Korea pension 2026 — National & Basic Pension reforms: +2.1%, eligibility eased 8.3%, couple-deduction phased out

Trending · May 24, 2026 · DIR

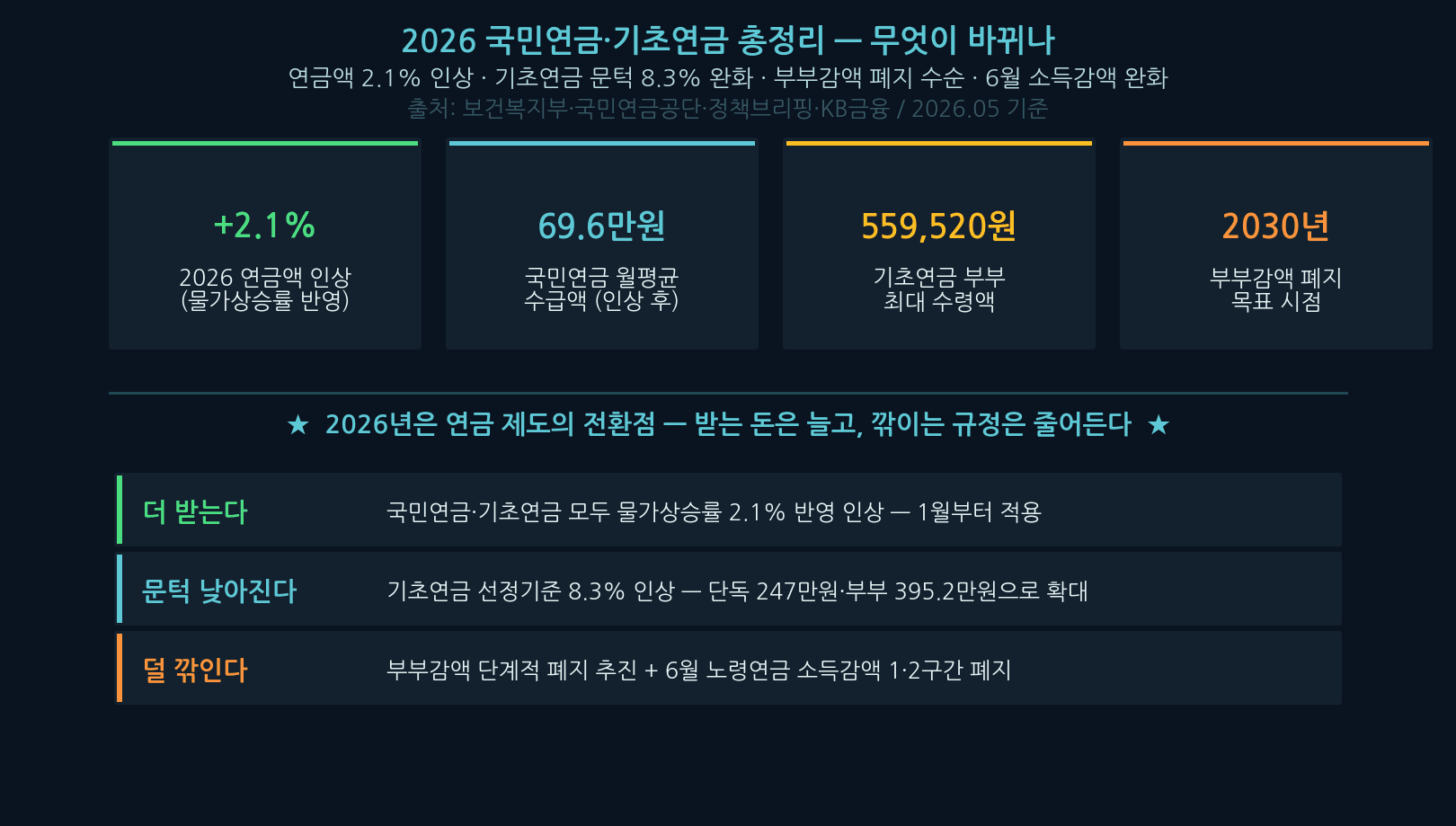

The Korea pension 2026 reforms touch every retiree. Both National Pension and Basic Pension rose 2.1%, eligibility eased by 8.3%, the controversial couple-deduction is phasing out, and a June 17 amendment removes early income-clawback brackets. We unpack what changed and what you should check.

2026 brings meaningful changes to Korea’s retirement system. Under the Korea pension 2026 updates, both National Pension and Basic Pension have been lifted 2.1% in line with last year’s CPI, and the income threshold for Basic Pension rose 8.3% — broadening eligibility. The long-debated couple-deduction is being phased out, and from June 17 the income-clawback on working seniors’ old-age pension will be significantly relaxed.

The system is complex, and misconceptions abound: “high National Pension means no Basic Pension,” “couples lose out.” This article walks through the differences between the two pensions, what changed in 2026, the truth behind couple- and link-deductions, and a checklist to make sure you actually claim what you are entitled to. Primary sources: Policy Briefing and the National Pension Service.

