W1 — Circle (CRCL) Stock Analysis: USDC $77B, ARC Token $222M, Q1 EPS +72% Beat

W Insights · Stock Analysis

W1 — Circle (CRCL) Stock Analysis: USDC $77B, ARC Token $222M, Q1 EPS +72% Beat

Circle CRCL stock analysis: From a $31 IPO to $298.99 peak — now trading at $122. We break down Q1 2026 earnings, USDC circulation dynamics, ARC Token presale, and whether the Clarity Act changes the long-term thesis.

“USDC volume hit $21 trillion in Q1 — up 263% year-over-year. The infrastructure is scaling. The question is whether regulation and rates align in time.”

W Editorial Desk

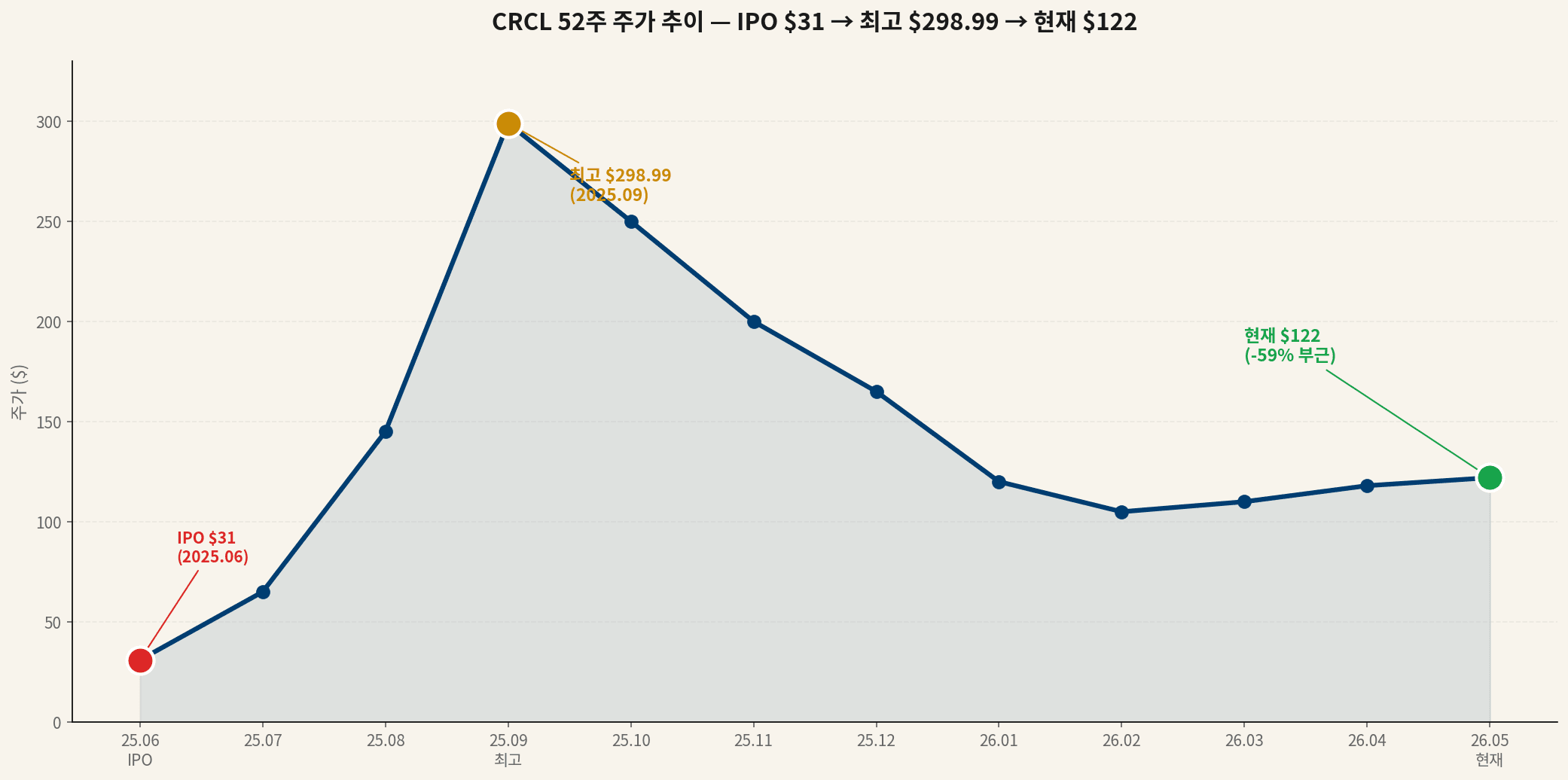

01Price History: $31 IPO → $298.99 → $122

Circle Internet Financial (NASDAQ: CRCL) went public in June 2025 at $31 per share. The IPO was cautiously received — Circle had attempted to go public via SPAC in 2022 before that deal collapsed amid a broader crypto downturn. The direct listing in 2025 was a clean second chance.

What followed was one of the most compressed rallies in recent fintech history. By September 2025, CRCL had reached its 52-week high of $298.99 — an 864% gain in roughly three months. The catalyst was a combination of USDC momentum, renewed institutional interest in stablecoins, and early signals that stablecoin legislation was finally gaining real traction in Washington.

Today, CRCL trades around $122 — down 59% from its peak but still up nearly 4× from IPO. That’s not a broken story; it’s a stock finding its post-euphoria equilibrium. The question is whether $122 represents a floor, a fair value, or a plateau before the next leg.

Key Price Levels: IPO $31 (Jun 2025) · 52-week low ~$100 · Current $122 · 52-week high $298.99 · Avg analyst target $127.59

