Jusung Engineering Stock Analysis — World-First ALG Shipment May 18, Global ALD #4, KIS Target KRW 189,000

Trending · 2026.05.18

Jusung Engineering stock (036930.KQ) full analysis — world’s first ALG transistor full-integration semiconductor equipment shipped today (May 18). Global ALD #4, Korea Investment Securities targets KRW 189,000. Up +433% in 52 weeks. Three scenarios and five trading strategies.

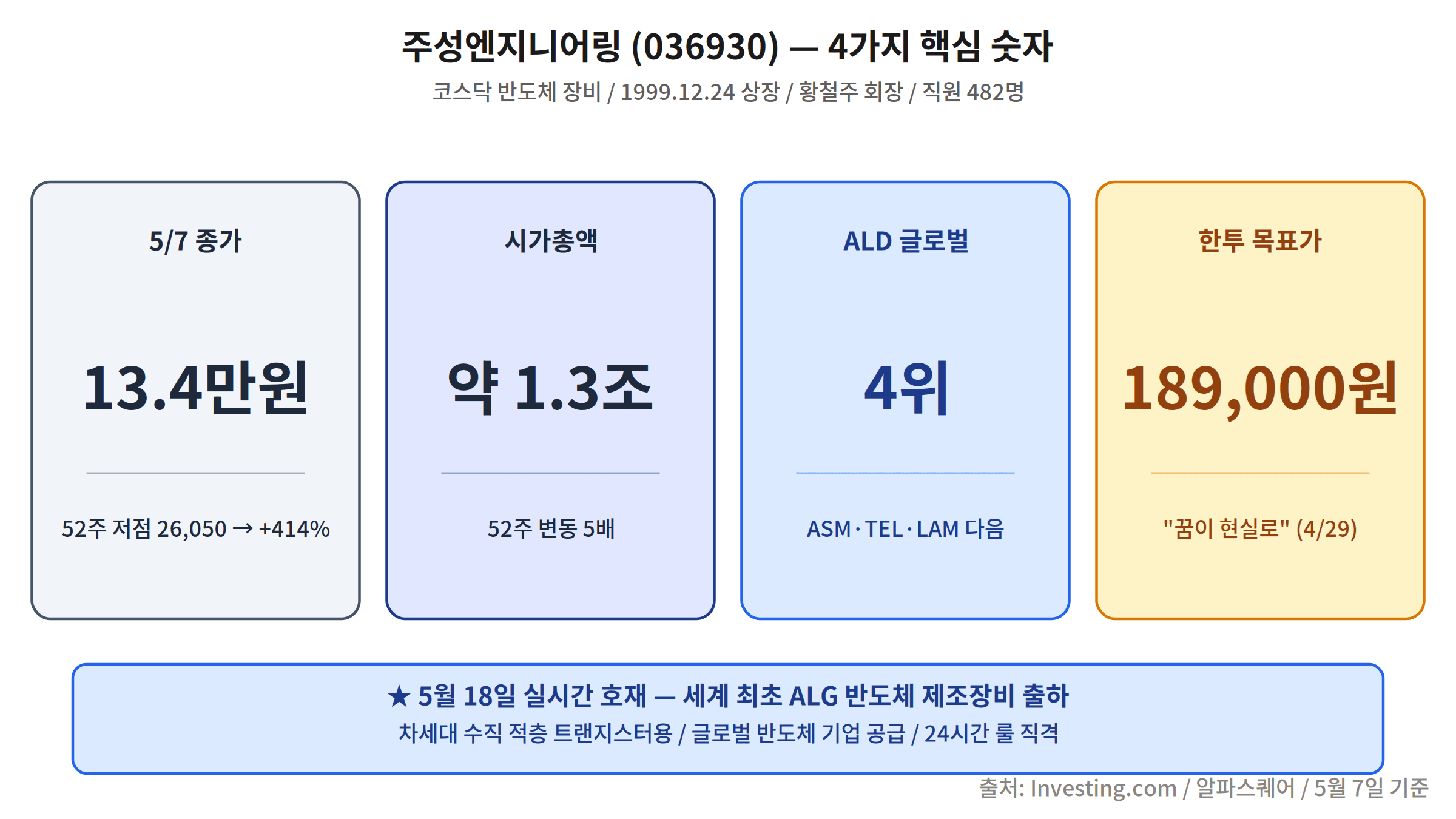

Jusung Engineering (KOSDAQ 036930) shipped the world’s first ALG (Atomic Layer Growth) transistor full-integration semiconductor manufacturing equipment to a global semiconductor company today, May 18. Closing price May 7: KRW 133,500. 52-week range: KRW 26,050–138,900 (+433%). Global ALD #4. Five-broker average target: KRW 130,000; Korea Investment Securities high target: KRW 189,000.