National Pension vs Basic Pension — do not confuse them

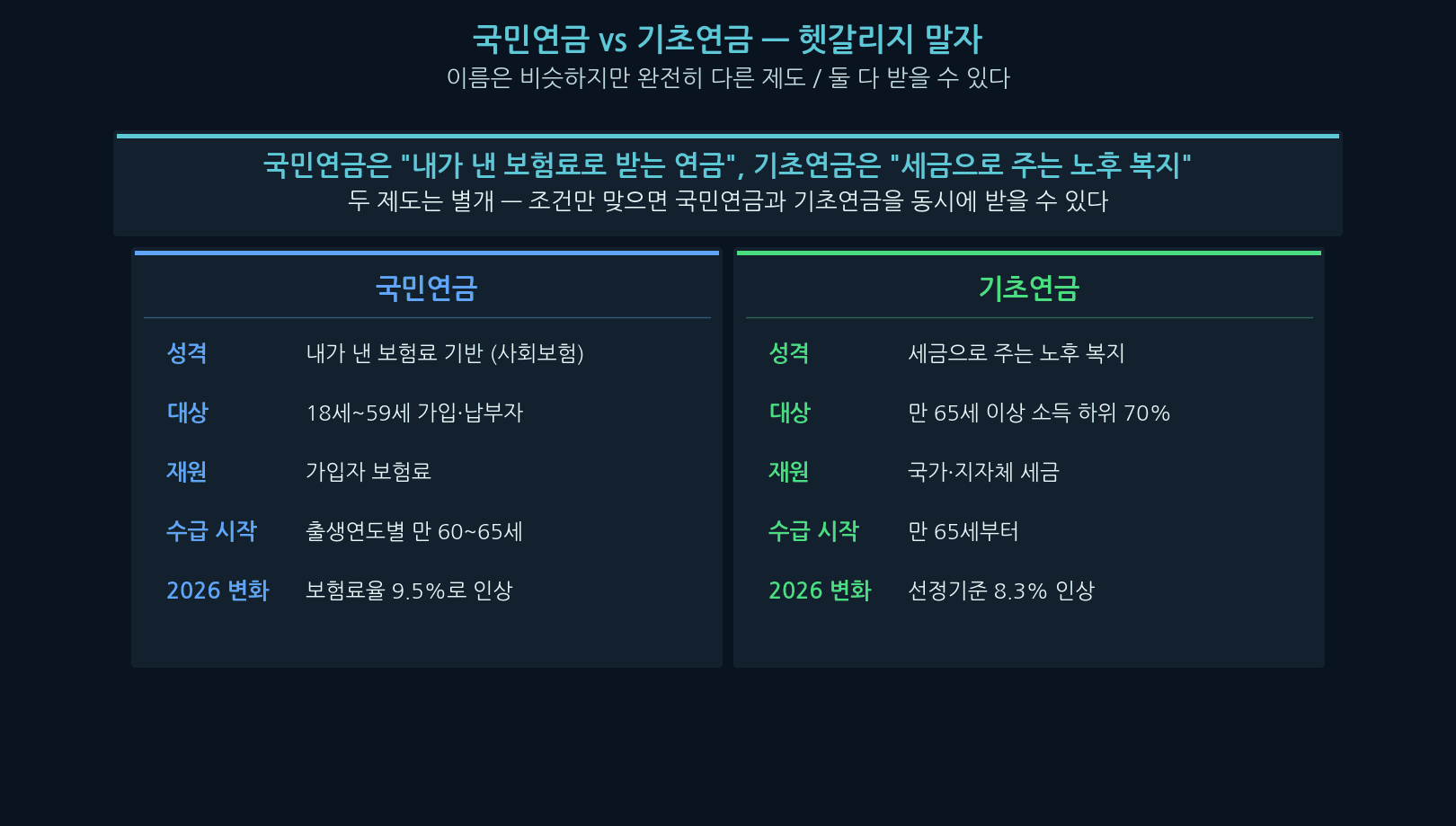

Before anything else: National Pension (NP) and Basic Pension (BP) are two entirely different programs. The names sound similar, but they have different funding sources and different target populations.

National Pension is a contribution-based social-insurance program: workers pay premiums and later receive benefits. Basic Pension is a tax-funded welfare program for the bottom 70% of seniors aged 65+. Crucially, the two are independent. If you meet the criteria, you can receive both at the same time.

