W7 — BitMine BMNR ETH Treasury: mNAV 0.86 Discount, 100× Dilution Risk & Kerrisdale Short Report

W Insights · May 17, 2026 · ~8 min read

BitMine BMNR ETH treasury mNAV has collapsed from 2.5x to 0.86 — now trading at a discount to net asset value. Tom Lee’s BitMine (NYSE: BMNR) amassed 5.21 million ETH in just ten months to become the world’s largest Ethereum treasury, but share count exploded 100× in six months and shareholders approved a 50-billion-share authorized limit. Kerrisdale Capital is short with a 40%-plus downside target.

1. Company Overview — How the BitMine BMNR ETH Treasury Model Works

BitMine Immersion Technologies (NYSE: BMNR) was founded in 2019 as a Nevada/Connecticut-based blockchain company originally running immersion-cooled Bitcoin mining rigs. In June 2025 it pivoted entirely to an Ethereum treasury strategy, with Fundstrat CIO Tom Lee serving as Chairman. The company runs on a staff of just seven — a skeleton crew typical of treasury-holding vehicles.

The business model is the “MSTR playbook, ETH edition.” The virtuous cycle: ① trade at a premium to ETH NAV → ② issue shares at that premium → ③ buy more ETH → ④ increase ETH-per-share → ⑤ re-establish premium → repeat. The company calls its north star “The Alchemy of 5%” — accumulating 5% of all circulating ETH supply. It now holds 4.31%.

The flaw is obvious: the model only works while the mNAV premium holds. The BitMine BMNR ETH treasury mNAV has already fallen below 1.0, meaning buying BMNR shares today is mathematically worse than buying ETH outright — before accounting for the dilution risk from 50 billion authorized shares.

