Yen Depreciation Hits 1973 Low — ‘Weaker Than Turkish Lira’ 5 Causes and Outlook

Yen Depreciation Hits 1973 Low — ‘Weaker Than Turkish Lira’ 5 Causes and Outlook

Yen Depreciation hit a fresh all-time low in April 2026. On a real effective exchange rate (REER) basis, it is the weakest since the float regime began in 1973, and analysts have even suggested the yen is now “weaker than the Turkish lira“. As of May 27, USD/JPY trades around 160, roughly +52% depreciation vs the 105 level in 2020.

This article synthesizes Daum (5/27), BIS, Itochu Research Institute, MOF Japan, BOJ, and BOK data to cover the 5 causes of Yen Depreciation (trade deficit, US-Japan rate gap, expansionary fiscal, energy imports, BOJ policy limits), REER currency comparison, trade balance trajectory, Takaichi-administration fiscal impact, 5 channels of Korean economy impact, outlook with 3 scenarios, and 5 investment strategies. BIS REER statistics at BIS EER; BOJ at BOJ.

| Item | Value | Notes |

|---|---|---|

| REER | Lowest since 1973 | Since float regime began |

| 2026.05 USD/JPY | ~160 (est.) | vs 105 in 2020, +52% |

| Key Comparison | Weaker than Turkish lira (analyst view) | Takeda, Itochu Research |

| 2022 Trade Bal. | -20T JPY (record deficit) | Energy price shock |

| 2026E Trade Bal. | About -5T JPY concern | Middle East + oil |

| Political Variable | Takaichi Sanae expansionary fiscal | Yen credibility concern |

| Recovery Path | AI·wage·real-rate cycle | Years required / no near-term rebound |

01USD/JPY Trajectory — Long-Term Depreciation 2020~2026

USD/JPY moved from ~105 in 2020 to ~160 in May 2026 — a +52% long-term depreciation over 6 years. 138 in 2022, 145 in 2023, 152 in 2024, and 158~160 settled in 2025~2026. 150 was once a psychological resistance line, but that level has now become routine.

A rising USD/JPY means weaker yen, which triggers higher import prices + household burden + exporter profit boost simultaneously. Structurally, Japan’s trade balance hit a record deficit of -20T JPY in 2022 and has not turned to surplus, creating a vicious cycle where currency weakness becomes locked in as fundamental deterioration.

| Year | USD/JPY | vs 2020 | Key Event |

|---|---|---|---|

| 2020 | 105 | Baseline | COVID + safe-haven demand |

| 2021 | 115 | +10% | Fed starts hiking |

| 2022 | 138 | +31% | Record -20T JPY trade deficit |

| 2023 | 145 | +38% | US rates hit 5% |

| 2024 | 152 | +45% | BOJ ends negative rates |

| 2025 | 158 | +50% | Weakness entrenched |

| 2026.05 | 160 | +52% | 1973 low re-broken |

iINFO — Why 150 Is No Longer a Resistance

In 2020~2022, 150 was a psychological resistance, but since 2024 the 150s have become normal, no longer functioning as meaningful resistance. The market now treats 160 as the new baseline, with a potential breach of 170 being the next watch point.

