jensen Huang projected $1.7 trillion in global data center investment from 2026 through 2028. Microsoft, Amazon, Google, and Meta alone plan to deploy more than $260 billion in CapEx in 2026, with Nvidia GPUs and HBM memory sitting at the center of that demand.

Microsoft: $80B/yr (Azure AI infrastructure)

Amazon AWS: $70B/yr (AI cloud)

Google: $75B/yr (TPU + GPU mix)

Meta: $65B/yr (Llama AI research)

Total: ~$290B → +40% vs 2025

| Spender | 2025 CapEx | 2026E CapEx | YoY | HBM exposure |

|---|---|---|---|---|

| Microsoft | $60B | $80B | +33% | HBM4 first-priority allocation |

| Amazon AWS | $55B | $70B | +27% | Multi-supplier strategy |

| $58B | $75B | +29% | TPU + NVDA hybrid | |

| Meta | $38B | $65B | +71% | Llama AI focus |

| Total | $211B | $290B | +37% | HBM demand explosion |

A single Grace Blackwell GB200 NVL72 rack packs 6x the HBM capacity of the previous H100. As unit prices rise, SK Hynix’s HBM4 ASP is projected to climb 30%+ above HBM3E.

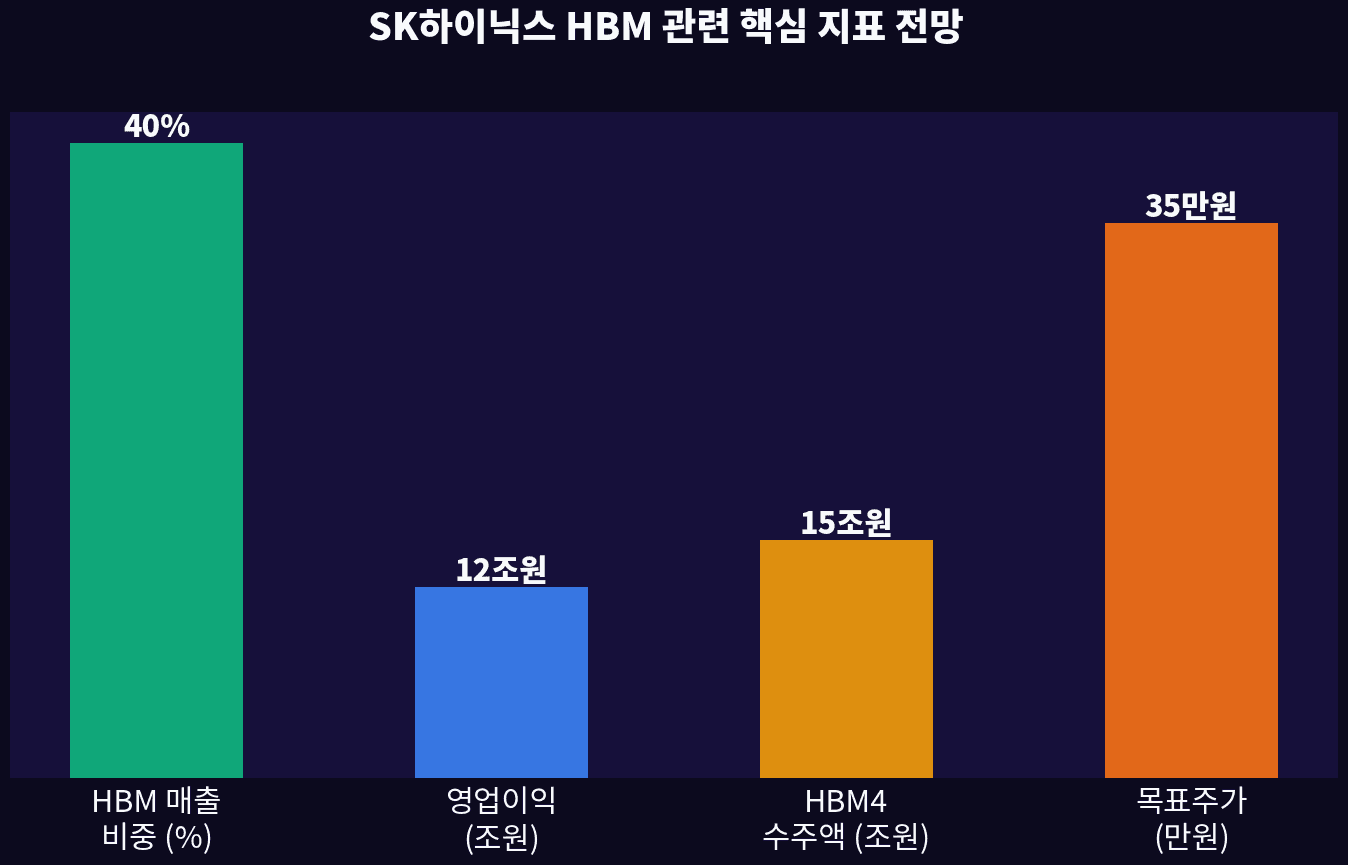

04. SK Hynix Earnings Outlook — How Big Is the HBM4 Lift?

Powered by expanding HBM4 supply, SK Hynix’s 2026 operating profit is projected at KRW 12–15 trillion. As HBM crosses 40% of total DRAM revenue, margins are improving sharply — and major brokerages are upgrading price targets in unison.

| Brokerage | Target price | Rating | Key thesis |

|---|---|---|---|

| KB Securities | KRW 350k | BUY | HBM4 exclusive windfall, KRW 15T OP outlook |

