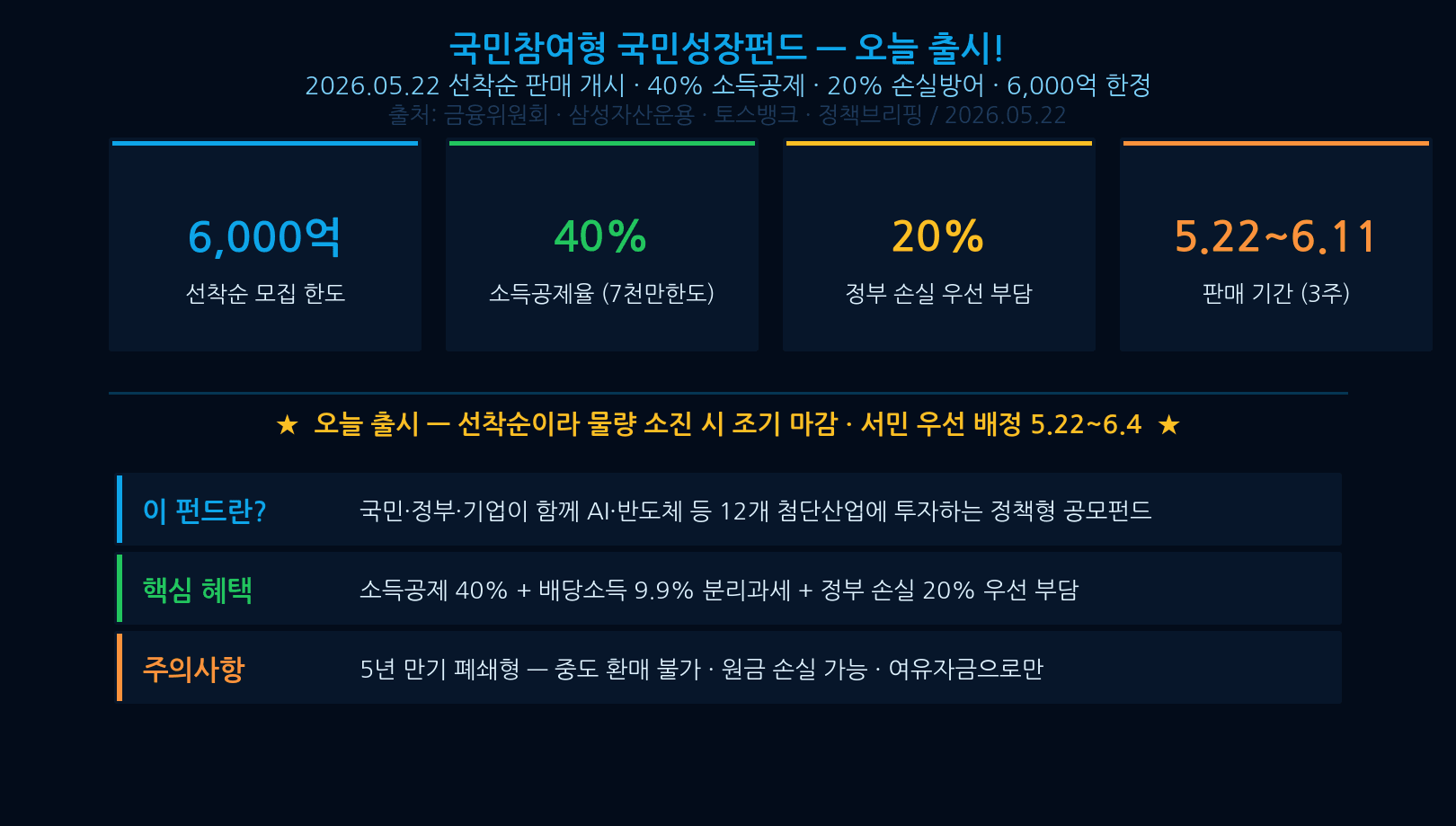

Korea National Growth Fund — Complete Guide: 40% Tax Deduction, 20% Loss Buffer

Real-Time Issue · May 22, 2026

Korea National Growth Fund — Complete Guide: 40% Tax Deduction, 20% Loss Buffer

Eligibility, How to Apply, Risks / Launches Today — 600B Won Limit on First-Come Basis

![[비비PICK] 리에티 LUNO RT 4056 선글라스](https://img1a.coupangcdn.com/image/affiliate/banner/8f965ee3220144b9189234e8256f5677@2x.jpg)