“Beyond making equipment, we are setting new standards for semiconductor manufacturing in the AI era. We will continue to present new paradigms based on world-first, world-only innovation.”

— Jusung Engineering · May 18, 2026 ALG Shipment Ceremony

Business Structure — 98% Semiconductor, Direct Play on Memory Supercycle

2025 revenue: KRW 310.7B total — semiconductor equipment KRW 303.7B (97.8%), display/solar KRW 6.9B (2.2%). Key customers: SK Hynix, Samsung Electronics, Chinese CXMT. Products: ALD, ALG, SDP, CVD equipment for memory and logic fabs.

The macro backdrop is favourable: SK Hynix Q1 2026 operating profit KRW 37.61T (+405.5% YoY, all-time high), Samsung Electronics 8x increase. The memory supercycle means major capex cycles are beginning — directly translating into Jusung equipment orders.

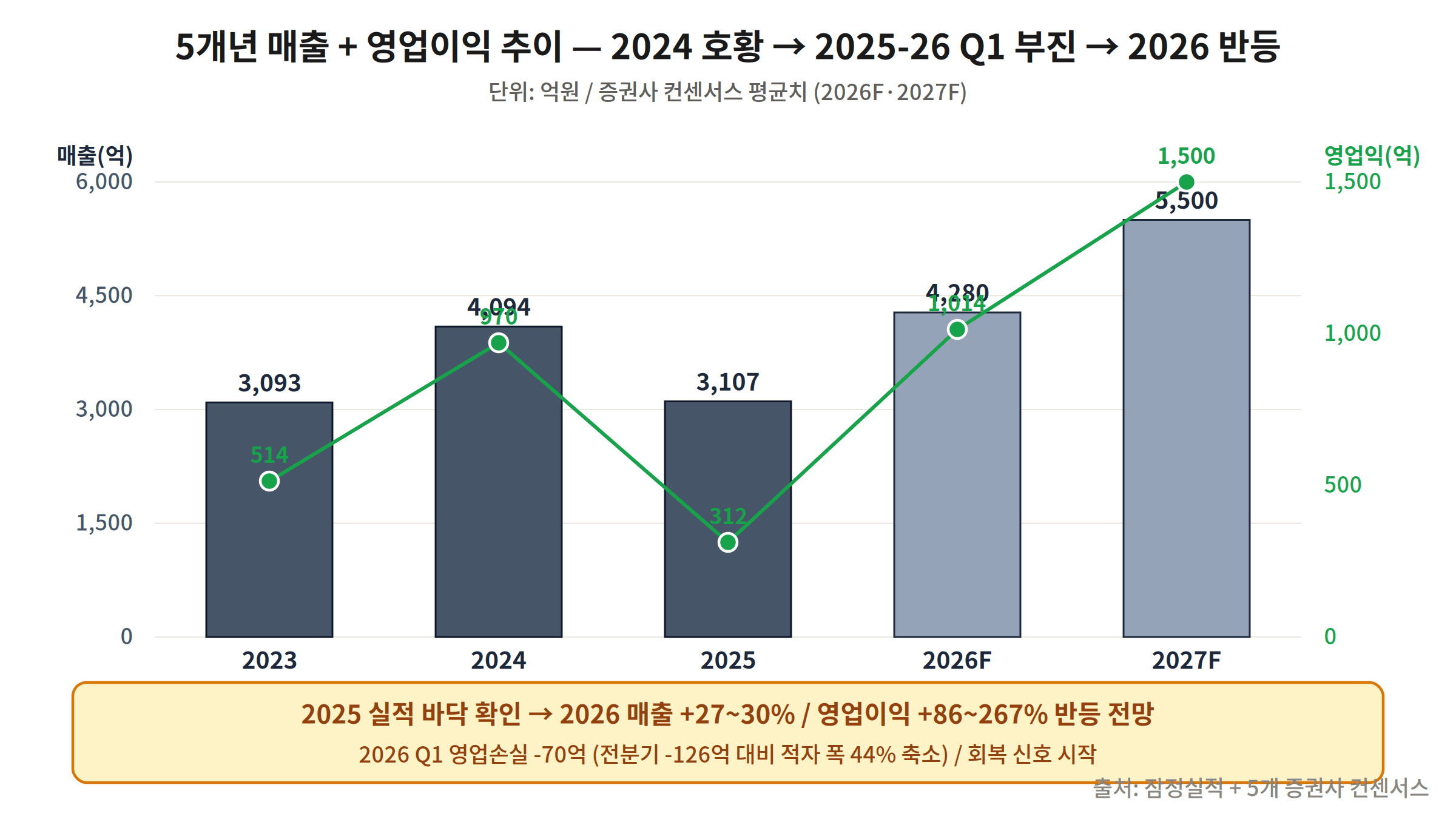

Jusung Engineering Stock Outlook — Five-Year Financials: 2024 Peak → 2025 Trough → 2026 Recovery

Five-year revenue arc: 2024 KRW 409.4B (record peak) → 2025 KRW 310.7B (-24%) → 2026F KRW 428.0B (+38%), operating profit KRW 101.4B (+225%) — 2026 is the inflection point. Q1 2026 posted KRW 54.9B revenue (-54.6% YoY) and KRW -7.0B operating loss, but the loss narrowed 44% vs Q4 2025’s KRW -12.6B — an early recovery signal. Q2 2026 results are due August 7.