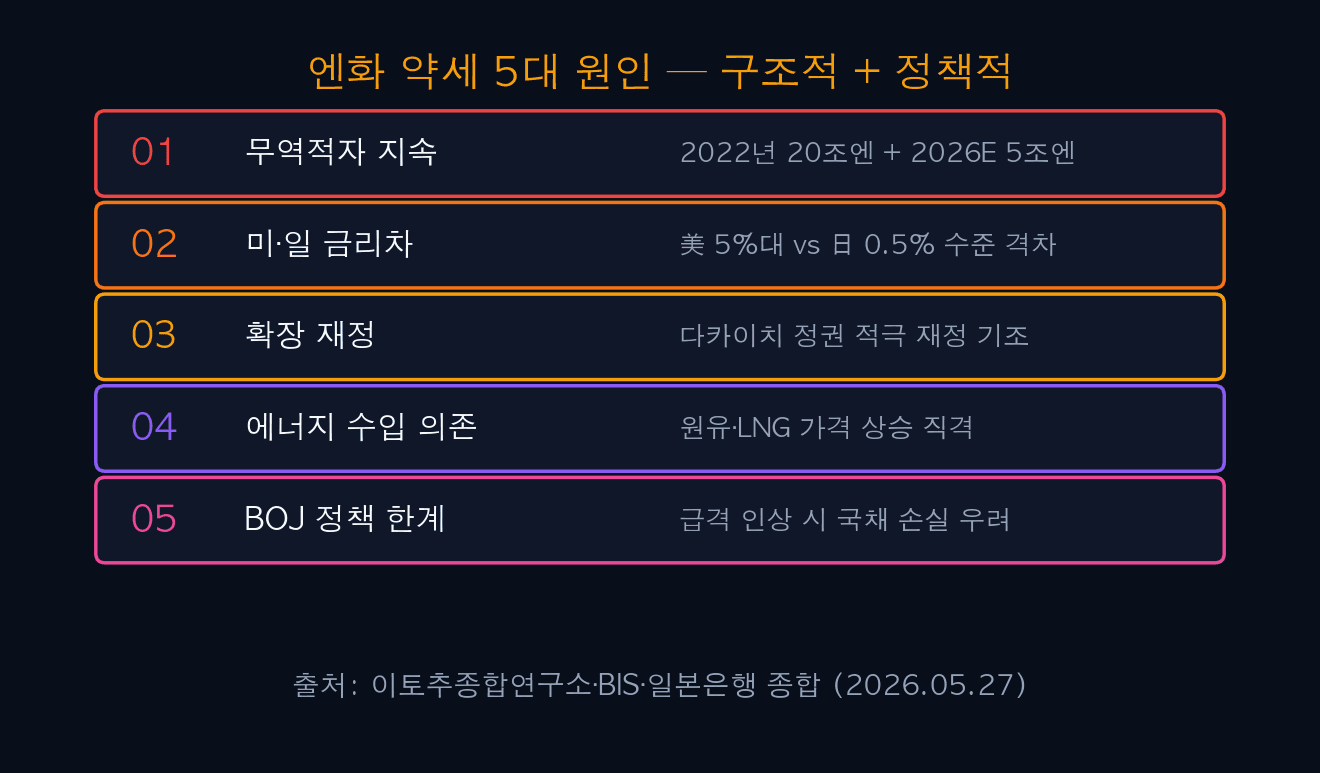

025 Causes of Yen Weakness — Structural + Policy

Yen weakness results from 5 compounding structural and policy factors, not a single driver. Persistent trade deficit, US-Japan rate gap, expansionary fiscal, energy import dependence, BOJ policy limits — these layer to cement the downtrend.

The US-Japan rate gap is the key short-term FX driver. With US policy rates around 5% vs Japan’s ~0.5%, carry trade flows (borrow low-yield yen to fund high-yield dollars) chronically pressure the yen lower. Since the Takaichi Sanae administration tilted toward expansionary fiscal, BOJ’s room to hike has further narrowed — a recently added factor.

| Cause | Core Content | Impact Strength |

|---|---|---|

| 1. Persistent Trade Deficit | 2022 -20T JPY + 2026E -5T JPY concern | Very Strong |

| 2. US-Japan Rate Gap | US 5% vs JP 0.5% — fuels carry trade | Very Strong |

| 3. Expansionary Fiscal | Takaichi active fiscal — credibility loss | Strong |

| 4. Energy Import Dependence | Oil·LNG price rises → trade deficit | Strong |

| 5. BOJ Policy Limits | Rapid hikes risk JGB losses | Moderate |

| 6. Safe-Haven Status Erosion | Traditional yen safe-haven appeal fading | Moderate |

03REER Comparison — Yen vs Major Currencies

Real Effective Exchange Rate (REER) adjusts nominal FX for inflation differentials weighted by trade. Per BIS data with 2020=100, Japan’s REER in 2026 is estimated at ~60 — lower than Turkish lira (65), Korean won (92), Chinese yuan (95), and US dollar (115).

