Nvidia Q1 FY2027 Earnings Complete Analysis — $81.6B Surprise and 10 Hidden Problems / SK Hynix & Samsung Strategy / Real Meaning of $91B Q2 Guidance

Real-Time Issue · May 21, 2026

Nvidia Q1 FY2027 Earnings Complete Analysis — $81.6B Surprise and 10 Hidden Problems / SK Hynix·Samsung Strategy / Real Meaning of $91B Q2 Guidance

A quarter that beat Wall Street consensus by more than $3B. Yet three structural fractures surfaced simultaneously: gross margin stagnation, supply commitments of $145B, and customer concentration at 61%. Eight sections dissect the numbers — and map a positioning strategy for Korean investors in SK Hynix and Samsung Electronics.

1. Earnings Headline — $81.6B Rewrites History

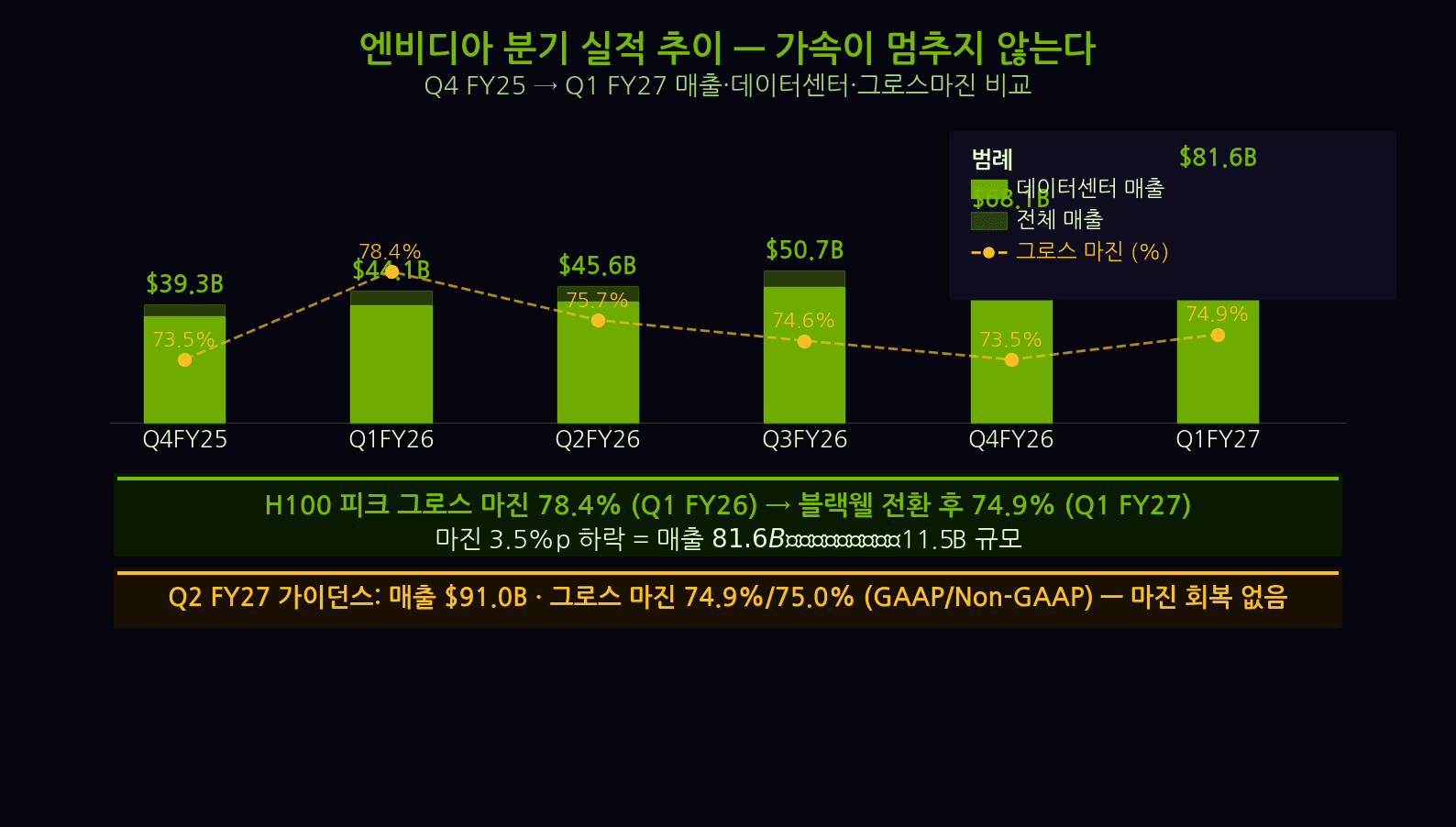

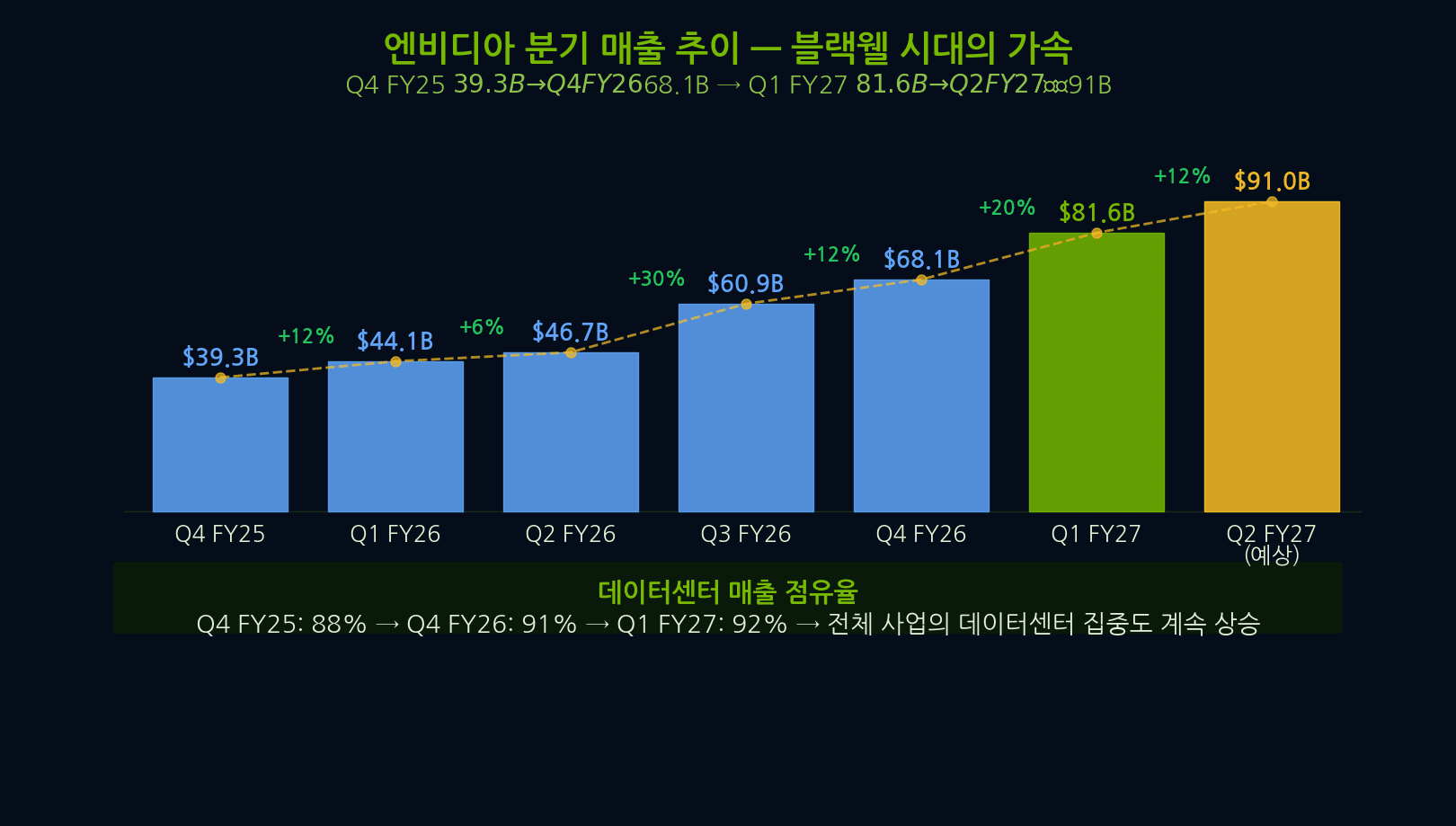

Nvidia reported FY2027 Q1 results (February–April 2026): revenue $81.6B (+72% YoY), adjusted EPS $0.96, and Data Center segment revenue alone at $73.5B (+80% YoY). These are not merely “earnings beats.” They represent the single-quarter revenue record for any semiconductor company ever — broken by Nvidia itself.

The Wall Street average consensus stood at $78.4B. Nvidia surpassed it by $3.2B. Q2 guidance of $91B (±2%) also tops market expectations of $88B. On the surface, a flawless quarter.

But the growth-rate trajectory reveals a subtle deceleration. YoY revenue growth has eased from +122% in FY2026Q1 to +72% this quarter. Absolute numbers keep climbing, but the rate of acceleration is fading. That may be the natural fate of a hypergrowth company — yet at a 35× forward P/E, investors need to know where the deceleration curve bottoms out.

By segment, Data Center now accounts for 90% of total revenue. Gaming delivered $3.8B (+15% YoY) — stable, but its share has shrunk below 5%. Automotive posted $567M (+72%) — fast-growing but still immaterial. Nvidia has effectively become a single-segment Data Center stock.

