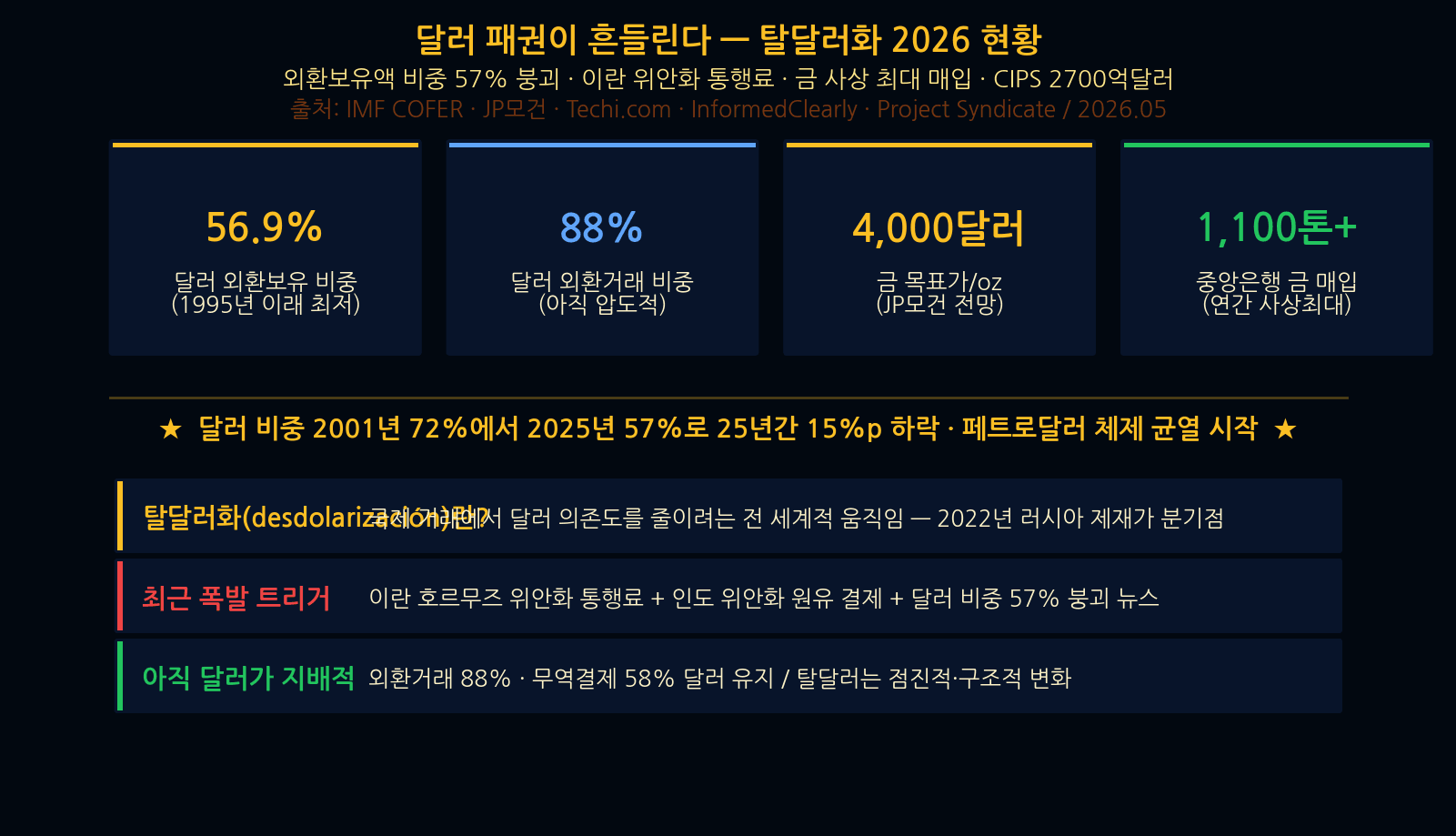

Dollar Hegemony Cracks — De-dollarization Drives IMF Reserve Share Below 57%

Economic Insights · May 23, 2026

Dollar Hegemony Cracks — De-dollarization Drives IMF Reserve Share Below 57%

Iran Yuan Tolls · BRICS Settlement Networks · Gold at $4,000 · 5 Investment Strategies