| Mirae Asset | KRW 330k | BUY | Solid data center demand, margin expansion |

| Samsung Securities | KRW 320k | BUY | HBM ASP rising, inventory normalized |

| Shinhan Investment | KRW 340k | BUY | NVDA exclusive secured through 2027 |

| Goldman Sachs | KRW 340k | BUY | Top AI supercycle beneficiary |

At today’s KRW 220–240k, SK Hynix trades roughly 40–50% below consensus targets of KRW 330–350k. With PBR near 2.0x, it screens as undervalued for a semiconductor up-cycle.

05. HBM4 Competition — Can Samsung Catch Up?

Samsung is racing to close the gap in HBM4, targeting NVDA qualification (supplier certification) in H2 2026. If it clears the qual, it could capture 30–35% of the HBM4 market. The pivotal variable, though, is its 6–9 month technology gap behind SK Hynix.

| Comparison | SK Hynix | Samsung | Micron |

|---|---|---|---|

| HBM4 mass production | H1 2026 start | H2 2026 expected | 2027 expected |

| NVDA qual status | Passed | In progress | HBM3E only |

| Stack height (Hi) | 16Hi roadmap | 12Hi → 16Hi | 12Hi |

| TSV (through-silicon via) | Leader | Gap exists | Chasing |

| 2026 HBM share | ~58% | ~32% | 8% |

| NVDA supply volume | Exclusive (through 2027) | Possible partial in H2 | Minor |

If Samsung’s NVDA HBM4 qualification slips, SK Hynix’s exclusive position strengthens further. Conversely, a successful H2 qual could put short-term pressure on SK Hynix’s share price. Track this variable closely.