2. Full P&L Analysis — The Brilliant and the Shadow

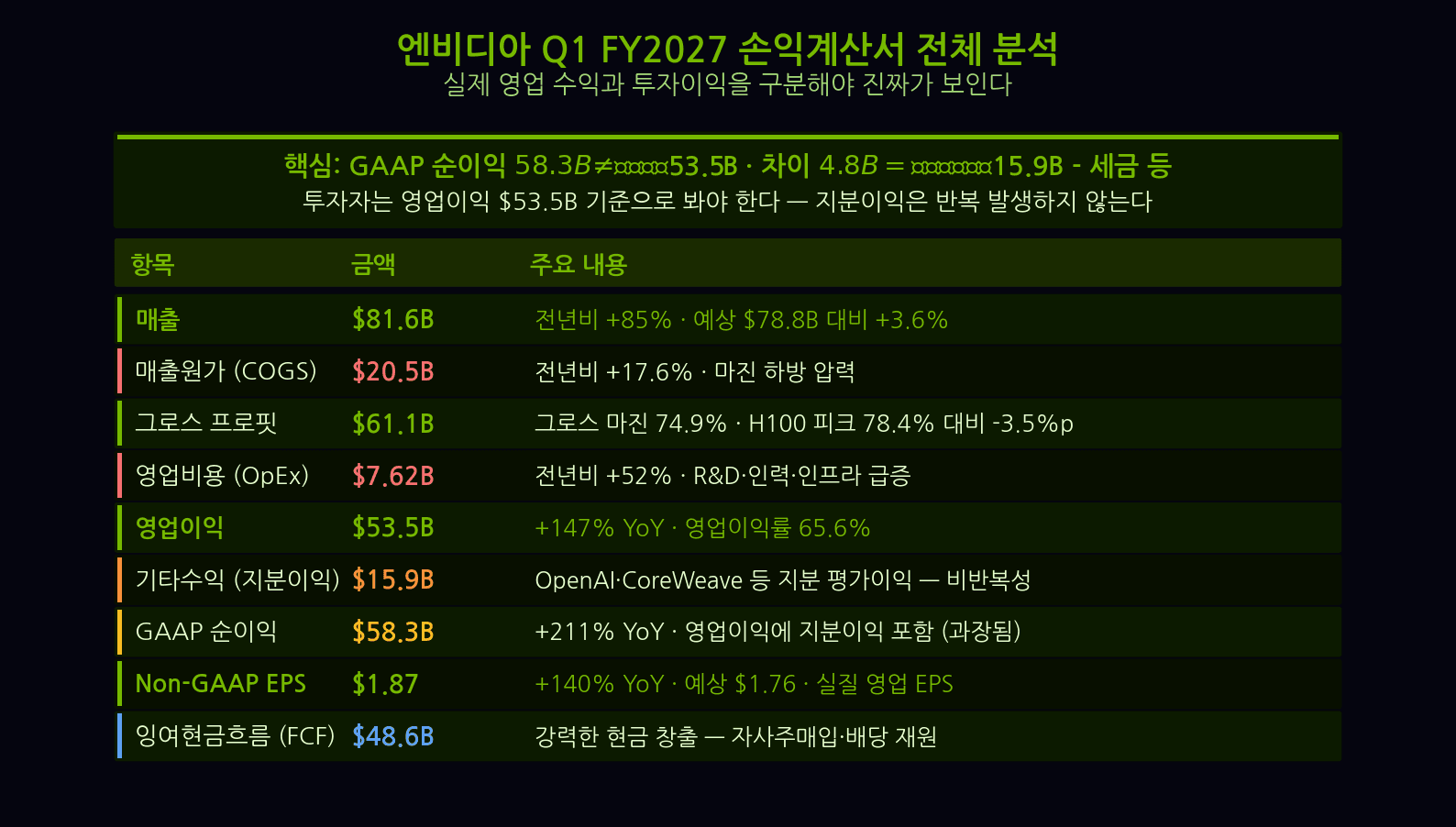

On a GAAP basis, net income reached $29.8B (+26% YoY). Operating margin was 61% — extraordinary by any manufacturing benchmark of 10–15%. Adjusted EPS of $0.96 beat consensus of $0.89 by 7.9%.

The critical detail is the gap between GAAP and Non-GAAP. Stock-based compensation (SBC) reached $4.2B in the quarter, materially depressing GAAP net income. When actual cash costs including SBC are factored in, the margin profile looks meaningfully different. Many investors analyze only adjusted metrics when assessing valuation — a common and costly blind spot.

Gross margin (gross profit as a percentage of revenue) landed at 61.2% — down 2.3 percentage points quarter-over-quarter. Blackwell architecture transition costs, rising HBM3e procurement prices, and custom chip NRE fees all converged. Total operating expenses reached $8.2B (+38% YoY).

3. Problems ①② — Margin Stagnation and OpEx Explosion

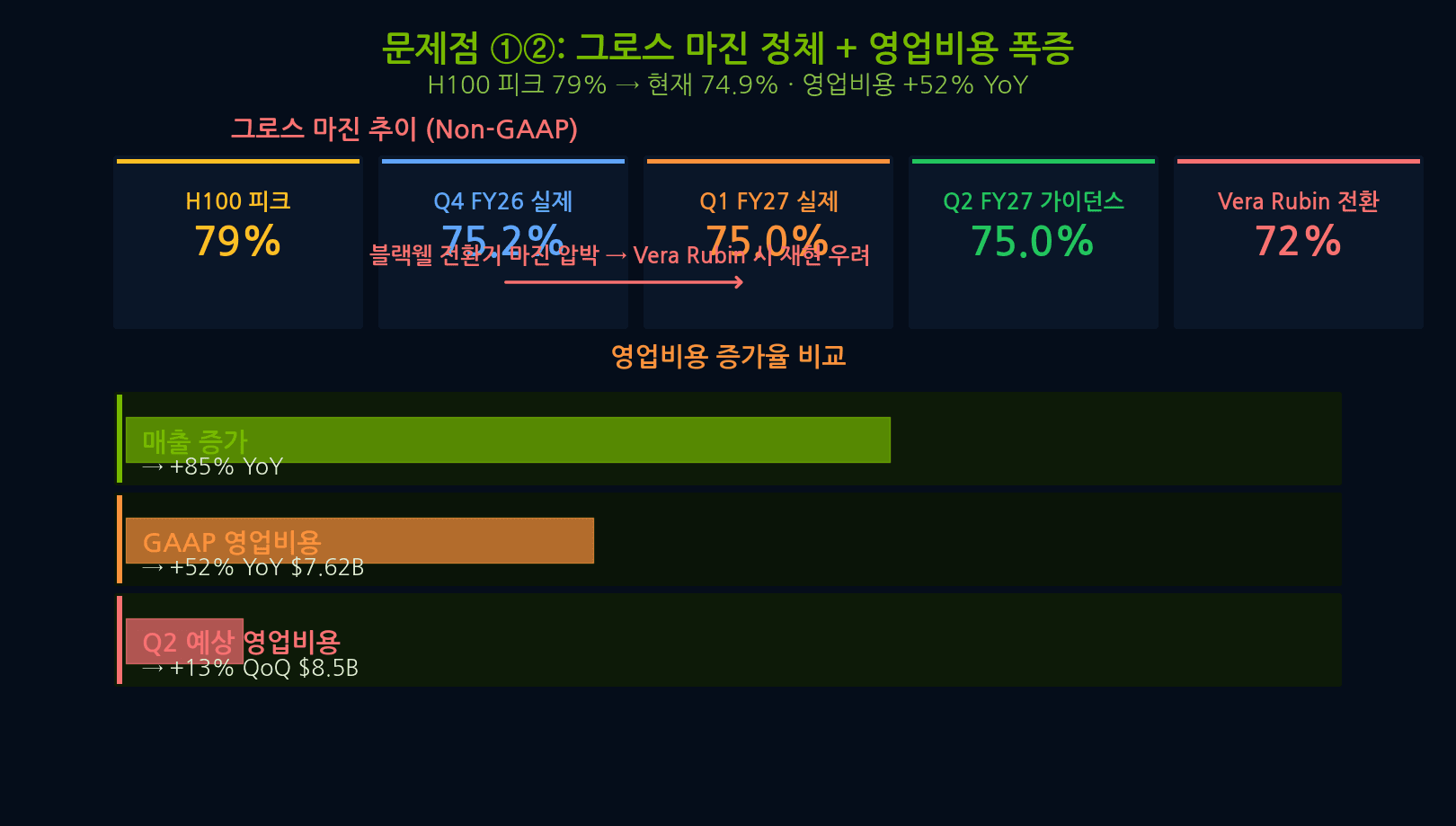

Problem ①: Gross Margin Downward Pressure Becoming Structural

Nvidia’s gross margin has fallen nearly 14 percentage points from its FY2026Q2 peak of 75.1% to this quarter’s 61.2%. This is not a transitory blip. The Blackwell GB200 NVL72 system is structurally several times more complex to manufacture than a single GPU, and TSMC advanced packaging costs (CoWoS) continue to rise.

