Korea market next week — US-Iran 60-day truce MOU close: oil, yields, KOSPI map and a five-step playbook

Trending · May 24, 2026 · DIR

A reported US-Iran 60-day truce MOU is close. For the Korea market next week, we trace how a free Strait of Hormuz reopening flows through oil → yields → KOSPI, list winners and at-risk sectors, lay out three scenarios, and a five-step playbook for Korean investors.

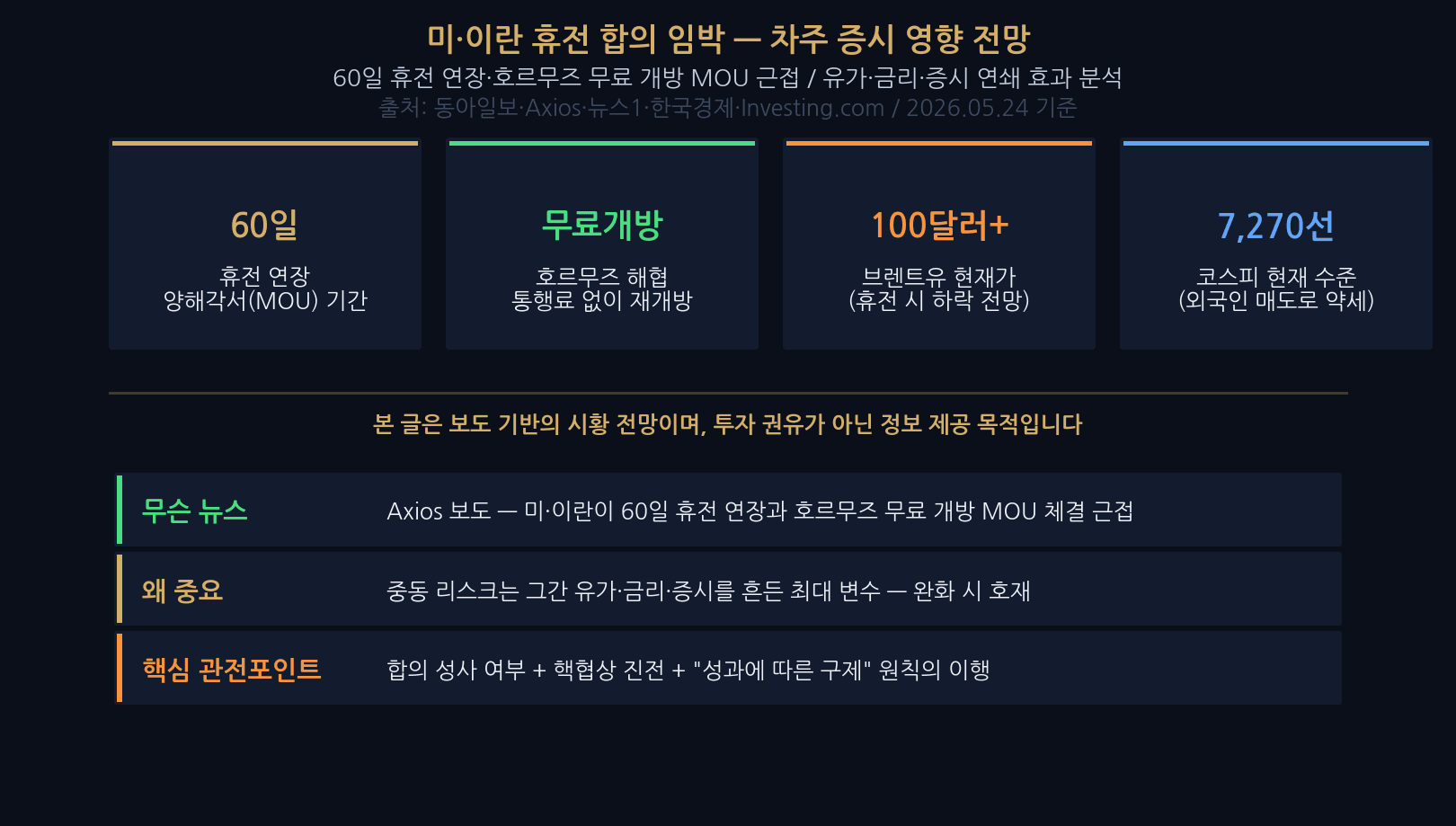

On May 23, 2026, the market got a noteworthy headline. US outlet Axios reported that the US and Iran are close to a 60-day truce extension and a free reopening of the Strait of Hormuz. The two sides plan to sign a Memorandum of Understanding (MOU); the core is Iran clearing mines while the US lifts its port blockade.

Middle East risk has been the dominant variable for oil, yields, and equities. So what does this mean for the Korea market next week? We trace the truce-to-market transmission, highlight winners and at-risk sectors, lay out three scenarios, and outline a Korean-investor playbook. Primary sources: Axios and Investing.com.