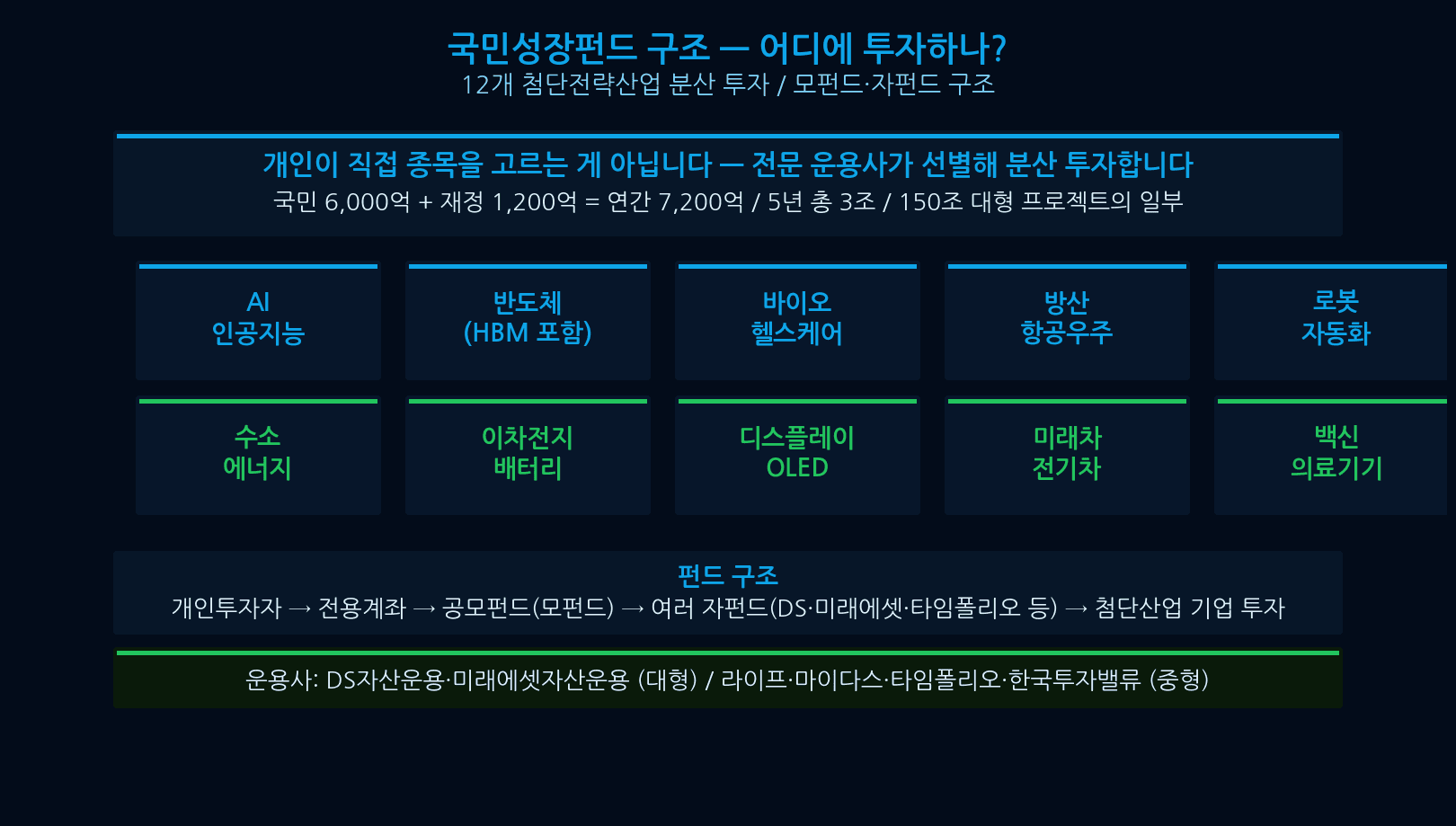

What Is the Korea National Growth Fund?

The Korea National Growth Fund (국민참여형 국민성장펀드) officially launched today, May 22, 2026, with a ₩600B cap on a first-come, first-served basis. It is a government-backed policy fund designed to channel capital into 12 strategic industries — AI, semiconductors, biotech, defense, robotics, hydrogen, batteries, displays, future mobility, and more. The public tranche of ₩600B combines with ₩120B in government fiscal funds to run ₩720B annually. Asset managers include DS Asset Management, Mirae Asset, Timefolio, Life, Midas Asset, and Korea Investment Value Asset Management.

