Samsung Margin Debt Tops 4 Trillion KRW — Second Liquidation Wave Warning

Real-Time Issue · May 23, 2026

Samsung Margin Debt Tops 4 Trillion KRW — Second Liquidation Wave Warning

Total credit balance hits record 36.5T / 1st wave of 305B liquidated / Survival guide

Samsung Margin Debt Crosses 4 Trillion KRW — What Happened

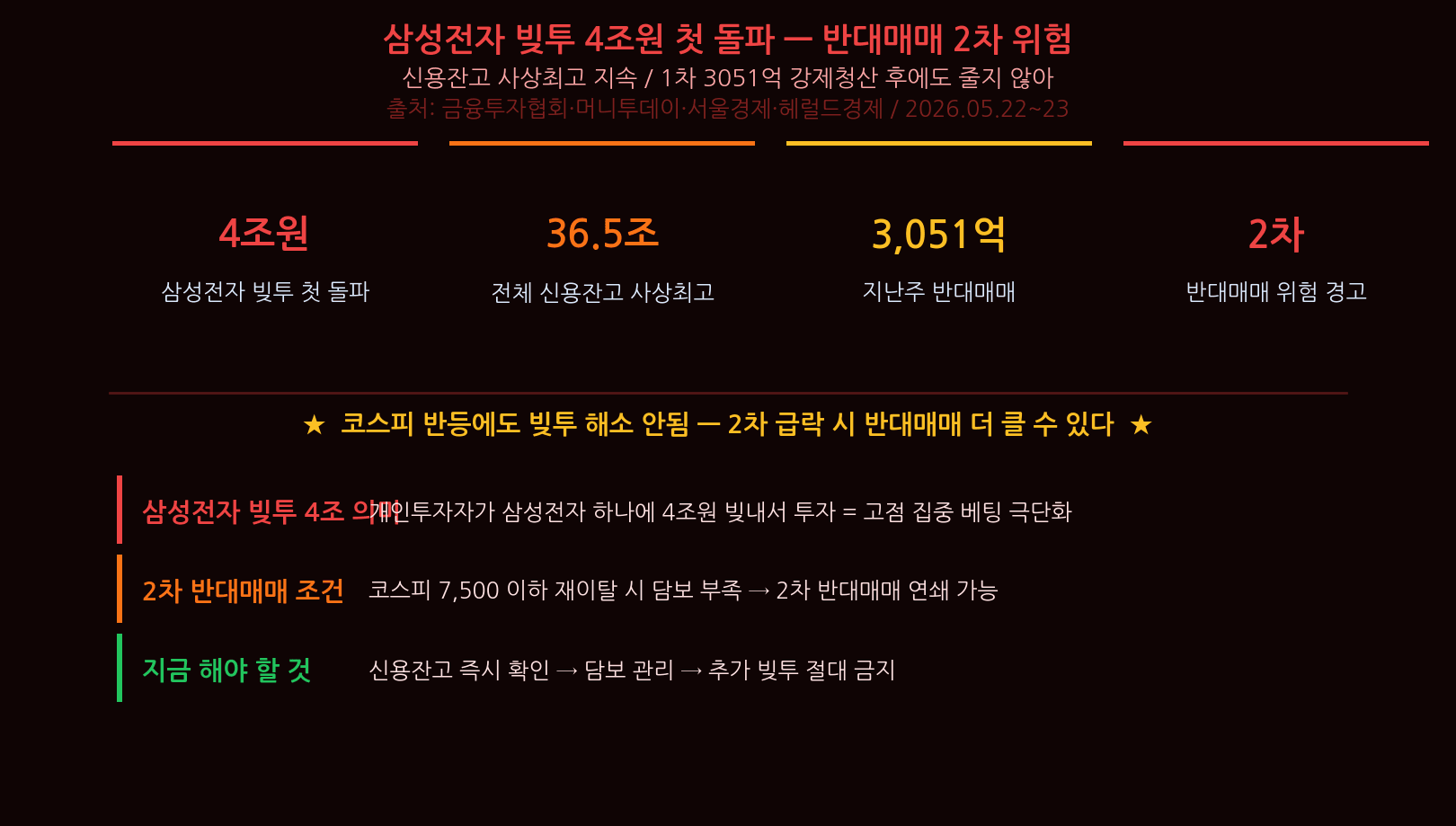