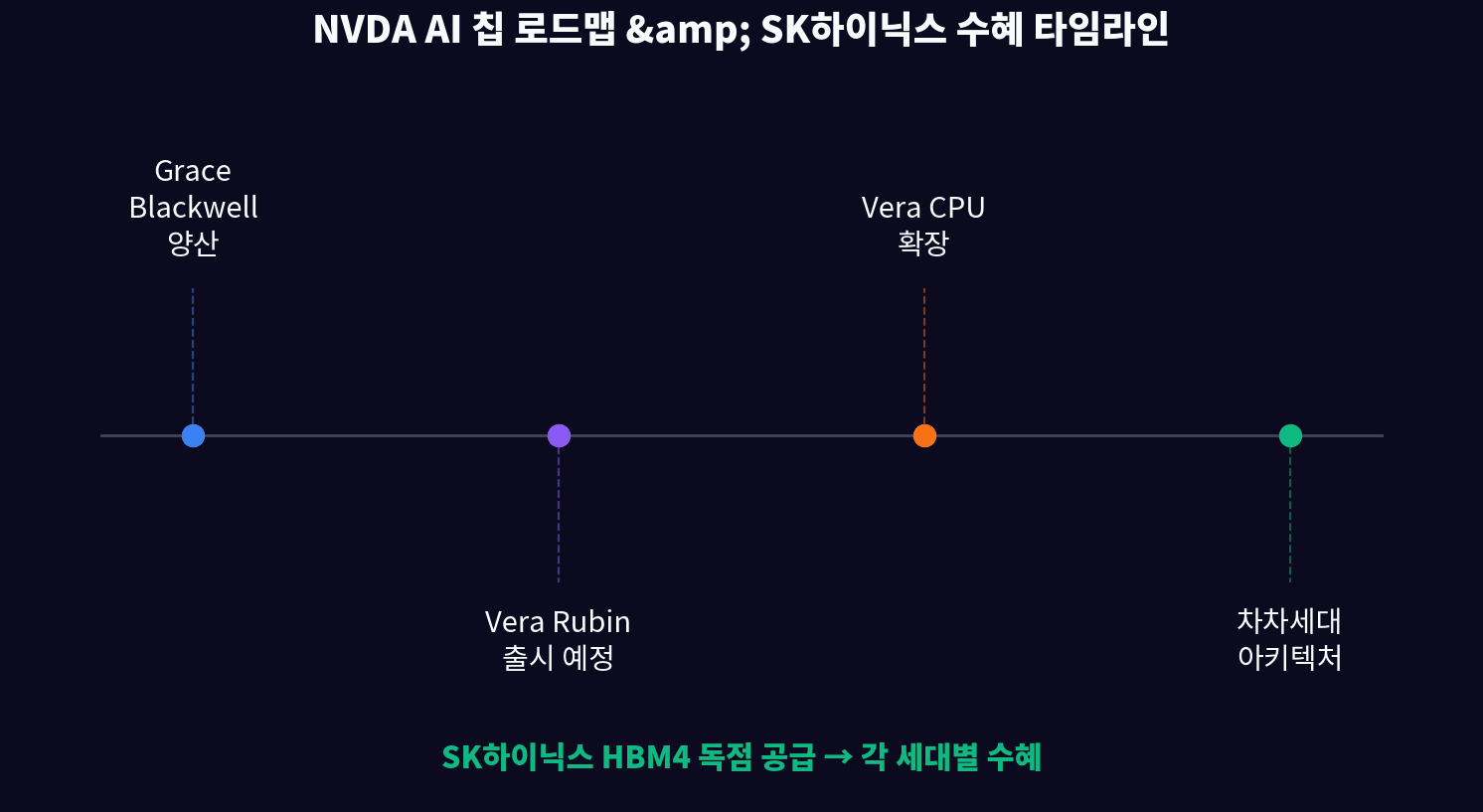

06. NVDA Chip Roadmap & Long-Term HBM Demand

Nvidia has committed to an “annual cadence” roadmap, releasing a new AI chip architecture every year. After Grace Blackwell comes Vera Rubin (late 2026) and the generation beyond — already on the official roadmap. Each generation roughly doubles HBM capacity and bandwidth, multiplying SK Hynix’s addressable demand.