Balance Sheet Health + Global ALD #4 — Cheapest Valuation at 25.1x P/E

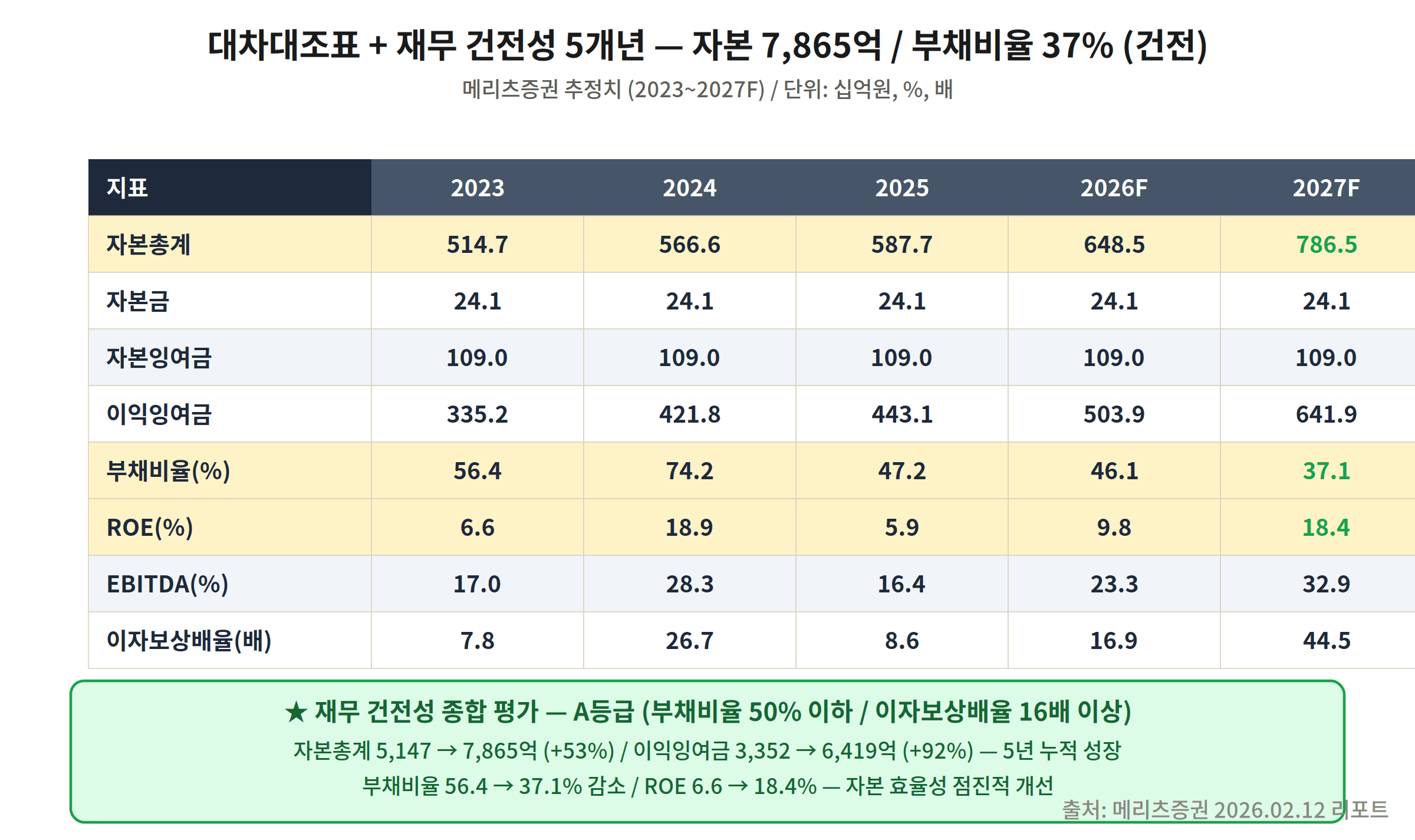

Financial health (2027F Meritz estimates): total equity KRW 786.5B / debt-to-equity 37% / interest coverage 44.5x (A-grade). Feb 10: KRW 40.9B treasury stock cancellation + KRW 2.4B cash dividend — shareholder return commitment confirmed.

