Korea National Growth Fund Complete Guide — Launches Today, 40% Tax Deduction, 20% Loss Protection, Eligibility, How to Apply

Real-Time Issue · May 22, 2026

Korea National Growth Fund Complete Guide — Launches Today, 40% Tax Deduction, 20% Loss Protection, Eligibility, How to Apply

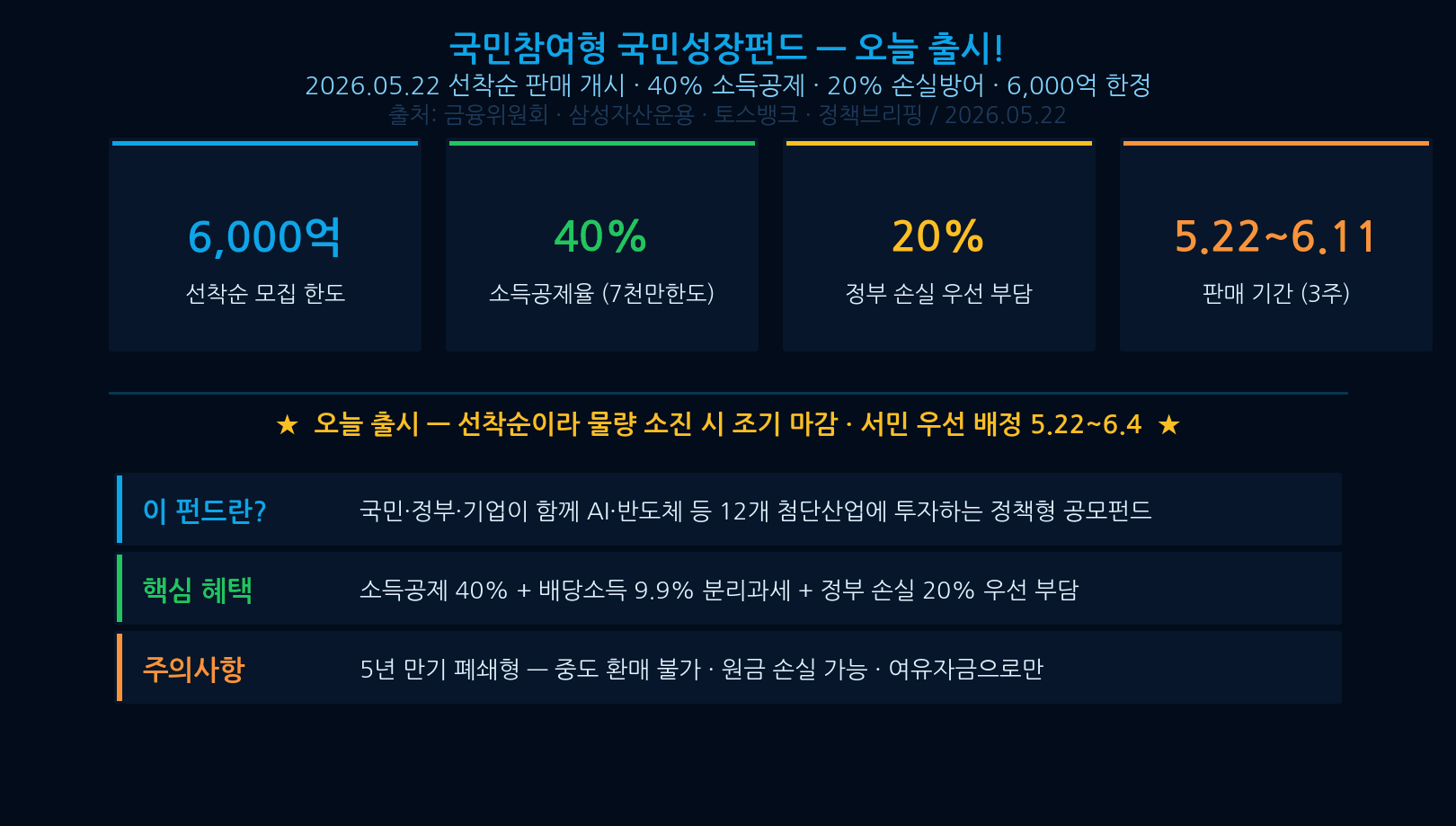

The Korea National Growth Fund officially launched today, May 22, 2026. It offers a 40% income tax deduction on contributions, a government-backed loss protection covering up to 20% of losses, and a per-person investment cap of 3 million KRW. This guide covers every detail — from core benefits to eligibility, how to apply, and six key risks to know before signing up.