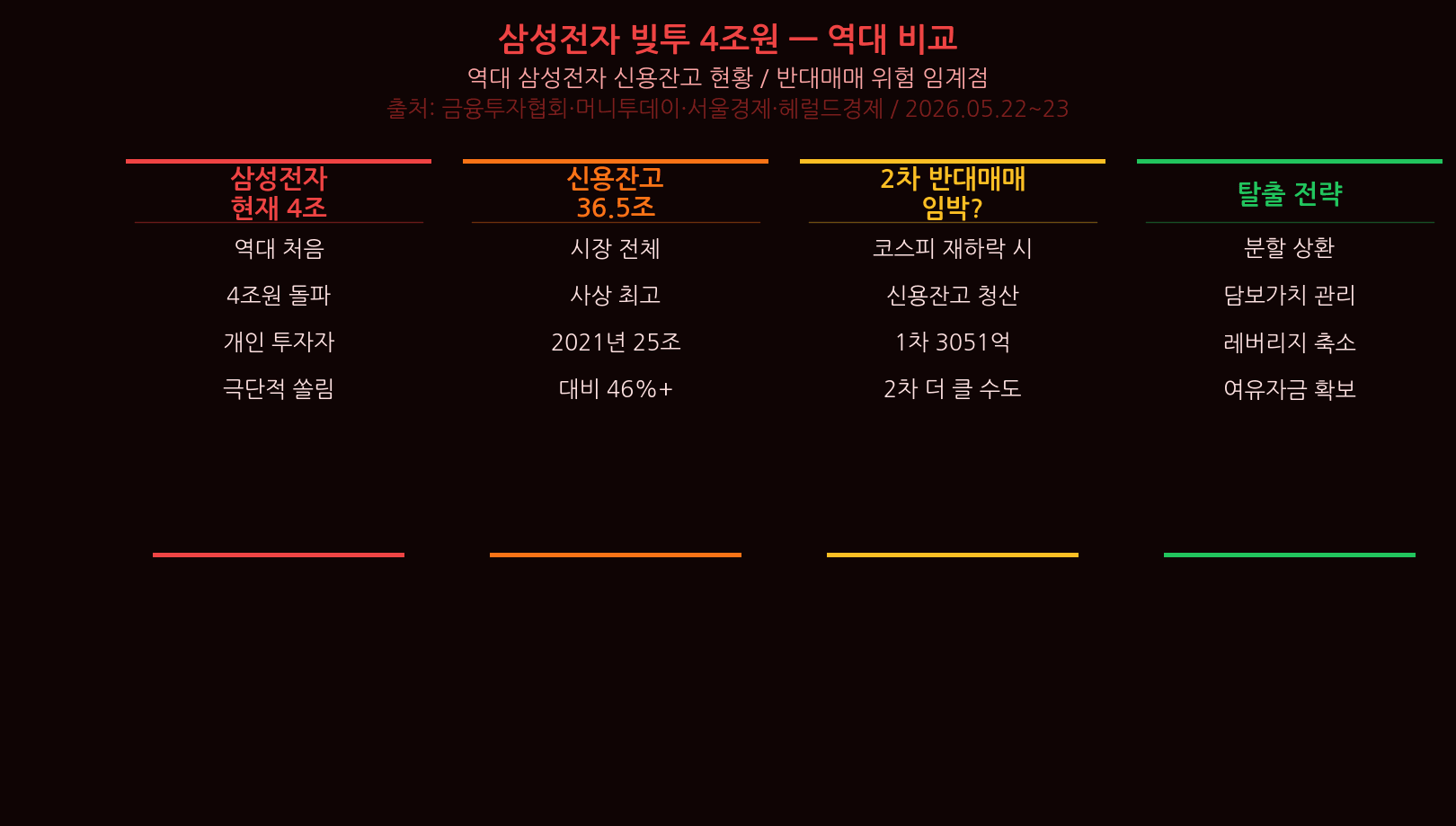

Samsung margin debt has crossed 4 trillion KRW for the first time ever. This represents the credit-loan balance retail investors hold on a single stock. The total market credit balance hit a record 36.5T KRW, far exceeding the 25T peak during the 2021 retail boom. A 4T KRW credit balance on a single security is unprecedented in Korean market history.