This is the basis for the “weaker than the Turkish lira” framing. Despite Turkey’s double-digit inflation and fiscal instability, Japan’s REER falling below the lira’s signals structural yen undervaluation.

| Currency | 2026 REER (2020=100) | vs 2020 | Key Factor |

|---|---|---|---|

| Japanese Yen (JPY) | 60 | -40% | Trade deficit + rate gap + fiscal |

| Turkish Lira (TRY) | 65 | -35% | High inflation + fiscal instability |

| Korean Won (KRW) | 92 | -8% | Export slowdown + US rates |

| Chinese Yuan (CNY) | 95 | -5% | Property bust + deflation |

| US Dollar (USD) | 115 | +15% | High rates + safe-haven |

⚠ALERT — Meaning of Yen Below Turkish Lira

A yen REER below the Turkish lira signals structural undervaluation of the Japanese currency. It hints at rebound potential, but also that market is pricing severe fundamental deterioration. Investors should not read this purely as a “value opportunity”.

04Japan Trade Balance — Yen Weakness + Oil Shock

Japan’s trade balance went from +1T JPY surplus in 2018 to a record -20T JPY deficit in 2022. It narrowed to -9T in 2023 and -5T in 2024, but as 2026 unfolds, Middle East tensions + rising oil prices are reigniting concerns of a -5T JPY deficit recurrence.

The core issue is Japan’s heavy dependence on imported energy and raw materials. Higher oil, LNG, and food prices feed directly into trade deficits, and yen weakness amplifies the burden. Exporters (Toyota, Sony) gain from a weak yen, while households and SMEs suffer from rising import inflation — bipolar structure deepening.