The deal — what is in it

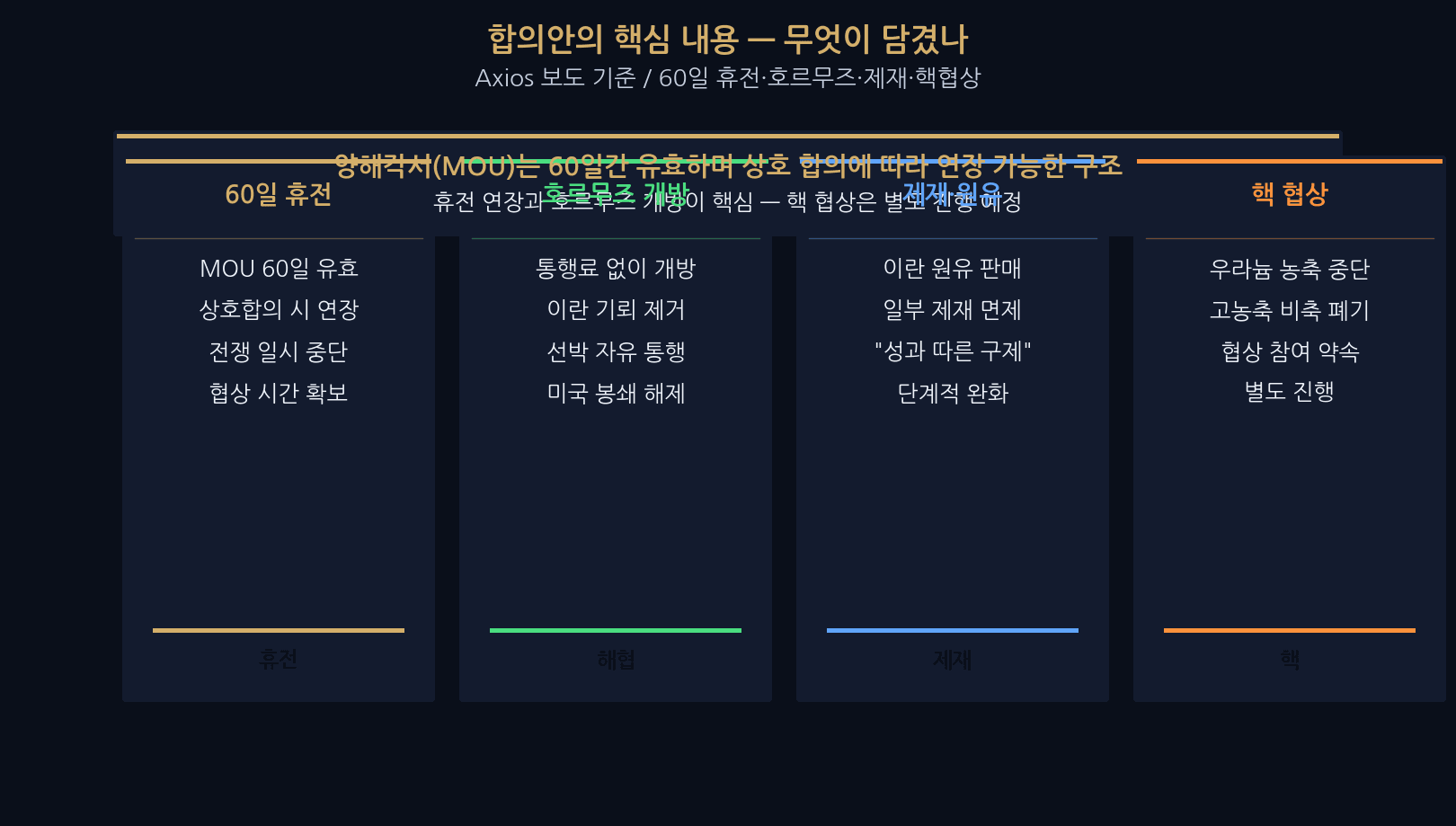

First the reported contents. On May 23, Axios — citing multiple US officials — reported the two sides are close to a 60-day truce extension and a toll-free reopening of the Strait of Hormuz.

The structure runs like this: an MOU valid for 60 days with mutual extension; the Strait reopens with no transit toll; Iran clears mines; in exchange, the US lifts the blockade on Iranian ports and grants some sanctions relief. The nuclear track reportedly includes a uranium-enrichment pause and a commitment to negotiate.

| Item | Reported content |

|---|---|

| Truce length | 60-day MOU, mutual extension possible |

| Hormuz | Toll-free reopening, Iran mine-clearing |

| US actions | Lift Iran port blockade, partial sanctions relief |

| Oil | Iran free-selling of crude reportedly possible |

| Nuclear track | Enrichment pause, negotiation commitment |

The US and Iran are close to a 60-day truce extension and a toll-free reopening of the Strait of Hormuz.