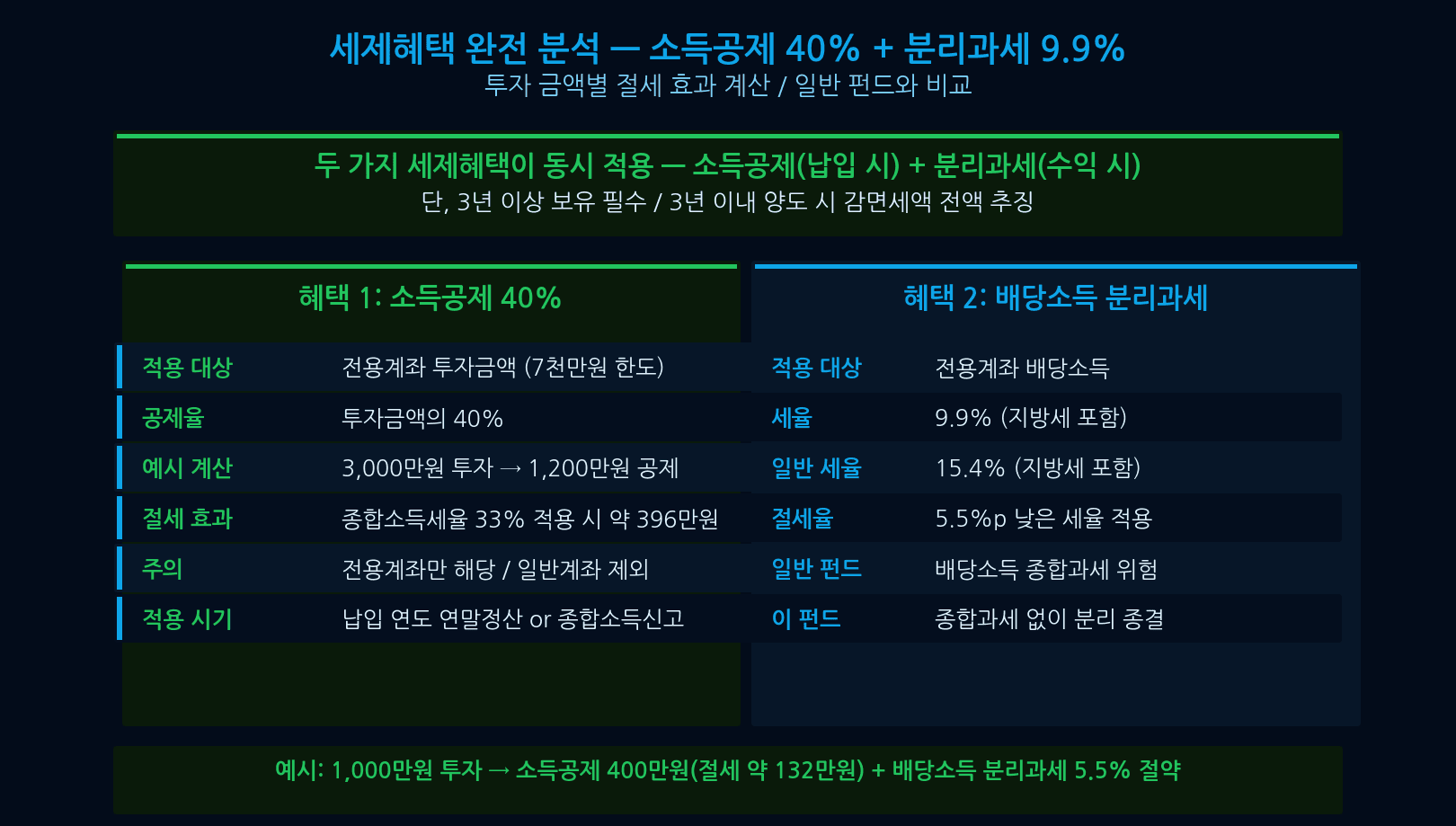

Tax Benefits — 40% Income Deduction + 9.9% Separate Tax

Two core tax advantages: ① 40% income deduction — on investments up to ₩70M, 40% of the invested amount is deductible from taxable income. A ₩30M investment yields a ₩12M deduction; at a 33% marginal rate that’s roughly ₩3.96M in tax savings. ② Dividend income taxed at 9.9% separately — versus 15.4% for regular funds, a 5.5%p advantage. Both benefits require holding in a dedicated account for at least 3 years. Early transfers trigger full clawback of benefits.

