Covered Call ETF Tax-Free Truth and NAV Erosion Traps — Korea KODEX TIGER RISE Yield Comparison

Economic Insights · May 17, 2026

Covered call ETF tax-free Korea — is the zero-tax claim on option premiums real? One ETF advertises a 19.5% distribution yield while delivering a -5.8% six-month return. This guide unpacks the legal basis for Korea’s option premium tax exemption, compares the six major domestic ETFs, and maps the five hidden traps that trip up retail investors.

What Is a Covered Call ETF? Structure and Yield Mechanics

A covered call ETF holds an underlying equity index while simultaneously selling call options on that same index to collect option premiums. In Korea, more than 100 such ETFs are listed, with combined assets under management running into the trillions of Korean won. The option premium is distributed to investors weekly or monthly, making regular cash flow the primary appeal.

Simplified: the fund manager buys index constituents (e.g., KOSPI 200 components) and sells call options on the same index. When the market rises sharply, the fund gives up part of the upside because options get exercised. When the market moves sideways or dips slightly, the premium acts as a cushion. In essence, covered call ETFs trade some upside potential for a predictable income stream.

Weekly (위클리) variants renew options every week to maximise premium capture. Because option premiums grow with market volatility, these ETFs can look deceptively attractive during high-volatility periods — a perception that does not always translate into superior total returns.

Korea’s Covered Call ETF Tax-Free Structure — Article 26-2(4) Explained

The legal basis for the covered call ETF tax-free treatment in Korea is Article 26-2, Paragraph 4 of the Enforcement Decree of the Income Tax Act. The rule sets a 0% tax rate on option premium income from Korea domestic equity-based ETFs and excludes it from the aggregate financial income calculation used to determine whether an investor is subject to the comprehensive financial income tax (종합과세).

The critical caveat: the exemption applies only to ETFs with Korean domestic equities as the underlying asset. Covered call ETFs benchmarked to the U.S. S&P 500, NASDAQ 100, or individual foreign stocks (e.g., TIGER US Dividend+3% Premium) attract the standard 15.4% dividend withholding tax on the same option premiums. Confusing the two categories is a costly and common mistake — always verify the underlying index before investing.

The Financial Supervisory Service’s consumer information portal (https://www.fss.or.kr) allows investors to look up tax treatment by ETF type — a recommended step before committing capital.

Six Major Korean Covered Call ETFs Compared — KODEX, TIGER, RISE Yields

All six ETFs below are domestic equity-based and qualify for the Korea covered call ETF tax-free treatment on their option premium distributions.

| ETF Name | Asset Manager | Target Annual Yield | Underlying Index |

|---|---|---|---|

| KODEX 200 Target Weekly Covered Call | Samsung Asset Management | ~15% p.a. | KOSPI 200 |

| TIGER 200 Target Weekly Covered Call | Mirae Asset | ~7% p.a. | KOSPI 200 |

| RISE 200 Weekly Covered Call | KB Asset Management | ~12% p.a. | KOSPI 200 |

| KODEX Financial High-Dividend TOP10 Target Weekly | Samsung Asset Management | ~15% p.a. | Finance & High-Dividend |

| TIGER Korea Dividend Dow Jones Target Weekly | Mirae Asset | ~10% p.a. | Korea Dividend Dow Jones |

| FOCUS AI Semiconductor Weekly Covered Call | Korea Investment Management | ~12% p.a. | AI & Semiconductors |

Target yields are management targets, not contractual guarantees. Actual distributions fluctuate monthly based on market volatility, prevailing option premium levels, and underlying asset dividends. Even a 15%-target ETF can see its NAV fall faster than the distribution rate if the underlying index drops sharply.

A 19.5% distribution yield paired with a -5.8% six-month return — this is the reality of NAV erosion in covered call ETFs.