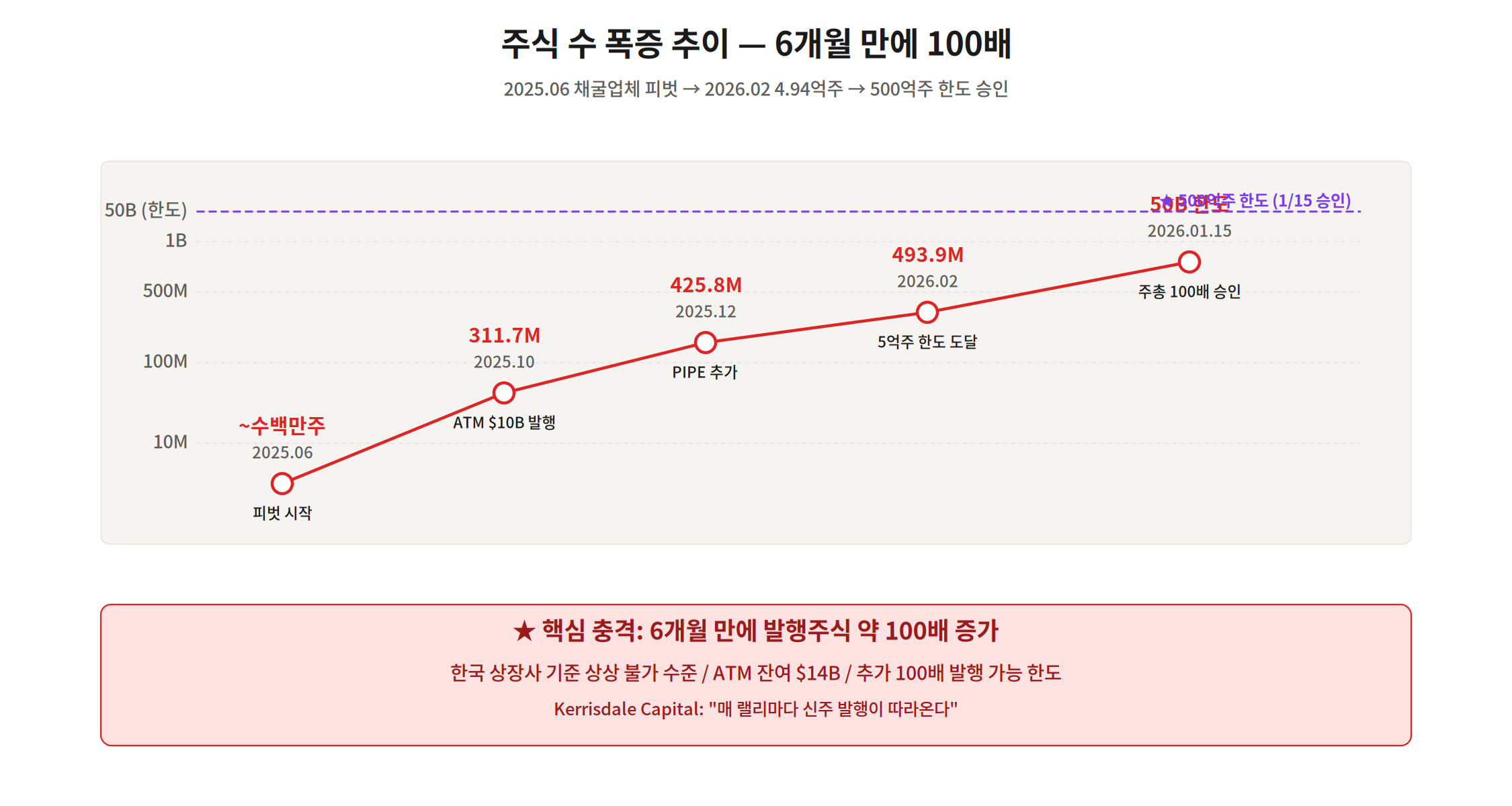

2. Share Count Explosion — 100× in Six Months

BMNR’s most startling feature is the velocity of share issuance. At the June 2025 pivot the float was in the single-digit millions. Eight months later it stood at roughly 500 million — a 100-fold increase. Then, at the January 2026 annual meeting, shareholders approved raising the authorized share limit from 500 million to 50 billion, another 100× expansion of potential dilution runway.

| Date | Shares Outstanding | Note |

|---|---|---|

| Jun 2025 (pre-pivot) | A few million | Small-cap miner |

| Oct 6, 2025 | 311.7M | $10B raised in 3 months |

| Dec 8, 2025 | 425.8M | +114M more shares |

| Feb 28, 2026 | 493.9M | Near cap limit |

| Jan 15, 2026 ★ | 50B authorized | 100× cap expansion approved |

By Korean market standards this would be immediate grounds for trading suspension. In the U.S., At-The-Market (ATM) offerings are fully legal — which is precisely why this structure is possible and why Korean retail investors may not fully appreciate the mechanics.