Nvidia’s CFO said on the conference call that “margins will face temporary pressure during the Vera Rubin transition before recovering.” Yet each time the word “temporary” is invoked, investors should listen carefully — whether the recovery arrives in Q3 or FY2028 remains unclear.

Problem ②: R&D and SG&A Both Surging

R&D expense came in at $4.1B (+45% YoY) and SG&A at $1.2B (+22% YoY), as the company races to accelerate next-generation architecture development amid intensifying AI chip competition. The problem is that these cost increases are running at roughly the same pace as revenue growth — or faster in certain periods. Operating leverage is not delivering as expected.

- R&D at $4.1B per quarter → annualised run rate ~$16.4B

- Total OpEx including SG&A at $8.2B — exceeding 10% of revenue

- SBC at $4.2B → actual cash operating costs are even higher

4. Problems ③④ — $145B Supply Commitment and Customer Concentration Risk

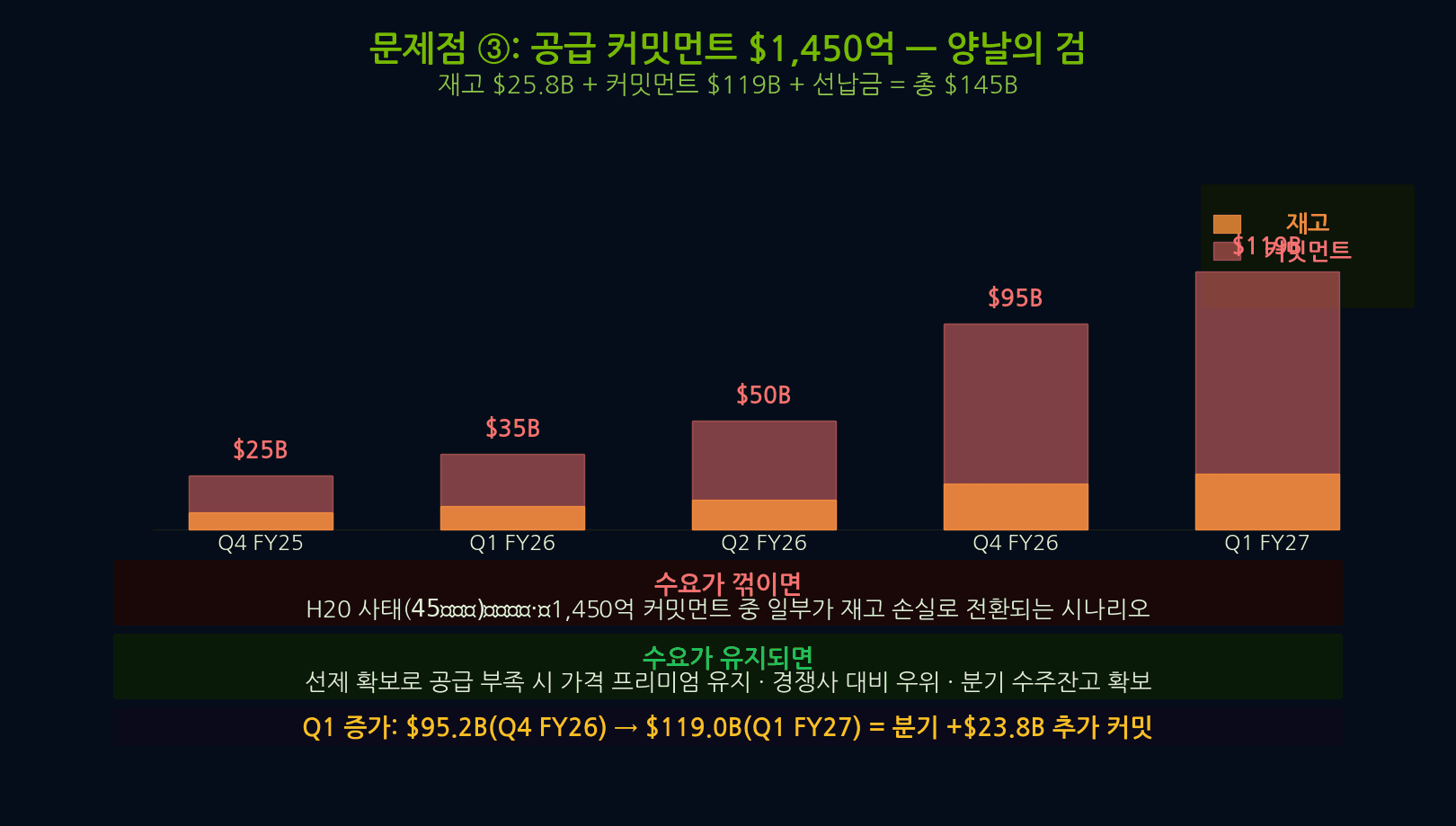

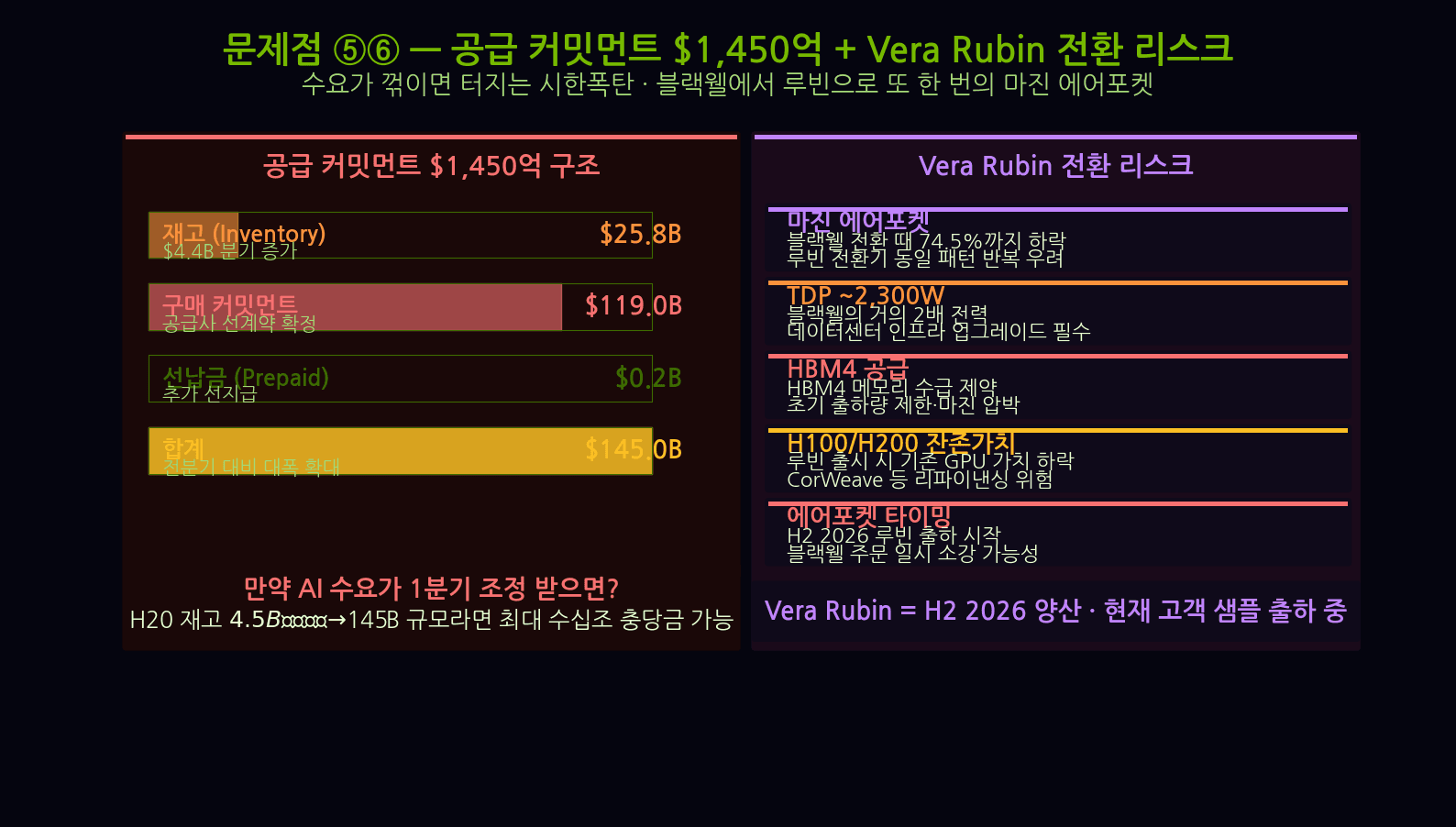

Problem ③: The $145B Supply Commitment — A Double-Edged Sword

Nvidia currently holds pre-committed production agreements totalling $145 billion with TSMC, SK Hynix, Samsung, and other supply chain partners. This is a strategic response to AI demand — but it is also enormous risk.

If hyperscalers collectively pull back on spending, if US export controls tighten further, or if a recession breaks the IT capex cycle, Nvidia could face catastrophic inventory losses. Think of this as the Data Center version of the 2022 gaming GPU inventory crisis — when Nvidia recorded a $1.32B inventory write-down. The scale of exposure is now orders of magnitude larger.