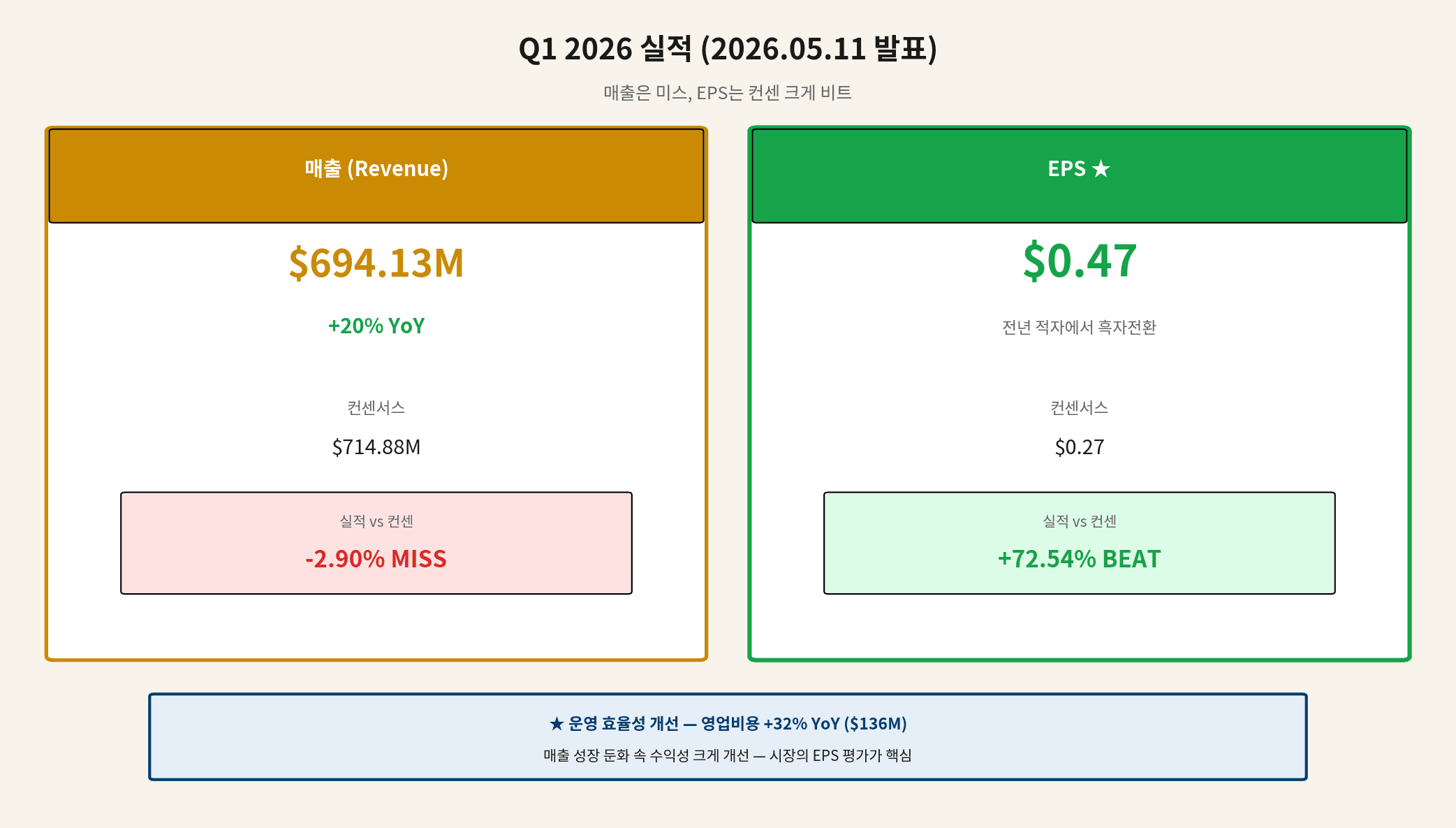

02Q1 2026 Earnings: Revenue Miss, EPS Beat

Circle reported Q1 2026 results that handed investors a split verdict: revenue came in slightly below expectations while earnings-per-share delivered a meaningful upside surprise.

| Metric | Actual | Consensus | vs. Estimate |

|---|---|---|---|

| Revenue | $694M | ~$715M | −2.9% miss |

| EPS (diluted) | $0.47 | $0.27 | +72.54% beat |

| USDC Transaction Volume | $21T (YoY) | — | +263% YoY |

| USDC Circulation | $77B | — | 40% CAGR guided |

The revenue miss is almost entirely explained by the interest rate environment. Circle’s primary revenue stream is the yield earned on USDC reserves — predominantly short-duration US Treasuries and repo agreements. As the Fed held rates and market expectations shifted toward eventual cuts, the carry on those reserves compressed slightly relative to analyst models.

The EPS beat, however, signals meaningful operational leverage. Circle has been aggressive about cost structure since the IPO, and the $0.47 print versus $0.27 consensus suggests management is running tighter than Wall Street anticipated. That’s a constructive sign for margin expansion as USDC scales.

Takeaway: The EPS beat (+72.54%) matters more than the revenue miss (−2.9%). Operational efficiency is improving. Revenue trajectory depends on USDC growth rate and Fed policy — not things Circle controls directly.

03USDC: $77B Circulation, 80% of the US Digital Dollar Market