Tax-Free Simulation and Five Hidden Traps — From NAV Erosion to Samsung Securities’ Error

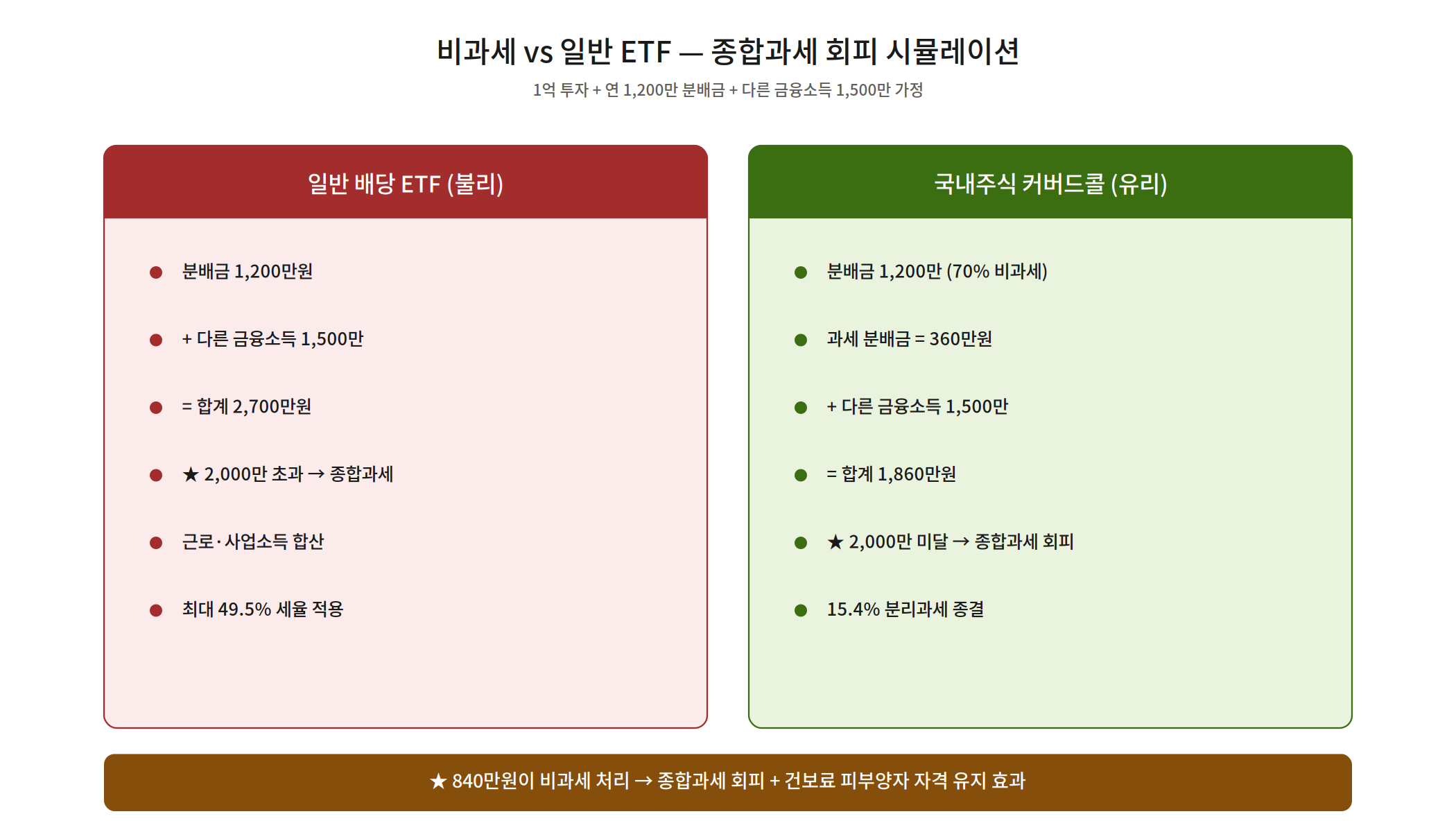

Simulation: KRW 100 million invested at a 12% annual distribution rate

Annual distributions total KRW 12 million. Assume 70% of that originates from option premiums (tax-exempt) and 30% from dividends and interest (taxable). Taxable financial income is KRW 3.6 million. Adding KRW 15 million from other financial sources brings the total to KRW 18.6 million — below the KRW 20 million comprehensive tax threshold. The same return from a standard bond ETF would be fully counted as KRW 27 million in financial income, triggering comprehensive taxation. This gap is the real, measurable value of the covered call ETF tax-free structure in Korea.