| Aspect | National Pension | Basic Pension |

|---|---|---|

| Nature | Premium-based social insurance | Tax-funded welfare |

| Eligibility | Ages 18–59, premium payers | Ages 65+, bottom 70% income |

| Funding | Member premiums | National + local taxes |

| Onset | Age 60–65 (by birth year) | Age 65 |

| Concurrent receipt | Yes | Yes |

Korea pension 2026 — five National Pension changes

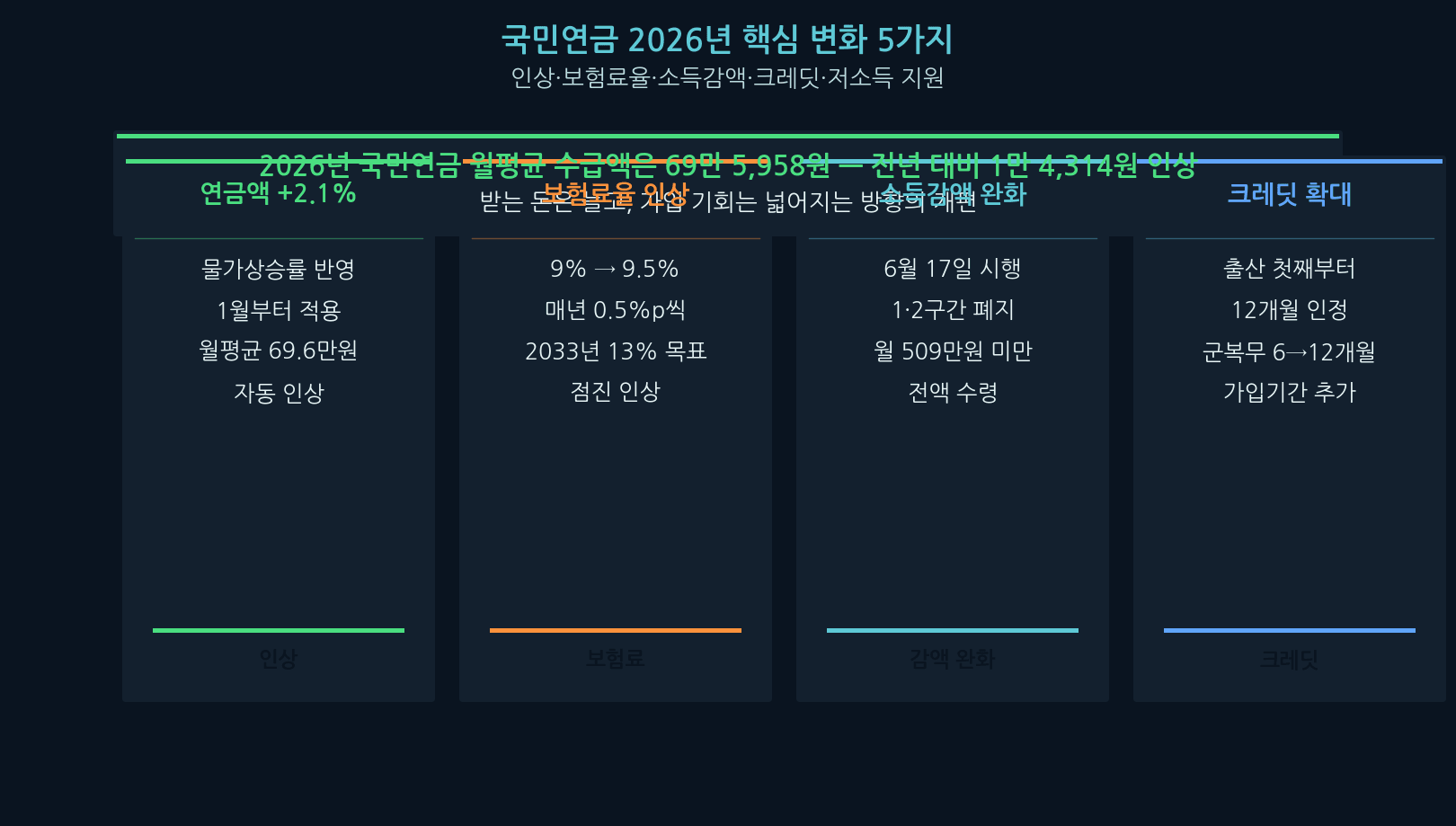

Korea pension 2026 brings several National Pension changes. First, benefits rose 2.1%, reflecting last year’s CPI, effective January. Average monthly benefits now sit at KRW 695,958 — up KRW 14,314 year-on-year.

The contribution rate also moves. Held at 9% since 1998, the premium rises to 9.5% in 2026, climbing 0.5 percentage points per year toward a target of 13% by 2033. Childbirth and military-service credits have also been expanded, recognizing more contribution months.

| Item | 2026 change | Detail |

|---|---|---|

| Benefit | +2.1% | Avg KRW 695,958/mo |

| Contribution rate | 9% → 9.5% | 13% by 2033 |

| Income clawback | Brackets 1–2 removed | Effective June 17 |

| Childbirth credit | From 1st child, 12 months | 50-month cap removed |

| Military credit | 6 → 12 months | Extra contribution months |

National Pension benefits are adjusted by the prior year’s CPI of 2.1% and paid out from January.