Why Credit Balances Did Not Shrink After the First Wave

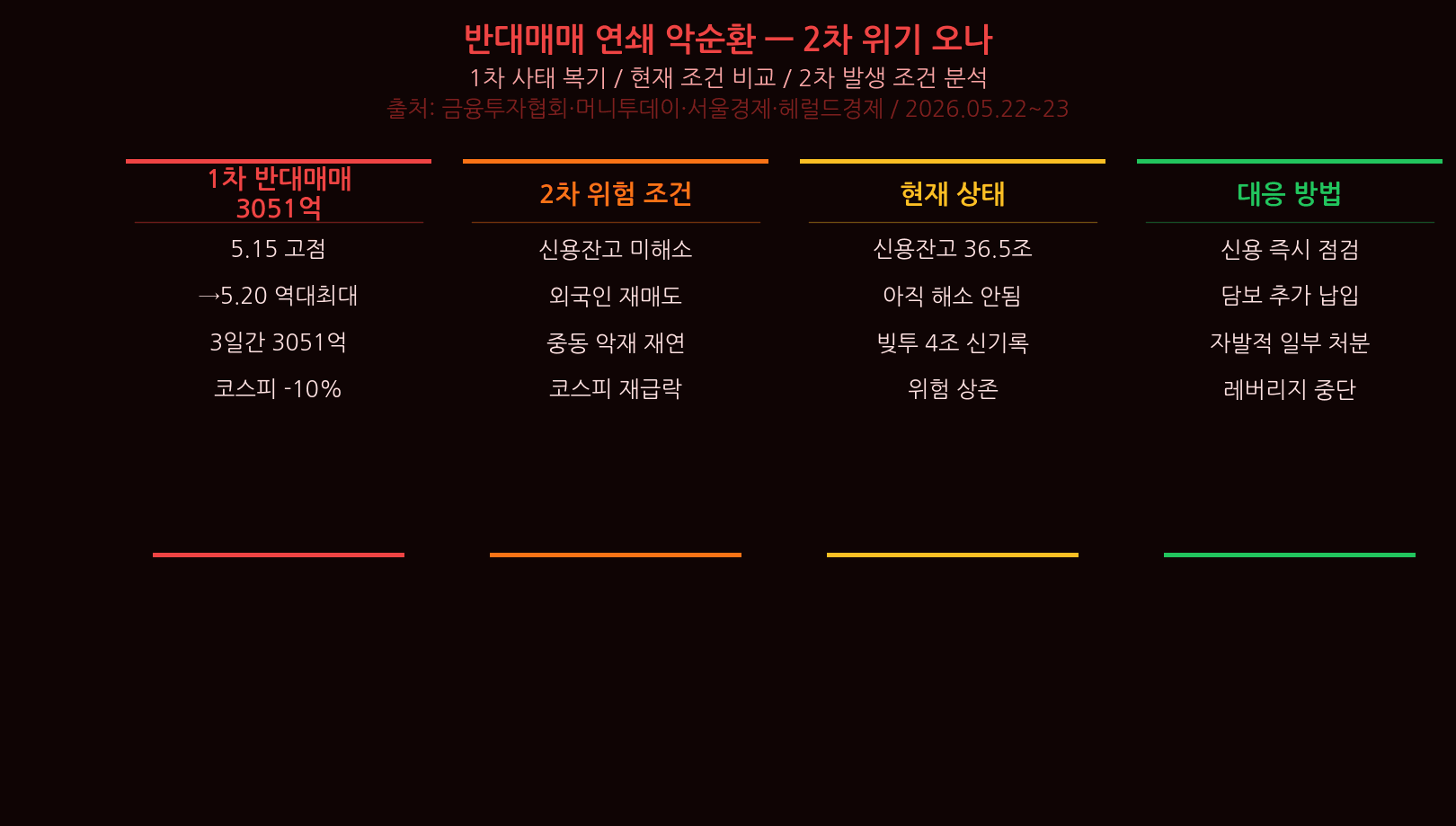

After the first wave of 305B KRW in forced liquidations, credit balances have barely declined. The pending leverage time bomb remains at 36.5T KRW. If KOSPI breaks below 7,500 again, a second wave could cascade. The first wave hit primarily T+2 unsettled trades; the longer 30–180 day credit loans still sit on the books, vulnerable to the next downturn.