| Year | Trade Balance (T JPY) | Key Driver | Notes |

|---|---|---|---|

| 2018 | +1 | Strong exports | Last surplus |

| 2019 | -1.6 | US-China trade war | Mild deficit |

| 2020 | +0.4 | COVID import drop | Temporary surplus |

| 2021 | -1.6 | Commodity recovery | Back to deficit |

| 2022 | -20 | Yen + oil shock | Record deficit |

| 2023 | -9 | Oil stabilizes + export rebound | Narrowing |

| 2024 | -5 | Yen weakness drag | Improving |

| 2025 | -3 | Solid exports + stable oil | Recovering |

| 2026E | -5 | Middle East + oil rise | Re-widening concern |

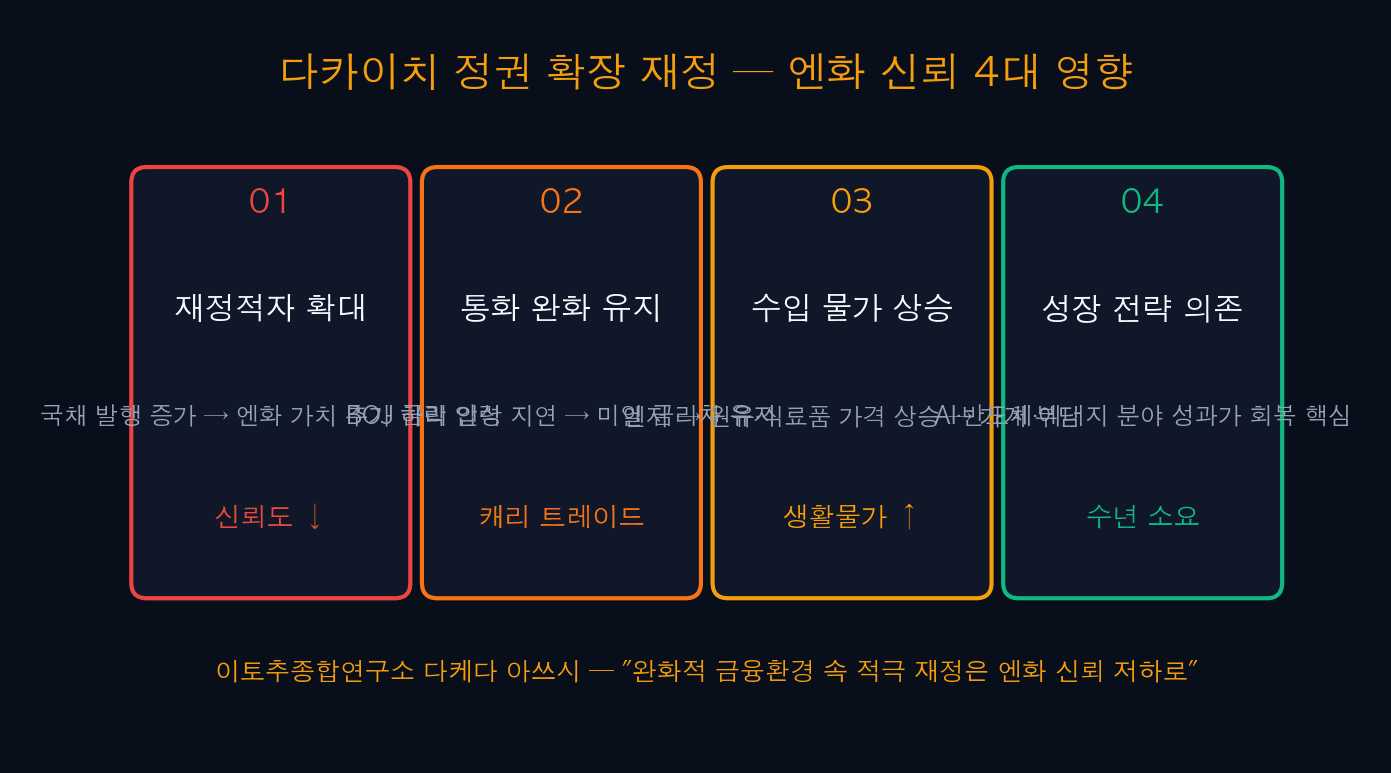

05Takaichi Fiscal Expansion — 4 Yen Credibility Impacts

Since the Takaichi Sanae administration took office, fiscal expansion has intensified. Short-term, this supports growth, but the chain more JGB issuance → wider fiscal deficit → loss of yen credibility → additional FX downside is widely flagged.

Takeda Atsushi, chief economist at Itochu Research Institute, warned that “active fiscal policy under accommodative monetary conditions can lead to a loss of yen credibility“. With BOJ maintaining easy money while the government adds fiscal stimulus, the US-Japan rate gap widens and yen selling pressure intensifies. Without success from AI, semiconductor, and energy growth strategies, this loop may persist for years.

| Impact | Mechanism | Yen Effect |

|---|---|---|

| 1. Fiscal Deficit | JGB issuance up → credit down | Additional weakness |

| 2. Easy Money Stays | BOJ delays hikes → US-Japan gap holds | Carry trade accelerates |

| 3. Import Inflation | Yen weakness → oil·food prices up | Household burden up |

| 4. Growth Dependence | AI·chip·energy results are key | Years required |

| Reference | Takeda warning | Itochu Research (2026.05) |

!WARNING — Two Sides of Expansionary Fiscal

Expansionary fiscal short-term boosts growth but erodes long-term currency credibility. In a country like Japan where gross debt/GDP is over 250% — world’s highest — additional fiscal expansion can quickly transmit via “JGB market → currency credibility → FX rate” channel.

06Korea Economy Impact — 5 Channels

Yen weakness has multi-layered effects on Korea. Export competitiveness erosion, tourism deficit, KRW/JPY drop, foreign flow volatility in equities, Japan ETF demand growth. Korean exporters directly competing with Japanese companies (autos, steel, semis) accumulate pricing disadvantage.