— MOHW Policy Briefing · Jan 2026

Basic Pension — am I eligible

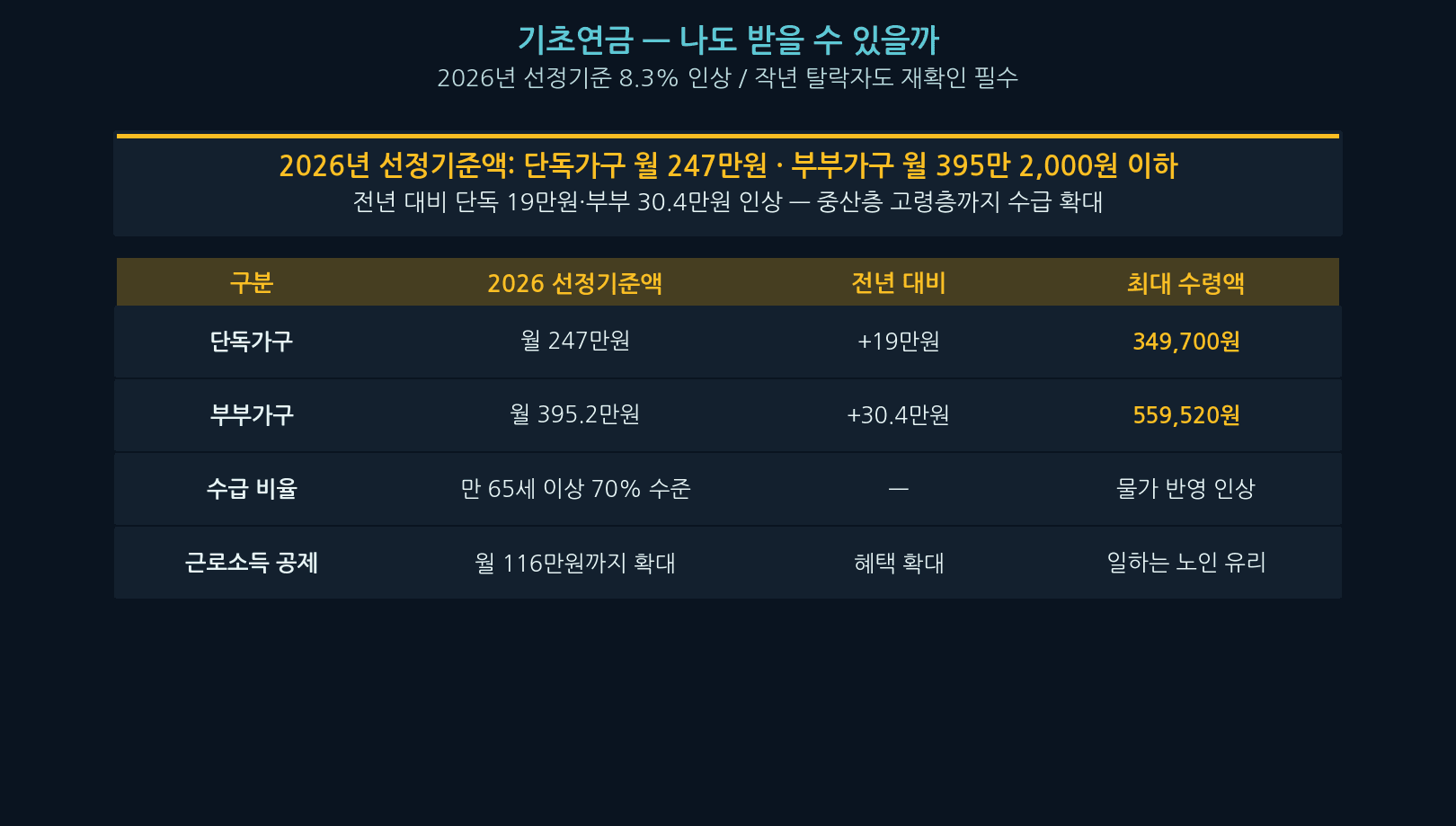

The most common Basic Pension question is “do I qualify?” In 2026, the income threshold jumped sharply: KRW 2.47 million per month for single households, KRW 3.952 million for couple households.

That is +KRW 190,000 for singles and +KRW 304,000 for couples versus last year — roughly an 8.3% increase. If you missed the cutoff last year, check again this year. Maximum monthly payments are KRW 349,700 (single) and KRW 559,520 (couple combined).

| Household | Income threshold | YoY change | Max benefit |

|---|---|---|---|

| Single | KRW 2.47M/mo | +KRW 190K | KRW 349,700 |

| Couple | KRW 3.952M/mo | +KRW 304K | KRW 559,520 |

| Increase | ~8.3% | Threshold eased | Reaches middle class |

| Earned-income deduction | Up to KRW 1.16M/mo | Expanded | Friendly to working seniors |