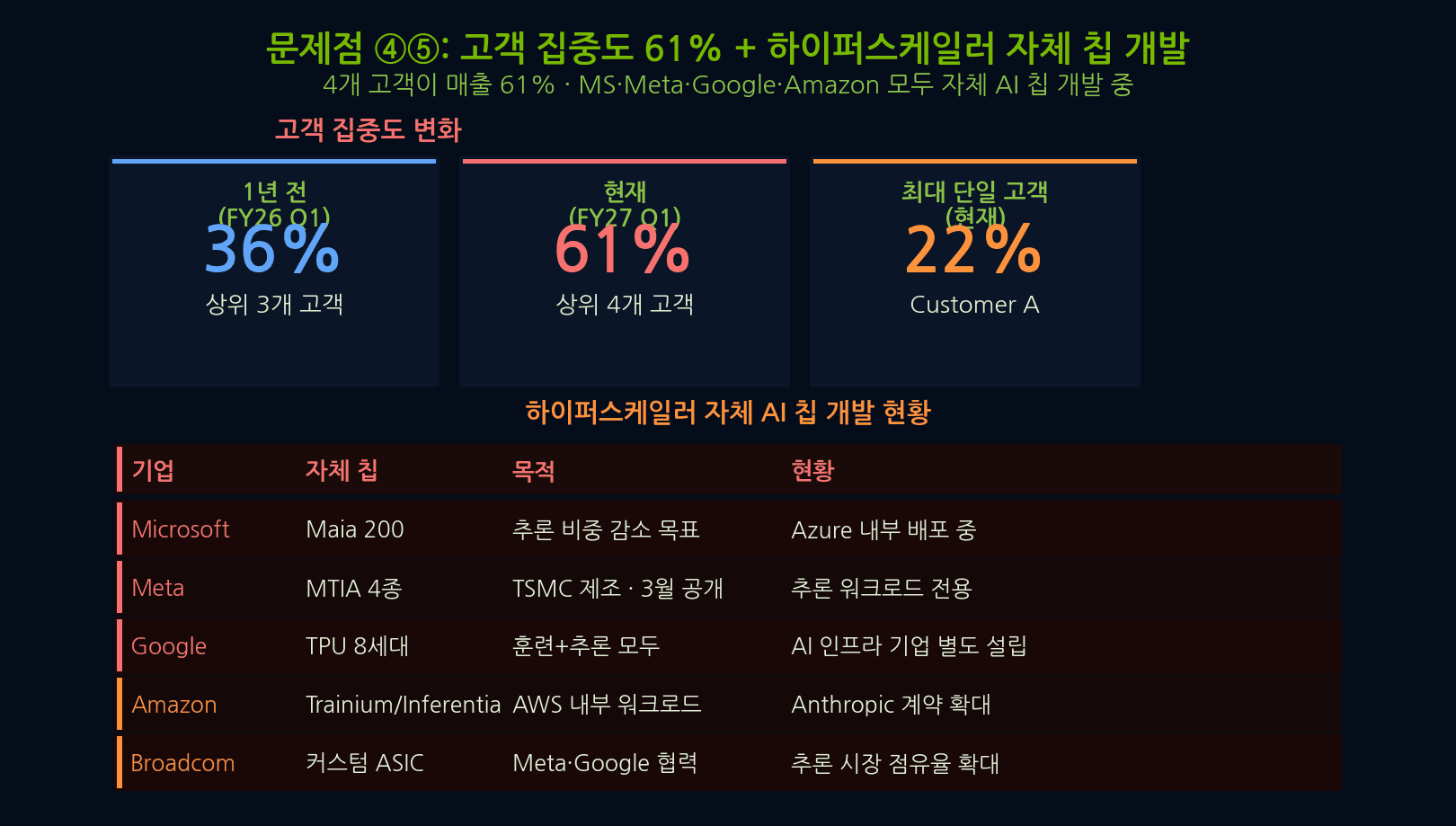

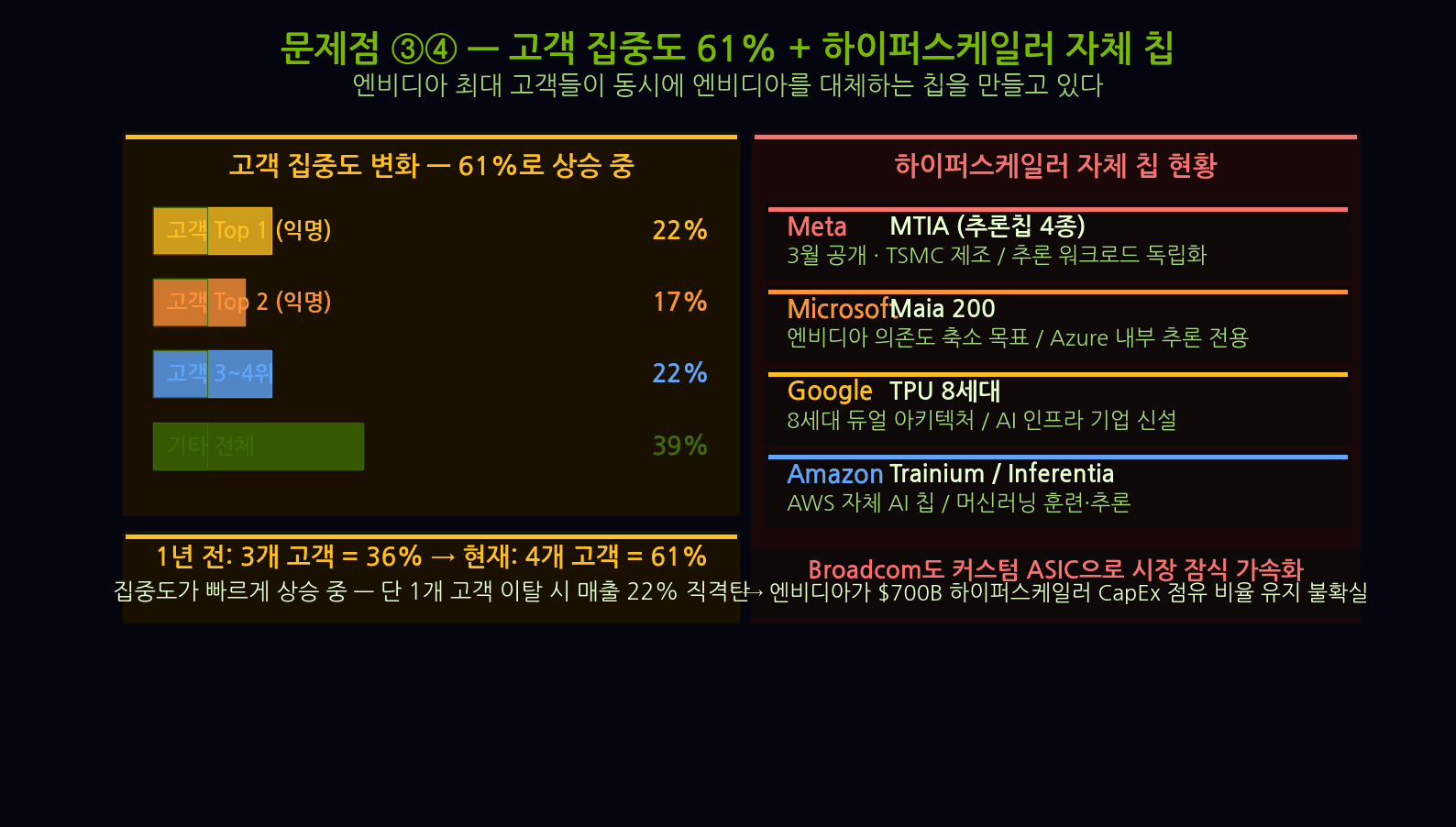

Problem ④: 61% Customer Concentration — Four Companies Hold the Keys

61% of Nvidia’s revenue originates from four hyperscalers: Microsoft, Google, Amazon, and Meta. That is up 9 percentage points from 52% a year ago — concentration is intensifying, not easing.

If even one of these four companies cuts its Nvidia GPU orders by 10%, Nvidia’s total revenue drops by roughly $5B. More worrying: all four are actively developing their own AI chips. The customer and the competitor are increasingly the same entity.

5. Problems ⑤⑥ — In-House Chip Threat and Vera Rubin Supply Risk

Problem ⑤: Big Tech Custom Chips — Customers Are Becoming Competitors

Google’s TPU v5p shows 1.7–2.1× better price-performance than the H100 on specific transformer inference workloads, according to published internal benchmarks. Amazon’s Trainium 2 is offered to AWS customers at 20–30% lower cost than equivalent H100 instances. Meta is targeting volume production of its third-generation MTIA chip within FY2027.

Nvidia’s CUDA moat remains formidable for training workloads. But in the inference market, custom chip share is forecast to grow from 15% in 2025 to 35% by 2027. Even if Nvidia retains training dominance, a partial loss of inference revenue would meaningfully dent its growth trajectory.