— Axios (via Dong-A Ilbo) · May 23, 2026

Transmission to the Korea market next week

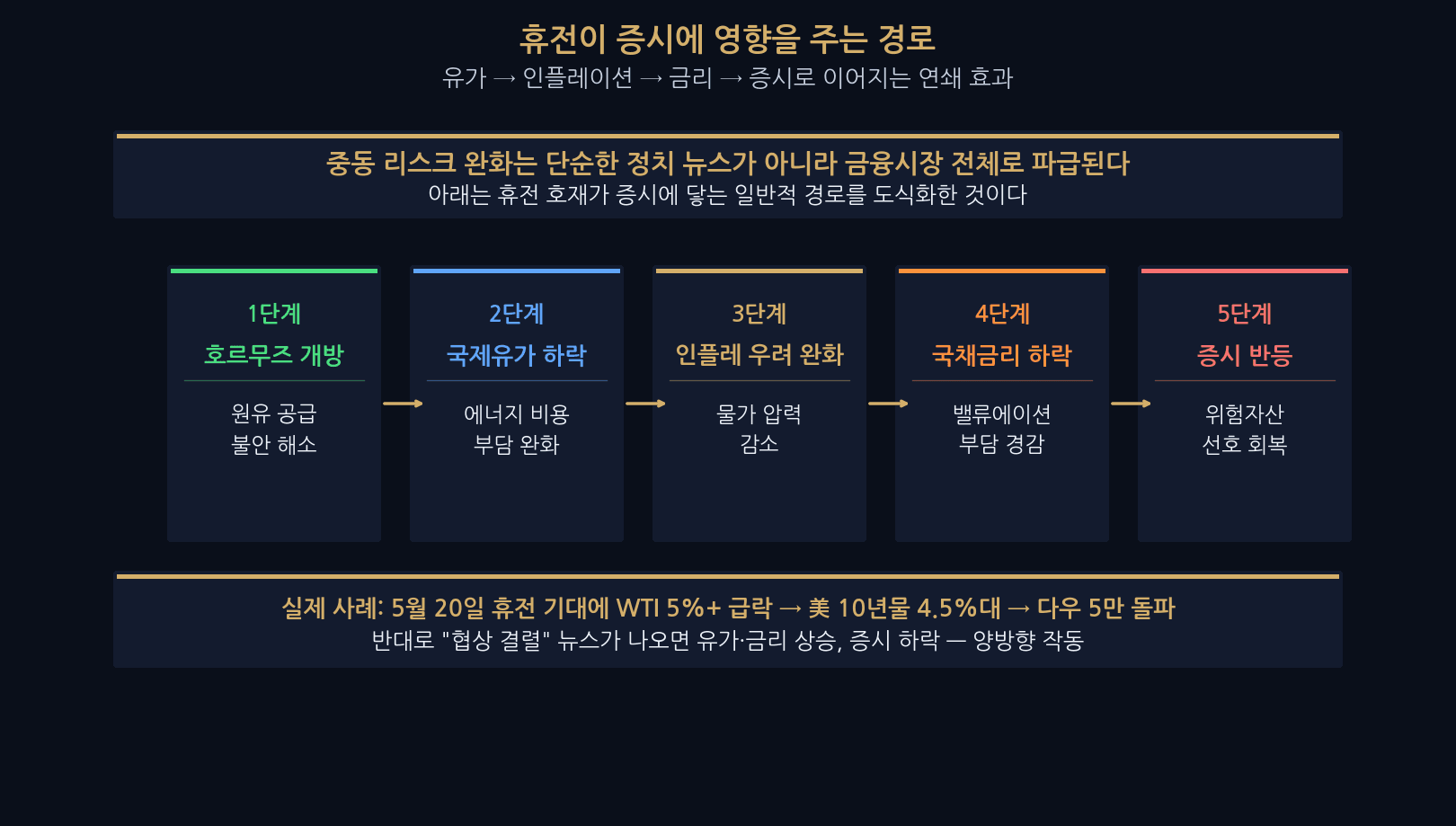

Why would a Middle East truce move Korean equities at all? The core chain is oil → inflation → rates → equities — the biggest macro pipeline shaping the Korea market next week.

If Hormuz opens up, supply anxiety eases and oil prices fall. Lower oil dampens inflation, which in turn cools rate-hike fears at central banks. Stable rates compress the valuation drag on equities and create room to rebound. On May 20, just the truce hope drove WTI down more than 5%, US 10-year yields back into the 4.5% area, and the Dow above 50,000.