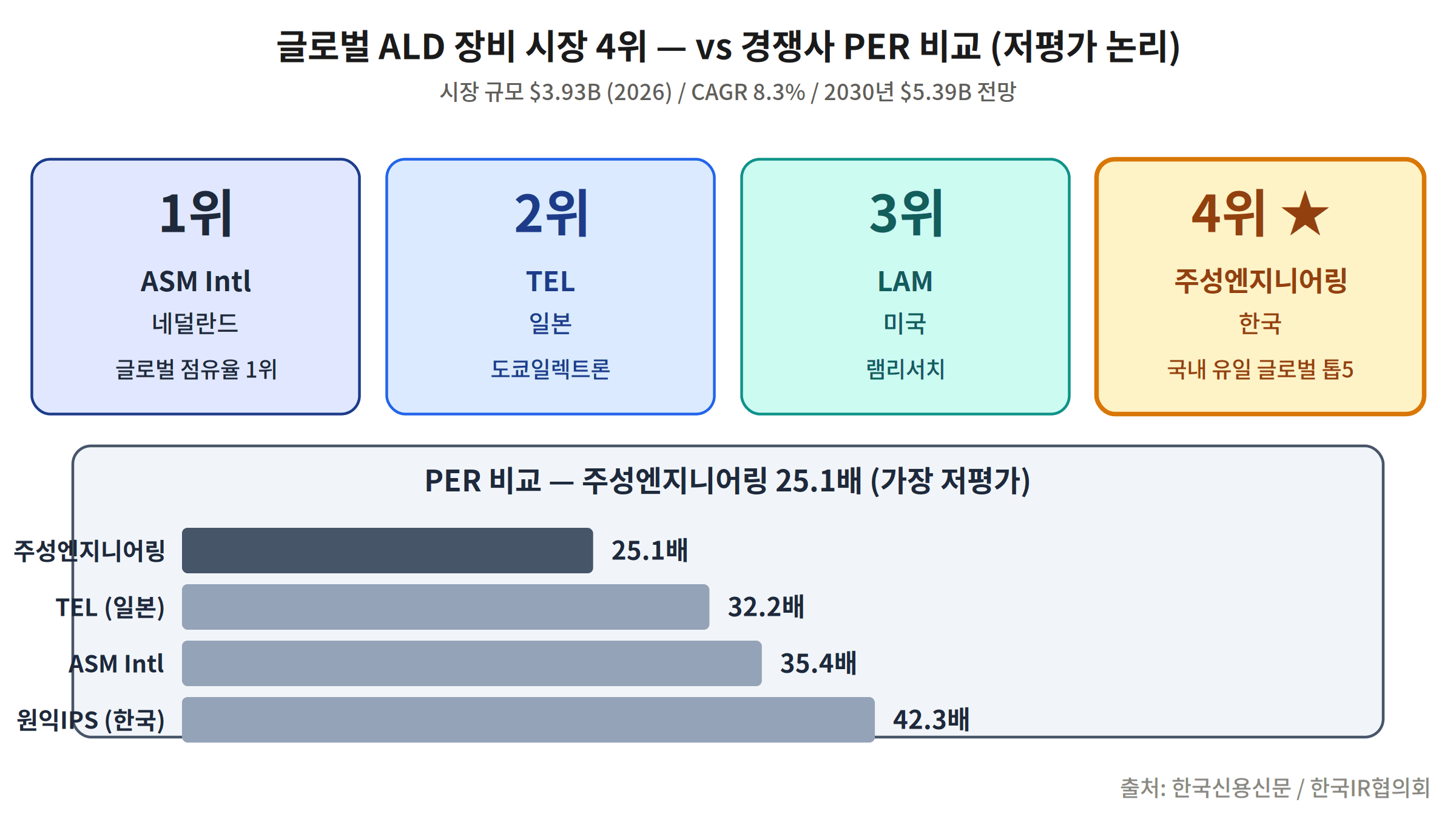

Global ALD equipment market: USD 3.93B in 2026, growing at 8.3% CAGR to USD 5.39B by 2030. Market rank: #1 ASM International (Netherlands) → #2 TEL (Japan) → #3 LAM Research (US) → #4 Jusung Engineering (Korea). P/E 25.1x — lowest among peers (Wonik IPS 42.3x, ASM 35.4x, TEL 32.2x).