USDC is Circle’s moat. With $77 billion in circulation, USDC commands roughly 80% of the US digital dollar market — the segment of stablecoins that is dollar-denominated, regulated, and primarily adopted by institutional and enterprise users rather than crypto-native traders.

That $21 trillion in Q1 transaction volume — up 263% year-over-year — reflects actual on-chain economic activity, not just circulating supply. Payments, settlements, cross-border transfers, and DeFi protocols are all routing through USDC rails at a pace that has fundamentally changed what Circle is: it’s no longer a crypto company with a stablecoin product. It’s becoming payment infrastructure.

Management is guiding for 40% CAGR in USDC circulation. To contextualize: at that rate, USDC would cross $100B in circulation within roughly 18 months. Whether that’s achievable depends on the Clarity Act (see Section 05) and whether institutional adoption continues accelerating or plateaus.

The critical structural risk: Circle’s revenue is almost entirely driven by interest earned on the Treasury securities and repo agreements backing USDC. Every 25bp Fed rate cut reduces Circle’s annual reserve income by approximately $190M at current circulation levels. USDC growth needs to outpace rate compression for revenue to grow.

Rate Sensitivity: Circle’s revenue = USDC supply × Fed funds rate × reserve yield. Growth in USDC circulation must exceed rate cut headwinds for top-line expansion. Current guided 40% CAGR provides a meaningful buffer against moderate easing cycles.