Despite the tax benefits, five traps await the unwary investor:

- NAV Erosion (Return of Capital, ROC): Part of a distribution may be a return of the investor’s own capital rather than genuine investment income. The PLUS High-Dividend ETF advertised a 19.5% target yield but posted a -5.8% six-month return, illustrating how a high distribution rate can mask a shrinking NAV.

- Bull Market Opportunity Cost: Selling call options caps upside participation. If the KOSPI 200 surges 30%, a covered call ETF may only capture 10–15% of that gain.

- No Downside Shield: Option premiums provide limited cushioning in bear markets. A deep drawdown in the underlying index easily overwhelms the premium income buffer.

- Target Yield Not Guaranteed: Managers are under no legal obligation to meet the stated target. When market volatility falls, premiums shrink and distributions can drop substantially.

- Brokerage Tax Processing Errors: Samsung Securities reportedly withheld 15.4% tax on option premium distributions — income that should have been tax-exempt — for approximately 15 years. Always review your year-end tax statement independently; brokerages can and do make errors.

Who Should Invest — and Who Should Stay Away — Plus Five Practical Strategies

Best suited for three investor profiles. First, retirees and elderly investors who need regular cash flow. Second, investors near the KRW 20 million financial income threshold who want to avoid a sudden jump into comprehensive taxation. Third, investors expecting the Korean market to move sideways over the next one to two years.

Poor fit for investors in their 30s and 40s focused on long-term wealth accumulation — the structural cap on upside compounding meaningfully reduces long-term returns. Also unsuitable for anyone selecting covered call ETFs based solely on the distribution yield headline without considering total return.

Five Strategies for Using Covered Call ETFs Effectively

- Domestic equity underlying only: The tax exemption requires a Korean domestic equity base. Exclude any U.S.- or NASDAQ-benchmarked products.

- Evaluate on total return (distribution + NAV change): Never judge these ETFs on distribution rate alone. Track total return over the holding period.

- Monitor financial income at the KRW 17 million mark: Build in a buffer below the KRW 20 million threshold. Reassess additional investment once total financial income approaches KRW 17 million.

- Use an ISA account: Placing covered call ETFs inside a Korean Individual Savings Account (ISA) means distributions are tax-exempt within the annual limit; upon maturity, a separate tax option applies.

- Limit allocation to 30% of the portfolio: Following basic diversification principles, keep covered call ETF exposure below 30% of total investable assets.

Scenario-based expected outcomes: Sideways market (probability ~40%) — the most favourable environment; premium income is maximised. Bull market (~35%) — underperforms plain index ETFs due to the structural upside cap. Bear market (~25%) — option premiums provide marginal cushioning but cannot offset a severe drawdown; covered call ETFs take the full hit.

Conclusion — Korea Covered Call ETF Tax-Free Is Real, but Conditional

The covered call ETF tax-free structure in Korea is legally grounded in the Enforcement Decree of the Income Tax Act. But “tax-free” does not mean “risk-free high yield.” The 19.5% yield masking a -5.8% NAV decline, Samsung Securities’ 15-year withholding error, and the structural drag in bull markets are realities that demand clear-eyed analysis. Stick to domestic equity underlying assets, total-return evaluation, a 30% or lower portfolio weight, and ISA utilisation — under these four principles, covered call ETFs become a legitimate and effective tool for retirement income and tax management in Korea.