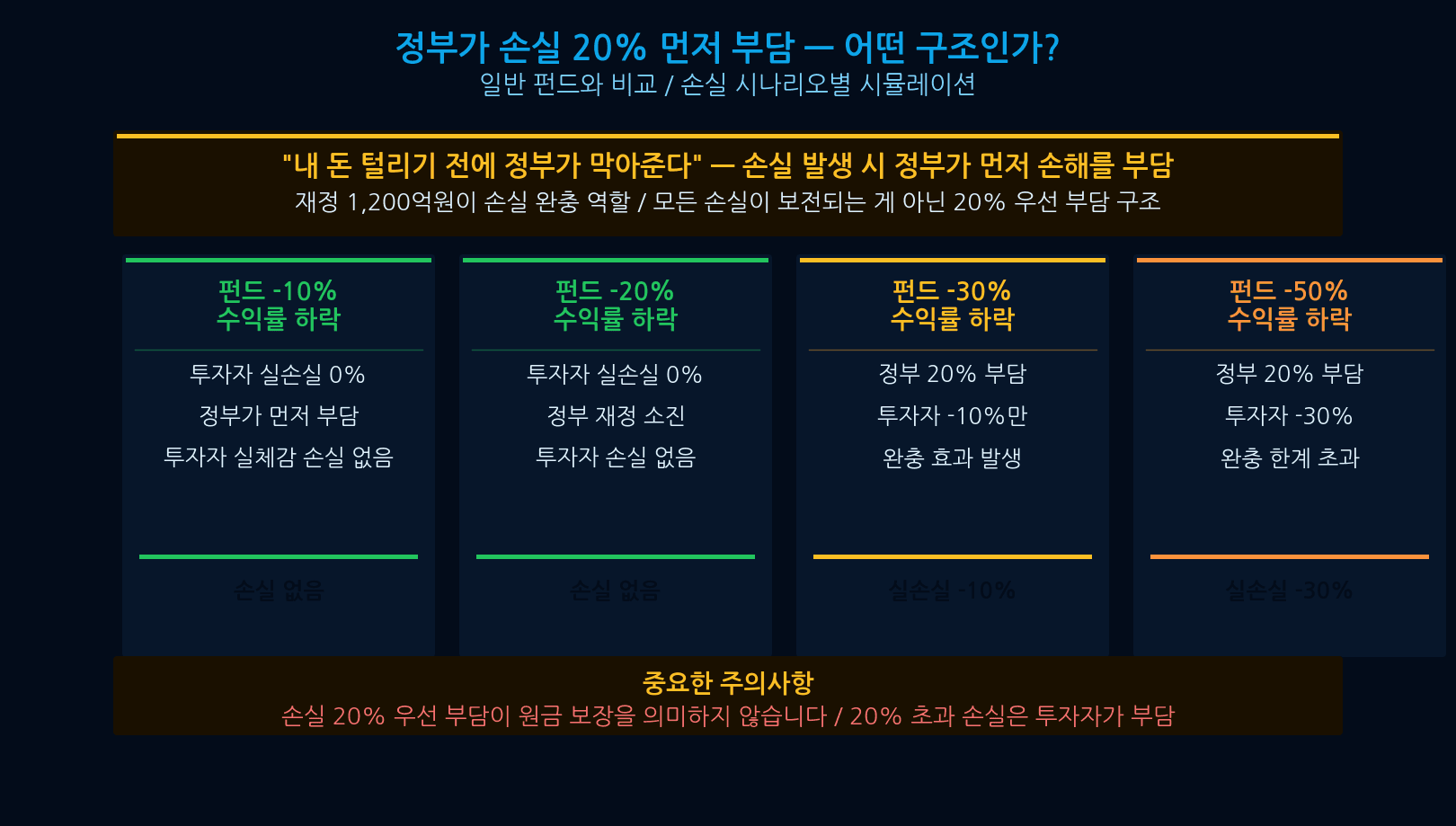

Government’s 20% Loss Buffer — How It Works

The ₩120B government fiscal tranche absorbs losses first. If the total fund declines 20%, retail investors are fully protected. If it declines 30%, the government absorbs the first -20% and investors bear the remaining -10%. This is a loss buffer, not a capital guarantee. The fund concentrates in high-growth strategic sectors with inherent market volatility. “Government fund = safe” is a dangerous misconception — always read the fund prospectus carefully.