1. Key Summary — 5 Things You Need to Know Today

Here are the five essential facts about the Korea National Growth Fund at a glance.

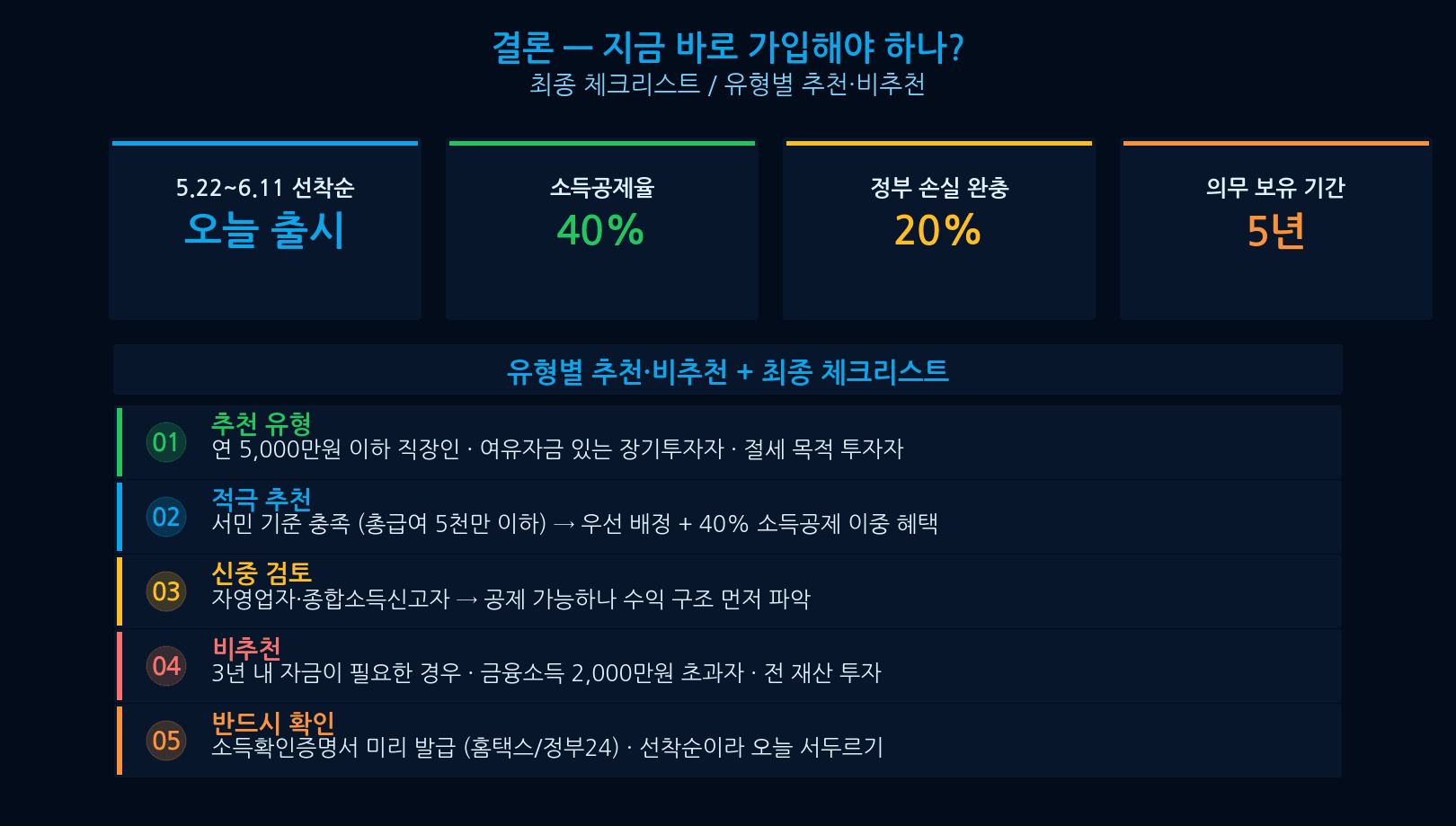

- Launches today (May 22) — The subscription window runs from May 22 to May 31.

- 40% income tax deduction — 40% of your contribution is deducted from taxable income, up to a maximum deduction of 1.2 million KRW.

- Government covers first 20% of losses — If the fund incurs losses, the government absorbs the first 20% before investors bear any loss.