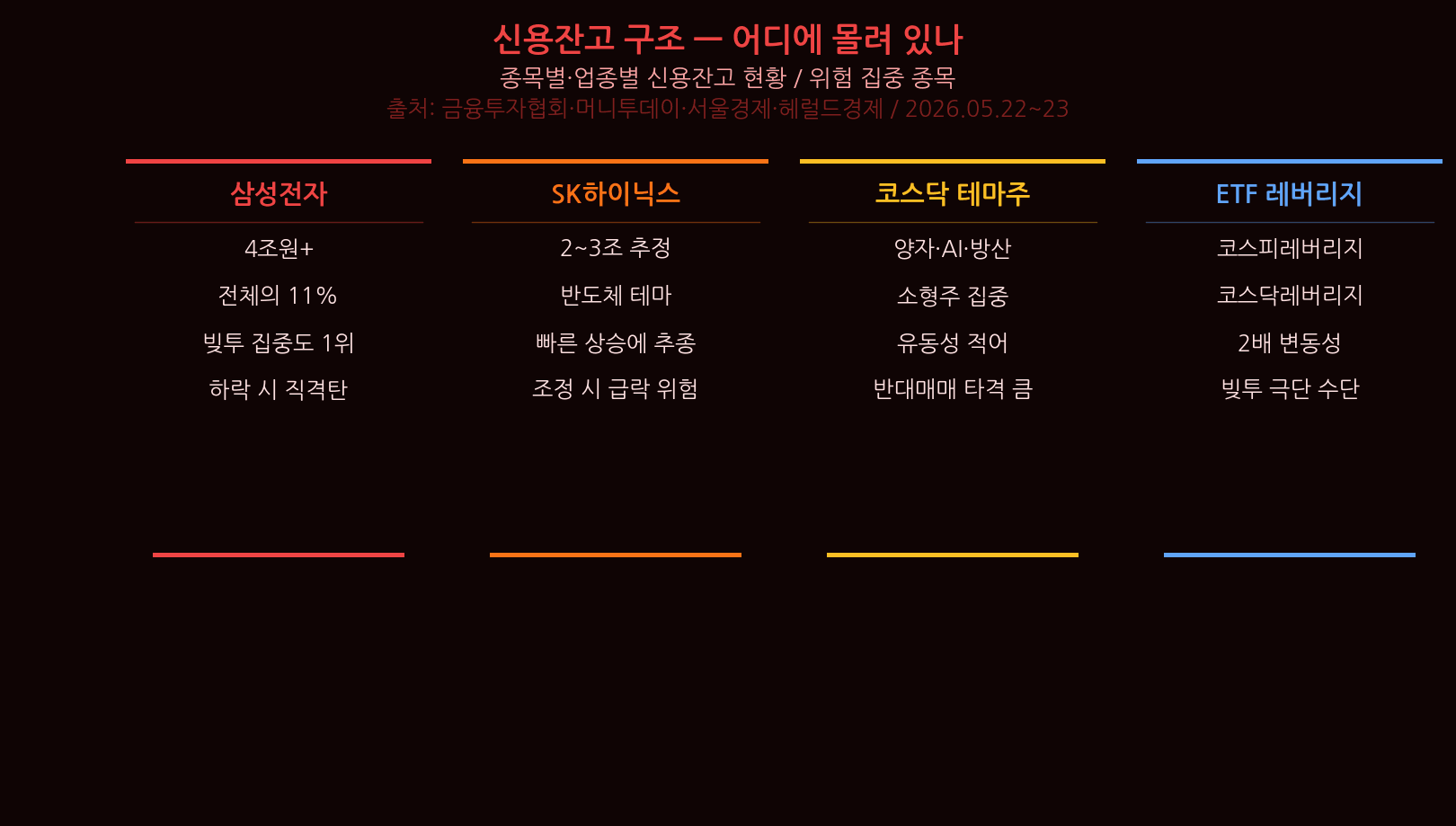

Credit Balance Distribution — Where the Margin Debt Concentrates

Margin debt risk is concentrated in specific names. Samsung leads at 4T KRW (11% of total), followed by SK Hynix at an estimated 2–3T. KOSDAQ thematic small-caps fill out the tail. Small-caps amplify forced-sale impact because liquidity is thin. Leveraged ETFs also attract margin debt, doubling the downside volatility when forced sales hit.