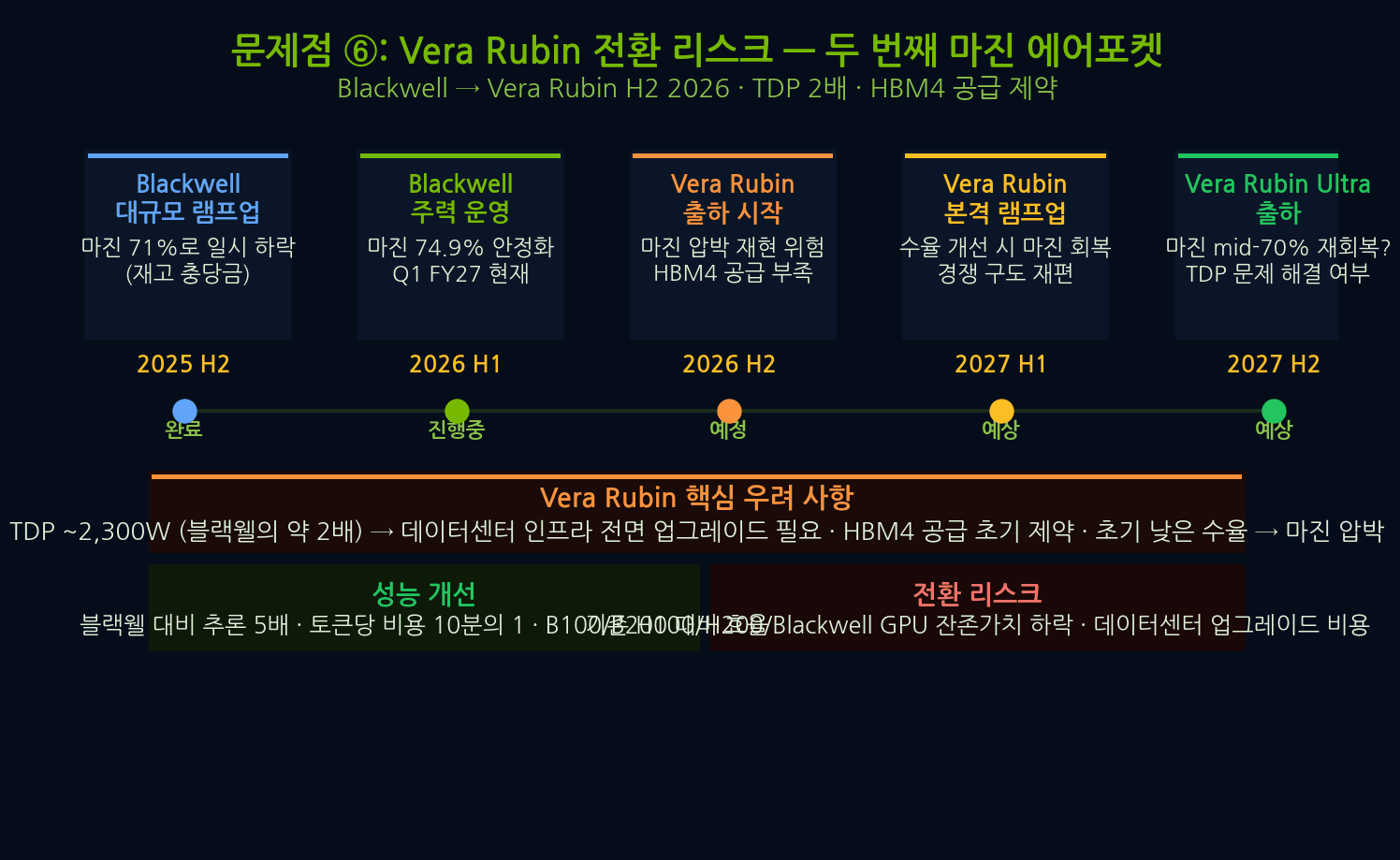

Problem ⑥: Vera Rubin — Innovation and Risk in the Same Package

The next-generation Vera Rubin architecture combines TSMC N2 (2nm-class) process, HBM4 memory, and NVLink Generation 6 — targeting 3–4× the performance of Blackwell. Nvidia has signaled initial volume shipments in H2 2026.

However, N2 process initial yields are estimated by industry sources at 30–40%. Combining CoWoS-L advanced packaging with N2 is an unprecedented engineering challenge. Supply delays could accelerate customer trials of AMD MI350X or Intel Gaudi 4. More critically, during the Vera Rubin ramp, gross margins are likely to be squeezed even harder than during the Blackwell ramp — a compression that could last two to three quarters.

6. Problems ⑦–⑩ — Circular Revenue, China, Inventory and Valuation

Problem ⑦: Circular Revenue Suspicion

Some analysts have raised the possibility of “revenue circularity” between Nvidia and its hyperscaler customers — a structure in which Nvidia purchases cloud services from customers who then use those funds to buy GPUs. Nvidia has denied the allegation, but the fact that the question surfaces repeatedly on conference calls is itself telling.

Problem ⑧: China Export Controls — A $15B Market Gone Dark

The US government’s H20 export ban cost Nvidia roughly $2–3B per quarter in Chinese revenue — an annualised loss of approximately $10–12B. Chinese buyers are rapidly migrating to Huawei Ascend 910C. Once substituted, winning those customers back is extremely difficult, and with domestic alternatives improving every generation, the window is narrowing.

Problem ⑨: GPU Inventory Overhang

Reports suggest certain cloud customers have already accumulated 6–9 months of H100/H200 inventory. As the Blackwell transition accelerates, used-market prices for legacy Hopper-architecture GPUs are under pressure. This could delay fresh procurement cycles — creating a temporary air pocket in demand even if end-user AI workloads continue growing.

Problem ⑩: 35× P/E — Is It Justified?

Nvidia currently trades at approximately 35× FY2027 estimated adjusted EPS. Even granting a premium for growth, sustaining this multiple requires EPS to compound at +35% or more annually over the next three years. When gross margin compression, growth deceleration, and custom chip threats are simultaneously priced in, a fair P/E range of 22–28× emerges from several valuation models.

At 28× P/E, reverse engineering from the multiple implies ~20% downside from the current share price. The most likely catalysts for that scenario: a Q2 miss, a guidance cut, or a hyperscaler capex reduction announcement.