| Stage | Mechanism | Market effect |

|---|---|---|

| 1. Hormuz reopens | Supply-anxiety eases | — |

| 2. Oil down | Energy costs ease | Inflation fears ↓ |

| 3. Rates stabilize | Treasury yields ease | Valuation drag ↓ |

| 4. Equity rebound | Risk-on returns | Upside room |

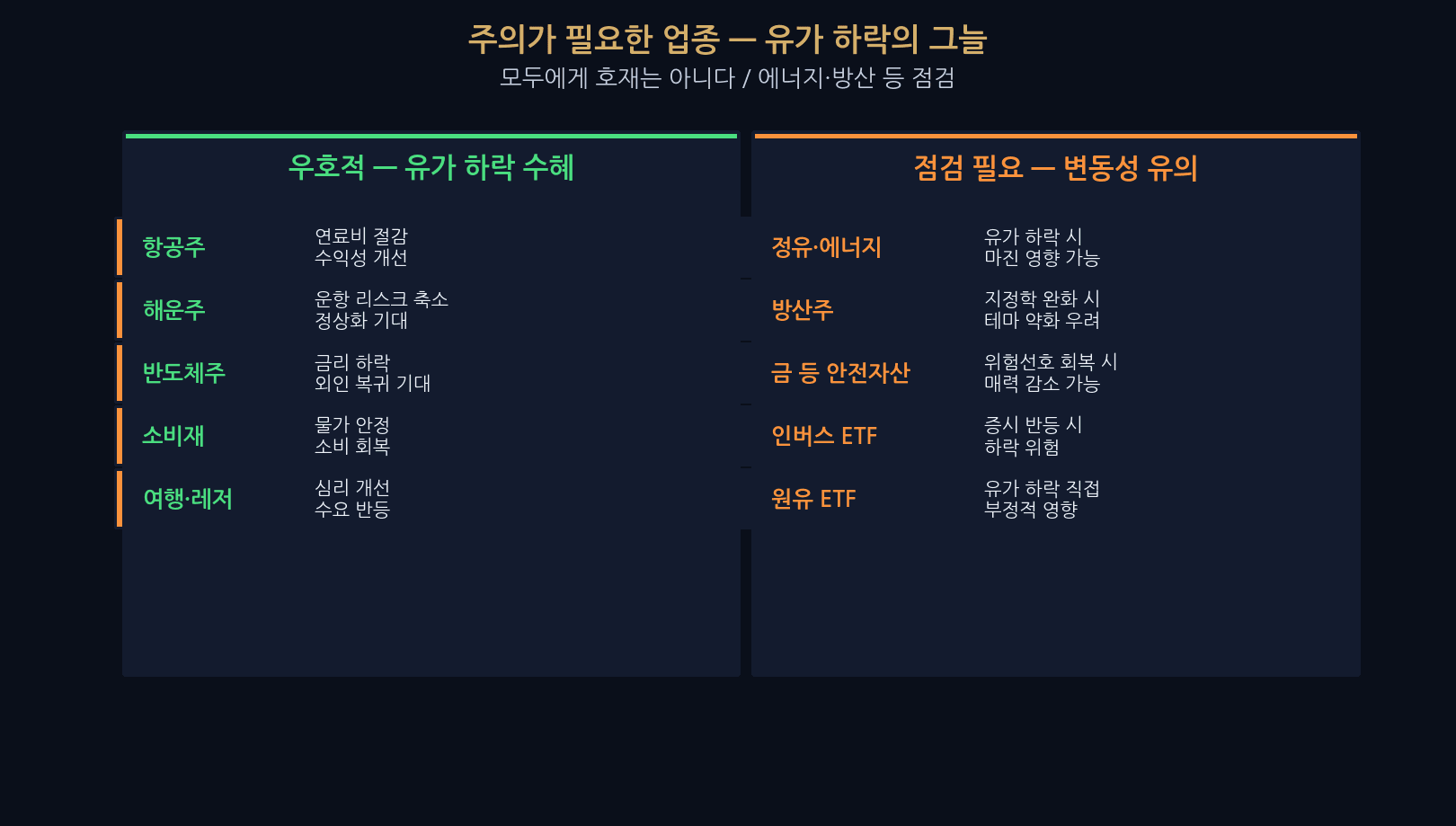

Likely winners if the truce holds

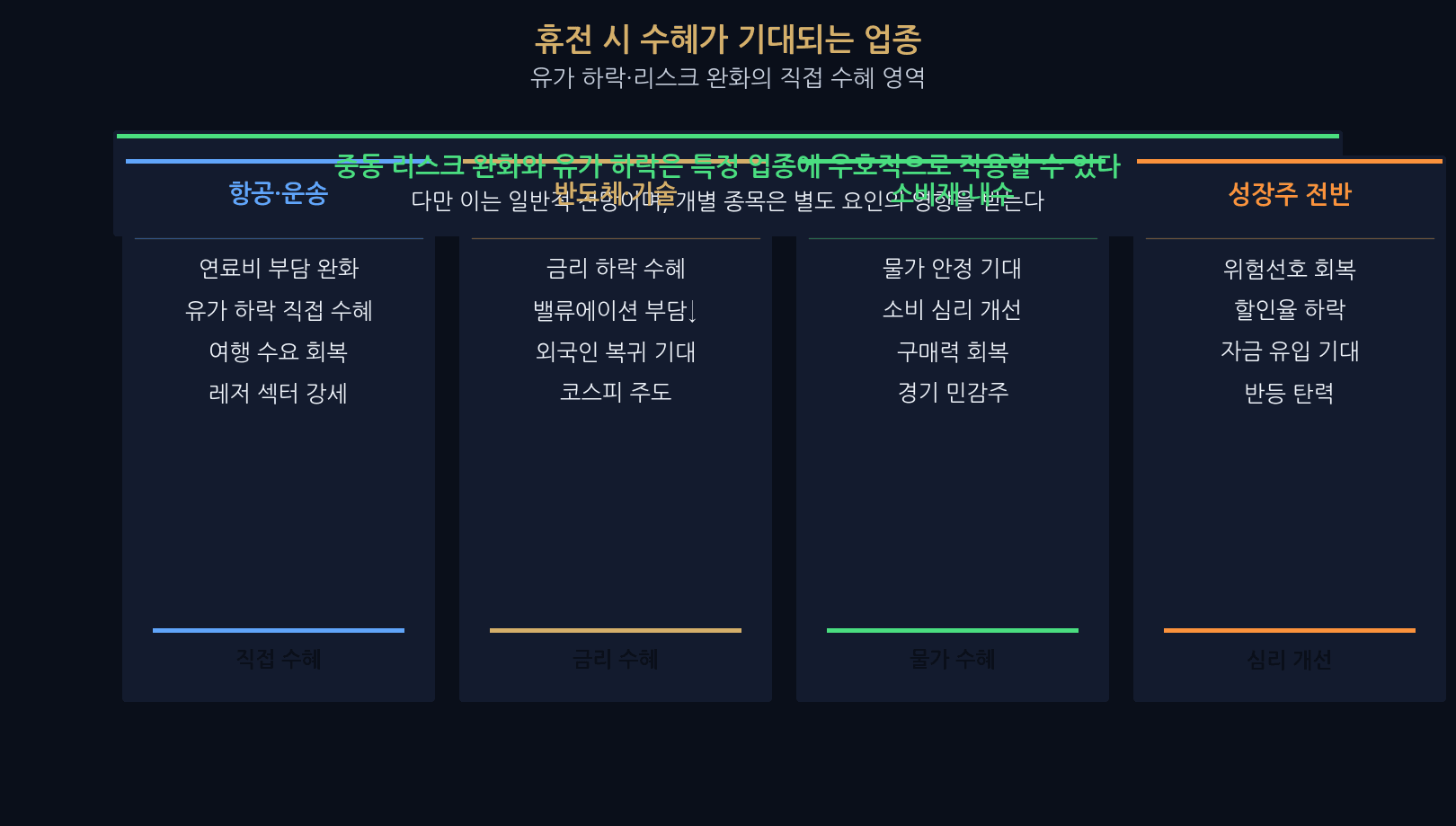

If the truce materializes, which sectors deserve attention? Typically direct beneficiaries of lower oil and risk normalization.