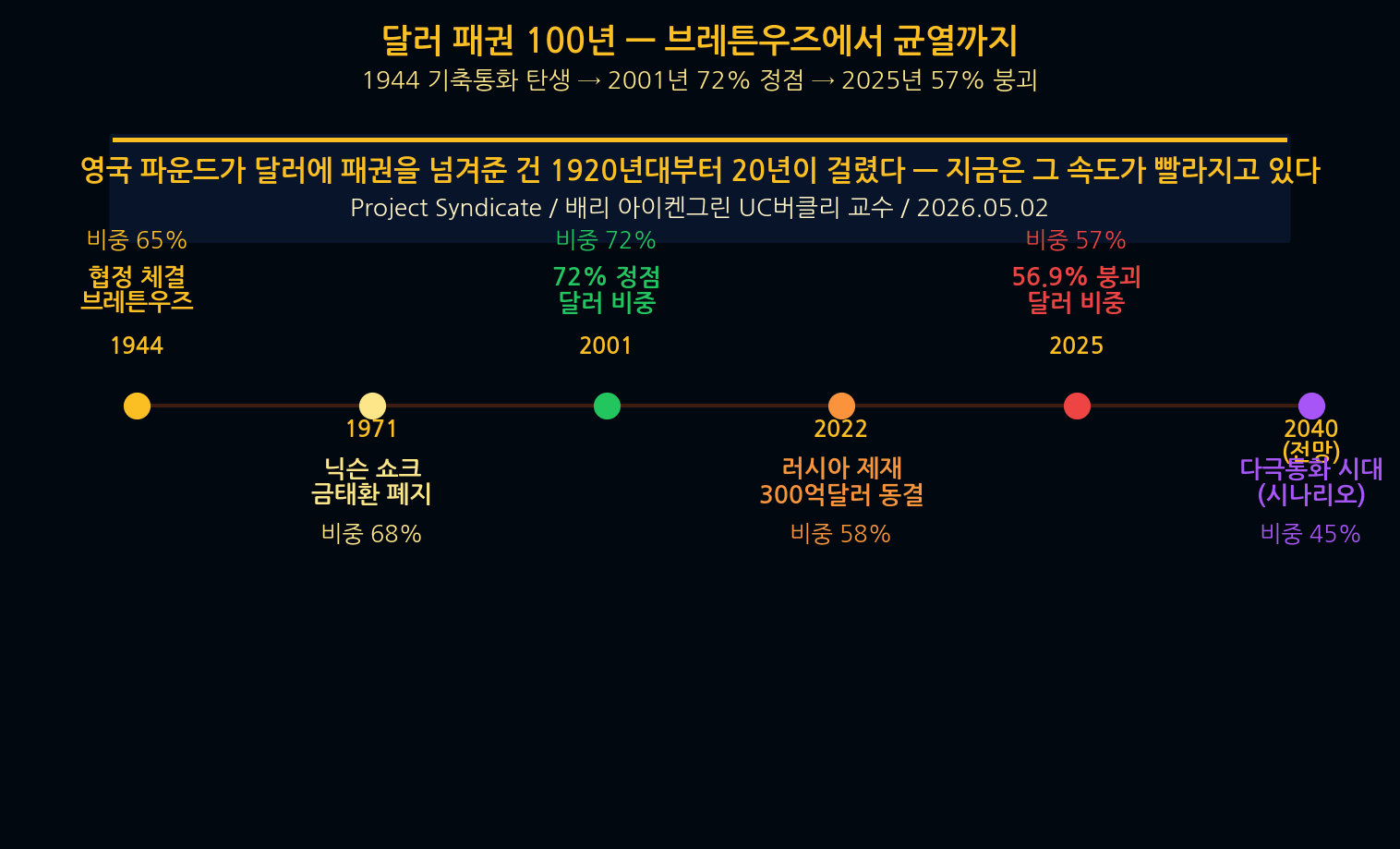

100 Years of Dollar Hegemony — How De-dollarization Began

The starting point of de-dollarization traces back to 1944’s Bretton Woods Agreement. Immediately after WWII, the United States — holding 75% of the world’s gold — pegged the dollar to gold to establish it as the global reserve currency. Even after Nixon abandoned the gold standard in 1971, the dollar maintained dominance through the petrodollar system (oil priced and settled in USD). The dollar peaked at 72% of global reserves in 2001. The real inflection point for de-dollarization was 2022: the freezing of $30B of Russia’s foreign reserves, which fundamentally rewired risk calculus at central banks worldwide.