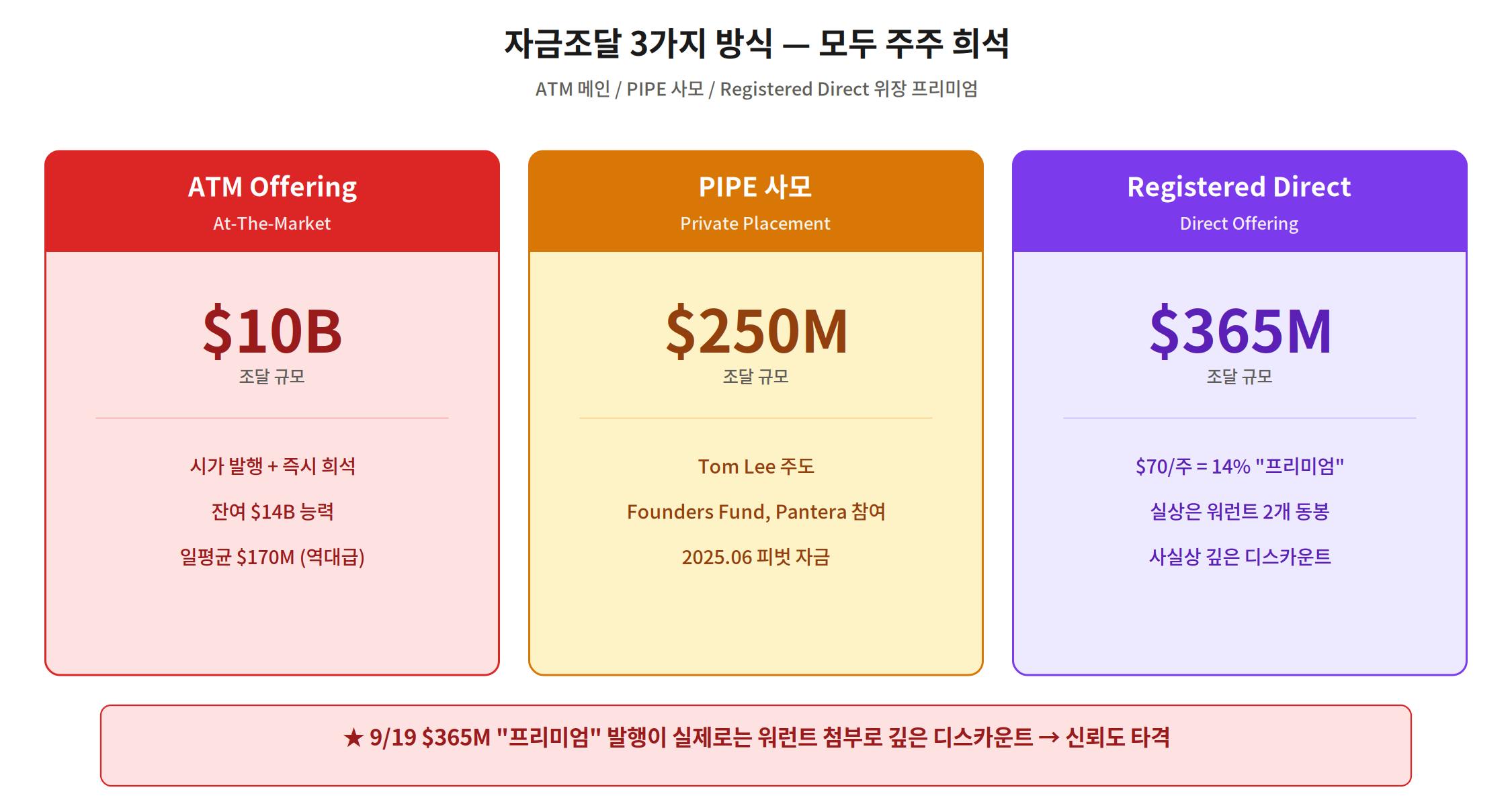

3. Three Fundraising Methods — All Dilutive

① ATM Offering (Primary) — $10B in 3 Months, $170M/day Average

BitMine’s main capital-raise channel is the At-The-Market program. Over three months it issued 240M+ shares raising $10 billion at an average daily rate of $170M — historically unprecedented. The August 11, 2025 prospectus supplement registered an additional 339M shares at $58.98, immediately diluting shareholders by $12.10/share. The remaining ATM capacity stands at approximately $14 billion.

② PIPE — Tom Lee’s $250M Seed

In mid-2025 BitMine completed a $250M private placement led by Tom Lee with participation from Founders Fund, Pantera Capital, and others. This was the seed capital that made the June 2025 pivot possible.

③ Registered Direct — A Disguised Discount

On September 19, 2025, BMNR raised $365M via direct offering at $70/share — 14% above the prior day’s close of $61.29, framed publicly as a “premium” raise. The reality: each share purchased came bundled with two warrants, making the effective price a substantial discount. Kerrisdale called it “a dilutive raise dressed up as a premium.”