The most direct beneficiary is airlines/transport. Fuel is a large share of airline costs, so lower oil flows directly into margins. Semiconductors and tech benefit from lower rates, as the valuation drag on growth names eases. Cooling inflation also helps consumer and domestic-demand names. These are broad-stroke views — individual stocks still depend on earnings and idiosyncratic factors.

| Sector | Logic | Type |

|---|---|---|

| Airlines / transport | Fuel cost relief | Direct oil beneficiary |

| Semis / tech | Lower rates, less valuation drag | Rate beneficiary |

| Consumer / domestic | Cooling inflation, recovery | Price beneficiary |

| Growth broadly | Risk-on returns | Sentiment |

Where to be cautious — the other side of cheaper oil

Not every headline is good for everyone. A truce and lower oil can be a headwind for some.

Refiners and energy producers may see margin pressure from cheaper crude. Defense names may lose some of the geopolitical premium they have enjoyed. Safe havens like gold see fading appeal as risk-on returns. In particular, inverse equity ETFs and crude-tracking ETFs are exposed on the wrong side of a truce-positive backdrop. Check your portfolio’s directional fit.

| Item | Favorable | Re-check |

|---|---|---|

| Representative | Airlines · semis · consumer | Refiners · defense · gold |

| Logic | Lower oil & rates | Geopolitical de-risking fades |

| ETFs | KOSPI / chip ETFs | Inverse / crude ETFs |

| Action | Scale in | Re-check size and direction |

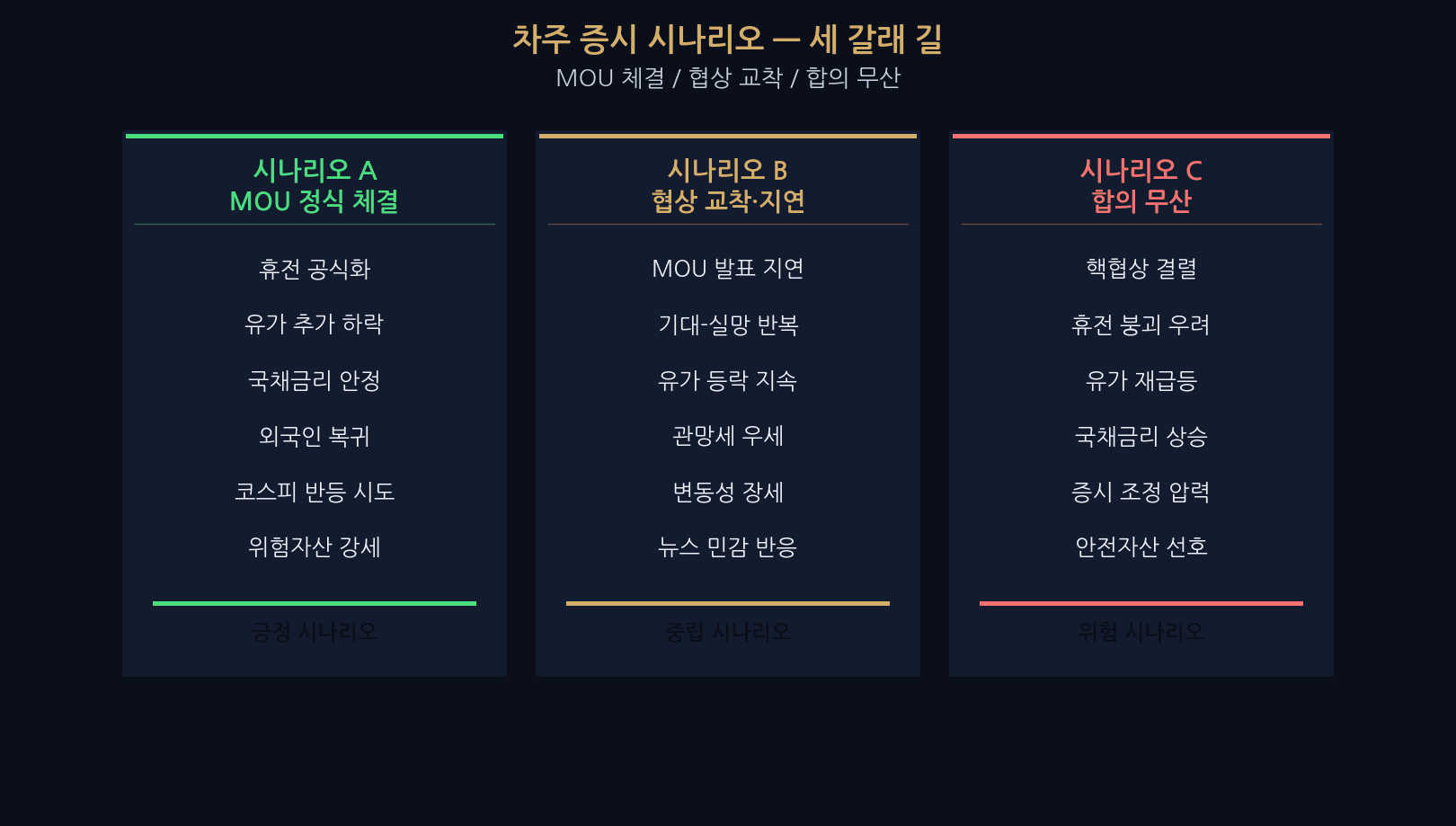

Three scenarios for the Korea market next week

Depending on how US-Iran talks land, the Korea market next week broadly splits into three scenarios.