| Chip generation | Launch | HBM gen | HBM per GPU | SK Hynix role |

|---|---|---|---|---|

| Hopper (H100) | 2022–2024 | HBM3 | 80GB | Major supplier |

| Blackwell (B200) | 2025–2026 | HBM3E | 192GB | Sole supplier |

| Grace Blackwell (GB200) | 2025–2026 | HBM3E | 480GB (system) | Sole supplier |

| Vera Rubin | H2 2026 | HBM4 | ~256GB+ | Exclusive contract pursuit |

| Vera Rubin Ultra | 2027 | HBM4 | ~512GB+ | Exclusive contract pursuit |

- 2026: HBM4 shipments projected 3x YoY (SK Hynix guidance)

- 2027: GB300 / Vera Rubin system HBM4 consumption = 6x current

- 2028: Transition to HBM4e (next-gen) — SK Hynix technology gap widens further

- ASP: HBM4 prices at least 30% above HBM3E, driving sharp margin expansion

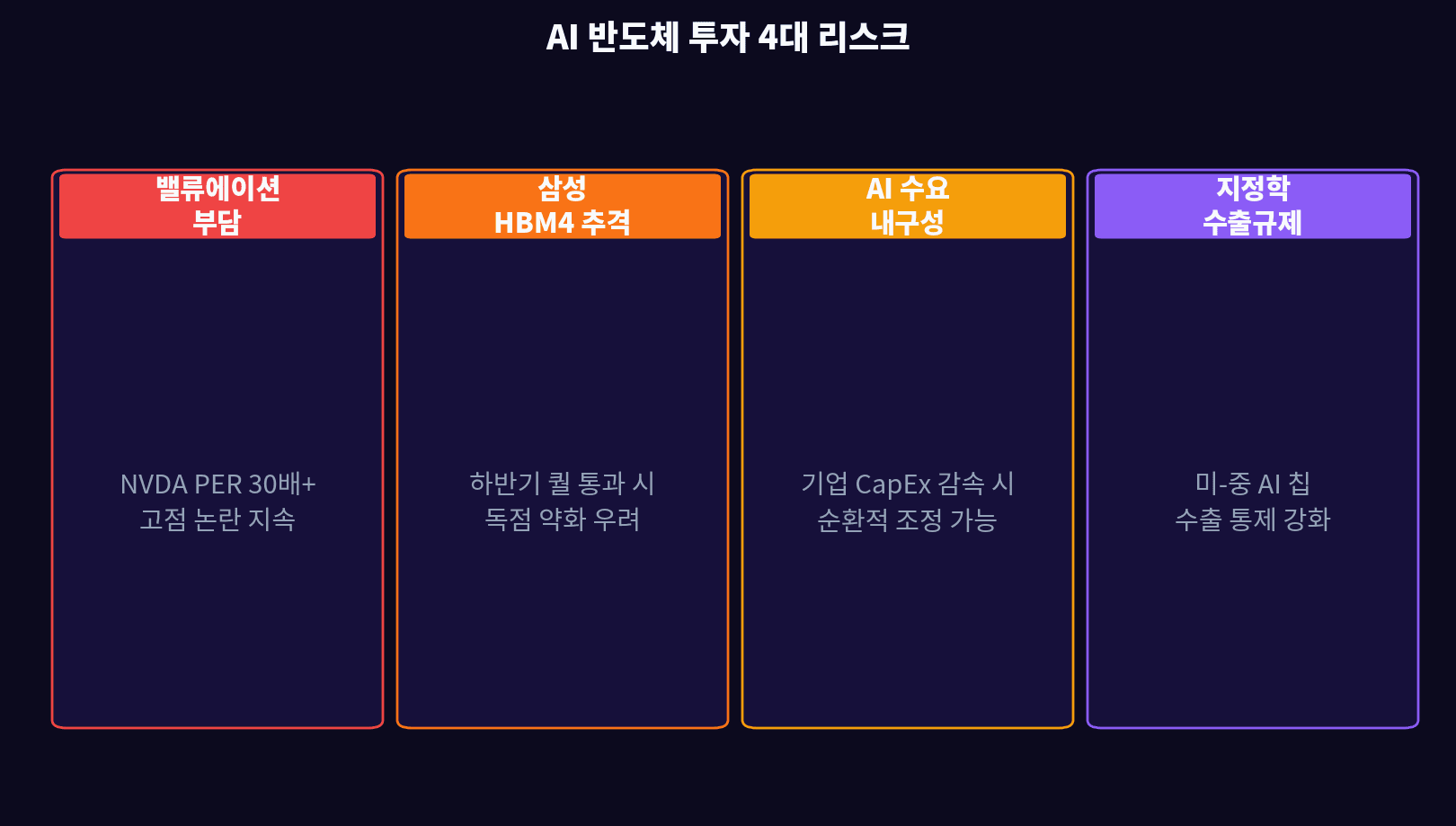

07. Investment Risks — 5 Variables You Cannot Ignore

The biggest risk in AI semiconductor investing is the durability of demand. Today’s big-tech CapEx is largely front-loaded ahead of full AI monetization. If AI services fall short of monetization expectations, CapEx could decelerate — which would feed straight through to slower HBM demand.

| Risk type | Detail | Probability | Response |

|---|---|---|---|

| Valuation pressure | NVDA PER 30x+ peak debate | Medium | Scale in; trim near targets |

| Samsung HBM4 qual pass | SK Hynix exclusivity could weaken | Medium | Trim ahead of qual results |

| AI demand durability | Big-tech CapEx may decelerate | Low–Medium | Watch quarterly results |

| US–China export controls | Tighter AI chip export restrictions | Medium–High | Re-rate NVDA on lower China mix |

| Iran war prolonged | Macro uncertainty rising | Medium | Hedge with USD and gold |