04ARC Token: $222M Presale, a16z Lead, $3B FDV

The most speculative — and potentially high-upside — element of the Circle story is ARC: a Layer-1 blockchain specifically architected for USDC-native payments. The presale has raised $222 million, with Andreessen Horowitz (a16z) leading the round. The fully diluted valuation (FDV) is priced at $3 billion.

ARC is designed to solve a specific problem: existing blockchains (Ethereum, Solana, etc.) are general-purpose. USDC payments on those chains compete for block space with DeFi, NFTs, gaming, and everything else. ARC would be purpose-built for stablecoin settlement — lower latency, predictable fees, compliance-native architecture.

The strategic logic is clear: if USDC is Circle’s product, ARC is the owned infrastructure layer beneath it. Rather than paying fees to Ethereum validators or Solana block producers, Circle would capture that value through the ARC network. At $21T in annual volume, even fractional basis-point fees represent enormous revenue potential.

Watch: ARC mainnet launch timing is a key catalyst. Until live, it’s a presale narrative. Once deployed and processing real USDC volume, it becomes a revenue story. The $222M raise with a16z backing provides credibility, but execution risk is real for any new L1.

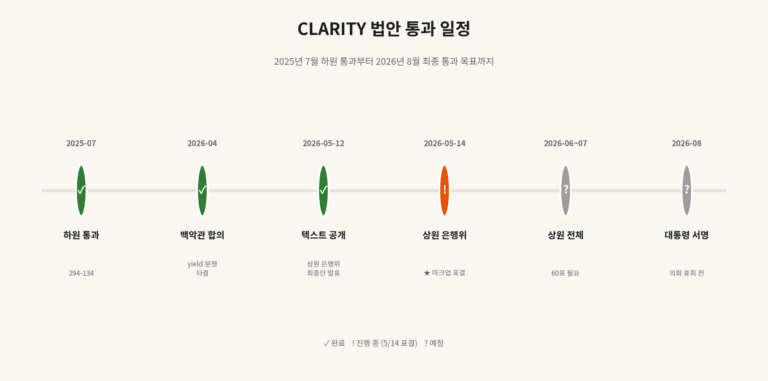

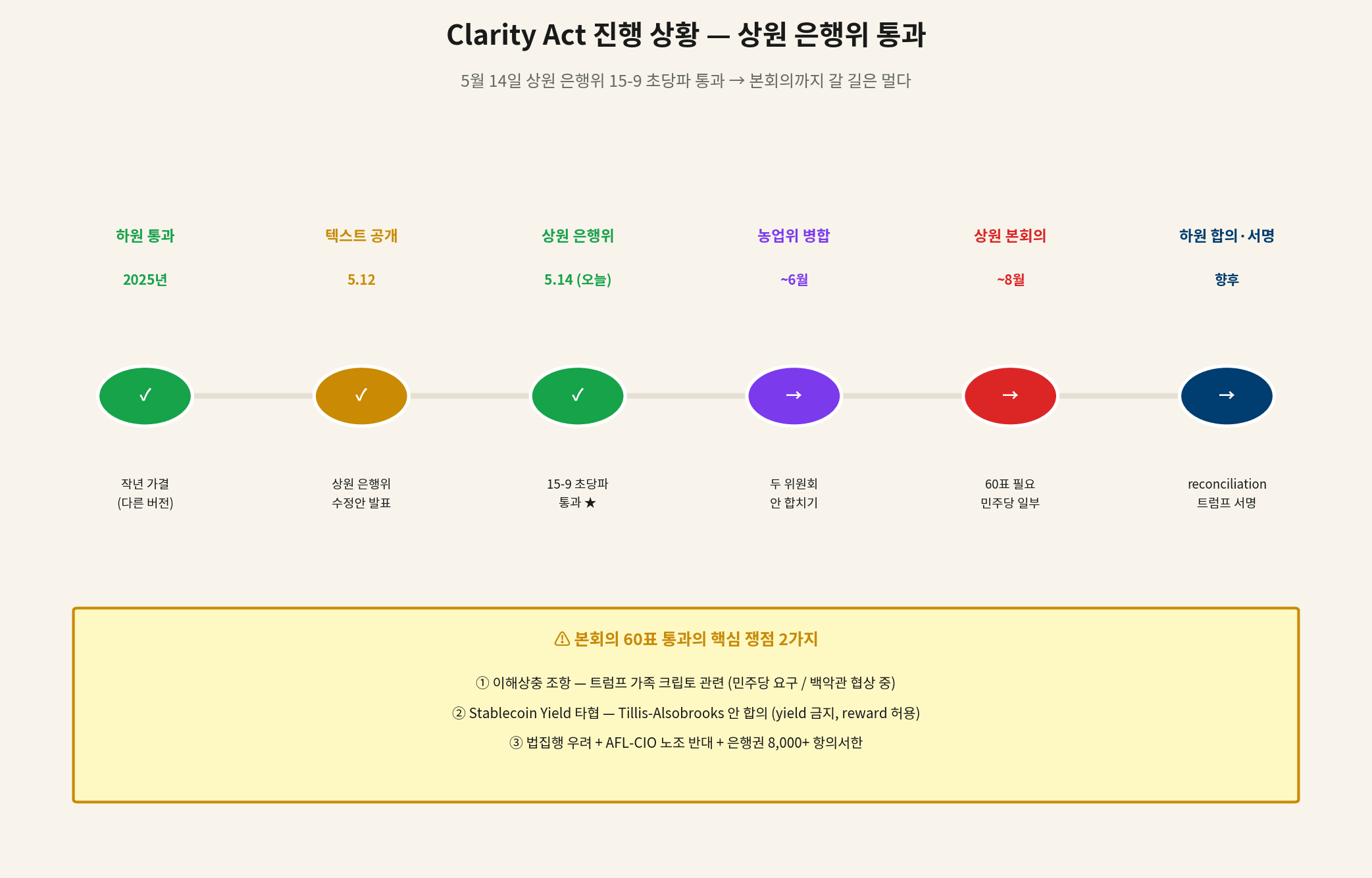

05Clarity Act: Senate Committee Passes 15-9, Floor Vote Next

On May 14, 2026, the Senate Banking Committee passed the Clarity Act 15-9 — a bipartisan vote that represents the most significant legislative progress on stablecoin regulation in US history. Circle’s Chief Strategy Officer, Dante Disparte, called it “meaningful bipartisan progress” and emphasized that the bill provides regulatory certainty that the industry has been operating without for years.

But the committee vote is not the finish line. The path to law still requires:

- Senate floor vote — needs 60 votes to overcome a filibuster (currently estimated at roughly August 2026)