Scenario A: MOU signed. A formal truce drives oil lower, foreign capital returns, and KOSPI attempts a rebound. Scenario B: stalemate. The MOU rollout is delayed, with hope-then-disappointment dynamics fueling a choppy tape. Scenario C: deal collapses. If nuclear talks break down, oil spikes back, and equities face downside pressure. US officials have noted the deal could fall apart inside 60 days if Iran is not serious about negotiations.

| Scenario | Setup | Equity impact |

|---|---|---|

| A. MOU signed | Formal truce, oil down | Rebound attempt |

| B. Stalemate | Delays, hope-then-disappointment | Choppy tape |

| C. Deal collapses | Nuclear talks break | Drawdown pressure |

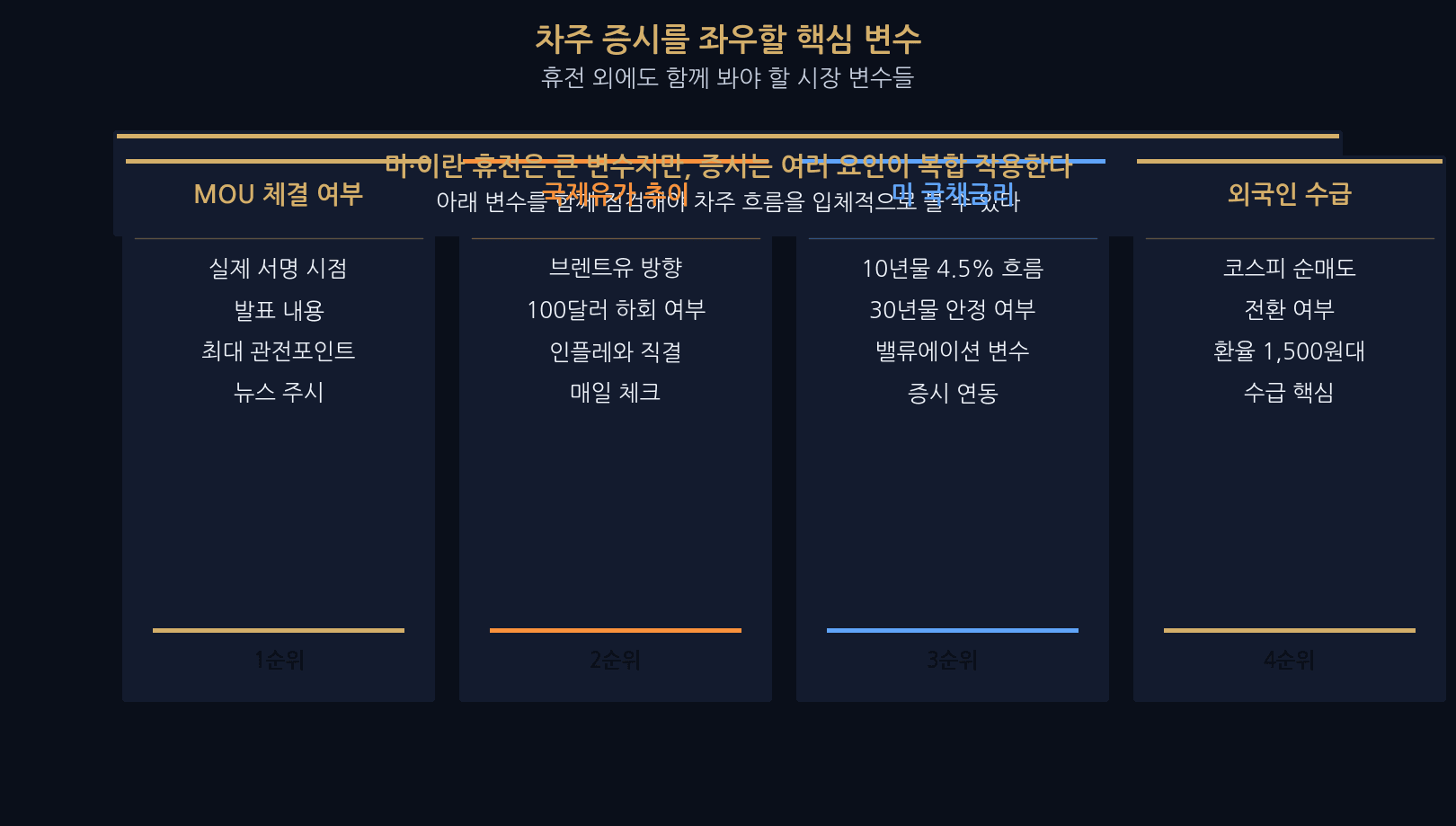

Key variables to watch

US-Iran is the biggest variable next week, but markets move on a mix of factors. Beyond the truce, here is what else to track.