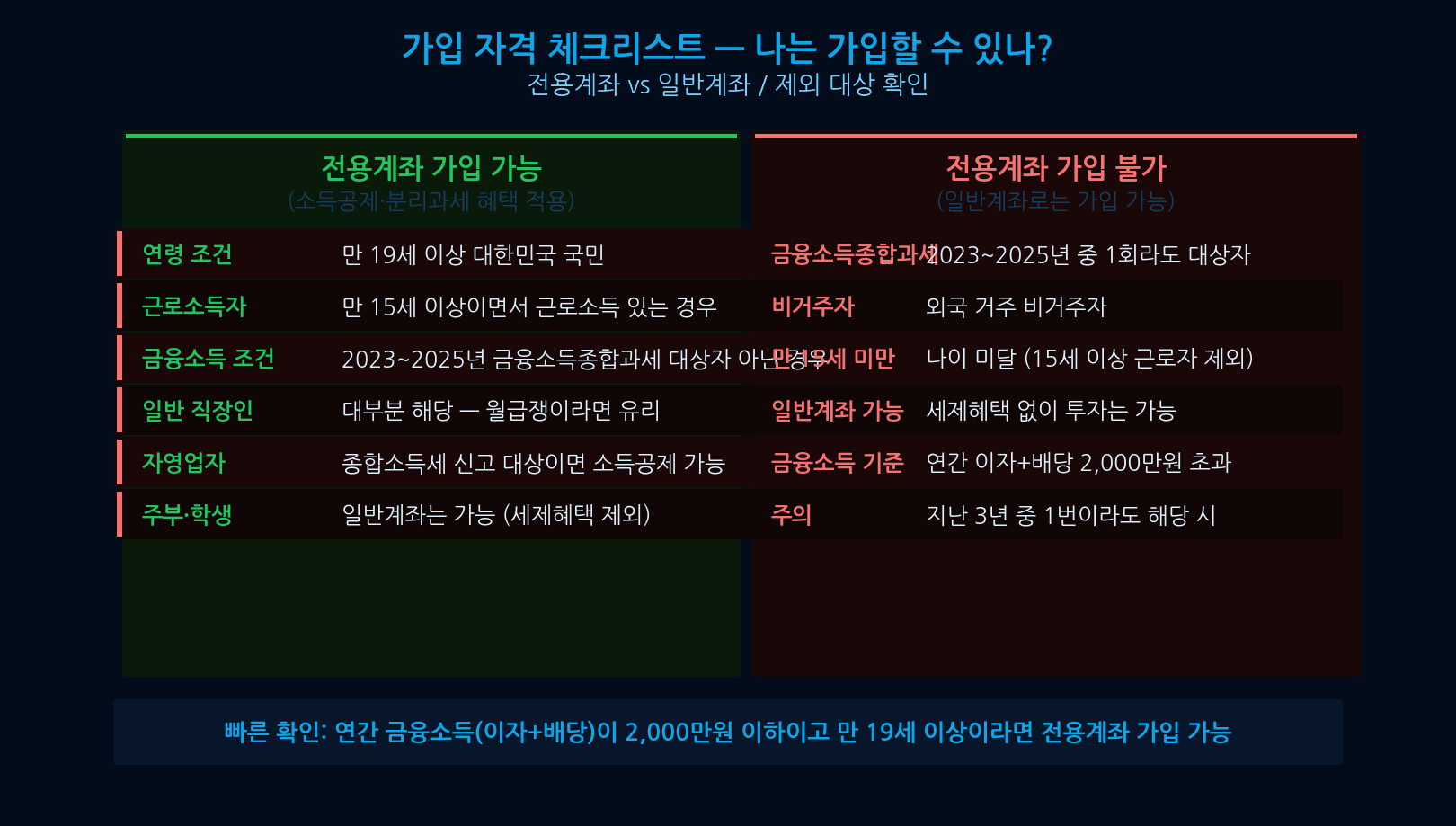

Eligibility — Can You Invest?