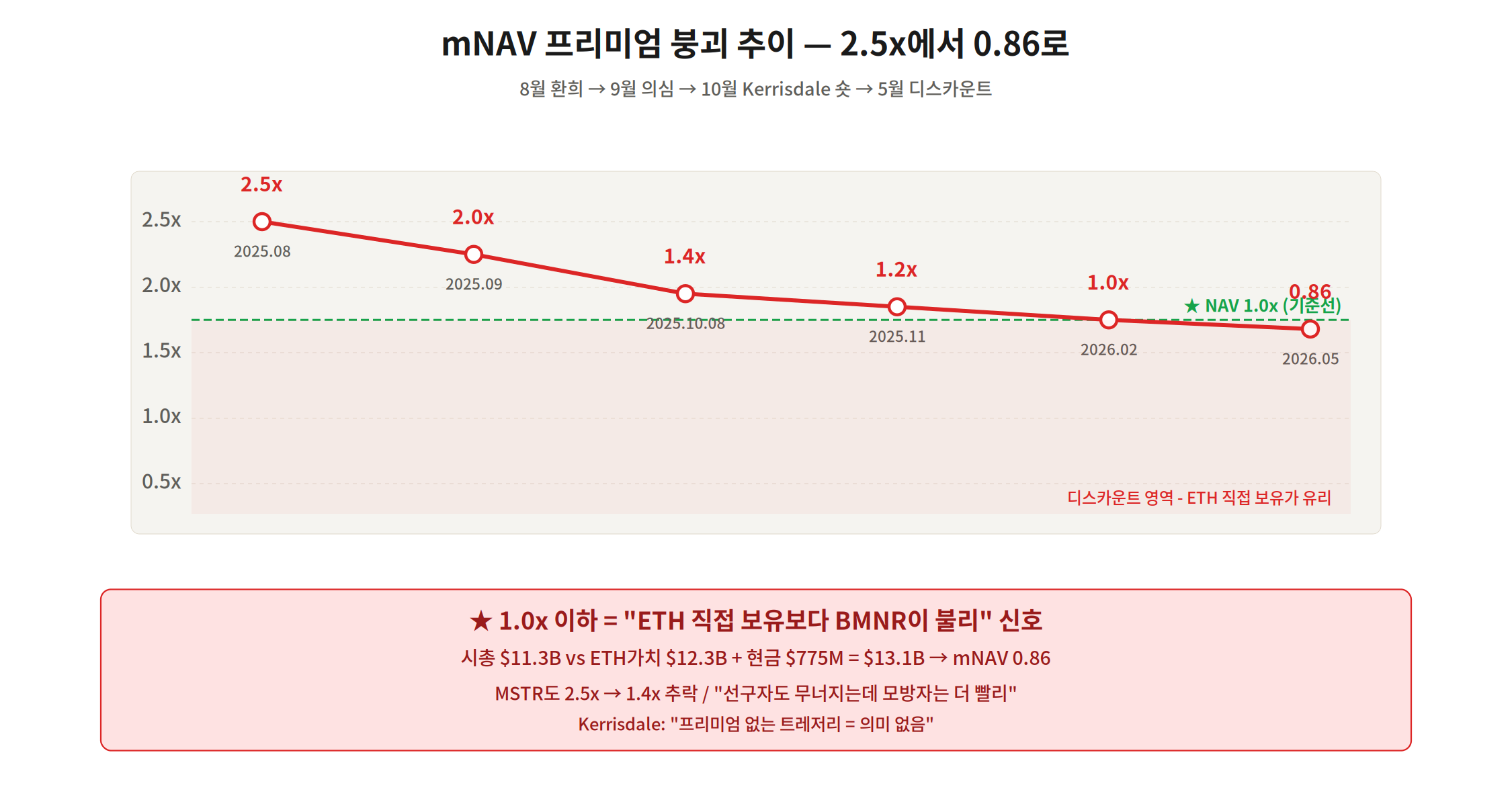

4. BitMine BMNR ETH Treasury mNAV Collapse — From 2.5x to 0.86

mNAV (multiple of Net Asset Value) is the defining metric for any treasury company. Calculated as market cap ÷ value of ETH holdings, a reading above 1.0 indicates a premium — the model’s raison d’être — while below 1.0 signals a discount. Currently: $11.3B market cap ÷ ($12.3B ETH + $775M cash) = 0.86. The BitMine BMNR ETH treasury is now cheaper than the underlying asset on a per-unit basis.

| Date | mNAV | Interpretation |

|---|---|---|

| Aug 2025 | 2.0–2.5x | Strong premium (model working) |

| Oct 8, 2025 (Kerrisdale short) | 1.2x | Premium eroding fast |

| Feb 2026 | 1.0x | At NAV |

| May 17, 2026 (Today) ★ | 0.86 | Discount — ETH direct better |

A sub-1.0 mNAV signals that markets judge ETH ownership superior to BMNR share ownership — a fundamental challenge to the whole premise of a treasury company. The 0.86 reading also embeds a risk premium for potential 100× dilution from the 50-billion authorized share pool.

