USD/KRW 1,497 Threat — 1,520 Scenario + BOK Intervention / Korea-US Rate Gap / US 30Y 5.13% / 5 FX Strategies + Playbook

Real-Time Issue · May 19, 2026

USD/KRW 1,497 Threat — 1,520 Scenario, BOK Intervention Risk, Korea-US Rate Gap 225bp, US 30Y at 5.13%, 1.8T KRW Foreign Selling, 5 FX Strategies + May 18 Playbook

1. Overview — 1,497: Testing the Year’s High

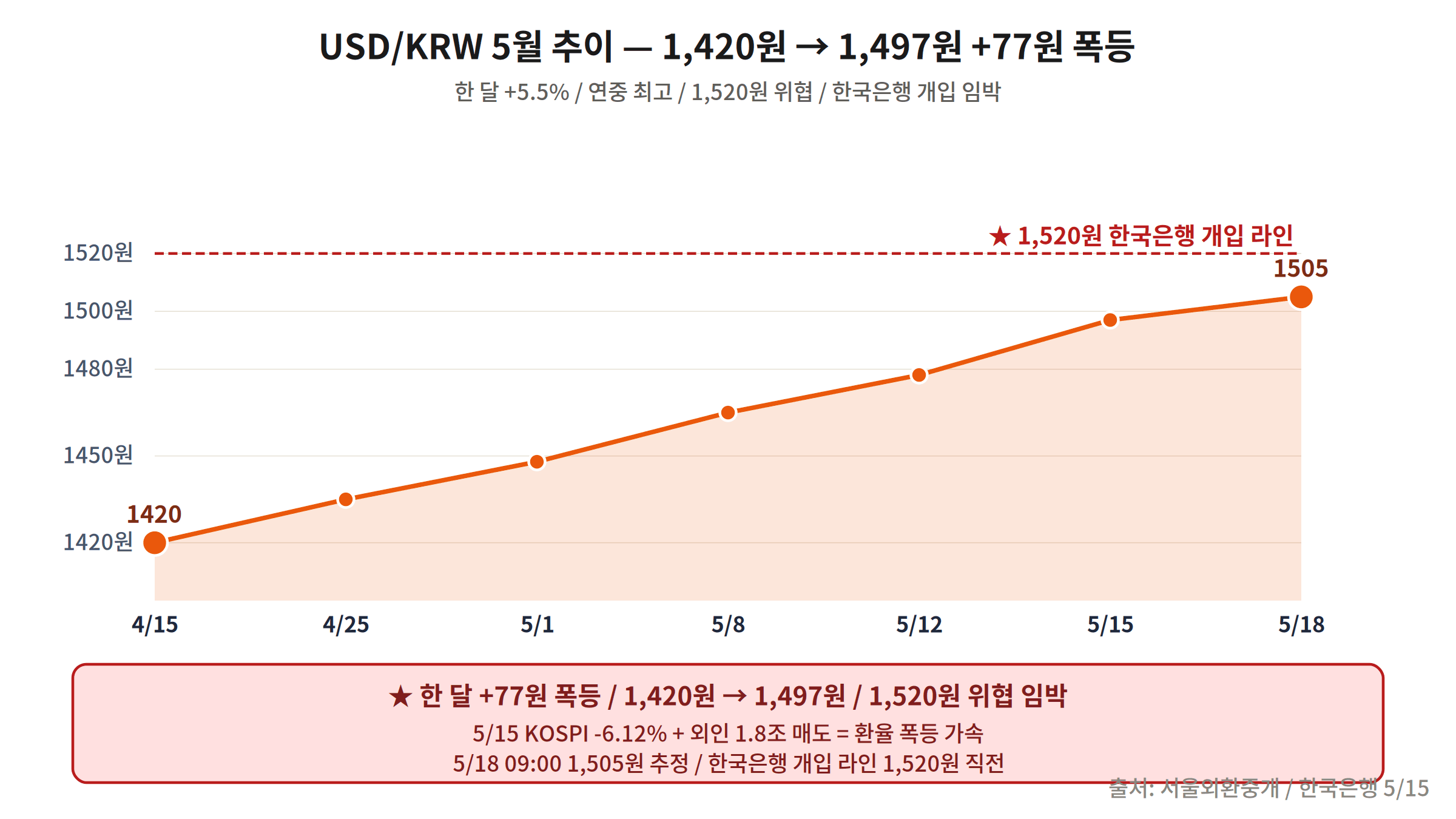

On Friday, May 15, 2026, USD/KRW surged to an intraday high of 1,497, closing in on its year-to-date peak. Compared to 1,420 on April 15 — just 22 trading days earlier — the won had depreciated by +77 won (+5.5%). On the same day, the KOSPI plummeted −6.12%, once again confirming the market’s established pattern of dollar strength and Korean equity weakness feeding each other.