- 3 million KRW per-person cap — Each individual may contribute up to 3 million KRW in total.

- 5-year mandatory holding period — Tax benefits are only retained if the investment is held for a full 5 years without redemption.

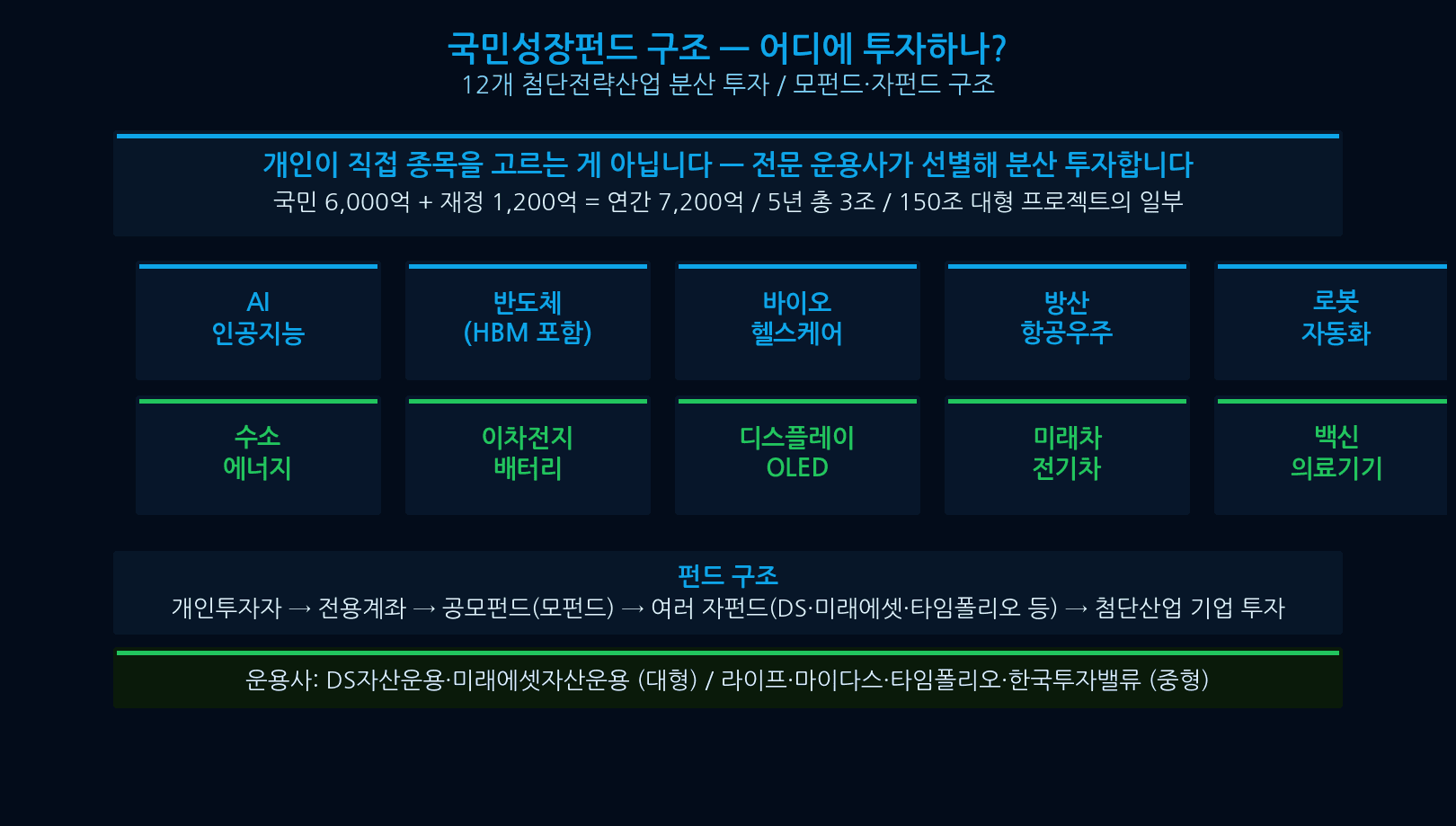

2. Fund Structure and Investment Targets

The Korea National Growth Fund operates as a public offering fund, managed by professional asset management firms. Individual investors do not need to select stocks themselves.

- Investment targets — The fund focuses on blue-chip stocks listed in the KOSPI 200 and KOSDAQ 150 indices.