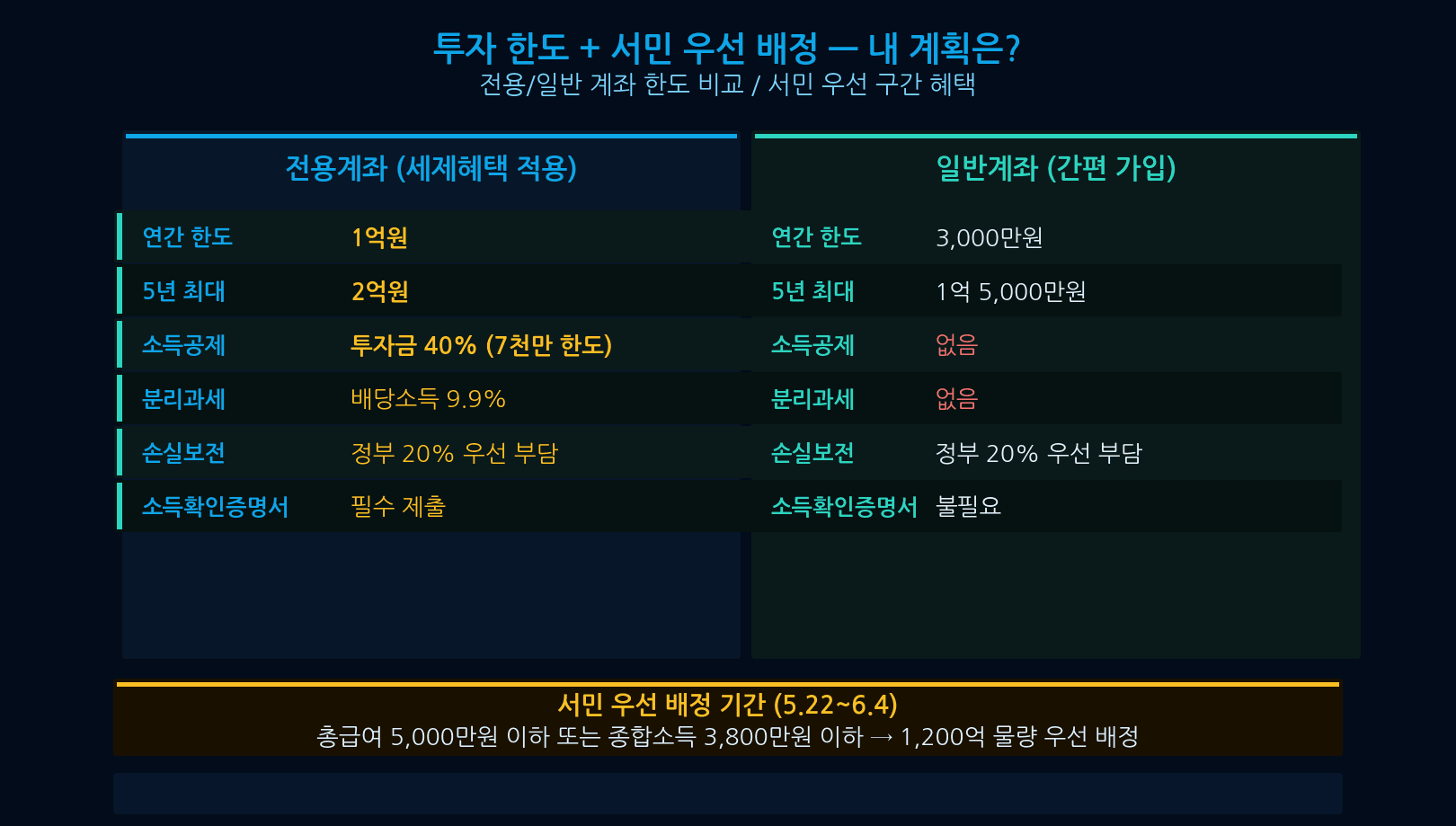

Dedicated account (with tax benefits): Age 19+, not subject to comprehensive financial income taxation in 2023–2025. Annual limit: ₩100M; 5-year total: ₩200M. Income verification certificate required. Regular account (no tax benefits): Age 19+, no income restrictions. Annual limit: ₩30M; 5-year total: ₩150M. Quick check: if your annual interest + dividend income is under ₩20M and you are 19+, you likely qualify for the dedicated account. Most salaried workers qualify.

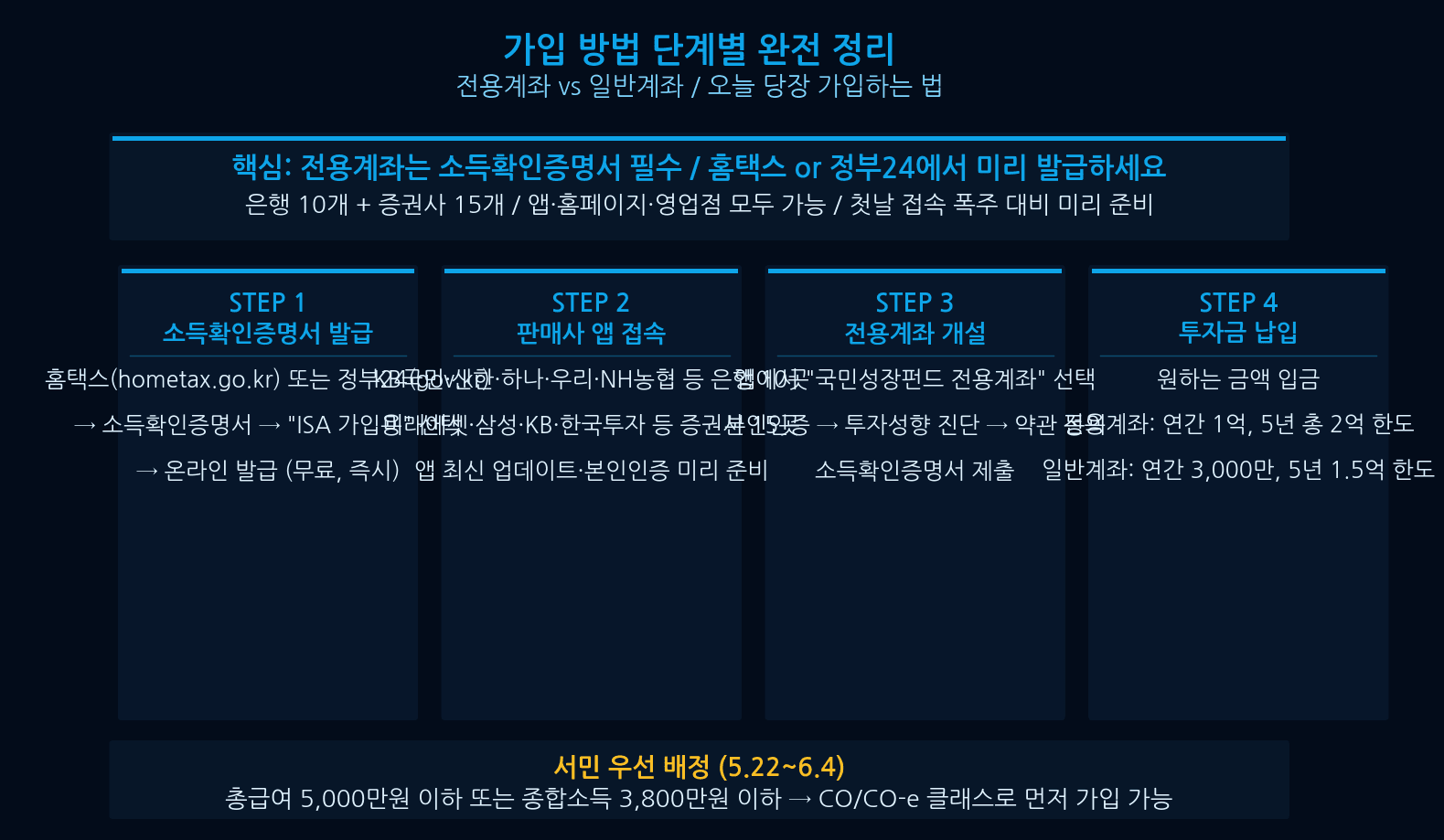

How to Apply — Step-by-Step Guide

Four steps: STEP 1 — Obtain an income verification certificate (ISA type) from Hometax (hometax.go.kr) or Government24. STEP 2 — Open the app of your bank (KB, Shinhan, Hana, Woori, NH Nonghyup, etc.) or brokerage (Mirae Asset, Samsung, KB, Korea Investment, etc.). STEP 3 — Open a dedicated account (submit income certificate). STEP 4 — Deposit your investment amount. From today through June 4, priority allocation is reserved for low-income earners (annual salary under ₩50M or comprehensive income under ₩38M).