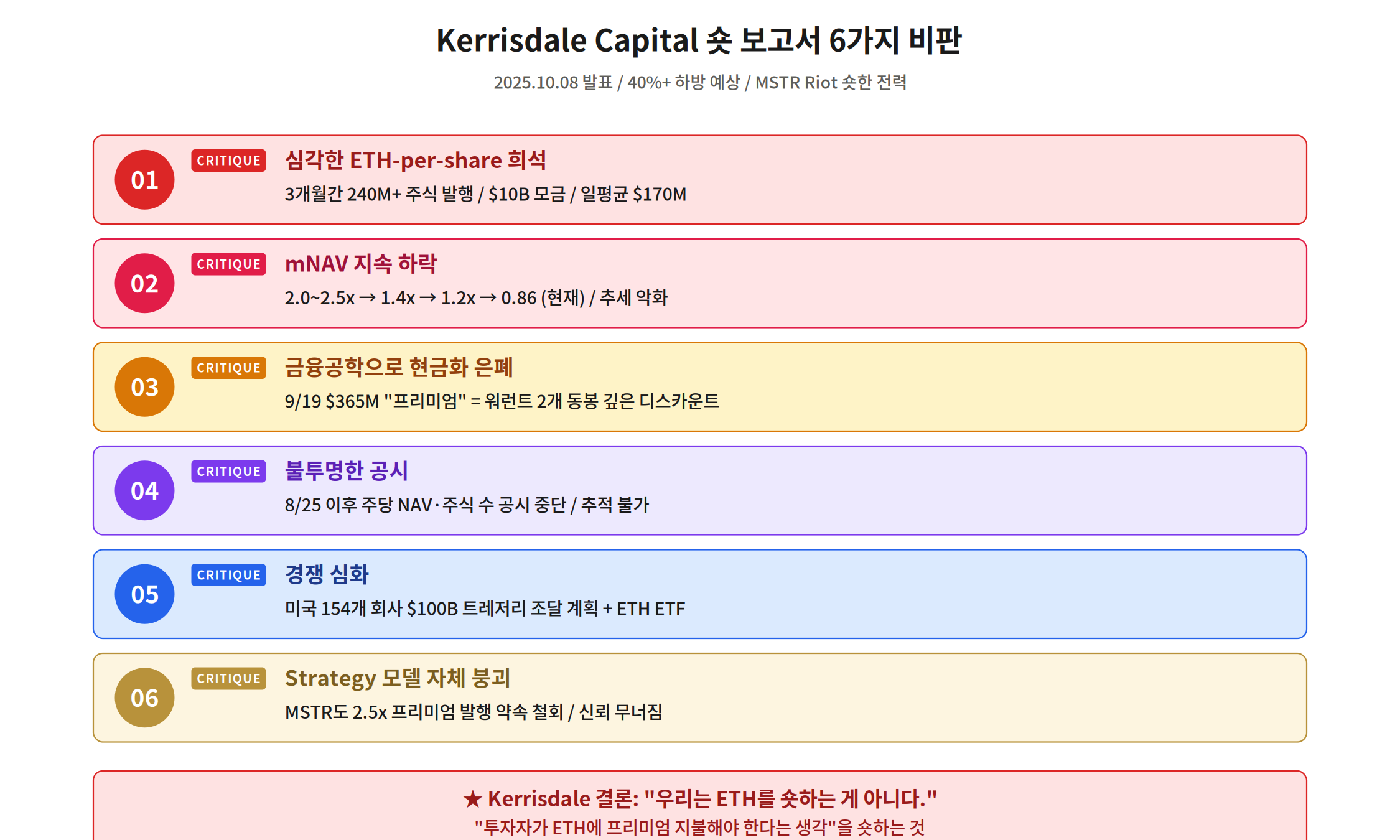

5. Kerrisdale Short Report — Six Critiques and 40%+ Downside

Activist short-seller Kerrisdale Capital (founded 2009 by Sahm Adrangi) officially disclosed a short position in BMNR on October 8, 2025. The firm has previously shorted Riot Platforms and MicroStrategy, successfully driving price declines in both.

- Severe ETH-per-share dilution — 240M+ shares in 3 months, $10B raised, $170M/day average (record pace)

- Persistent mNAV decline — 2.0–2.5x → 1.4x → 1.2x → 0.86 (worsening trajectory)

- Financial engineering obscures dilution — Sep 19 “premium” raise was actually a deep discount via two bundled warrants

- Opaque disclosure — Per-share NAV and share count disclosures halted after Aug 25, 2025

- Intensifying competition — 154 U.S. companies planning $100B in treasury raises; new ETH ETFs launching

- The Strategy (MSTR) model itself is fraying — MSTR abandoned its own “no issuance below 2.5x mNAV” pledge

“We are not short ETH. We are short the idea that investors should pay a premium for exposure to ETH. If you want ETH, just buy it — or buy an ETF.”