- Public offering (공모펀드) structure — Retail investors can participate with relatively small amounts and gain broad diversification.

- 10 asset managers participating — Major Korean firms including Mirae Asset, Samsung, KB, and Korea Investment Management are among the 10 participating managers.

- Diversified portfolio — The structure limits single-stock concentration risk by spreading exposure across large-cap quality equities.

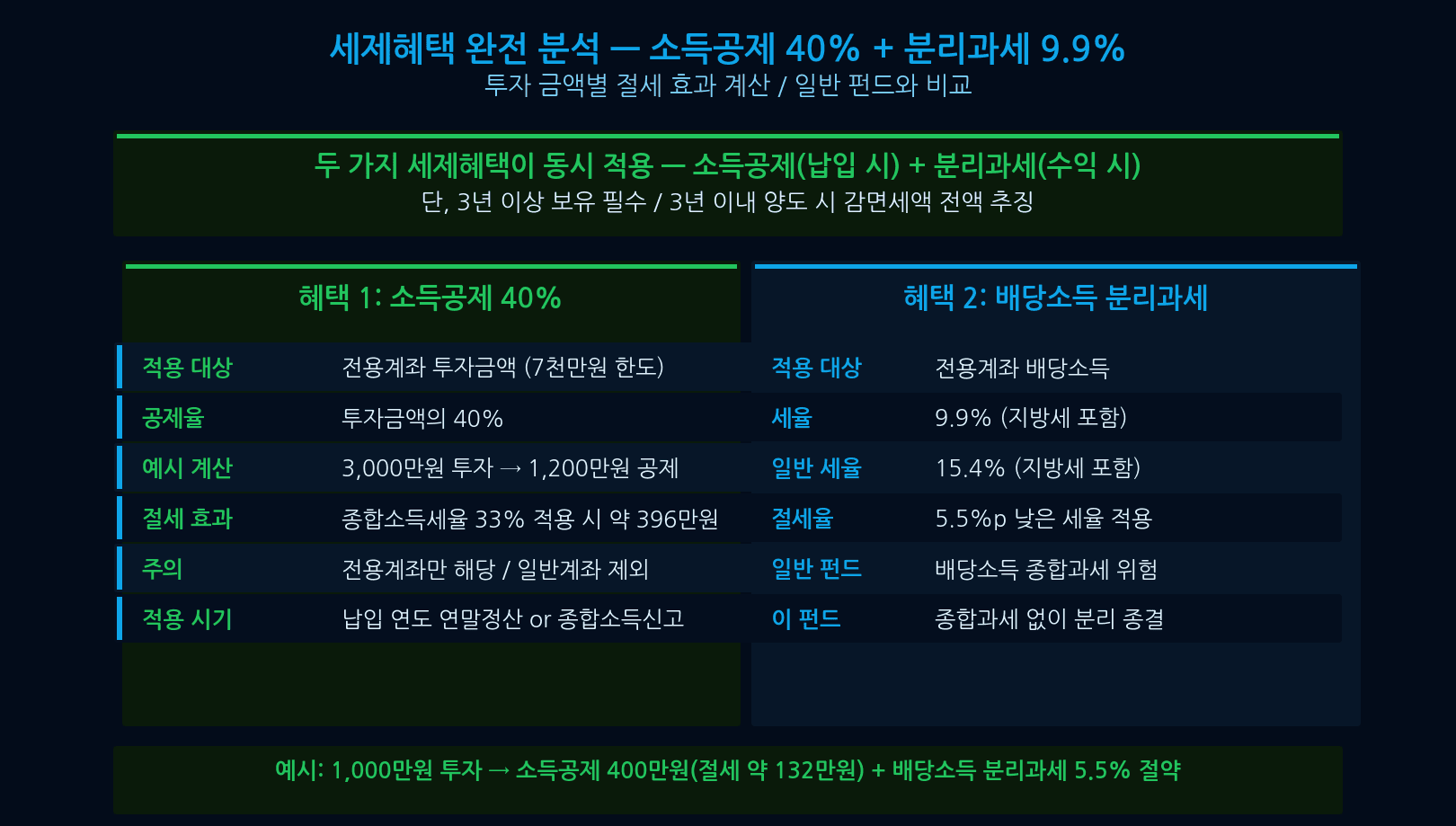

3. Tax Benefits — 40% Deduction and 9.9% Separate Taxation

Two distinct tax advantages set this fund apart from standard equity products: an upfront income deduction and preferential tax treatment on gains.