- House reconciliation — the House has its own competing stablecoin bill language

- Presidential signature — the Trump administration has signaled support in principle

The 60-vote threshold is the critical hurdle. With a 15-9 committee vote (roughly 63% support), the math is close but not certain to translate to the full chamber. A handful of undecided senators — particularly those from states with large financial services industries — will determine whether this becomes law in 2026.

If the Clarity Act passes in its current form, it would establish federal licensing for stablecoin issuers, mandate 1:1 reserve backing with high-quality liquid assets, and preempt a patchwork of state-level regulations. For Circle, it would be the single largest regulatory catalyst since USDC’s launch — providing institutional clarity that could unlock adoption from banks, payment processors, and global corporates that have been waiting on the sidelines.

For more coverage of the legislative process, see CNBC’s ongoing reporting on the Clarity Act.

Legislative Status (May 14, 2026): Senate Banking Committee ✓ 15-9 · Senate Floor (60 votes needed) — pending, est. Aug 2026 · House Reconciliation — pending · Presidential Signature — pending

06Analyst Price Targets: $127.59 Average, $200 Bull Case

Wall Street coverage on CRCL has expanded rapidly since the IPO. Here’s where the major voices stand:

| Firm | Price Target | Rating | Implied Upside from $122 |

|---|---|---|---|

| Needham | $150 | Buy | +23% |

| Mizuho | $135 | Outperform | +11% |

| Wall St. Average | $127.59 | — | +5% |

| Manhattan Crypto (bull) | $200 | Strong Buy | +64% |

The consensus target of $127.59 suggests the stock is essentially fairly valued at current levels — a modest 5% upside baked into the average. Needham at $150 and Mizuho at $135 represent the more constructive institutional views, premised on continued USDC growth and eventual Clarity Act passage.