Investment Limits + Priority Allocation Period

Dedicated account: ₩100M/year, ₩200M over 5 years. Regular account: ₩30M/year, ₩150M over 5 years. The priority allocation period (May 22 – June 4) reserves the bulk of the ₩600B cap for low-income earners. Given the first-come, first-served structure, remaining allocation for general applicants after this period may be limited. If you’re interested, apply now rather than waiting.

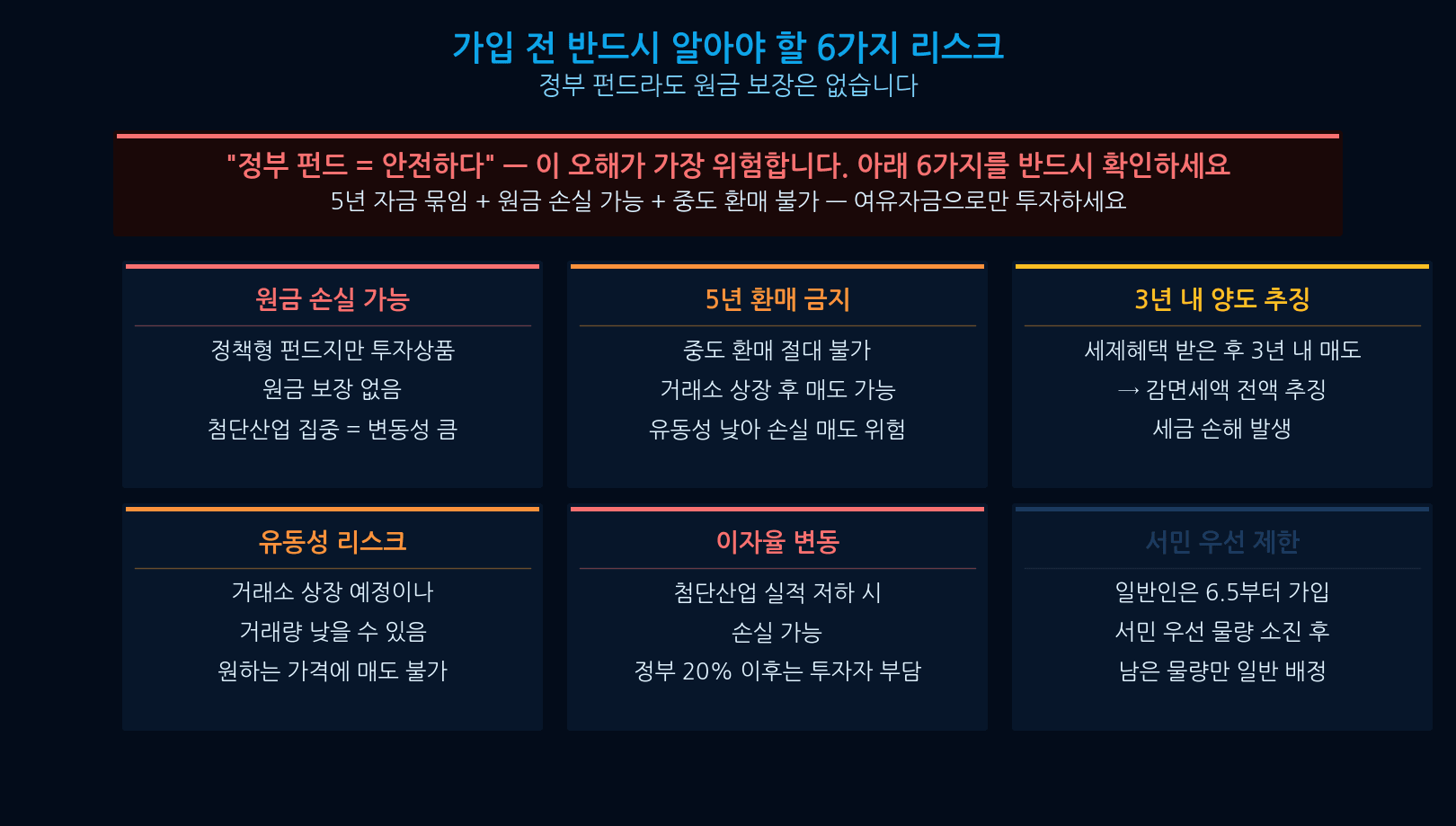

Key Risks — 5 Things You Must Know Before Investing

Five critical cautions: ① Mandatory 5-year hold — no early redemption. ② No principal guarantee — loss buffer covers only the first -20%. ③ Full clawback of tax benefits if transferred within 3 years. ④ Tax benefits only apply to dedicated accounts — regular accounts receive none. ⑤ High concentration in strategic sectors means elevated volatility risk. The fund is backed by the government in structure — not in outcome. Always read the prospectus before investing.