- 40% income tax deduction — On the maximum contribution of 3 million KRW, investors can deduct 1.2 million KRW from taxable income. The actual tax saving varies by income bracket.

- 9.9% separate taxation on gains — Investment returns are taxed at a flat 9.9% rate and excluded from global income aggregation, offering significant savings for higher earners.

- Dual-layer benefit — The combination of a contribution-stage deduction and a gains-stage flat rate makes the after-tax return substantially higher than ordinary funds or direct stocks.

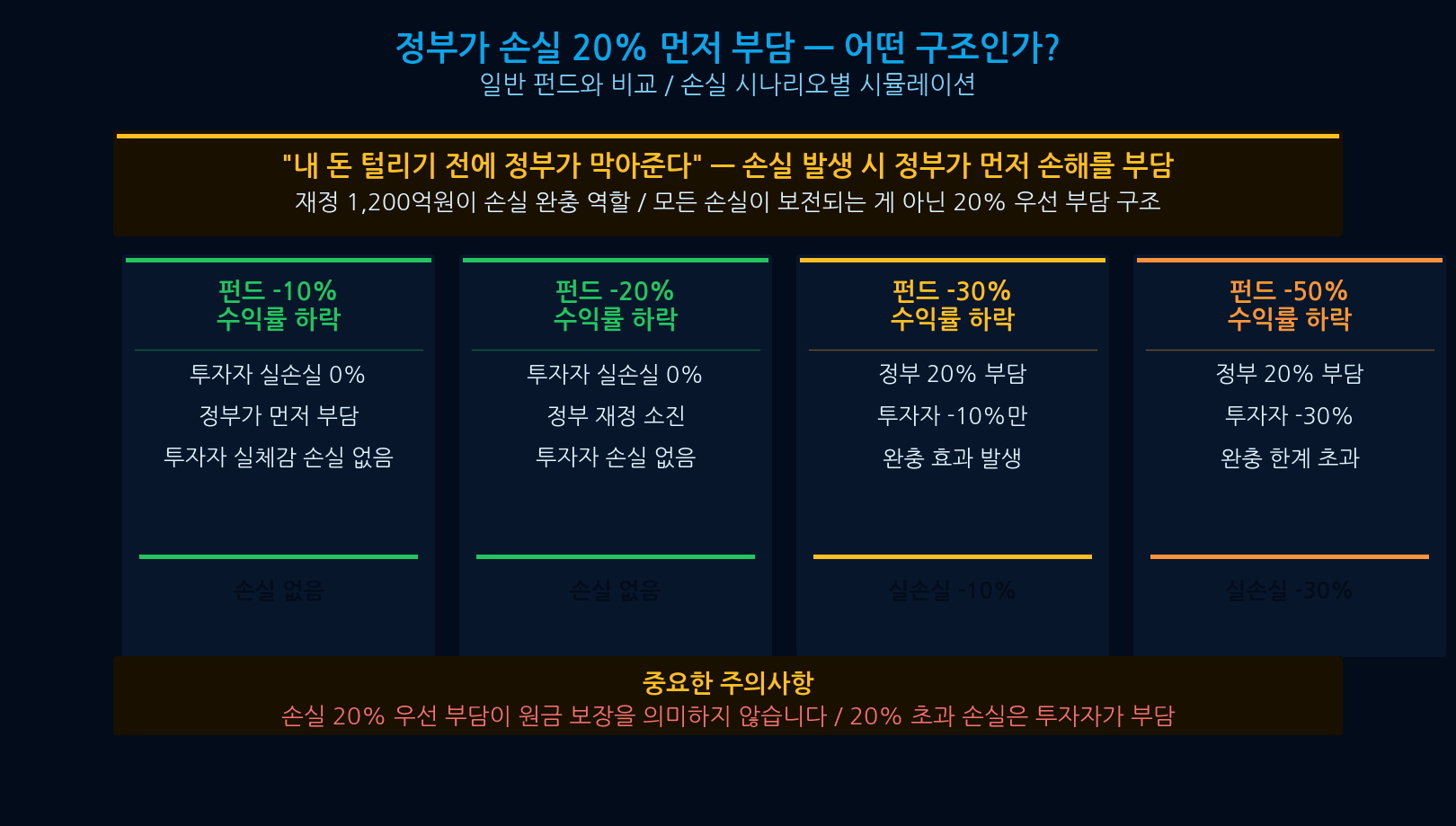

4. Government Loss Protection — 20% Buffer, Not a Capital Guarantee

The government’s loss protection mechanism is real, but it is often misunderstood. This is not a capital guarantee — read carefully before investing.