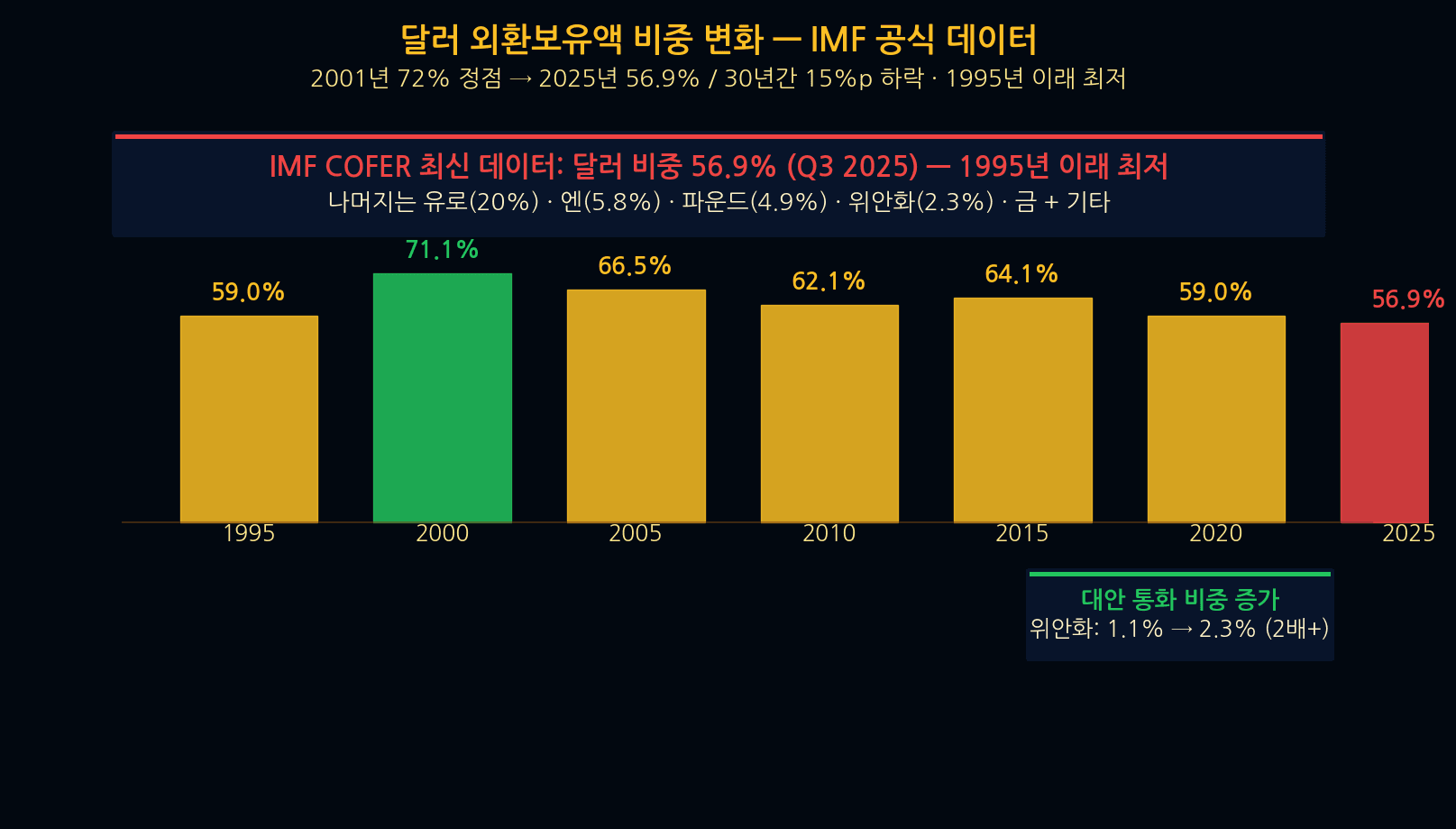

IMF Official Data — Dollar Share Falls Below 57%

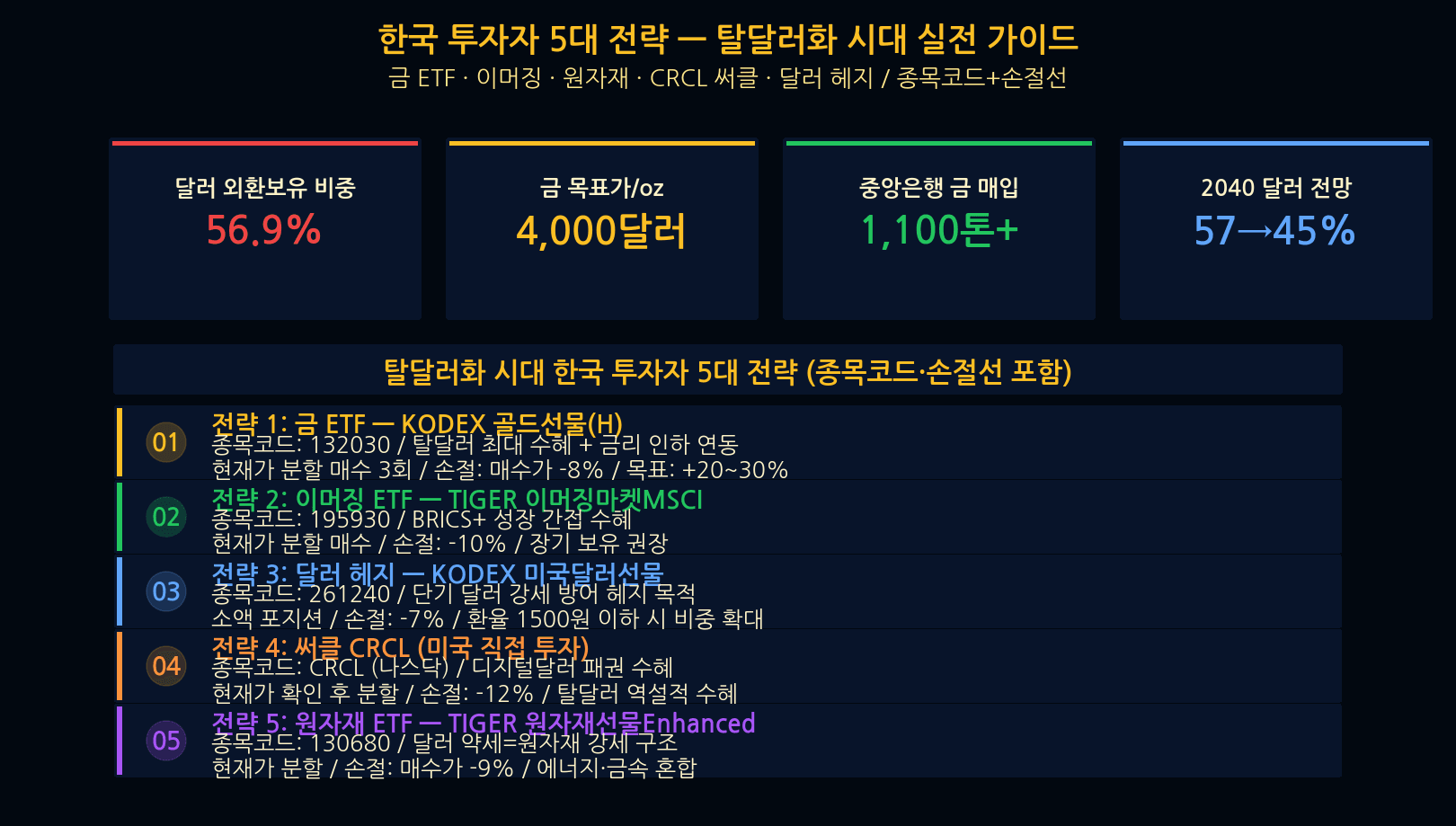

IMF COFER official data shows the dollar’s global reserve share at 56.9% — the lowest since 1995. From a peak of 72% in 2001, the dollar has lost 15 percentage points over 25 years. The 2016→2025 trajectory: USD 65.3% → 56.9% (-8.4pp), Euro 19.1% → 20.0%, Gold 9% (EM) → 14% (India), Yuan 1.1% → 2.3% (more than doubled). However, the dollar still accounts for 88% of global FX trading and 58% of international trade settlement — de-dollarization is gradual structural change, not collapse.