In tourism, Koreans surging to Japan + fewer Japanese visiting Korea simultaneously widens the deficit. KRW/JPY has slid from ~9.0 to ~8.5 KRW per JPY, favorable for travel·shopping·Japan stocks but a burden for Korean exporters and tourism-dependent businesses.

| Channel | Concrete Impact | Beneficiary/Loser |

|---|---|---|

| 1. Export Comp. | Auto·steel·semi vs Japan | Korean exporters lose |

| 2. Tourism Balance | More to Japan + fewer to Korea | Tourism deficit |

| 3. KRW/JPY | ~9.0 → ~8.5 KRW per JPY | Travel·shopping benefit |

| 4. Foreign Flows | Carry trade swings → KOSPI flow | Flow instability |

| 5. Japan ETFs | Korean investor Japan ETF demand grows | Investment opportunity |

iINFO — Meaning of KRW/JPY 9.0 → 8.5

KRW/JPY moving from 9.0 to 8.5 means the won has strengthened ~6% vs yen. Favorable for Japan travel·shopping·stock investing, but a burden for Korean businesses serving Japanese tourists or exporting to Japan. Investors can consider phased FX conversion strategies using this shift.

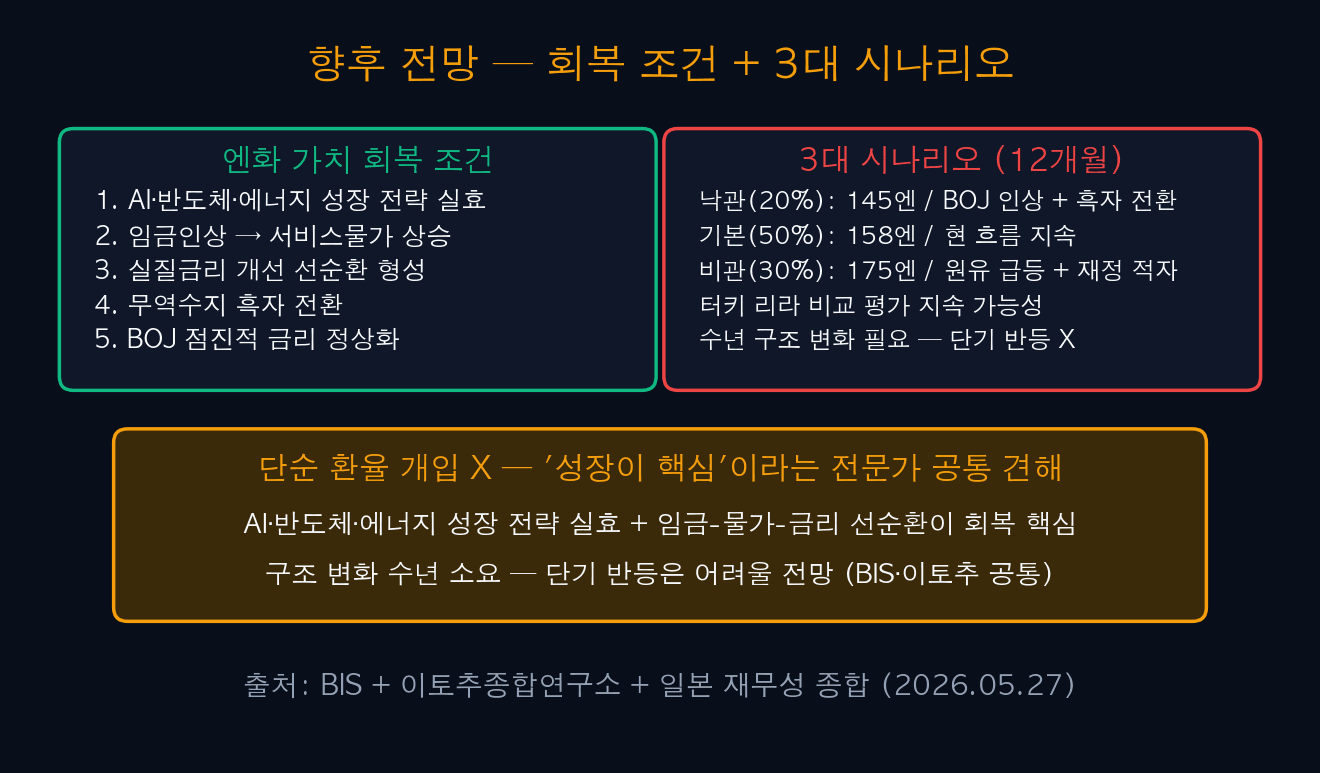

07Outlook — Recovery Conditions + 3 Scenarios

Yen recovery cannot come from FX intervention alone. Experts emphasize effective AI·semiconductor·energy growth strategies + wage rises → service inflation → real-rate improvement virtuous cycle. Structural change requires years, and near-term rebound is unlikely — BIS and Itochu shared view.

12-month scenarios split 3 ways. Bull (20%): 145 — BOJ hikes + trade surplus. Base (50%): 158 — current trajectory continues. Bear (30%): 175 — oil spike + fiscal deficit + BOJ limits. With 30% bear probability significant, FX hedging tools are recommended.

| Scenario | 12M USD/JPY | Conditions | Probability |

|---|---|---|---|

| Bull | 145 | BOJ hike + trade surplus | 20% |

| Base | 158 | Current trend + gradual normalization | 50% |

| Bear | 175 | Oil spike + fiscal deficit + BOJ limits | 30% |

✓TIP — 5 Recovery Condition Checklist

Yen recovery signals to watch: (1) AI·semi·energy growth strategies deliver (2) wages rise → service inflation up (3) real-rate improvement cycle (4) trade balance turns positive (5) BOJ gradual normalization. When 3+ of these emerge simultaneously, seriously consider trend reversal.