- Government absorbs first 20% of losses — If the fund’s net asset value declines, the government bears the first 20% of that loss on behalf of investors.

- Capital is not guaranteed — Losses exceeding 20% fall entirely on the investor. A severe market downturn can result in meaningful principal loss.

- Conditional protection — The loss buffer applies only if the mandatory 5-year holding period is honored. Early redemption may forfeit this protection.

- Market-linked product — Despite government backing, this is an equity-linked fund. Principal loss is always a possibility.

5. Eligibility — Who Can Apply?

Eligibility criteria are relatively broad. There is no minimum income requirement, but those subject to comprehensive financial income taxation are excluded.

- Age 19 or older, Korean resident — Any adult residing in Korea may apply, including salaried workers, self-employed individuals, and homemakers.

- No income threshold — Unlike some policy financial products, there is no upper or lower income limit for participation.

- Excluded: comprehensive financial income taxpayers — Individuals whose annual financial income (interest + dividends) exceeds 20 million KRW are ineligible.

- Foreign residents — Foreign nationals residing in Korea should confirm eligibility with their brokerage or bank, as additional conditions may apply.

6. How to Apply — Subscription Open Through May 31

The subscription window is open from May 22 to May 31, 2026. Applications can be submitted entirely online through participating brokerage or banking apps.

- Brokerage apps and branches — Search for “국민성장펀드” (Korea National Growth Fund) in the app of any participating firm — Mirae Asset, Samsung Securities, KB Securities, Korea Investment & Securities, and others.

- Banking apps — Participating banks also offer mobile sign-up through their apps.

- Subscription period — From today, May 22, through May 31. Allocations are made on a first-come, first-served basis once demand is confirmed.

- Required documents — Government-issued ID for identity verification. A brokerage account at a participating firm is required; financial income tax status is checked automatically by the system.

7. Investment Cap and Priority Allocation for Lower-Income Investors

The per-person cap is 3 million KRW, and 50% of the total fund allocation is reserved for lower- and middle-income investors. Early application is strongly advised given expected demand.

- Maximum 3 million KRW per person — The contribution ceiling is 3 million KRW. Contributions above this limit are not permitted.

- 50% reserved for lower- and middle-income investors — Half of the total fund units are allocated with priority to applicants meeting income-based criteria.

- Remainder for general allocation — Units not claimed through priority allocation are distributed to the general pool of eligible applicants.

- Early closure possible — If subscriptions exceed supply before May 31, the window may close early.

8. Six Risks to Know Before Investing

The benefits are compelling, but this fund carries real risks. Review all six before committing your money.

- No capital guarantee — Government loss protection exists, but your principal is not protected. Market declines can cause real losses.

- 5-year mandatory lock-in — Your funds must remain invested for 5 full years. Do not invest money you may need in the short or medium term.

- Tax benefit clawback on early redemption — Redeeming before the 5-year period triggers repayment of previously received income deductions.

- Uncertain fund performance — Returns are not guaranteed. Different managers will produce different results, and past performance does not predict future outcomes.

- KOSPI / KOSDAQ market risk — A prolonged domestic equity market downturn could push losses well beyond the 20% government buffer.

- Watch for deduction limit overlaps — If you also hold an ISA, pension savings fund, or other deduction-eligible products, confirm that combined contributions do not exceed the annual deduction ceiling.

9. Should You Invest? A Guide by Investor Type

The Korea National Growth Fund is not the right choice for every investor. Use the type-by-type breakdown below to decide whether it fits your financial situation.

- Salaried workers — The 40% income deduction delivers maximum value at year-end tax settlement. If you have 3 million KRW in idle savings you won’t need for 5 years, this is worth serious consideration.

- Self-employed individuals — The deduction reduces comprehensive income tax liability, which can be substantial for the self-employed. Keep investment capital completely separate from operating funds.

- Lower-income investors — Priority allocation improves your odds of securing units. Only apply with genuinely surplus funds — do not invest emergency or essential savings.

- Higher earners (non-comprehensive financial income taxpayers) — The 9.9% separate taxation on gains is highly attractive for those in upper income brackets. Note that those already subject to comprehensive financial income tax are excluded entirely.

For more real-time financial news and trending topics, visit the links below.