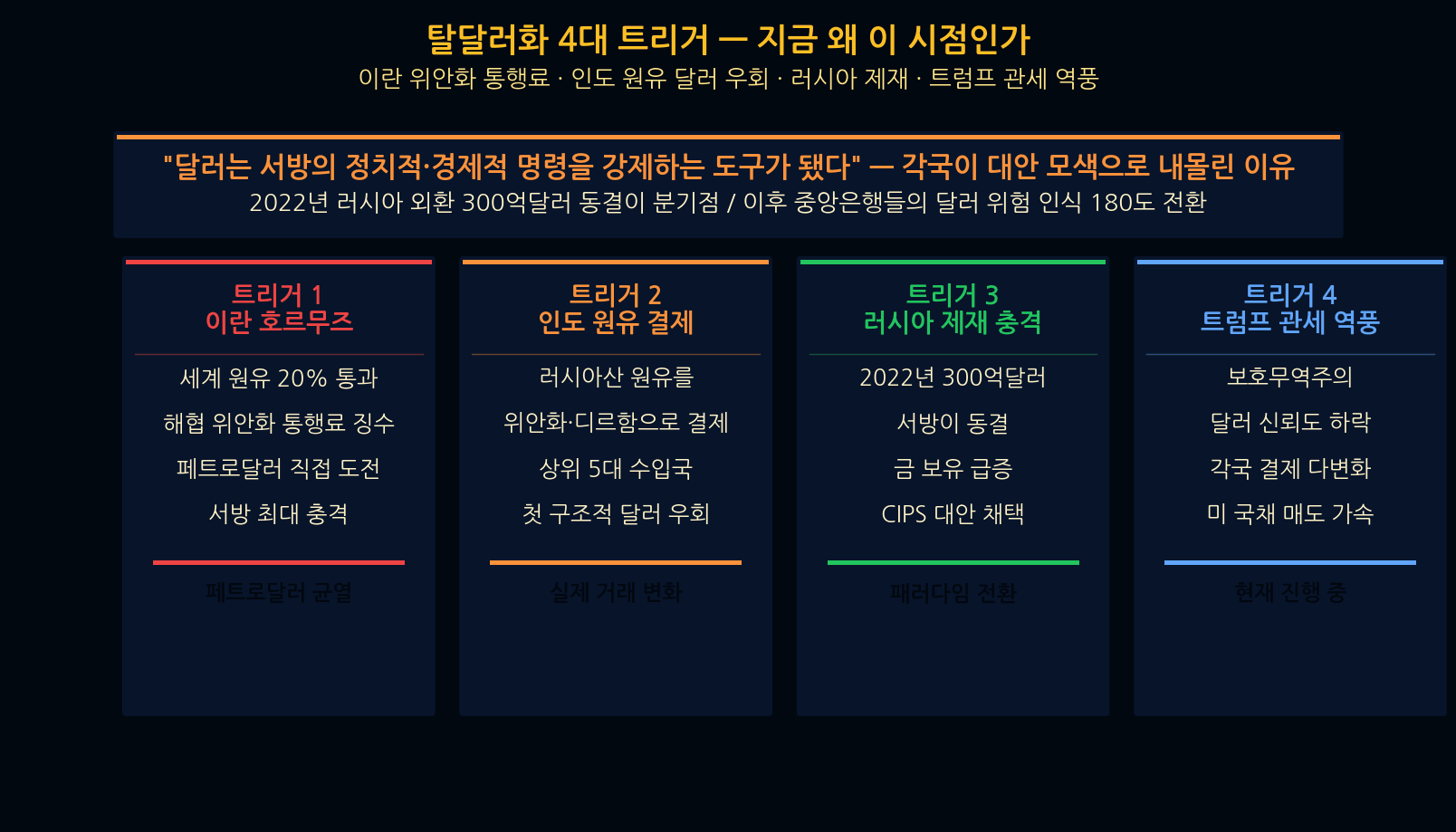

4 Triggers of De-dollarization — Why Now?

Four catalysts accelerating de-dollarization right now: ① Iran’s yuan tolls in the Strait of Hormuz — 20% of global crude transits this strait, and Iran now collects passage fees in yuan, a direct challenge to petrodollar architecture. ② India bypasses the dollar — Russian crude purchases