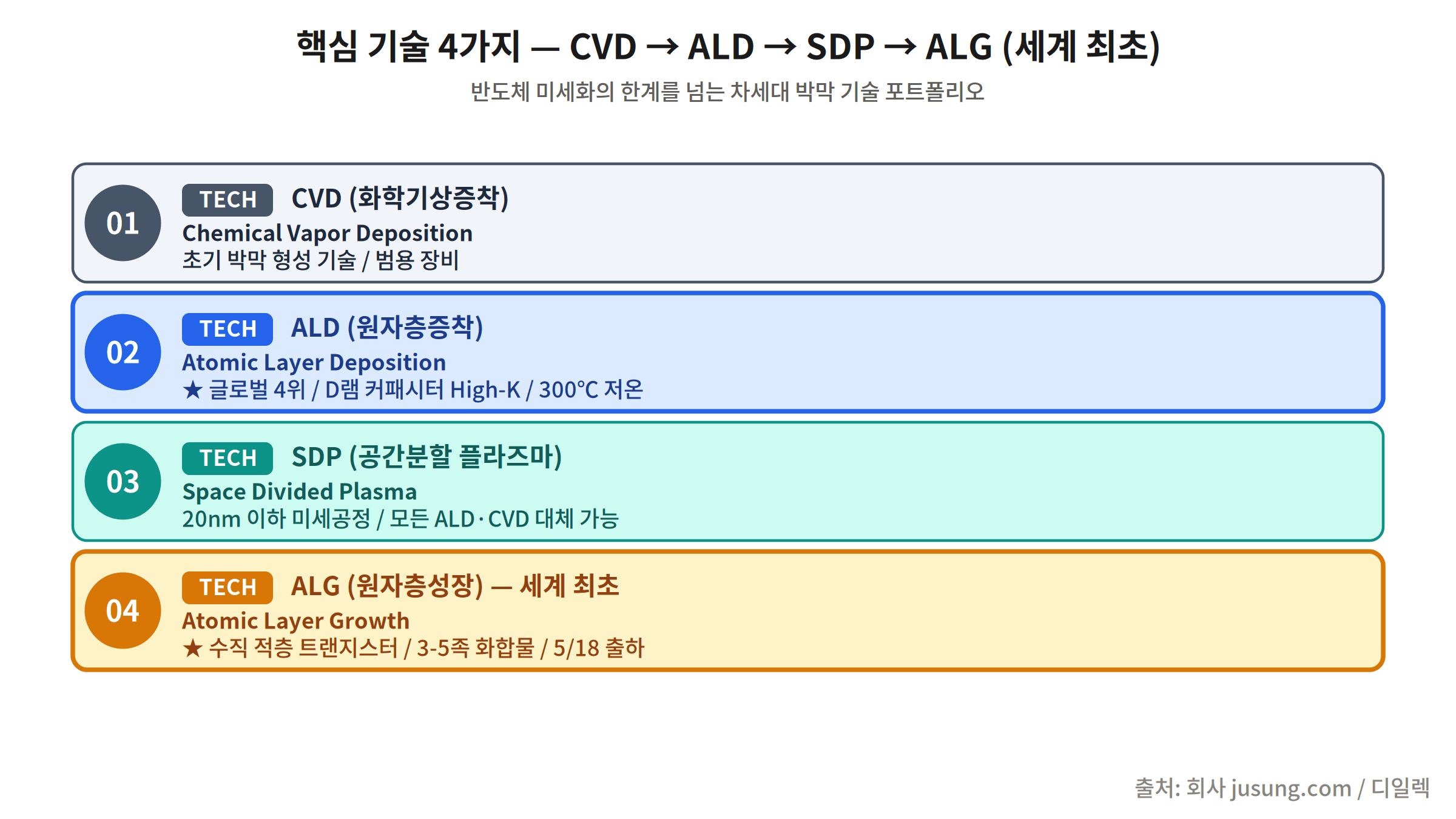

Four Core Technologies — CVD → ALD → SDP → ALG (World First)

ALG (Atomic Layer Growth) is a world-first technology. Unlike ALD, ALG grows atomic layers like growing crystals — not limited to silicon wafers but capable of compound semiconductors (III-V, III-VI groups) on glass substrates. Electron mobility is 6x higher than silicon (8,500 cm²/Vs vs 1,400 cm²/Vs). SDP can replace all ALD/CVD equipment in sub-20nm processes. CEO Hwang Cheol-joo: “We are the world’s first to achieve yields more than 10x higher than existing methods.”