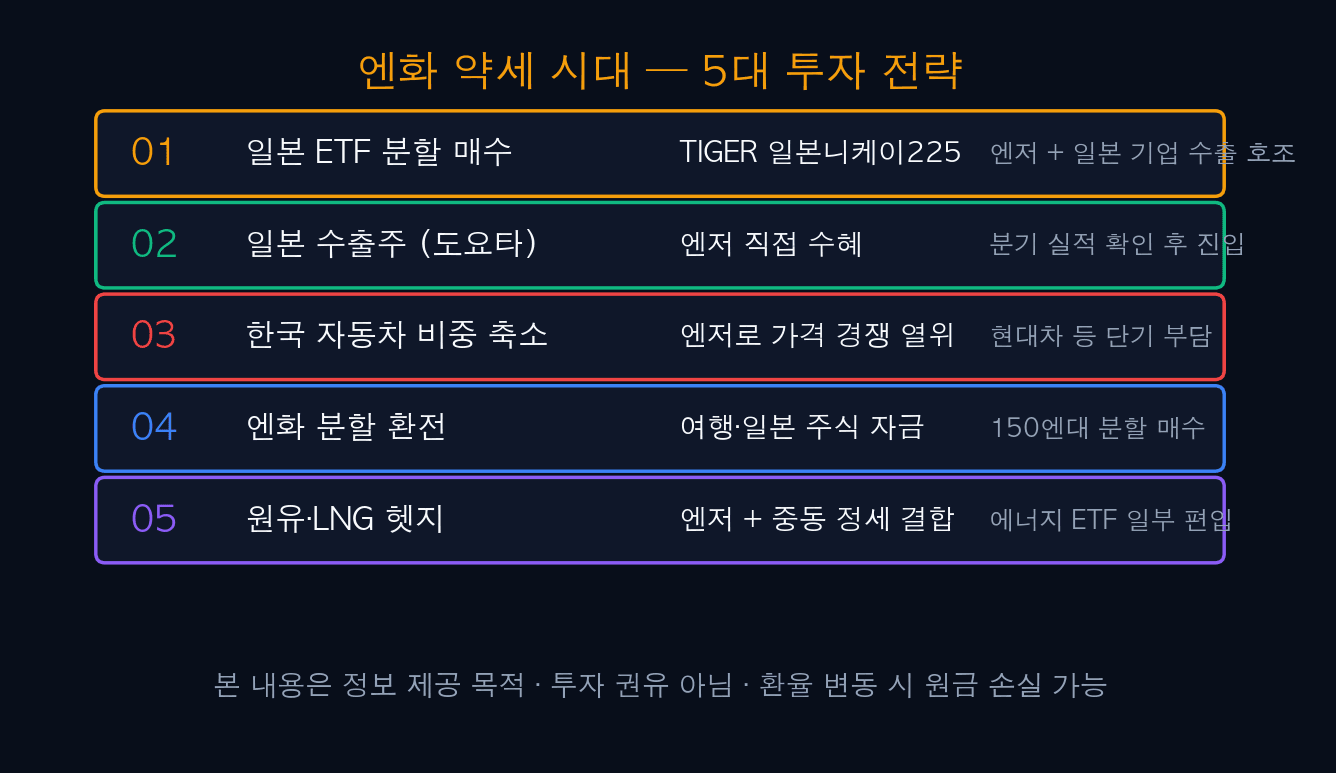

08Yen Weakness Era — 5 Investment Strategies

Five usable strategies in the yen weakness era: phased Japan ETF buying + Japan exporter stocks + reduce Korean autos + phased yen conversion + oil·LNG hedge. All require phased entry and pre-set stop-losses.

| Strategy | Ticker/Target | Allocation | Rule |

|---|---|---|---|

| S1: Japan ETF | TIGER Japan Nikkei 225 | 5% | -12% stop |

| S2: Japan Exporter | Toyota·Sony | 3% | Quarterly earnings |

| S3: Korean Autos | Hyundai·Kia reduce | Reduce | Until yen stabilizes |

| S4: Yen Conversion | KRW/JPY 8.5 phased | Spare | Long-term hold |

| S5: Oil Hedge | KODEX WTI Crude Futures | 2~3% | Oil -15% stop |

- Status: REER weakest since 1973 float regime

- USD/JPY: ~160 (2026.05) · +52% vs 105 in 2020

- Comparison: Weaker than Turkish lira (BIS REER)

- Causes: Trade deficit + US-Japan rate gap + expansionary fiscal + energy + BOJ limits

- Trade Deficit: 2022 -20T JPY record · 2026E -5T JPY concern

- Political: Takaichi expansionary fiscal → yen credibility loss