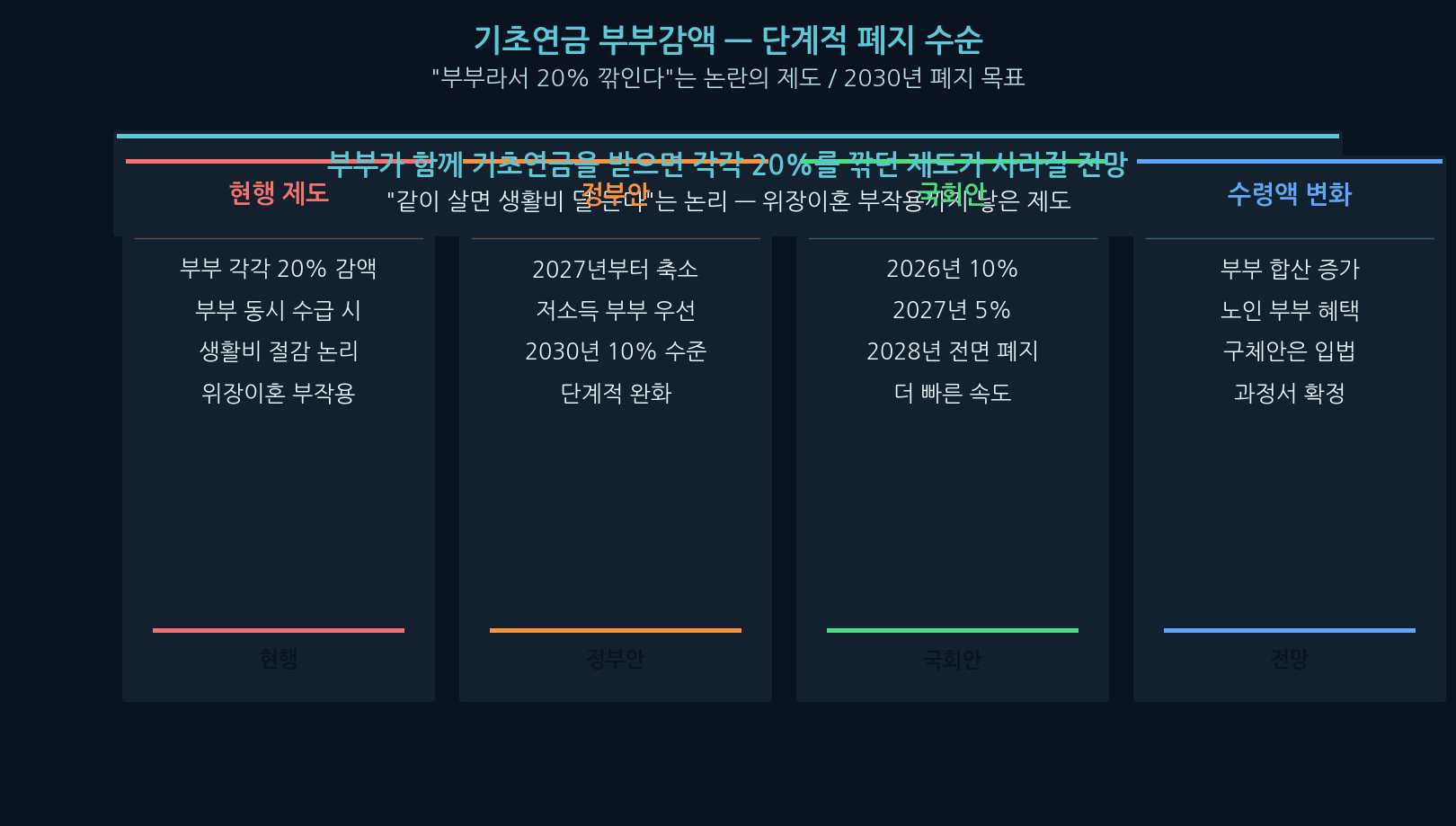

Basic Pension couple-deduction — a phased rollback

A long-controversial Basic Pension feature is the “couple-deduction”: when both spouses qualify, each receives 20% less. The original rationale — couples spending less per head — has been criticized as outdated under high inflation.

It even led to paper divorces aimed at preserving full benefits. Reform is now in motion: the couple-deduction is being phased out. The government plan targets reduction to ~10% by 2030, while a National Assembly proposal seeks full repeal by 2028.

| Item | Detail | Timing |

|---|---|---|

| Current | 20% deduction each | In force |

| Government plan | Phased down to ~10% | By 2030 |

| NA proposal | 10% → 5% → full repeal | By 2028 |

| Effect | Higher combined benefit for couples | Confirmed via legislation |

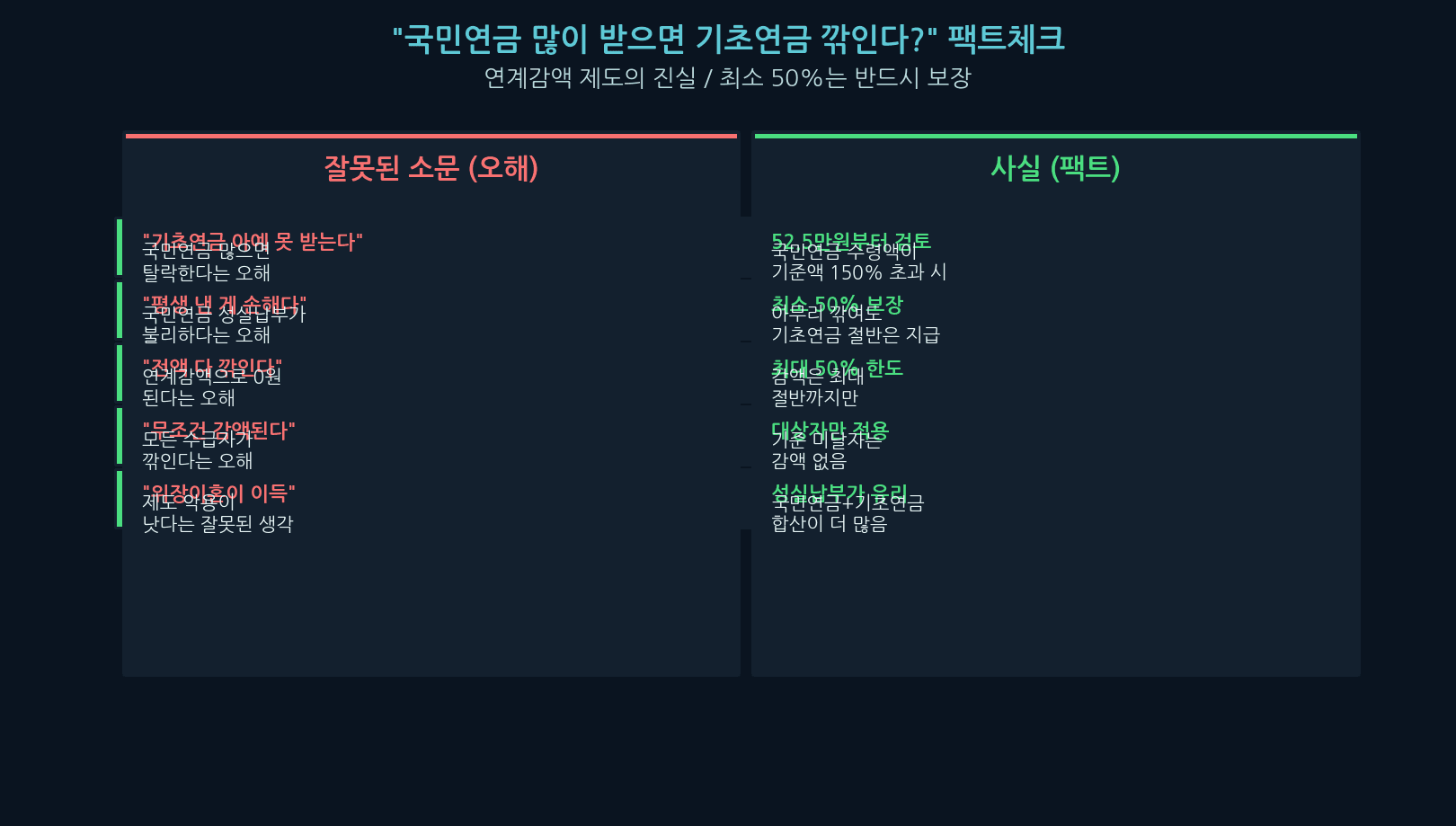

“Does higher National Pension cut Basic Pension?” — a fact-check

A widespread complaint among seniors targets the “link-deduction”: “I paid in honestly for decades and they cut my Basic Pension.” The short answer is — that’s largely a misconception.