Market participants are rapidly circulating a scenario in which a break above the key psychological level of 1,500 could bring in momentum buyers and push the rate to 1,520 within seven trading days. The 1,520 level is comparable to the external shock highs seen in October 2022, making the Bank of Korea’s (BOK) decision on direct intervention the single biggest variable to watch.

2. May Rate Trajectory — +77 Won in a Month

Through mid-April, the exchange rate remained broadly stable in the 1,420 range. The turning point came on April 22, when US Treasury officials signaled tolerance for a stronger dollar, prompting the first wave of won selling. The release of FOMC minutes on May 2 — which reaffirmed a “higher for longer” rate stance — then triggered a swift break above 1,460.

A large wave of foreign institutional selling on the KOSPI between May 8–12 added fresh pressure, pushing the rate step by step from 1,480 to 1,497. The average daily range has expanded to ±9 won, more than double the trailing 12-month average of ±4.2 won — a level of volatility that typically draws the attention of FX authorities.

3. Five Root Causes of the Surge

- Widening Korea-US Rate Differential: The Fed funds rate stands at 5.50% versus the BOK base rate of 3.25%, a gap of 225 basis points. Carry-trade unwinding is translating directly into sustained won selling pressure.

- KRW 1.8 Trillion in Foreign Net Selling: Between May 1–15, foreign institutions net-sold a cumulative KRW 1.84 trillion on the KOSPI. The cycle of equity selling → won conversion → dollar repatriation is self-reinforcing the exchange rate rise.

- US 30-Year Treasury Yield at 5.13%: Safe-haven flows into long-dated US Treasuries have pushed the dollar index (DXY) to 105.8. The spread between Korean 10-year bonds and their US equivalents has widened to 180bp.

- Broad Dollar Strength (DXY 105.8): The euro and yen are both weakening simultaneously, generating across-the-board dollar gains. Among major Asian currencies, the won’s year-to-date depreciation of −5.8% is the largest in the region.

- Iran Geopolitical Risk and Energy-Driven Inflation: The collapse of renewed Iran nuclear talks has pushed WTI crude to $87 per barrel. As a major energy importer, South Korea faces mounting current-account deterioration risk, stoking additional won-selling sentiment.