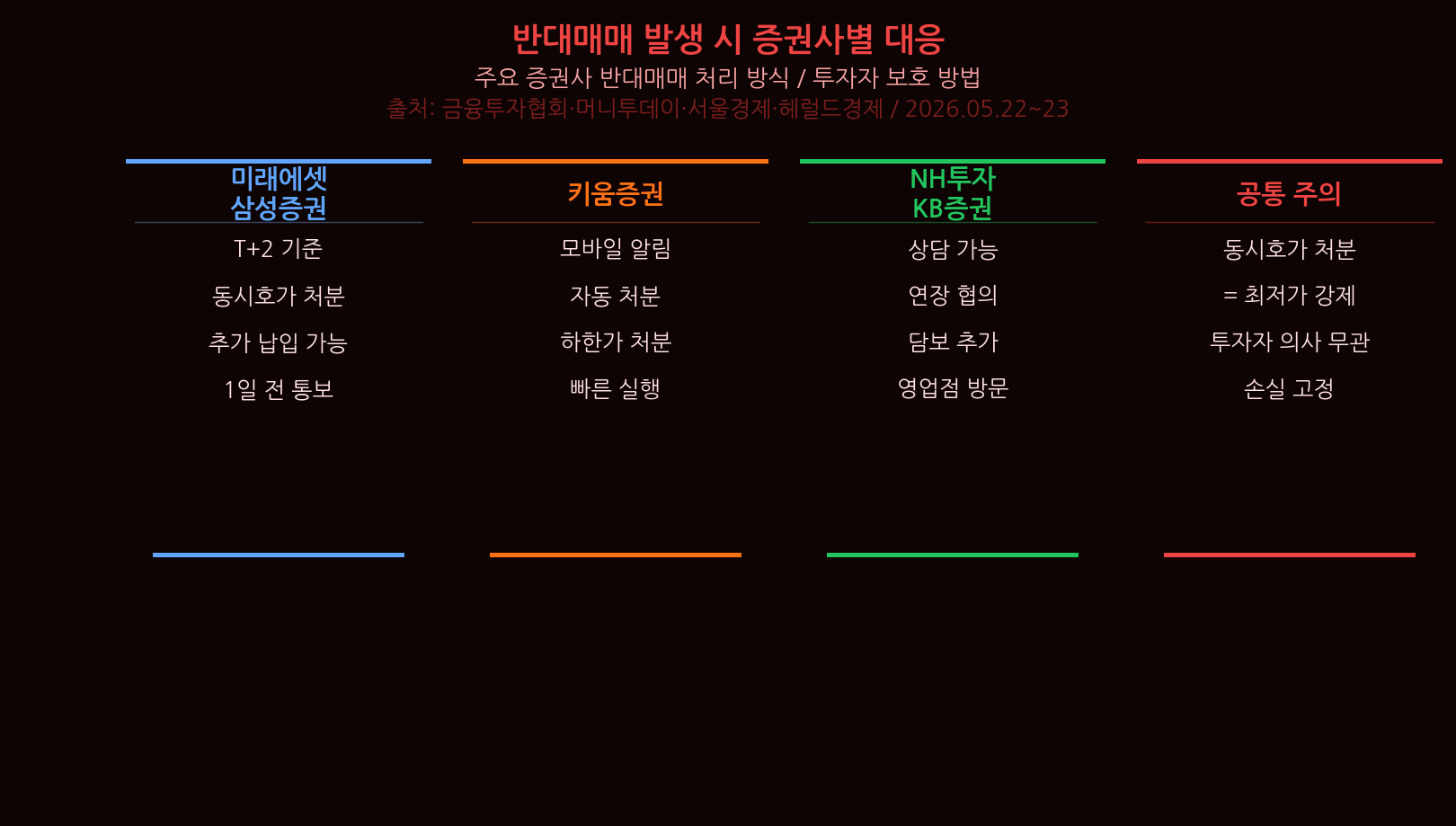

How Forced Liquidation Mechanics Actually Work

Forced liquidation triggers after collateral shortfall, executed at T+2 in the opening auction — effectively a forced sale at the lower-limit price. The loss crystallizes regardless of investor preference. Unsettled trades liquidate immediately upon non-payment; credit loans liquidate after margin call when maintenance margin breaks; stock loans liquidate the moment collateral ratio falls below threshold. Different triggers, different timing.