The link-deduction only kicks in once your monthly National Pension exceeds 150% of the standard amount — roughly KRW 525,000. Even then, the crucial point is: at least 50% of the Basic Pension is always guaranteed. Basic Pension never falls to zero. Counting NP + BP together, honest contributors still come out ahead.

| Misconception | Fact |

|---|---|

| “I get no Basic Pension at all” | Only triggers above ~KRW 525K NP |

| “It’s all clawed back” | At least 50% always guaranteed |

| “Lifetime contributions hurt me” | NP + BP combined favors contributors |

| “Everyone gets cut” | Below threshold, no deduction |

Even when National Pension exceeds the threshold, at least 50% of Basic Pension is always guaranteed.

— 2026 Basic Pension notice · MOHW

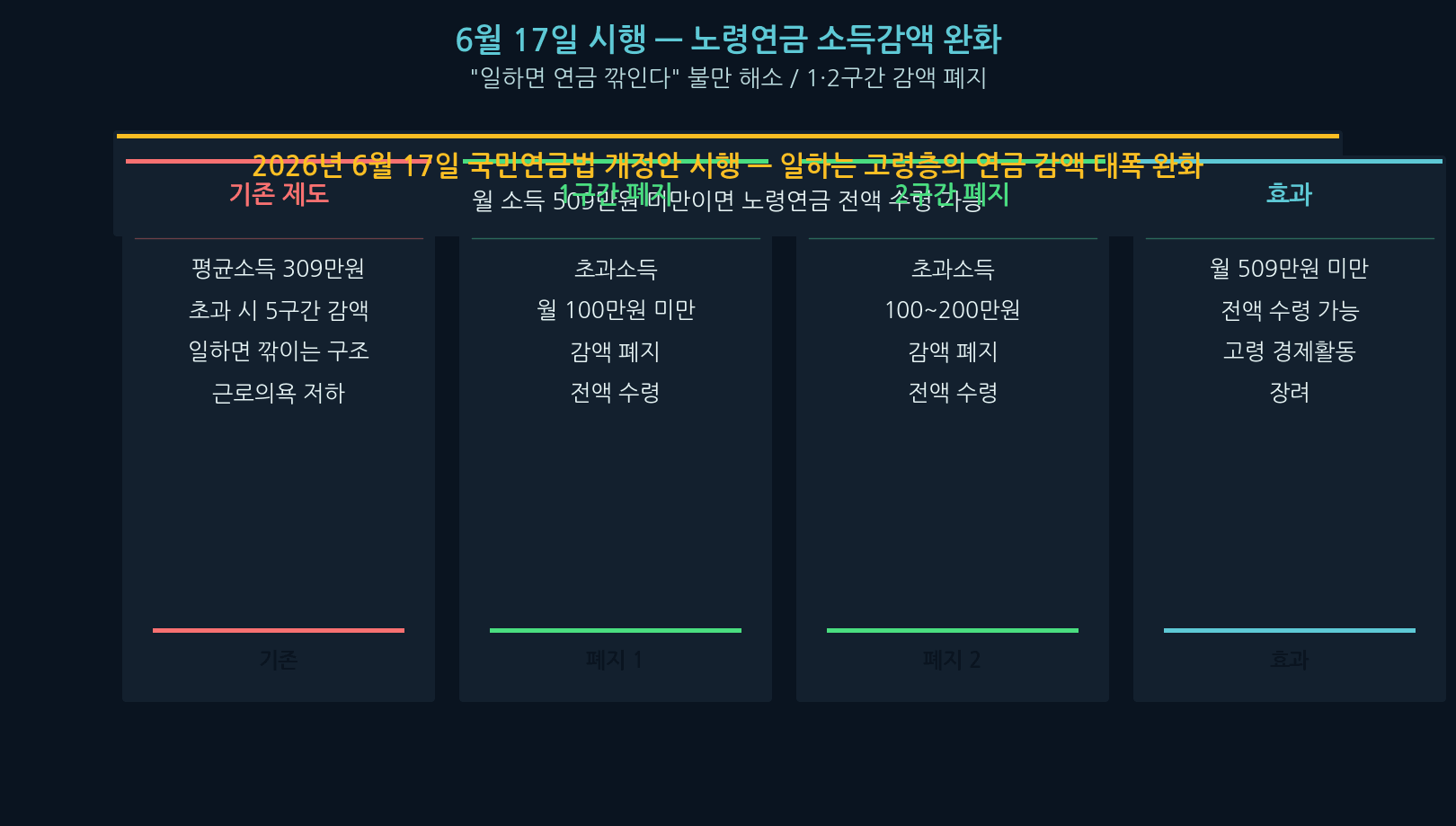

June 17 — relaxed income clawback on old-age pension

Good news for working seniors. With the amended National Pension Act effective June 17, 2026, the income-clawback that reduces pensions for those who keep earning is being significantly relaxed.