settled in yuan and dirham; structural shift among the top 5 oil importers. ③ Russia FX freeze shock — the $30B 2022 freeze made central banks viscerally aware of dollar weaponization. ④ Trump tariff backlash — eroding dollar trust accelerates BRICS settlement adoption.

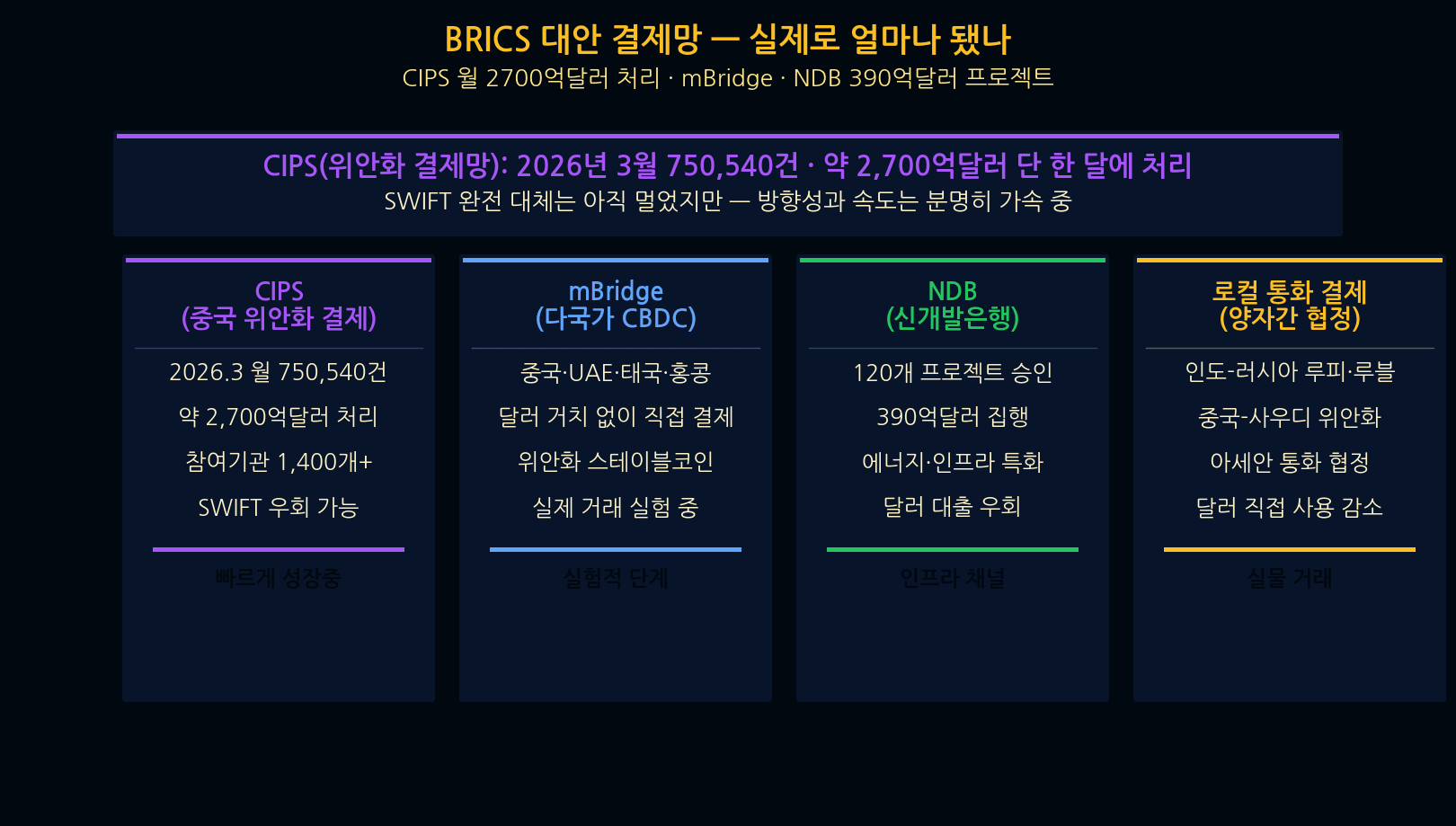

BRICS Alternative Payment Networks — How Real Are They?