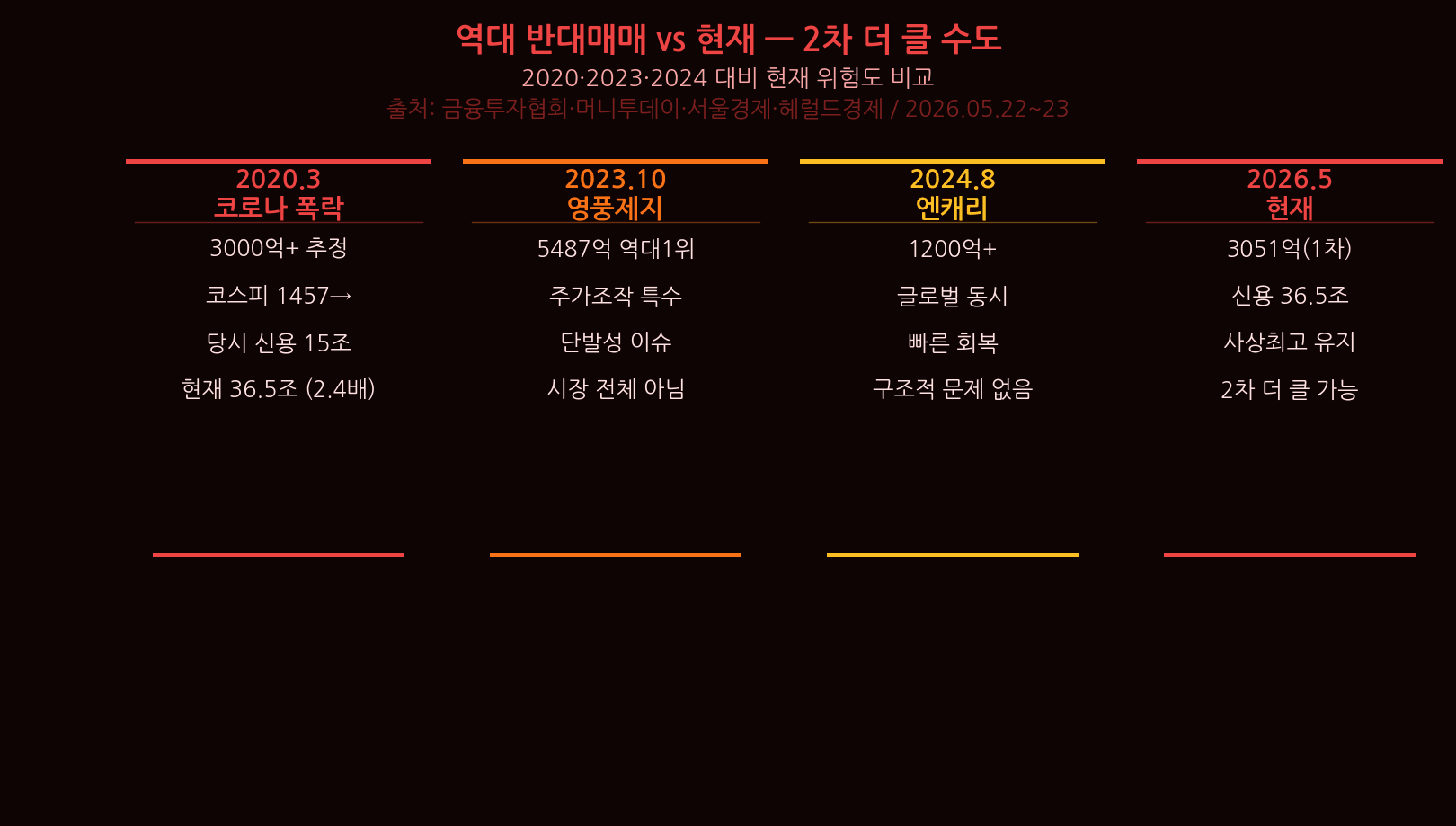

Historical Forced Liquidation Events vs. Today — Risk Comparison

In March 2020 (COVID), total credit balance was 15T KRW. Today it is 36.5T — 2.4x larger. The October 2023 Yeongpung Paper case (5.5B KRW) was a special situation driven by a trading halt. The August 2024 yen carry unwind (1.2B+) was a short-lived shock. The current May 2026 episode is unfolding with a 36.5T credit overhang. The latent risk has never been higher.