Previously, if a recipient’s monthly income exceeded the average member income (KRW 3.09 million), the excess was clawed back across five brackets. The reform removes brackets 1 and 2, so anyone earning under KRW 5.09 million per month will receive the full old-age pension. The change targets the “work and lose pension” complaint head-on.

| Item | Detail | Change |

|---|---|---|

| Old rule | 5 brackets above KRW 3.09M income | Work = cut |

| Bracket 1 removed | Excess income < KRW 1M | No cut |

| Bracket 2 removed | Excess KRW 1M–2M | No cut |

| Net effect | Income < KRW 5.09M/mo | Full pension |

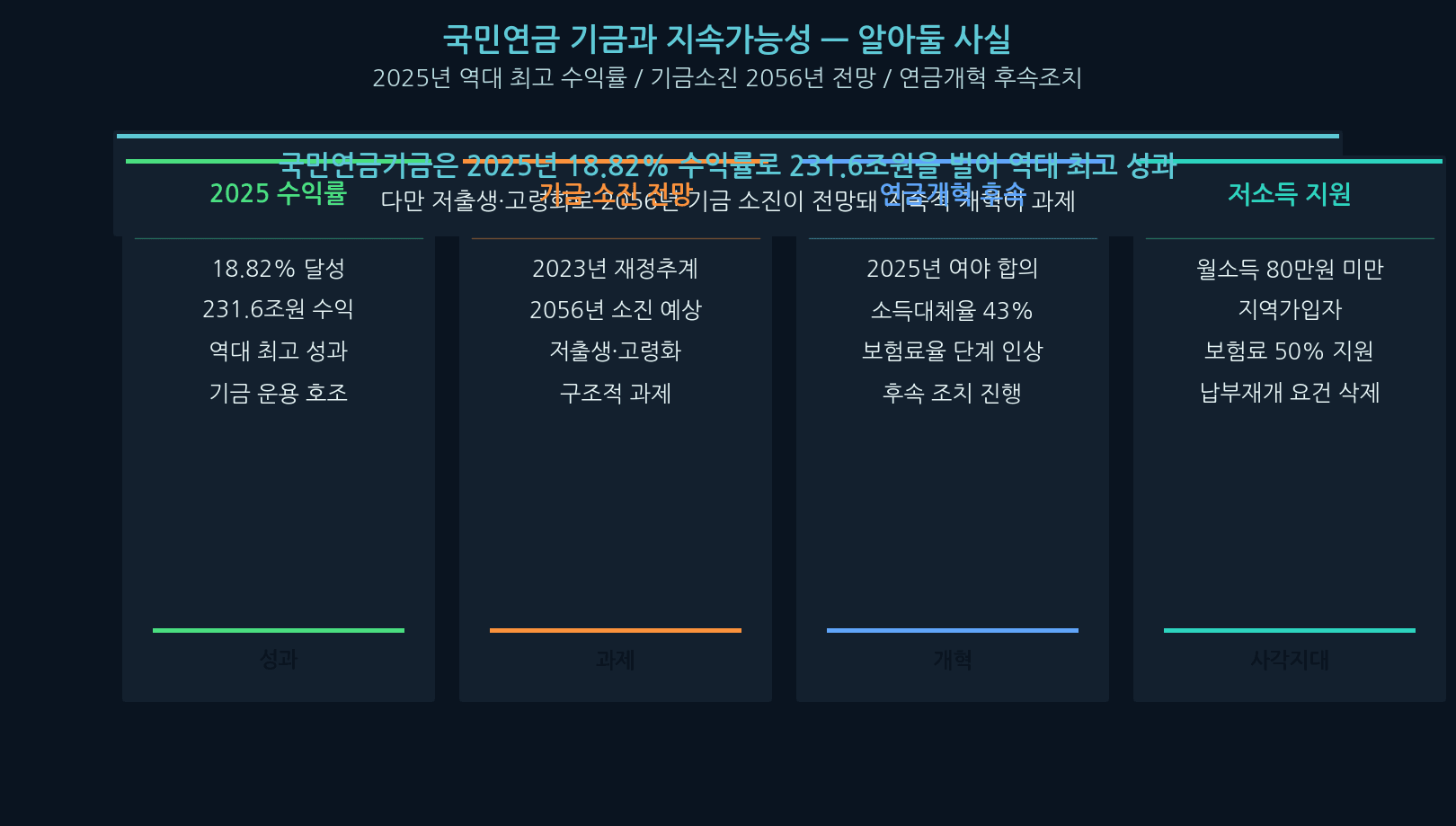

National Pension fund and sustainability — what to know

“They say the fund runs out — will I get anything?” A common concern. Let’s separate facts. First, the National Pension Fund posted a record 18.82% return in 2025, earning KRW 231.6 trillion.