Manhattan Crypto’s $200 bull case is an outlier, but it’s not irrational. It models a scenario where USDC circulation accelerates toward $110B by end of 2026, ARC achieves meaningful mainnet adoption, and the Clarity Act passes — unlocking the institutional adoption wave that has been deferred by regulatory uncertainty. At $200, Circle would trade at roughly 13× projected 2027 revenue, which is aggressive but not unprecedented for high-growth fintech infrastructure with network effects.

07Bull vs. Bear: What Changes the Thesis

CRCL is a binary-outcome stock in many respects — the upside and downside cases are driven by discrete, identifiable variables rather than gradual drift. Here’s the framework:

BULL CASE → $150–$200

- USDC circulation accelerates past $100B

- Clarity Act passes Senate floor (60 votes)

- ARC mainnet launches, captures volume share

- Fed holds rates steady through 2026

- Enterprise/bank USDC adoption unlocks

BEAR CASE → $100

- Fed cuts rates aggressively (reserve income collapses)

- Tether (USDT) expands into regulated US markets

- Banks launch competing proprietary stablecoins

- Clarity Act stalls or passes with unfavorable terms

- ARC execution fails; development delays mount

The bear case at $100 implies the market prices Circle purely as a rate-sensitive vehicle with a 40% discount from current levels. That’s plausible if the Fed begins an aggressive easing cycle before USDC growth offsets the revenue compression. The bull case at $150–$200 requires multiple catalysts aligning — not impossible, but dependent on external variables Circle cannot control.