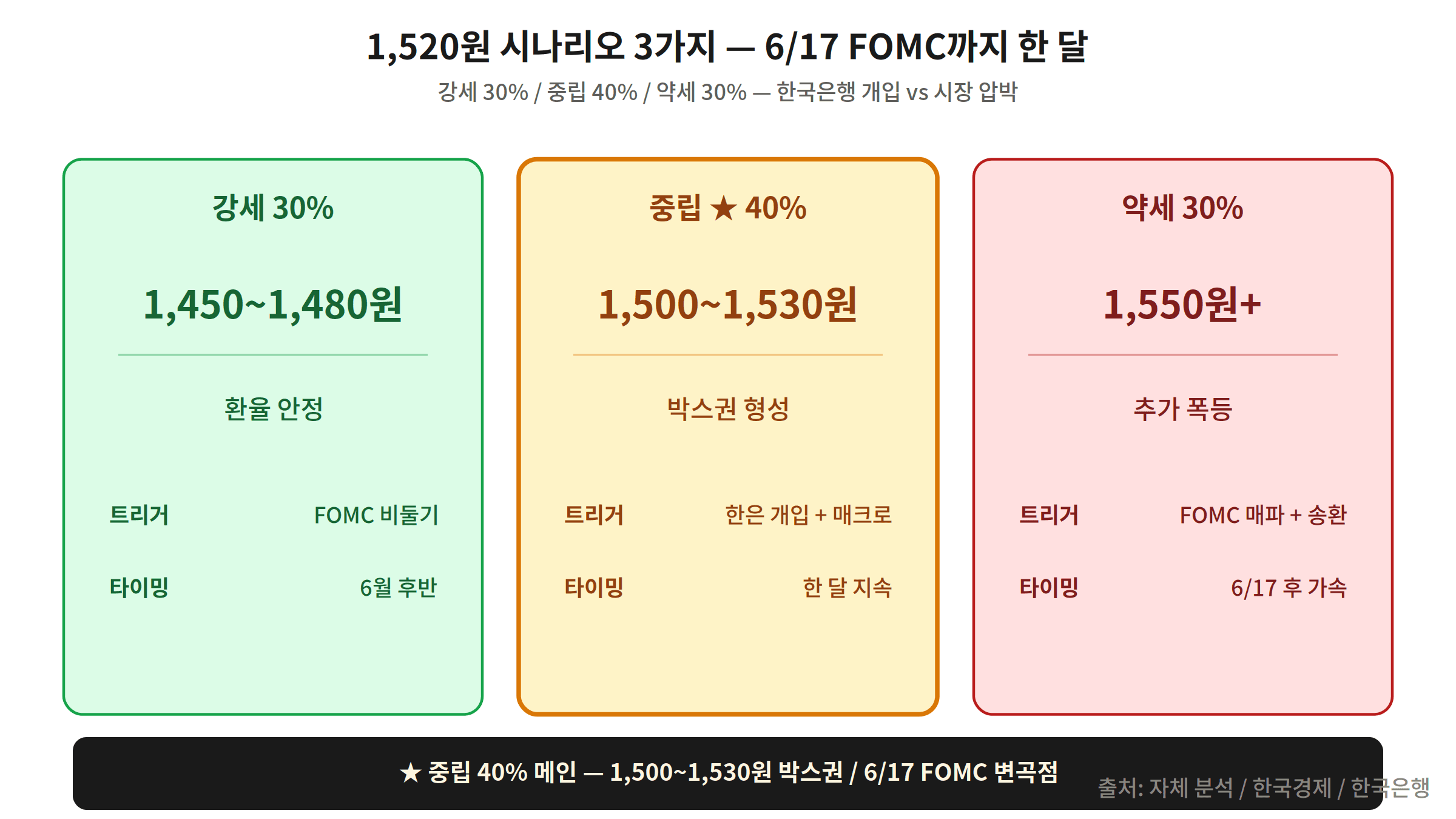

4. The 1,520 Scenario — Three Possible Paths

Markets are currently pricing three distinct paths forward.

- Breakout to 1,520 (30% probability): Requires continued dollar strength and the Fed to pass on a June rate cut again. Technically, a clean break above 1,500 could bring the rate to 1,520 within 3–5 trading days as momentum buyers engage. With the 2022 peak of 1,444 already surpassed, psychological resistance is eroding fast.

- Range-Bound 1,480–1,510 (40% probability): BOK verbal warnings collide with exporter hedge-selling (net-don selling) in this band. If authorities hold an “observation” stance through the May 30 FX policy meeting, oscillation within this range is the base case.

- Pullback to 1,460s (30% probability): A downside surprise in US CPI or a dovish pivot from a Fed official could trigger a rapid reversal. A DXY drop back to the 102–103 zone would likely bring the won along for the ride.

5. Five Ripple Effects if 1,520 Is Breached

- Self-Reinforcing Foreign Selling on the KOSPI: Rate rises → mark-to-market losses on won assets → more selling → further rate rise. Foreign investors hold roughly 28% of KOSPI market cap, creating a large potential overhang.

- Export Stocks: Short-Term Tailwind, Long-Term Headwind: Companies like Samsung Electronics and Hyundai Motor, with high dollar-revenue exposure, see near-term earnings boosts from translation effects. However, global demand softening and rising dollar-denominated input costs typically weigh on earnings with a 6-month-plus lag.

- Mortgage Rates Breaking 6%: Rate surge → higher foreign-currency funding costs for banks → passthrough to mortgage benchmarks. Variable-rate home loans are estimated to rise to 6.0–6.3%, adding an average of KRW 140,000/month to household repayments.

- Import Inflation Reignited: Energy and food import costs face an additional annualized +3.2 percentage-point pressure from currency translation. CPI will reflect this with a 6–8 week lag into Q2 data.

- Profit-Taking Pressure on US Equity Investors: As won-denominated returns on overseas holdings swell, the temptation to realize gains grows — capping the reflow of domestic capital. Overseas equity ETFs managing roughly KRW 45 trillion in AUM represent a meaningful latent FX demand overhang.

6. BOK Intervention Scenarios

The BOK and the Ministry of Economy and Finance (MoF) have a tiered toolkit that activates at different exchange rate thresholds.

- Verbal Intervention (upon 1,500 breach): Official statements warning against “excessive one-sided moves” and pledging to take “market stabilization measures if necessary.” In 2023, similar BOK verbal interventions produced an average pullback of −12 won in the short term.

- Direct Smoothing Operations (approaching 1,520): Dollar sales from the National Pension Service (NPS) and official FX reserves. South Korea’s FX reserves stood at USD 412.3 billion as of end-April 2026. This can cushion the rate for one to two weeks but does not address structural drivers.

- Korea-US Currency Swap (1,550+ crisis scenario): In March 2020, the BOK secured a USD 60 billion swap line with the Fed. No permanent standing facility currently exists; the mere announcement of negotiations would likely produce a sharp psychological stabilization effect.