The state of BRICS alternative payment infrastructure: CIPS (China’s yuan settlement network) has grown to $270B monthly, enabling partial SWIFT bypass. mBridge (China-UAE-Thailand CBDC) is still experimental but actively tested. NDB (New Development Bank) has approved $39B in loans. Multiple bilateral local-currency agreements exist (India-Russia, etc.). However, SWIFT still processes trillions daily — BRICS alternatives are supplementary, not replacements, for the foreseeable future.

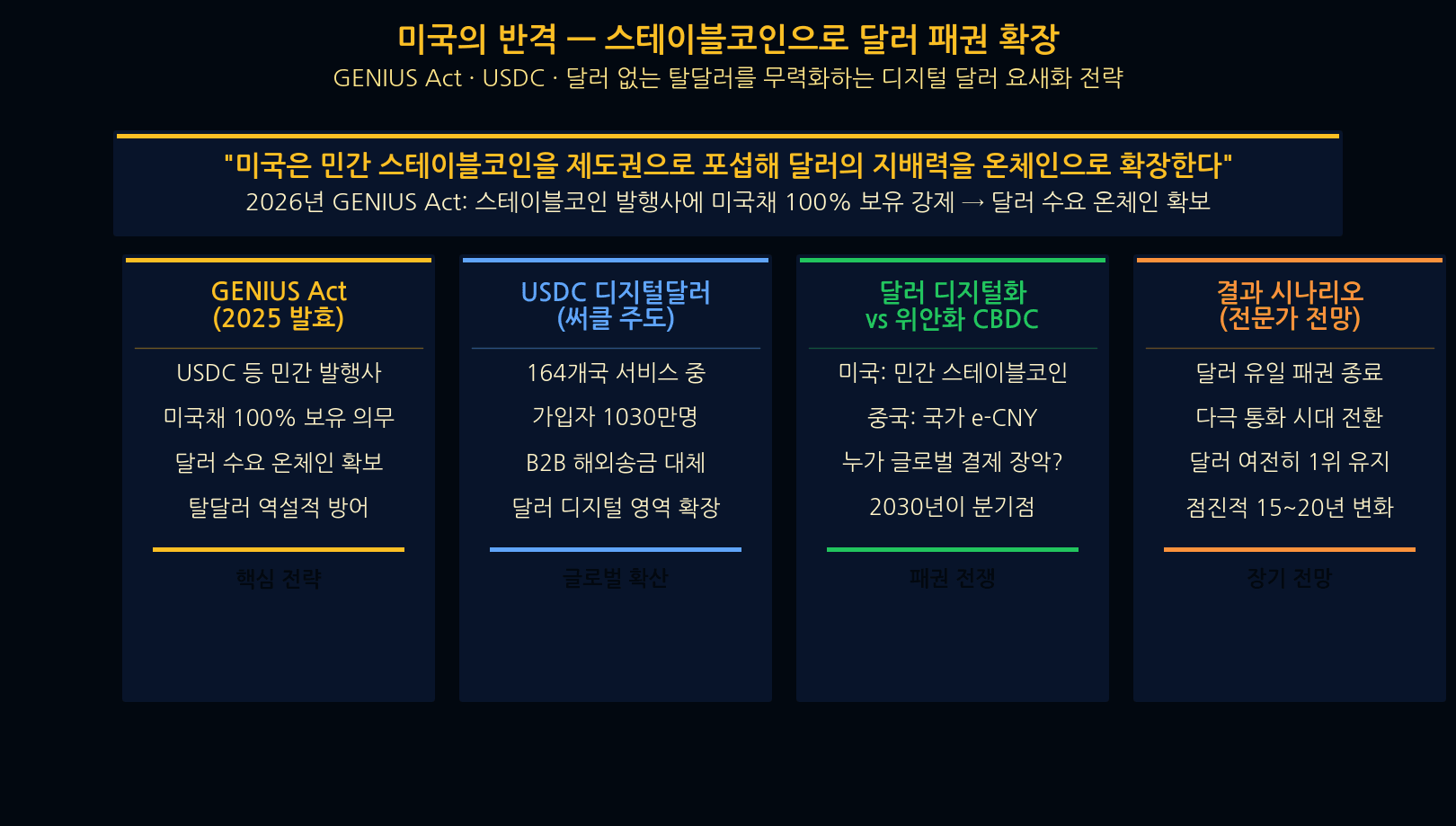

America’s Counter — Fortifying the Digital Dollar via Stablecoins

The US has not been passive. The GENIUS Act (effective 2025) mandates 100% US Treasury backing for stablecoin issuers like USDC. As stablecoins spread globally, Treasury demand grows automatically — a brilliant counter to “dollarless de-dollarization” by deploying the digital dollar. China responds with the e-CNY central bank digital currency, building direct yuan settlement networks that bypass SWIFT. Experts view 2030 as the first inflection point in this digital currency war.