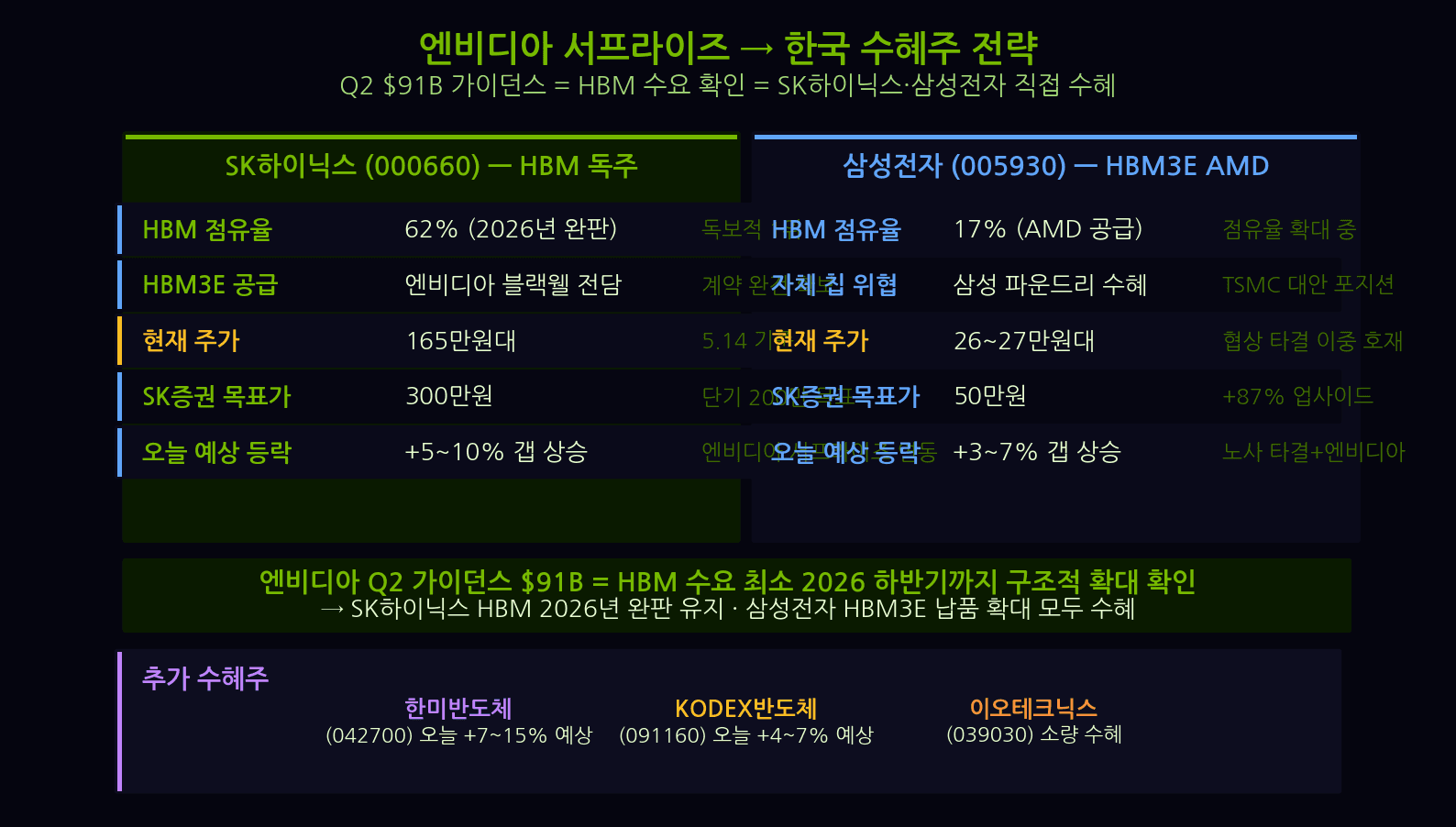

7. Korean Beneficiary Strategy — Positioning in SK Hynix and Samsung Electronics

The clearest Korean winner from Nvidia’s earnings is SK Hynix. HBM3e memory is effectively the sole supplier to Blackwell GPUs, and the company is well positioned to maintain that status into the HBM4 era. SK Hynix HBM shipments grew +150% YoY in Q1, while HBM average selling prices carry a 4–5× premium over standard DRAM. The economics are transformational.

The domestic brokerage consensus target price for SK Hynix sits in the KRW 2,000,000–2,400,000 range. If Nvidia’s Q2 guidance of $91B is realized, SK Hynix’s HBM volume commitment expands in lock-step. A staged buying strategy on any short-term corrections is compelling.

Samsung Electronics requires more patience. The company is working to re-enter Nvidia’s supply chain following HBM3e qualification, but analysts broadly expect another two to three quarters before volume ramp and yield stability are confirmed. That said, once re-entry is officially announced, a meaningful re-rating of the stock is likely — making a small starter position at current levels worth considering. Samsung’s HBM supply contribution, once confirmed, is estimated at an additional $800M–$1.2B per quarter in incremental revenue.

- SK Hynix: HBM3e exclusivity, HBM4 lead development, target KRW 2.0M–2.4M — core hold

- Samsung Electronics: Monitor HBM re-entry confirmation, small starter position — cautious accumulation

- Hanmi Semiconductor: Exclusive TC bonder equipment for HBM — indirect beneficiary worth watching

8. Conclusion — Five Investor Strategies and Stop-Loss Levels

In a quarter where a $81.6B surprise coexists with ten structural problems, individual investors need a disciplined framework — not euphoria and not panic. Five principles follow.

- Hold SK Hynix: The most direct and defensible Korean proxy for Nvidia upside. HBM exclusivity is valid through at least FY2028. Target price KRW 2.0M–2.4M.

- Accumulate Samsung Electronics in Three Tranches: Buy one-third at current price, one-third at -5%, one-third at -10% before HBM re-entry is confirmed. Avoid concentrating before the catalyst.

- Exercise Caution on Direct NVDA Purchases: A 35× P/E does not reconcile easily with decelerating growth. Existing holders should consider taking partial profits in the 20–25% gain range. New buyers should wait for margin evidence of stabilization.

- Set Hard Stop-Losses: For NVDA holders, a mechanical stop-loss of -15% from cost basis. For SK Hynix, reassess positioning if the stock falls below KRW 1,600,000.

- Monitor Q2 Earnings: The Q2 results expected in August 2026 are the most important checkpoint. The single most critical metric: gross margin recovery to 63%+. Also watch guidance credibility closely. A guidance cut warrants immediate position reassessment.

Nvidia remains the backbone of AI infrastructure. But investors who let the $81.6B headline cloud their judgment — and ignore the three fractures of margin stagnation, supply risk, and stretched valuation — are setting themselves up for painful surprises. Long-term returns belong to those who read the structure behind the headline.