Top priority is whether the MOU actually gets signed. “Close” is not “signed” — watch the actual signature timing and contents. Second is oil — whether Brent slips back below $100. Third is US Treasury yields, fourth is foreign flow into Korea. The key to a rebound is whether KOSPI’s foreign net-selling flips to net-buying, and whether USD/KRW stabilizes from the 1,500 area.

| Priority | Variable | What to watch |

|---|---|---|

| 1 | MOU signed? | Actual signature and contents |

| 2 | Oil | Brent below $100? |

| 3 | US Treasury yields | 10Y around 4.5% |

| 4 | Foreign flows | Net-buy switch; FX stabilization |

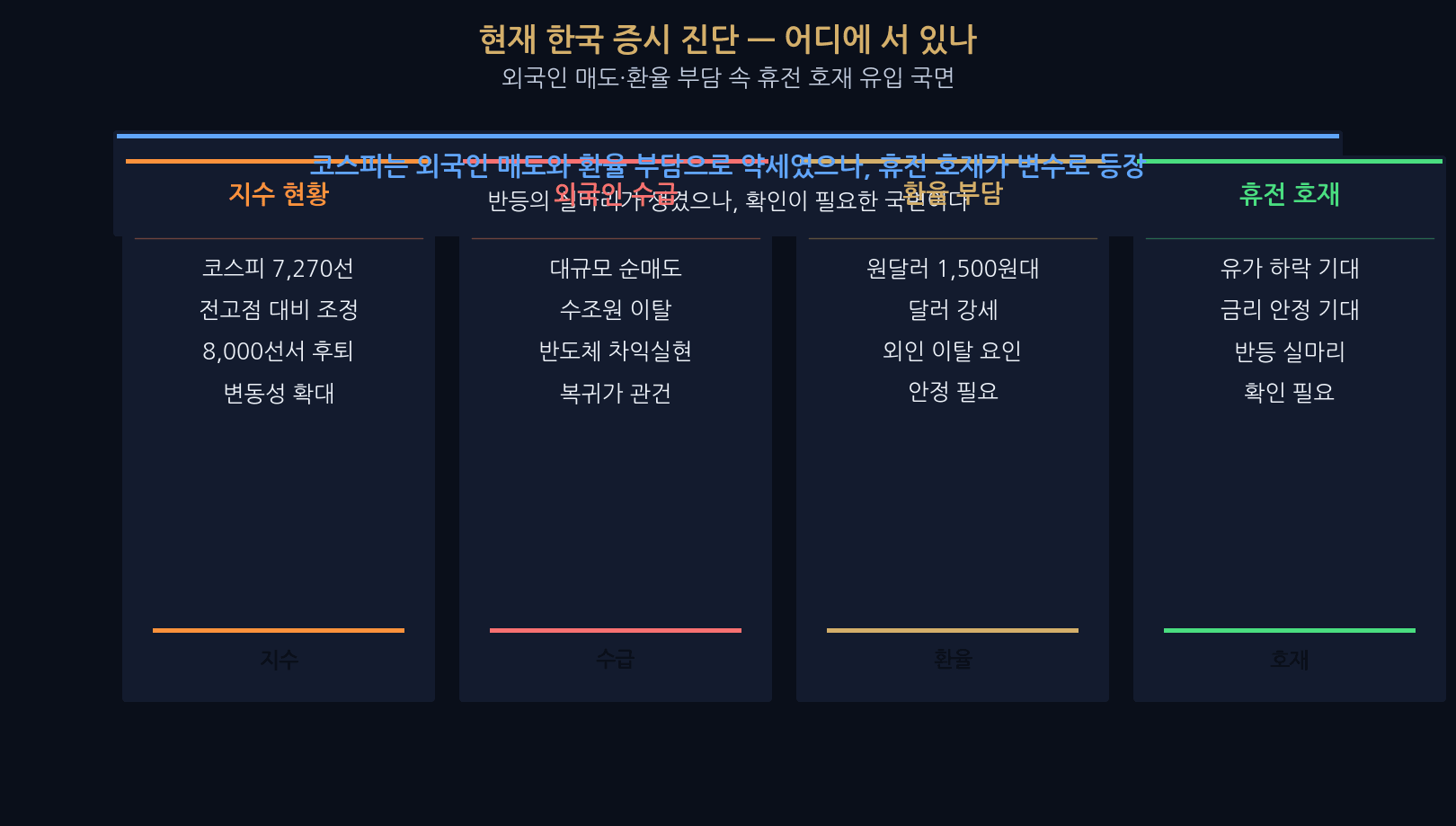

Where the Korean market stands today

Before discussing the truce upside, where does the market sit now? KOSPI flirted with 8,000 but has been pushed back to around 7,270 by heavy foreign selling and FX pressure.