- Korea Impact: Export loss + tourism deficit + KRW/JPY 8.5

- 12M Scenarios: Bull 145 (20%) · Base 158 (50%) · Bear 175 (30%)

- Recovery: AI·wage·real-rate cycle (years required)

🔗 [This] Yen Depreciation Hits 1973 Low — ‘Weaker Than Turkish Lira’ 5 Causes Outlook

🔗 [Related] MakinaRocks 477850 Stock Outlook 5/27 — Post-Quadruple Korea Palantir 5 Scenarios

🔗 [Related] Samjeonix Leverage ETF May 27 Launch — 18 Products + 5 Strategies

🔗 [Related] Leverage ETF Pre-Education 30 min Free 5 Steps

🔗 [Related] US-Iran Negotiations Imminent — Oil·Tech 5 Scenarios

🔗 [Next] BOJ June Rate Decision D-Day Scenarios (Planned)

#Yen

#YenDepreciation

#YenWeakness

#USDJPY

#YenOutlook

#JPY

#REER

#BISStatistics

#TurkishLiraComparison

#JapanTradeDeficit

#TakaichiAdministration

#ExpansionaryFiscal

#ItochuResearch

#BOJ

#USJapanRateGap

#CarryTrade

#JapanTravelFX

#JapanStocks

#TIGERJapanNikkei225

#ToyotaStock

#HyundaiYenWeakness

#YenConversionStrategy

#KRWJPY

#KoreaImpact

#getdirRealTime

#getdirYen

#jyfamilyoffice

#2026YenOutlook

#JapanEconomy

#BOJPolicy