— Kerrisdale Capital (Oct 8, 2025), 40%+ downside target

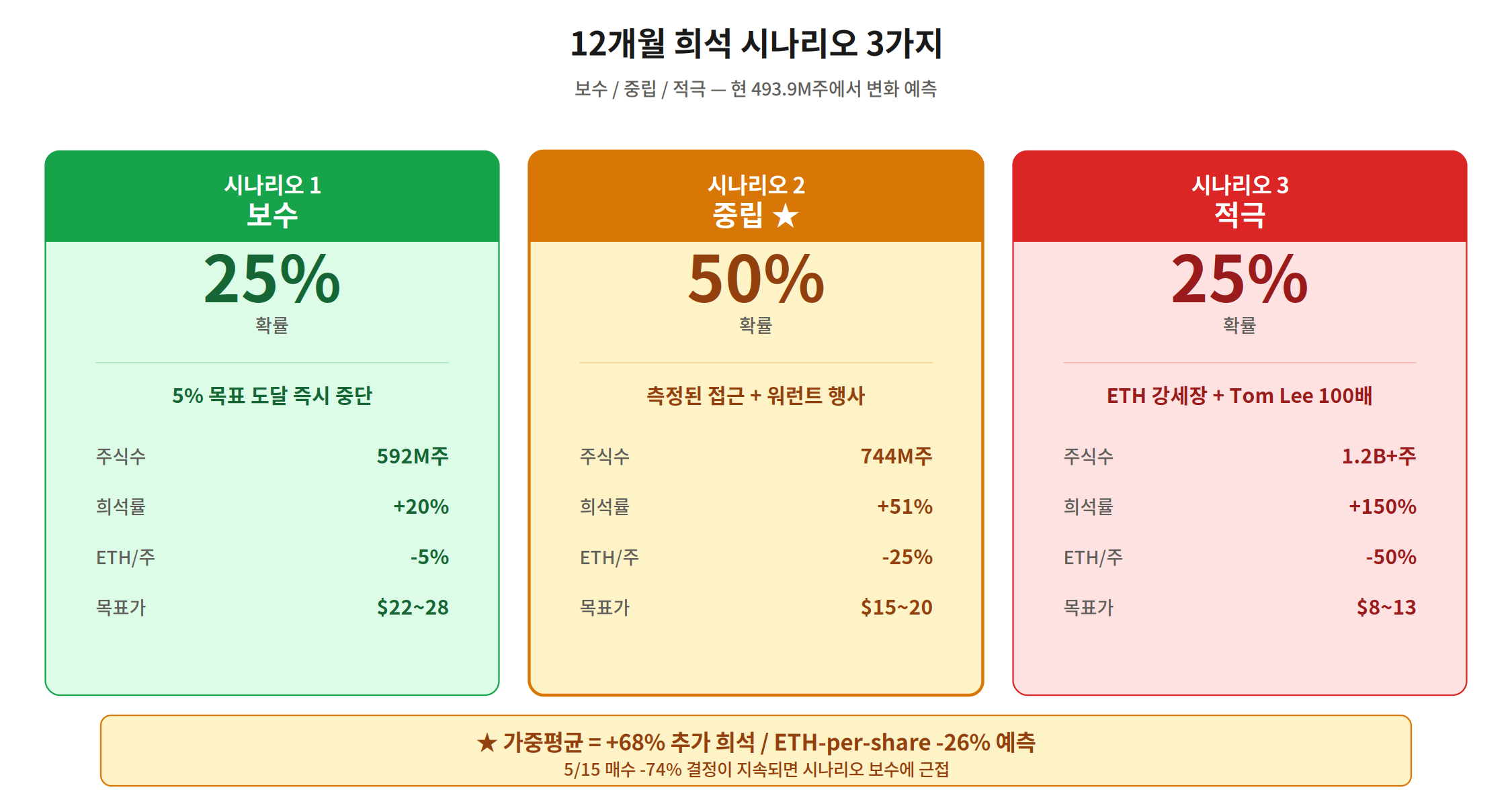

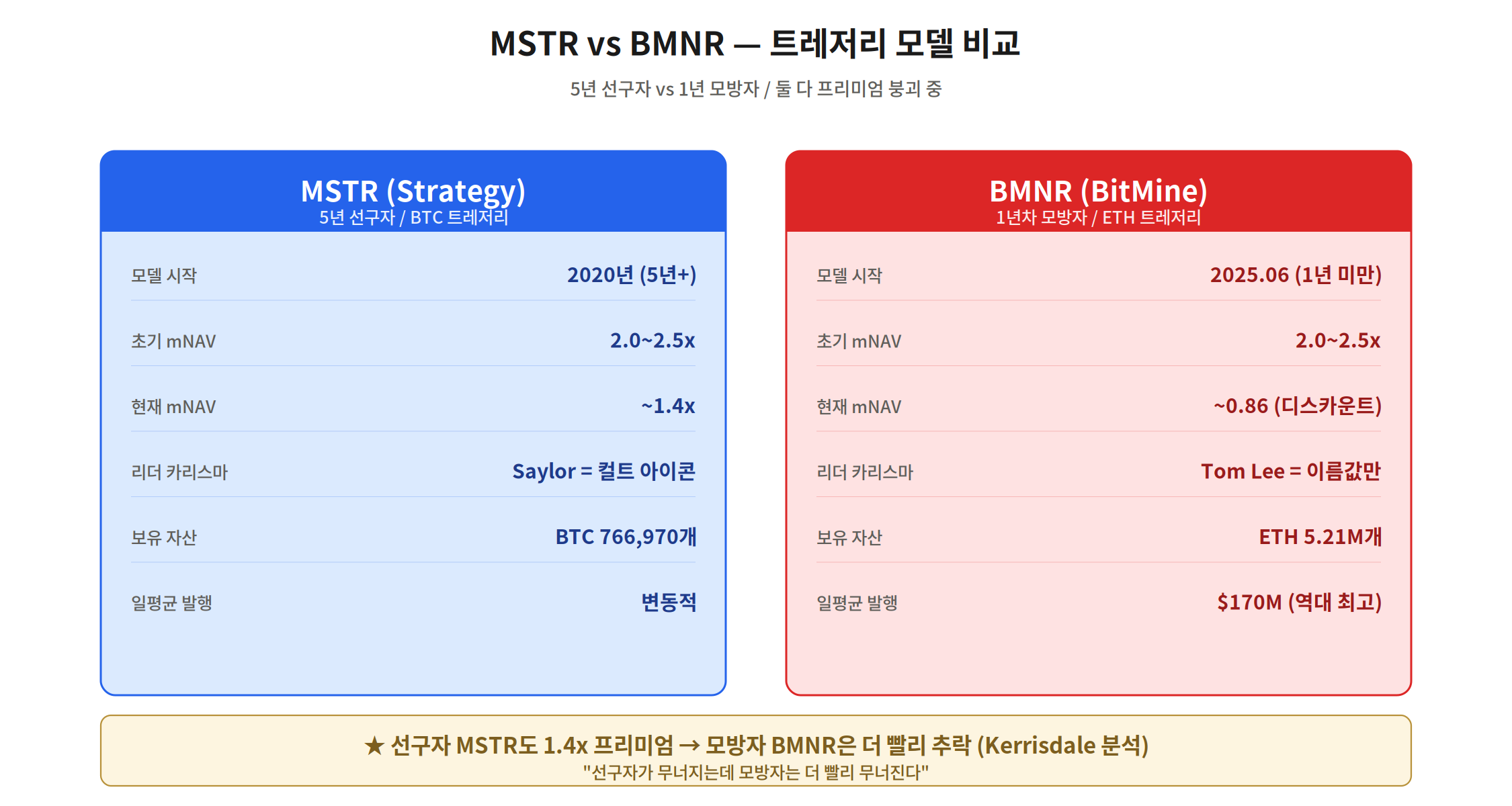

6. Three Dilution Scenarios + MSTR vs BMNR Comparison

Starting from 493.9M shares, three scenarios for the next 12 months. Probability-weighted result: +68% dilution / ETH-per-share -26%.

| Scenario | Probability | Shares (12mo) | Dilution | ETH/share |

|---|---|---|---|---|

| ① Conservative | 25% | 592M | +20% | -5% |

| ② Base ★ | 50% | 744M | +51% | -25% |

| ③ Aggressive | 25% | 1.2B+ | +150% | -50% |

The single most important variable is Tom Lee’s May 15 “more measured approach” announcement — a 74% slowdown in ETH purchases. Three forces appear to be behind the decision: (1) acknowledging the mNAV premium is gone, (2) approaching the 5% accumulation target (4.31% now), (3) signaling shareholder-value protection mode. If this holds for 6–9 months, the conservative scenario becomes more realistic.

MSTR (Strategy) is the five-year pioneer of the treasury model. Its current mNAV sits around 1.4x — still above 1.0 — while BMNR has already crossed into discount territory. Kerrisdale’s argument is direct: if the original model is breaking down, its one-year-old imitation will break faster. In August 2025, MSTR itself abandoned the “no issuance below 2.5x” discipline it had long promised. If the rule-setter can’t keep its own rules, what hope does the rule-follower have?

7. Five Monitoring Signals + Buy vs. Avoid — Final Assessment

- Every Monday — PR Newswire: Search “Bitmine Immersion Technologies” → weekly ETH holdings update + cash balance (5 min)

- Weekly ETH purchase pace: 100K+ ETH/week = aggressive mode; 30K or fewer = measured mode; track the post-5/15 trend

- Calculate mNAV yourself: Yahoo Finance market cap ÷ (BMNR-disclosed ETH value + cash). Below 1.0 = discount = caution signal

- Quarterly SEC EDGAR 10-Q: shares outstanding + warrants + remaining ATM capacity (March, June, September, December)

- Compare MSTR mNAV: The pioneer’s trajectory is a leading indicator for the BitMine BMNR ETH treasury