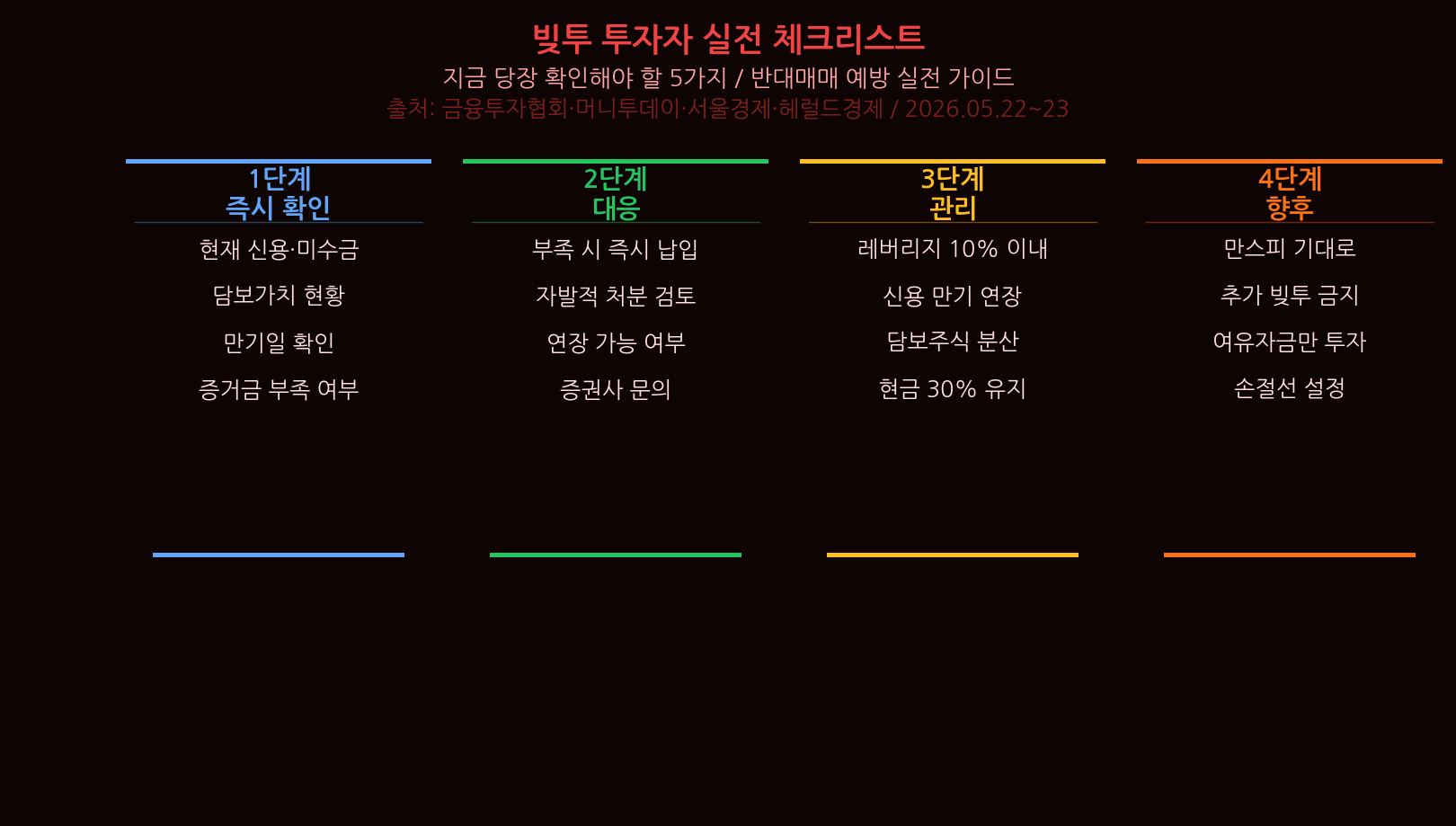

Margin Debt Investor Action Checklist — Do This Today

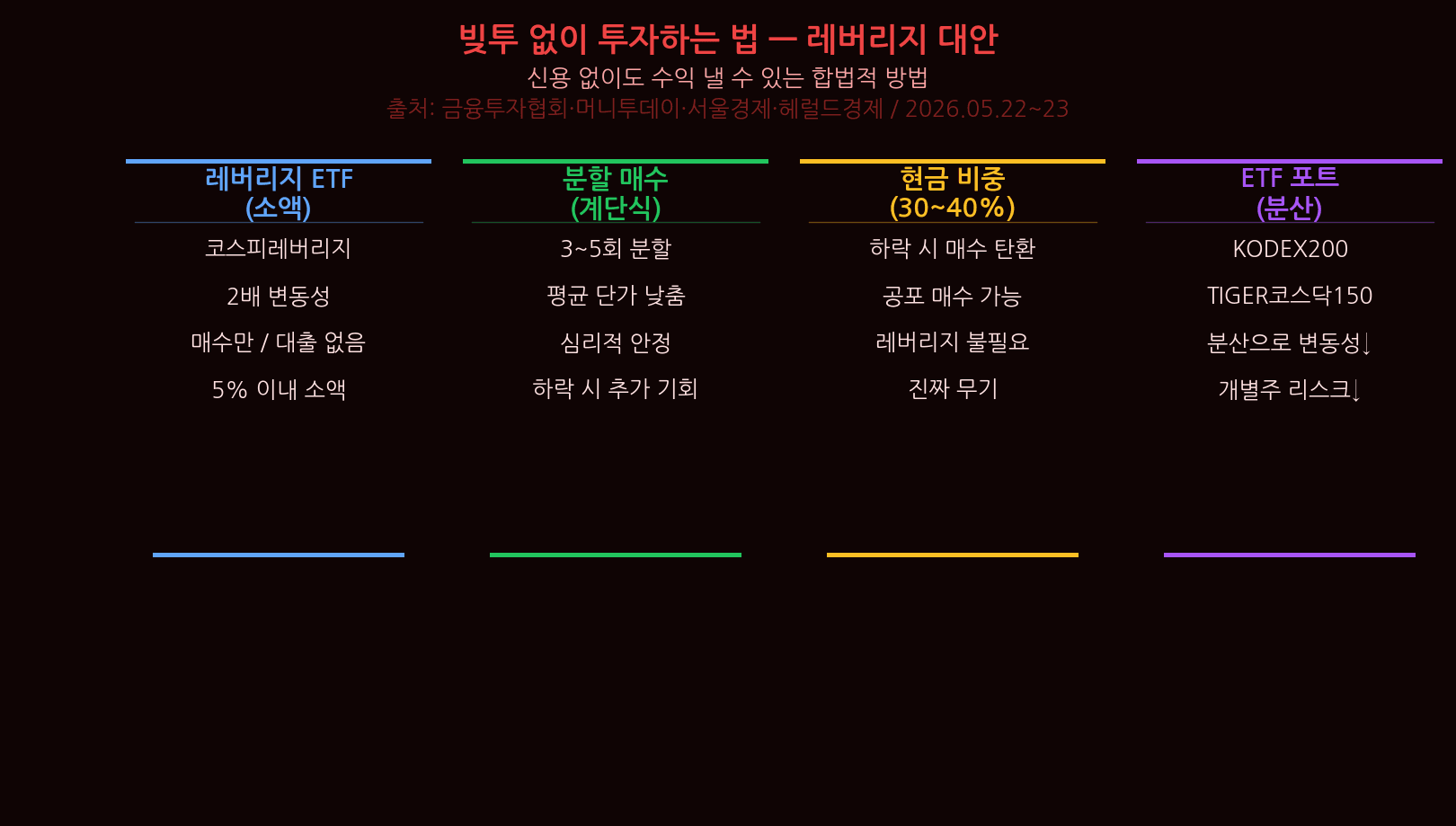

If you are currently on margin, act now. ① Check margin balances, settlement amounts, and collateral value today. ② If short, deposit cash or voluntarily reduce positions. ③ Cap total leverage at 10% of your portfolio. A voluntary partial exit beats a forced sale at the lower-limit price every time. Do not leave this to the system — manage it yourself.

5 Strategies for Korean Investors — Tickers and Stop-Loss Levels

Five strategies in response to the Samsung margin debt episode: ① Audit credit and unsettled positions now — maintenance margin first. ② KODEX 200 (069500) tranche-buy at 7,500–7,800, stop-loss -8%, weight 20%. ③ Samsung (005930) enter only after the 300,000 KRW breakout, stop-loss 240,000, weight 15%. ④ KODEX KOSPI Inverse (114800) as a hedge before the 36.5T balance unwinds, stop-loss -5%, weight 5%. ⑤ Hold 30–40% cash — no new leverage until credit balance normalizes.

Conclusion — What the Samsung Margin Debt Warning Really Says

Samsung margin debt crossing 4T KRW exposes a structural risk in the Korean market. The key fact: after the first wave of 305B in forced sales, 36.5T in margin debt remains on the books. If KOSPI drops another 10%, a much larger second wave could follow. Final checklist: clean up margin positions, cap leverage at 10%, hold 30%+ cash, dollar-cost average only, never chase.