That said, the structural challenge — low birth rates and aging — remains. The 2023 financial projection sets fund depletion at 2056. That motivated the 2025 cross-party pension-reform agreement: phased premium-rate hikes and replacement-rate adjustments are now in motion. Expanded premium subsidies for low-income local subscribers are part of the same package.

| Item | Detail |

|---|---|

| 2025 return | 18.82% — KRW 231.6T earned (record) |

| Depletion projection | 2056 (per 2023 estimate) |

| Pension reform | 2025 cross-party deal — rate & replacement adjusted |

| Low-income support | 50% premium subsidy for incomes < KRW 800K/mo |

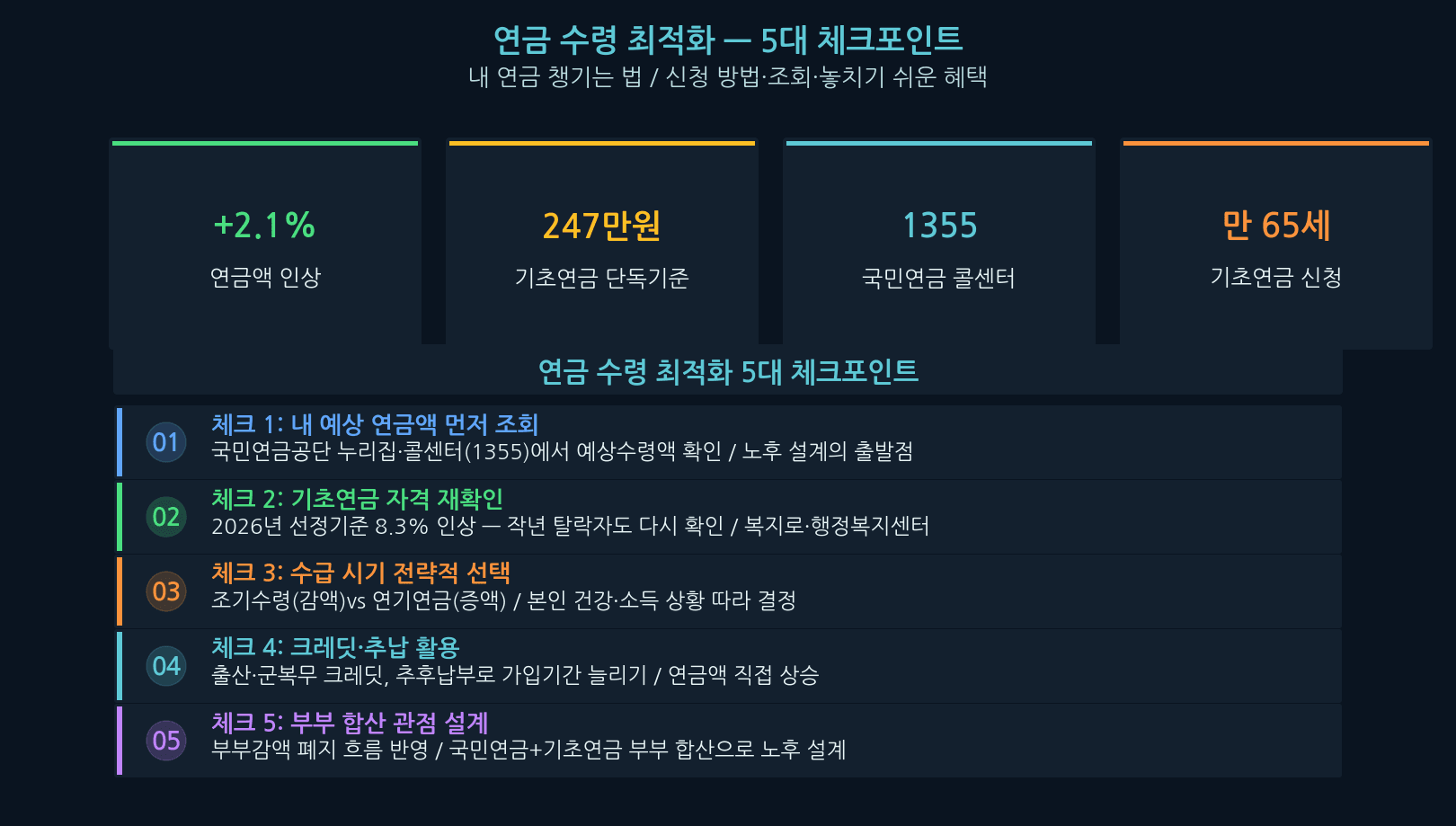

Pension claim optimization — five checkpoints

| Checkpoint | What to verify | How |

|---|---|---|

| 1. Estimated benefit | NP projected amount | NPS website · 1355 |

| 2. BP eligibility | Threshold +8.3% — re-check | Bokjiro · admin center |

| 3. Claim timing | Early vs deferred | Depends on health/income |

| 4. Credits / arrears | Childbirth, military, back-pay | Add contribution months |

| 5. Couple planning | Reflect couple-deduction phase-out | Plan NP + BP combined |

□ Re-check BP eligibility — threshold up 8.3%, re-apply if you missed before

□ Single ≤ KRW 2.47M / couple ≤ KRW 3.952M → BP eligible

□ Link-deduction guarantees ≥ 50% of BP — don’t believe the rumor

□ From June 17, income < KRW 5.09M/mo = full old-age pension

□ Use childbirth/military credits and back-payment to lift contribution months

□ Apply at admin centers, NPS branches, or bokjiro.go.kr

Sources

- MOHW — 2026 Basic Pension threshold notice (Jan 2026)

- MOHW — NP/BP +2.1% adjustment (Policy Briefing, Jan 2026)

- National Pension Service — Old-age pension monthly tables and program details (nps.or.kr)

- Ministry of Economy and Finance — 2026 economic growth strategy (income clawback relaxation, Jan 2026)

- KB Financial — 2026 National Pension average benefit summary (Mar 2026)

- NPS — NP Act amendment and fund projection materials

This article is for informational purposes based on official MOHW/NPS materials. Pension rules and amounts can change with legislation; the couple-deduction phase-out and similar items are confirmed via the legislative process. For your specific eligibility and benefit amount, verify with NPS (1355), local administrative centers, or Bokjiro.