Six 2026 Catalysts — World-First ALG Shipment Today

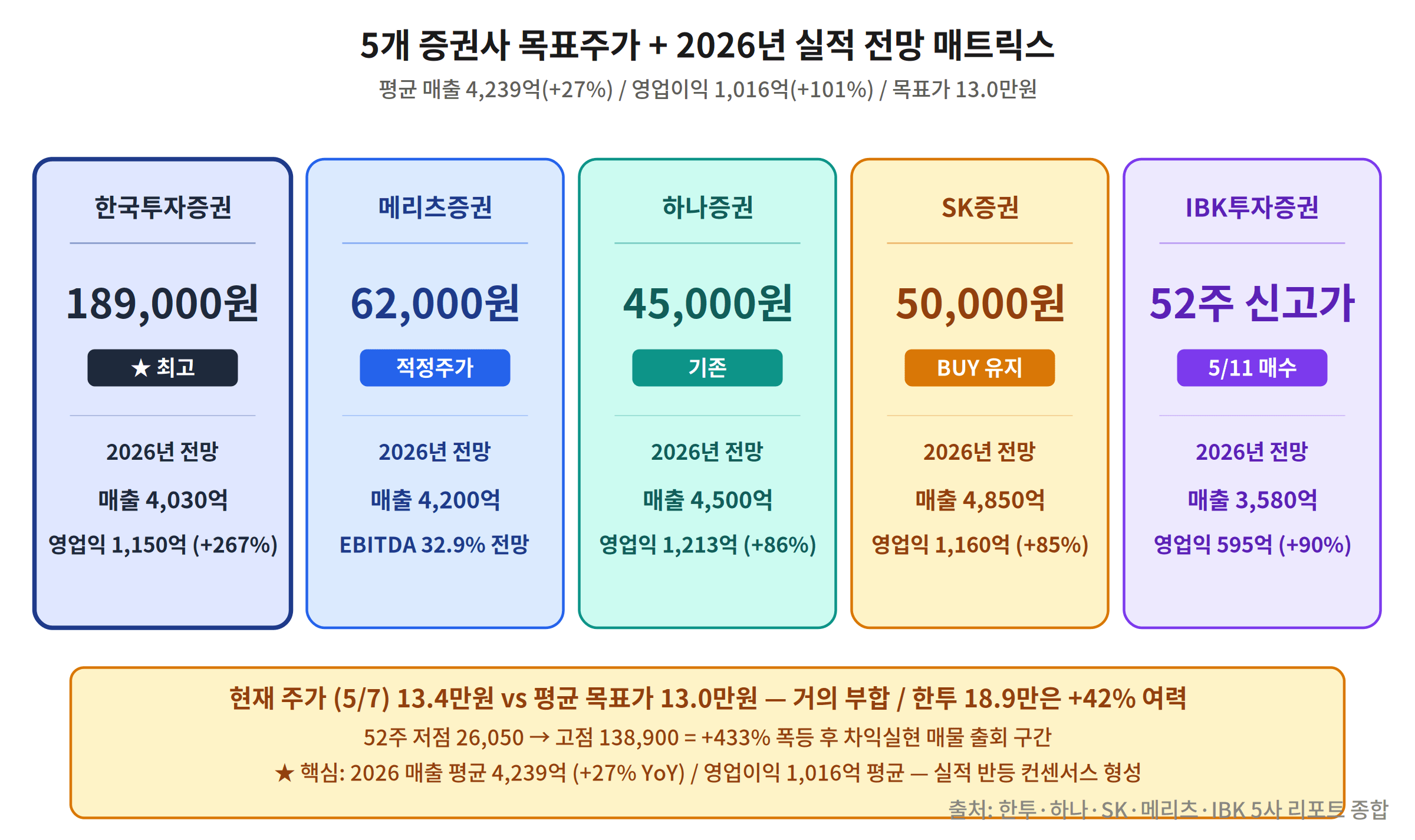

Five Broker Jusung Engineering Stock Targets — Average KRW 130,000

Five-broker consensus: 2026 revenue KRW 423.9B (+27%), operating profit KRW 101.6B (+101%). The target range is extreme: Korea Investment Securities KRW 189,000 (high) vs Hana Securities KRW 45,000 (low). Current price KRW 134,000 is nearly equal to the five-broker average. Check real-time data via Naver Finance 036930.

| Broker | Target Price | 2026 Revenue | Rating |

|---|---|---|---|

| Korea Investment Securities ★ | KRW 189,000 | KRW 403.0B | BUY / Apr 29 |

| Meritz Securities | KRW 62,000 | KRW 420.0B | BUY / Feb 12 |

| SK Securities | KRW 50,000 | KRW 485.0B | BUY |

| Hana Securities | KRW 45,000 | KRW 450.0B | BUY |

| IBK Securities | 52W High | KRW 358.0B | BUY / May 11 |

| Average | ~KRW 130,000 | KRW 423.9B | BUY consensus |

Three Scenarios + Five Trading Strategies for Jusung Engineering Stock

6–12 month scenarios: Bull 30% (KRW 180–190K) / Neutral 40% (KRW 130–150K range) / Bear 30% (KRW 80–100K). Neutral is the base case. Five trading rules:

- Three-tranche entry: One week apart. KRW 120,000 or below is the attractive entry zone.

- Max 5% portfolio weight: +433% in 52 weeks = extreme volatility stock.

- -10% stop-loss: Entry at KRW 130K → stop at KRW 117K.

- Staged profit-taking: 1/3 at KRW 150K / 1/3 at KRW 170K / 1/3 at KRW 190K (KIS target).

- D-day management: June 17 FOMC + August 7 Q2 earnings. Confirm earnings recovery before increasing weight.

Five key risks: ① 52-week +433% surge → heavy profit-taking overhang ② 98% semiconductor single-segment exposure ③ 80%+ China revenue exposure (US export control risk) ④ Wide broker target gap (4-broker avg KRW 50K vs KIS KRW 189K) ⑤ Q2 2026 loss continuation risk.