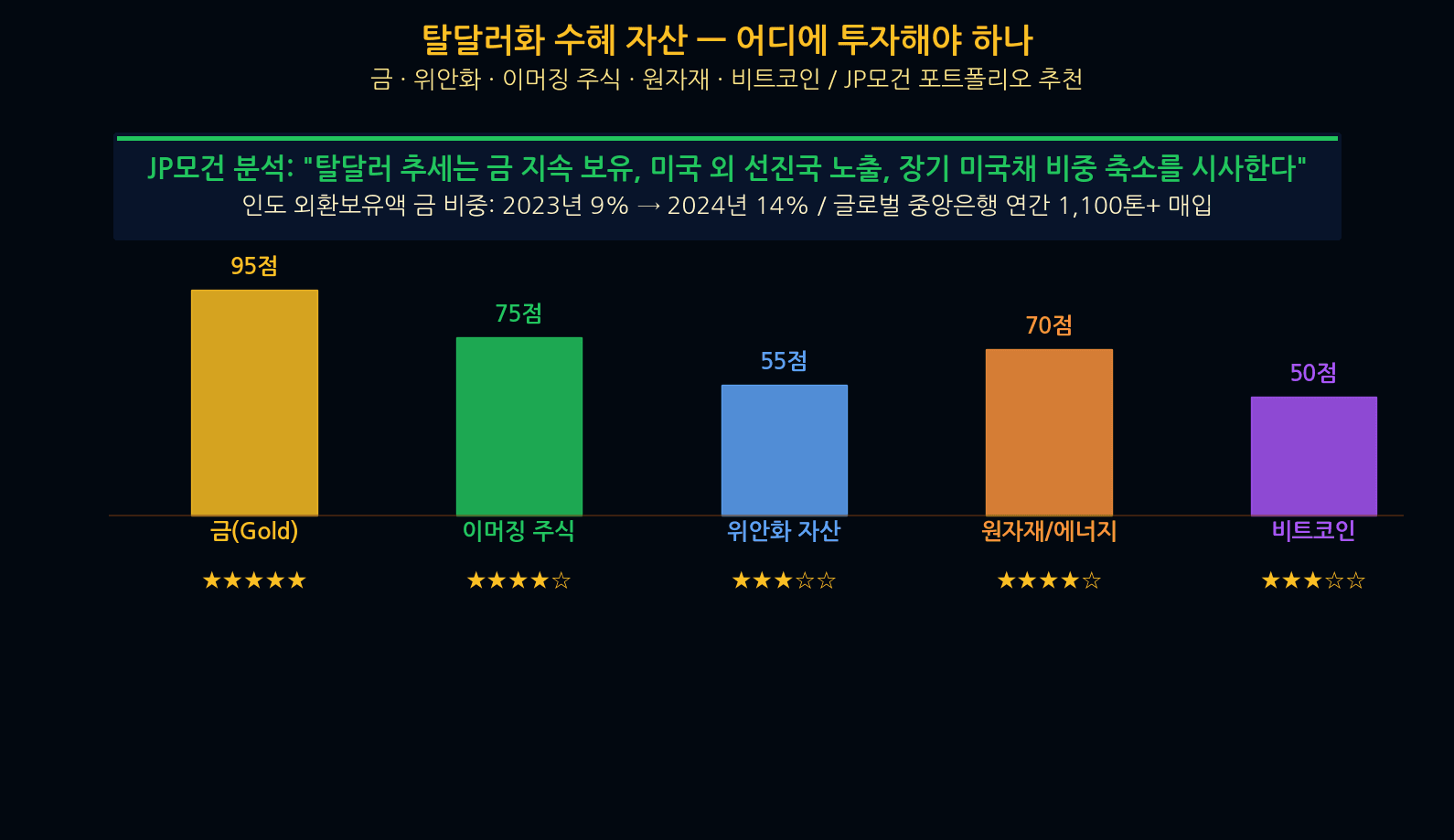

De-dollarization Beneficiary Assets — Gold, EM, Commodities

Assets positioned to benefit from de-dollarization: ① Gold — central banks buying 1,100+ tons/year, JP Morgan targets $4,000/oz. ② Emerging market equities — dollar weakness plus low valuations, ex-US developed market exposure recommended. ③ Commodities and energy — dollar weakness = commodity strength across crude, metals, agricultural products. ④ Yuan assets — gradual increase as yuan internationalizes. ⑤ Bitcoin — alternative hedge against the dollar system, but high volatility. Long-dated US Treasuries face pressure under de-dollarization and warrant reduced allocation.