Foreigners have net-sold in the trillions of won, with profit-taking heavy in the previously surging semis. USD/KRW pushed back into the 1,500 area, reinforcing outflows. It is into this softness that the truce headline lands. The seed of a rebound is there, but it needs confirmation — actual foreign re-buying and FX stabilization.

| Item | Status |

|---|---|

| KOSPI | ~7,270; correction off the high |

| Foreign flow | Large net selling persists |

| USD/KRW | 1,500 area; USD strength |

| Truce headline | Rebound seed — needs confirmation |

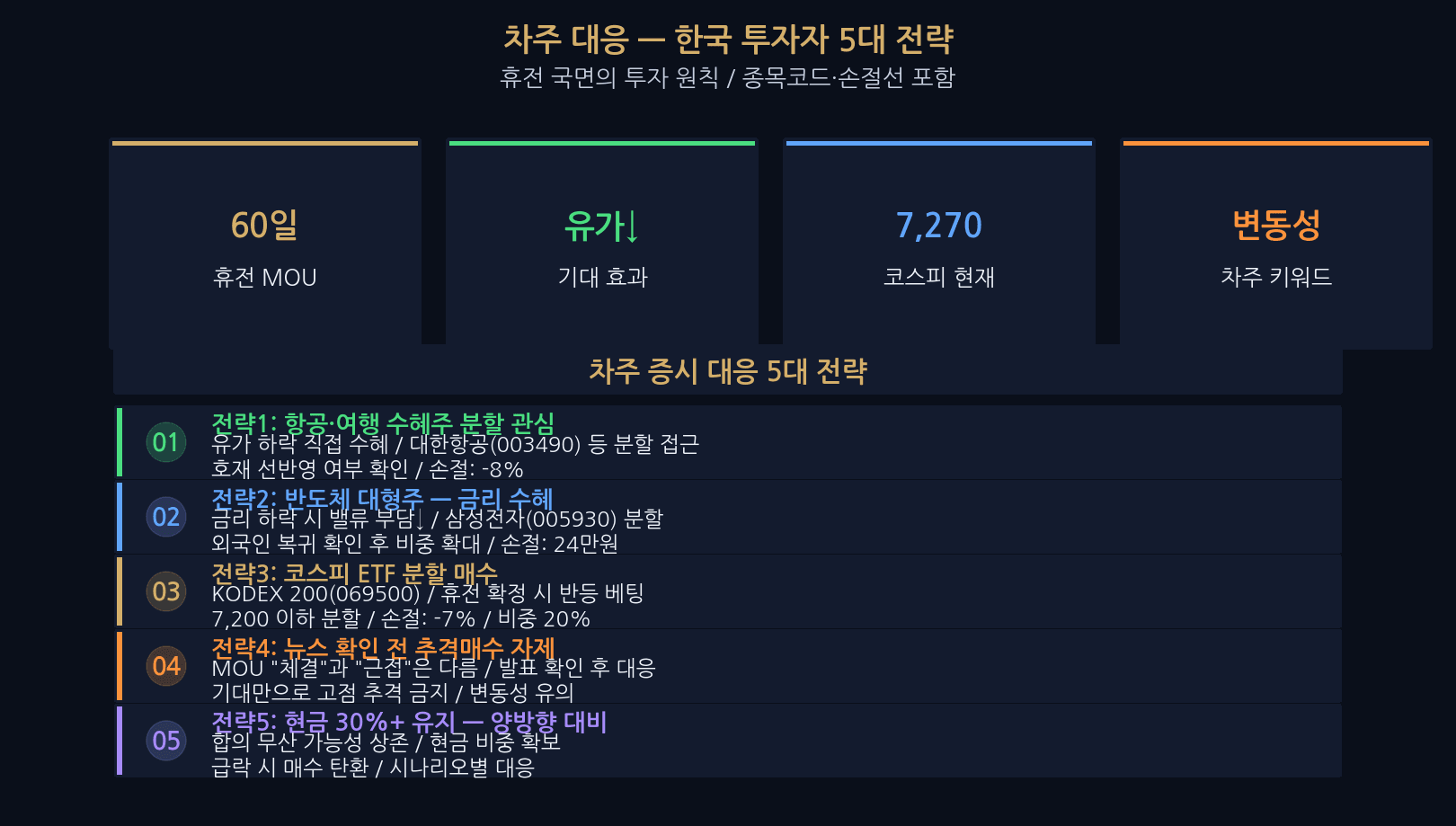

Five moves for Korean investors

| Move | Name | Code | How | Stop | Weight |

|---|---|---|---|---|---|

| 1. Airlines / travel | Korean Air | 003490 | Scale into oil-down beneficiary | -8% | 8% |

| 2. Large-cap semis | Samsung Electronics | 005930 | Rate beneficiary + foreign re-buy | KRW 240K | 15% |

| 3. KOSPI ETF | KODEX 200 | 069500 | Buy below 7,200 in tranches | -7% | 20% |

| 4. No chasing | Watch news | — | Act after MOU signature | — | Watch |

| 5. Cash buffer | Cash | — | Scenario-based response | — | 30%+ |

□ If truce holds, lean toward airlines / semis / consumer; re-check refiners / defense / inverse

□ Track Brent vs $100 daily

□ Watch US 10Y around 4.5% and a foreign net-buy flip

□ Prepare for scenario C (deal collapse) — keep 30%+ cash

□ No chasing single headlines — scale in, use stops

Sources

- Dong-A Ilbo — “US-Iran close to 60-day truce extension and free Hormuz reopening” (May 24, 2026)

- Axios — US-Iran ceasefire extension and Strait of Hormuz reopening (May 23, 2026)

- News1 — Trump “puts Iran strike on hold” and oil calms (May 19, 2026)

- Hankyung / Newspim — KOSPI foreign-flow and FX market notes (May 2026)

- Investing.com — Truce expectations and equity analysis (May 2026)

This article is a market view based on reported facts and does not recommend any specific security. Market views carry uncertainty; actual markets can move differently due to many variables. Investors bear sole responsibility for their decisions.