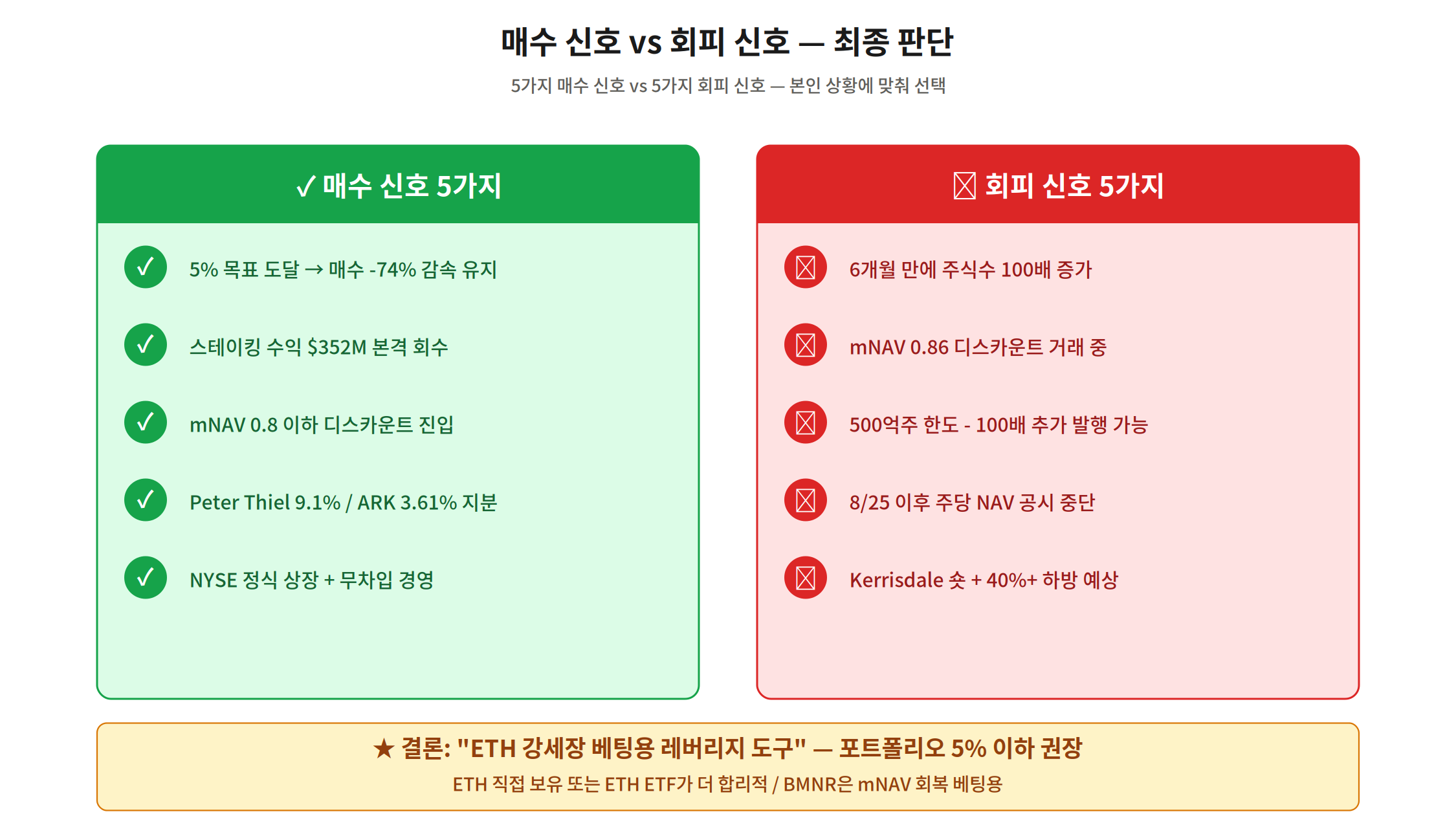

Buy Signals (Five Positives)

- Approaching 5% target → 74% purchase slowdown — potential dilution deceleration ahead

- Staking income of $352M — MAVAN platform generating real cash flow

- mNAV 0.86 discount — entering safety-margin territory

- Peter Thiel 9.1% / ARK 3.61% stakes — institutional conviction (Cathie Wood added in October)

- NYSE-listed, zero-debt balance sheet — no accounting insolvency risk

Avoid Signals (Five Negatives)

- 100× share count increase in six months — Korean-market equivalent of immediate trading suspension

- BitMine BMNR ETH treasury mNAV 0.86 — holding ETH directly is mathematically superior

- 50B authorized shares — potential 100× further dilution — existential risk premium baked in

- Per-share NAV disclosure halted since Aug 25 — transparency erosion undermines trust

- Kerrisdale short + 40%+ downside target — sustained hedge-fund selling pressure

Bottom Line — BMNR Is a Leveraged ETH Bet, Nothing More

BitMine accomplished something genuinely remarkable: becoming the world’s largest Ethereum treasury in under a year. Zero debt, institutional backers, a functioning staking platform, NYSE blue-chip listing — the credentials are real. So is the danger. Six months of 100× dilution, a BitMine BMNR ETH treasury mNAV at 0.86, a 50-billion authorized share overhang, and one of the most respected activist short funds in the market with a 40% downside call.

The pivotal question is whether Tom Lee’s May 15 measured-pace declaration sticks for six to nine months. If it does, dilution slows and mNAV could recover. If ETH enters a bull run and BMNR resumes aggressive buying, scenario C — 150% dilution — becomes live. For investors who want ETH exposure, buying ETH directly or through an Ethereum ETF remains the cleaner path. BMNR is a tool for those explicitly betting on both mNAV recovery and an ETH bull run simultaneously — cap it at 5% of portfolio and keep the five monitoring signals on your radar.