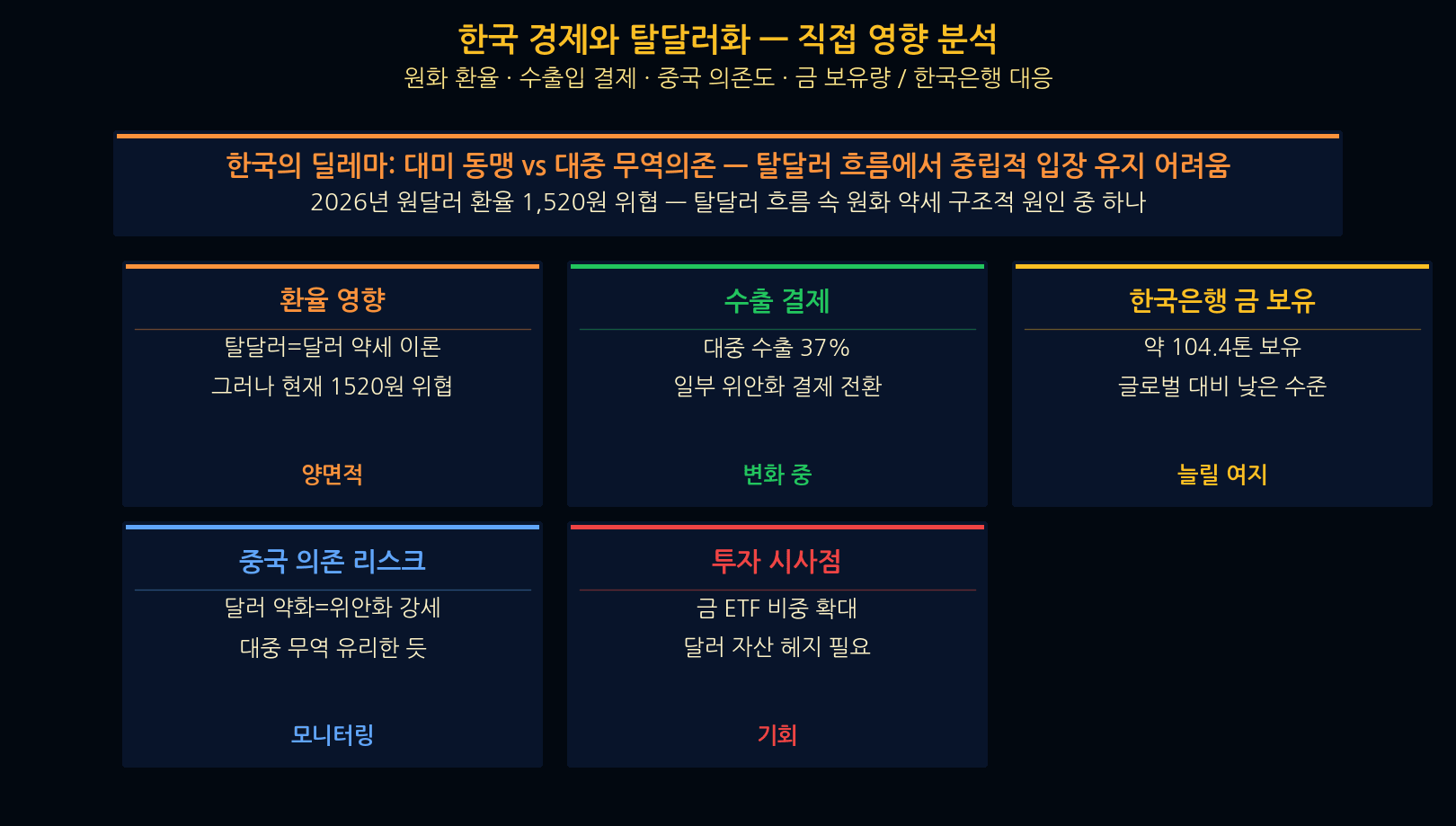

Impact on Korea — KRW, Exports, and Imports

The exchange rate paradox: theoretically de-dollarization = weak dollar = strong won, but reality is the opposite. With no immediate dollar alternative, uncertainty drives safe-haven dollar demand higher, pushing USD/KRW above 1,520. Korea’s exports to China (37% of total) are seeing partial yuan settlement transition. The Bank of Korea holds 104.4 tons of gold (3.4% of reserves) with ample room to expand. With 90% Middle East crude dependency, pressure to diversify settlement currencies is mounting. De-dollarization does not mean near-term won strength — that’s the critical insight.

5 Strategies for Korean Investors — De-dollarization Era

Five actionable strategies for the de-dollarization era: ① KODEX Gold Futures (132030) — three split entries at current price, stop-loss -8%, 15% weight. ② TIGER Emerging Markets MSCI (195930) — split entries, stop-loss -10%, 10% weight. ③ KODEX USD Futures (261240) — buy when USD/KRW dips below 1,500, stop-loss -7%, 8% weight. ④ Circle (CRCL, US) — confirmed price then split entry, stop-loss -12%, 5% weight. ⑤ TIGER Commodities Futures Enhanced (130680) — split entries, stop-loss -9%, 8% weight.

Conclusion — The Answer to De-dollarization Is Diversification

De-dollarization does not mean the immediate death of the dollar. But anyone holding only dollars is at risk. Final checklist: ① Consider Gold ETF (132030) at 15%+ portfolio weight ② Diversify with EM ETF (195930) — Asia and BRICS indirect exposure ③ USD hedge ETF (261240) for exchange rate risk defense ④ Circle CRCL — digital dollar hegemony winner (paradoxical de-dollarization beneficiary) ⑤ Reduce US long Treasury allocation (per JP Morgan) ⑥ Resist short-term dollar strength illusion — structural change unfolds on a 10–20 year horizon.

Sources: IMF COFER JP Morgan Project Syndicate