Should You Invest? — Decision Guide by Investor Type

Recommended for: salaried workers earning ₩50M–₩100M+ annually (maximum tax deduction benefit), investors with 5+ years of idle capital, those seeking long-term exposure to AI and semiconductor themes. Not recommended for: those who may need funds within 5 years, those seeking capital guarantees, or those subject to comprehensive financial income taxation (ineligible for dedicated account). The 40% deduction is most powerful for those in the 33–45% marginal tax bracket.

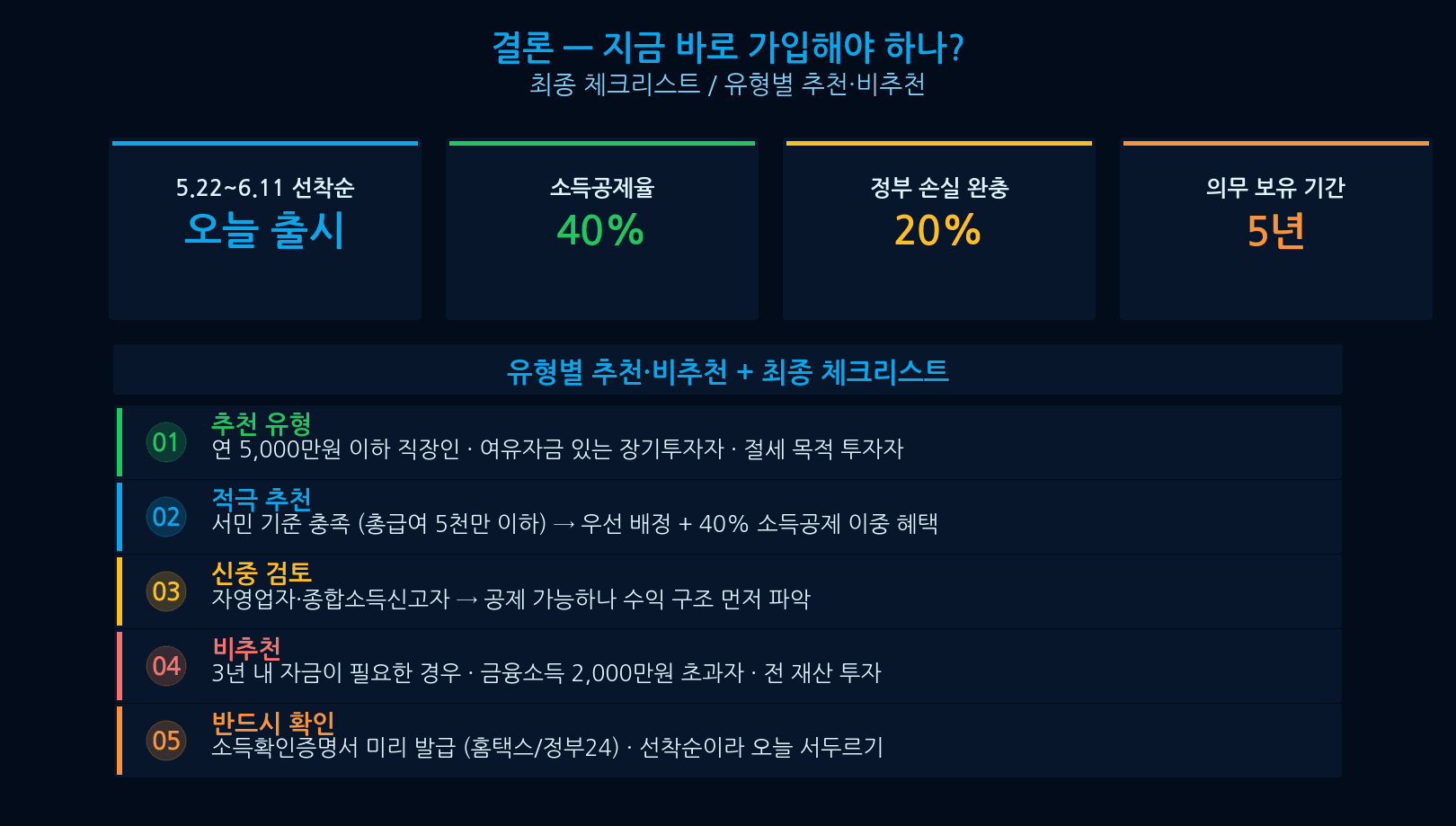

Conclusion — Final Checklist

Korea National Growth Fund final checklist: Confirm age 19+ and not subject to comprehensive financial income tax / Obtain income verification certificate from Hometax / Search “국민성장펀드” in your bank or brokerage app / Confirm 5-year liquidity plan (no early exit) / Calculate 40% deduction benefit (investment x 40% x your marginal rate) / Apply by June 4 during priority allocation period. The 40% deduction delivers an immediate, concrete return before a single stock moves. Only invest if you can genuinely commit to the 5-year lock-up.

Sources: FSC Korea Korea JoongAng Daily Reuters