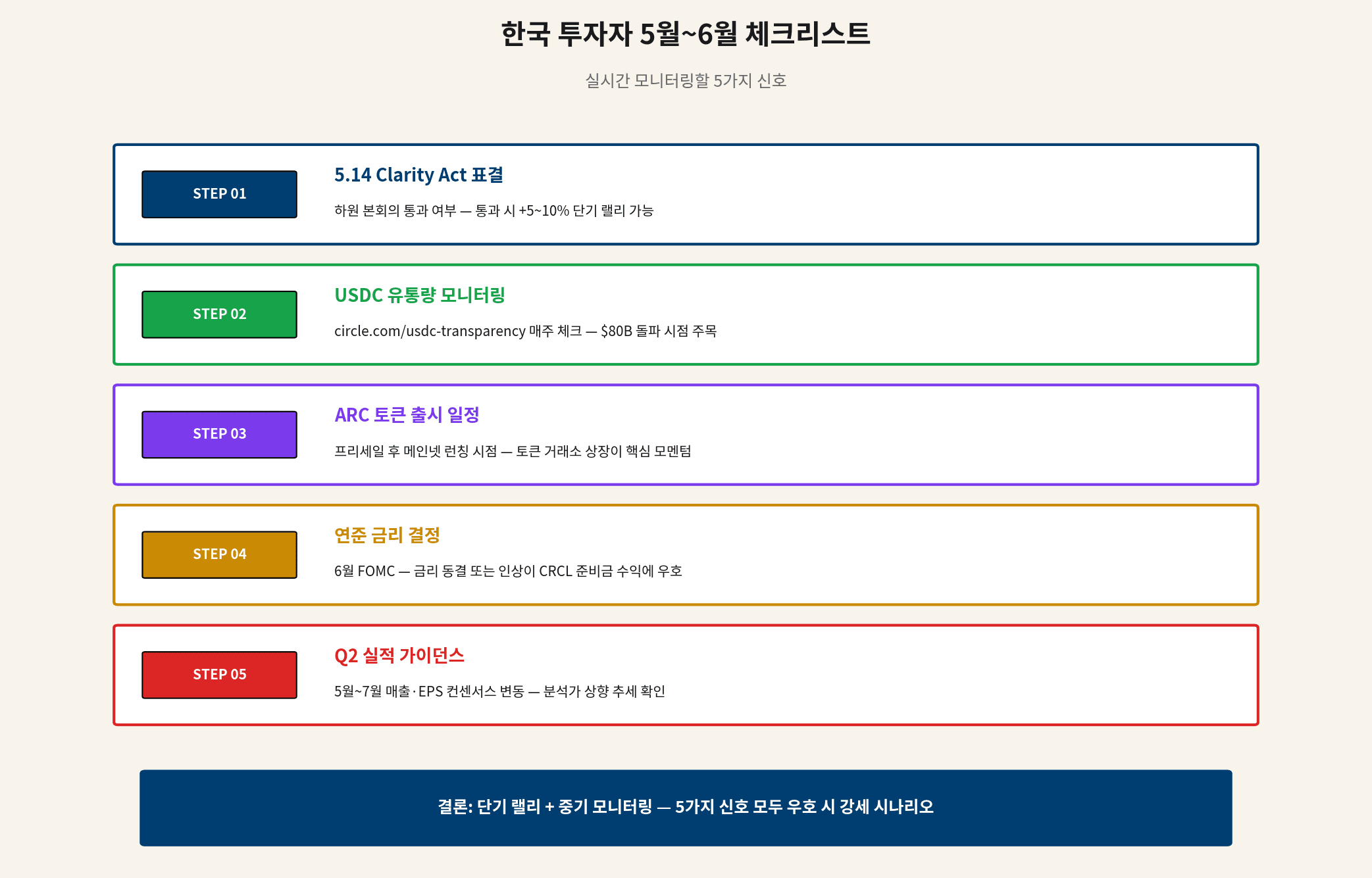

085 Signals to Monitor — The CRCL Checklist

Rather than watching the stock price daily, track these five variables. They’re the actual inputs that determine where CRCL goes from here:

| # | Signal | What to Watch | Key Threshold |

|---|---|---|---|

| 1 | Senate 60-Vote Count | Undecided senators on Clarity Act floor vote | 60+ confirmed “yes” votes → major catalyst |

| 2 | USDC Transparency Tracker | Circle’s monthly attestation data (circulation) | $80B crossing = validates 40% CAGR guidance |

| 3 | ARC Mainnet Launch | Developer announcements, testnet → mainnet timeline | Mainnet + first $1B USDC routed = proof of concept |

| 4 | June FOMC Decision | Fed rate decision and forward guidance language | Cut + dovish guidance = headwind; hold = neutral |

| 5 | Q2 2026 Guidance | Management outlook on USDC growth and margins | Revenue guidance beat signals volume offsetting rate risk |

Strategy note: At $122, CRCL is trading near the Wall Street consensus target of $127.59. That’s not a screaming buy or a clear sell — it’s a stock fairly priced for the base case, with asymmetric upside if the Clarity Act passes and ARC delivers. Dollar-cost averaging into a position rather than making a lump-sum bet is the appropriate approach given the binary legislative risk ahead.

Position Framework: Current $122 ≈ consensus fair value. Dollar-cost average on dips toward $100. Add conviction on: Clarity Act floor progress + USDC crossing $80B. Trim/reassess on: aggressive Fed easing cycle beginning before USDC growth offsets.

Bottom Line

Circle (CRCL) is a structurally sound business facing a crossroads defined by three forces it doesn’t fully control: Federal Reserve rate policy, the US legislative calendar, and the competitive dynamics of the global stablecoin market. The Q1 earnings showed that the core USDC engine is working — 263% volume growth, 72% EPS beat, improving operational leverage. The Clarity Act is closer to law than it has ever been. ARC adds a long-term optionality layer that is either transformative or a footnote, depending on execution.

At $122, the stock prices in the base case but not the upside scenarios. For investors with a 12–18 month horizon and tolerance for legislative timing risk, the risk/reward is reasonable — particularly if sized as a position to be built over time rather than committed to all at once.

The Clarity Act vote count is now the single most important number for CRCL investors. Not the Fed funds rate. Not Q2 earnings. The vote count.

W Editorial Desk

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. All figures referenced are based on publicly available data as of May 14, 2026. Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal. Always conduct your own due diligence and consult a licensed financial advisor before making investment decisions. getdir.app and W Editorial are independent and have no financial relationship with Circle Internet Financial or any entity mentioned in this article.