- May 30 FX Policy Meeting: Separate from the regular Monetary Policy Committee, the MoF-led foreign exchange market review is scheduled for May 30. Its outcome could sharply redirect market direction — position management around May 29–30 is essential.

7. Five Investor Strategies

- Maintain 30% Dollar Asset Allocation: The baseline hedge for a KRW-heavy portfolio. Dollar time deposits at major Korean banks currently yield 4.8–5.1% p.a., offering a genuine carry advantage over won deposits. Above 1,520, consider staged selling rather than adding to positions.

- KODEX USD Futures ETF: Gain dollar exposure without a bank FX conversion — real-time trading, tight spread of 0.02–0.05%, and a total expense ratio of 0.25% p.a. Daily trading volume exceeds KRW 30 billion, ensuring adequate liquidity. Dollar-cost average in below 1,480 on pullbacks.

- Overweight Export Stocks (Samsung Electronics, Hyundai Motor): Every 10-won rise in USD/KRW adds roughly KRW 200 billion to Samsung’s annual operating profit and KRW 80 billion to Hyundai Motor’s (consensus estimates). However, reassess weighting if 1,520 breaks, as global demand deterioration typically dominates over a 6-month horizon.

- Consider Fixed-Rate Mortgage Conversion: Once variable mortgage rates breach 6%, the 5-year fixed rate (currently 5.45–5.60%) becomes economically attractive. Calculate the breakeven period against early repayment fees — typically 18–24 months — before switching.

- Remove FX Hedge on US Equity Positions: In a won-weakening environment, unhedged S&P 500 ETFs outperform their hedged counterparts. Year-to-date, TIGER US S&P 500 (unhedged) has outperformed TIGER US S&P 500 (H) by +4.9 percentage points. Stay unhedged until the dollar shows a structural reversal.

8. FX Strategy Practical Guide

In a high-volatility FX environment, understanding each instrument’s mechanics is critical before committing capital.

- KOFEX Dollar Futures (Short-Term Hedging / Speculation): Contract size of USD 10,000, initial margin approximately KRW 1.2 million per contract. The inherent leverage makes this instrument suitable only for directional short-term trading with high conviction. Always pre-calculate rollover costs and margin call thresholds. Individual investors should limit exposure to 1–2 contracts maximum.

- KODEX US Treasury Ultra 30Y Futures (H): With the 30-year yield at 5.13%, this ETF allows investors to position for a rate decline (bond price rise). Choose the unhedged variant if you also want dollar exposure alongside the rate bet. Duration means every 1bp move in yield translates to approximately −0.25% in NAV.

- Foreign Currency Deposits vs. Dollar ETFs — Side by Side: Foreign currency deposits carry deposit insurance up to KRW 50 million but involve an FX conversion spread of ~1.5%. Dollar ETFs trade in real time with a spread of just 0.02–0.05% but offer no deposit protection. Rule of thumb: ETFs win on cost for horizons under 3 months; foreign currency deposits are more cost-efficient for positions held over 12 months.

9. May 18 Playbook — What to Do Right Now

The key market variable for the week of May 18–23 is the FOMC meeting minutes release and Fed speaker appearances on Thursday, May 22. Follow these four action points.

- Execute Dollar Diversification Now: Investors with zero dollar exposure should convert 20–30% of liquid cash into dollar deposits or a dollar ETF this week. If USD/KRW breaks above 1,500, resist chasing — instead, wait for a pullback to the 1,480 range and add incrementally.

- Book a Mortgage Rate Consultation: Log into your bank’s app and compare the current variable rate against available 5-year fixed rates. If the gap between them is 0.5 percentage points or less, the economic case for switching is now compelling — act before banks reprice upward.

- Review Export-Stock Weighting: If Samsung Electronics, Hyundai Motor, or LG Energy Solution together account for less than 15% of your equity portfolio, consider phased buying at current levels. If 1,520 breaks, however, pause and wait for confirmation from global demand indicators before adding.

- Pre-FOMC Risk Reduction — May 21 Deadline: Volatility around the May 22 minutes release could be severe in both directions. Reduce leveraged positions to no more than half their current size by the evening of May 21. Re-enter after assessing whether the minutes signal a hold, a cut, or a hawkish surprise.

Bottom line: USD/KRW 1,497 is not just a number. Three structural forces — a 225bp Korea-US rate differential, KRW 1.8 trillion in foreign net selling, and a US 30-year yield of 5.13% — are operating simultaneously. The more important question over the next six weeks is not whether 1,500 breaks, but when and with what tools the BOK steps in — and that decision will set the direction.