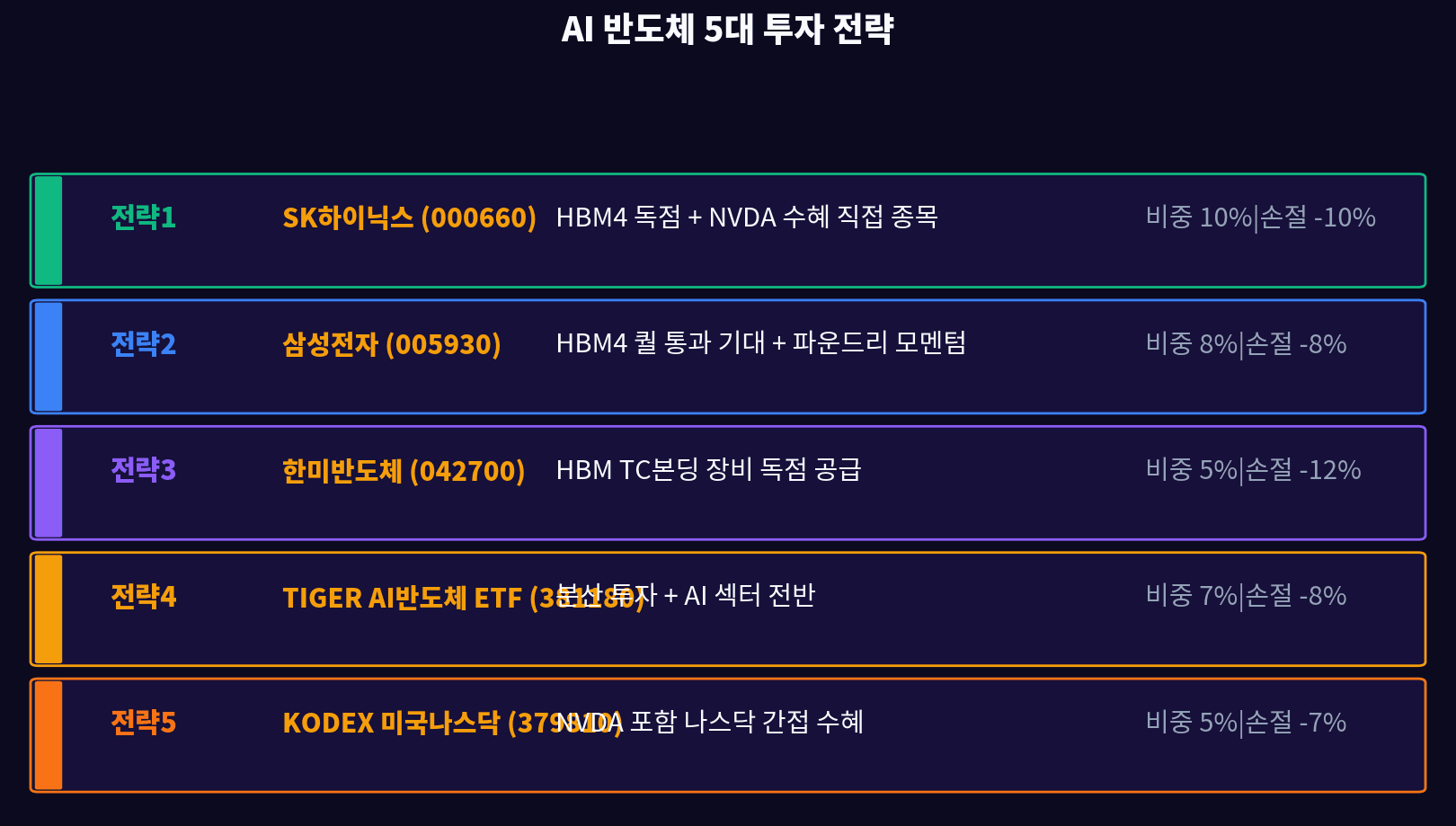

08. Five AI Semiconductor Investment Strategies (May 25, 2026)

Below are five strategies that translate the Nvidia surprise and SK Hynix’s HBM4 windfall into a portfolio. The AI supercycle is real, but in overheated short-term windows, scaling in and respecting stop-losses matter more than chasing. This mix is optimized for risk-adjusted returns.

| Strategy | Ticker | Code | Stop-loss | Weight | Thesis |

|---|---|---|---|---|---|

| ① Direct HBM4 | SK Hynix | 000660 | -10% | 10% | NVDA exclusive supplier |

| ② HBM4 catch-up | Samsung Electronics | 005930 | -8% | 8% | Qual upside + dividend |

| ③ Equipment monopoly | Hanmi Semiconductor | 042700 | -12% | 5% | Global TC bonder monopoly |

| ④ Sector ETF | TIGER AI Semiconductor | 381180 | -8% | 7% | Diversified exposure |

| ⑤ Nasdaq proxy | KODEX US Nasdaq 100 | 379810 | -7% | 5% | Indirect NVDA exposure |

Rather than chasing the post-earnings spike, scale in on 3–5% pullbacks. When Samsung HBM4 qual headlines pressure SK Hynix in the short term, treat that dip as an add-on opportunity.

② SK Hynix HBM4 — NVDA exclusive through 2027, ~KRW 15T order book visible

③ Big tech 2026 CapEx $290B (+37%) — HBM demand keeps exploding

④ Sell-side targets KRW 330–350k — 40–50% upside vs current price

⑤ Key risks: Samsung HBM4 qual, US–China controls, AI demand durability — scale in, respect stops

Sources

- NVIDIA Q1 FY2027 Earnings Release (May 22, 2026)

- SK Hynix IR — HBM4 Supply Contract Status (May 2026)

- KB Securities — SK Hynix Target Price Raised to KRW 350k (May 22, 2026)

- Goldman Sachs — AI CapEx Supercycle Analysis (May 2026)

- Bloomberg — Nvidia Beats Estimates as AI Demand Surges (May 22, 2026)

- Meritz Securities — HBM4 Supply & Demand Outlook Report (May 2026)

Disclaimer: This article is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. All investments carry the risk of loss; final decisions are the reader’s own responsibility. Content is based on public information as of May 25, 2026 and accuracy is not guaranteed thereafter.