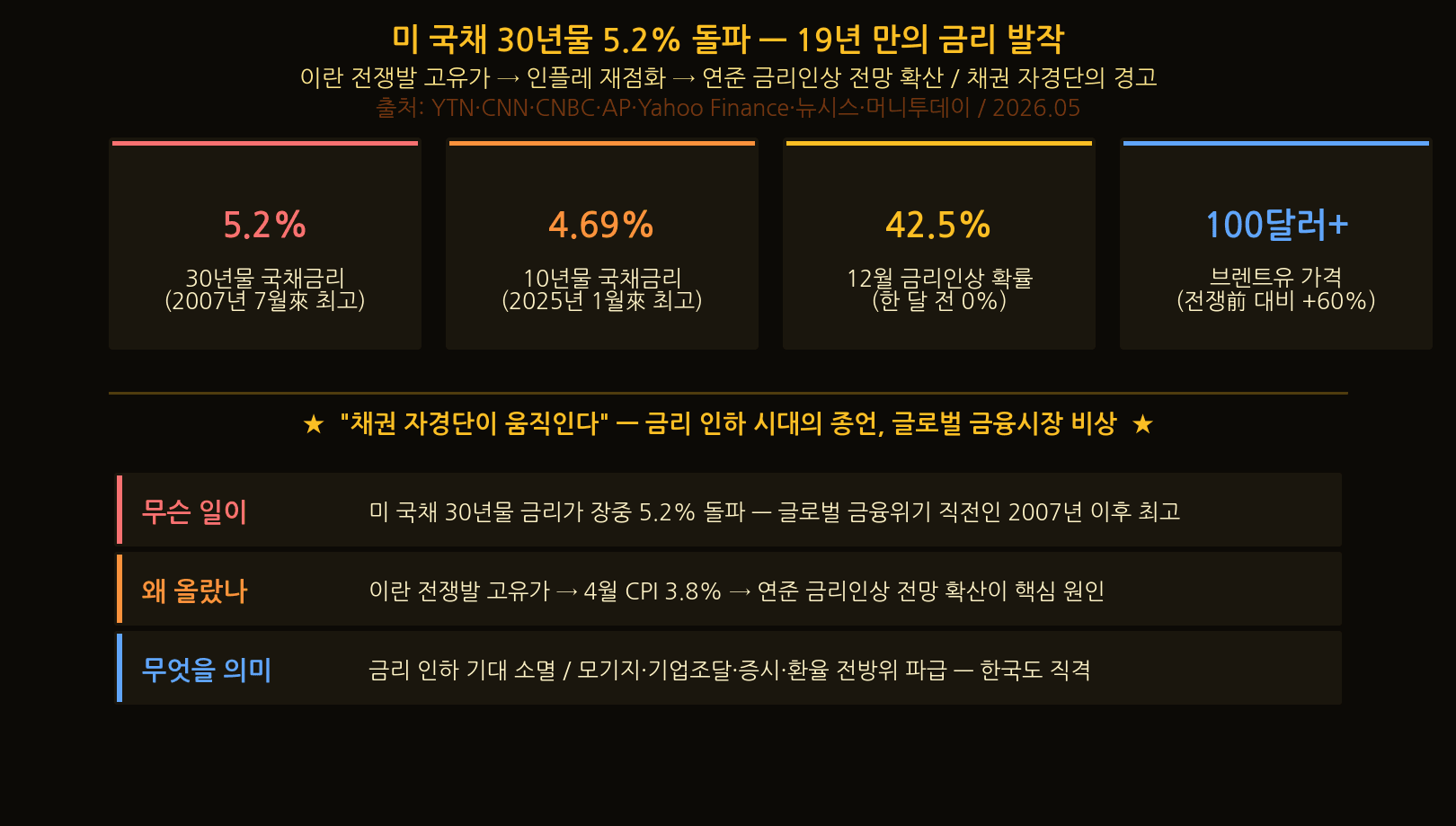

30-year Treasury yield tops 5.2% — A 19-year rate spasm, bond vigilantes, and Korea on the receiving end

Trending · May 24, 2026 · DIR

The 30-year Treasury yield just broke 5.2% — a level not seen in 19 years. The Fed cut rates by 1.75 points, yet long yields rose by more than 1 point. We unpack the return of the bond vigilantes, Chair Warsh’s dilemma, KOSPI’s -4.56% tumble, and what Korean investors should do next.

A 19-year first hit the US Treasury market. On May 19, the 30-year Treasury yield spiked to 5.2% intraday — the highest since July 2007, just before the global financial crisis. The 10-year benchmark also climbed to 4.69%, a new high since January 2025.

The truly shocking part is the direction. The Fed has cut policy rates by 1.75 percentage points since September 2024, but long Treasury yields have moved against that trend by more than a full point. The market is starting to say one thing: “the bond vigilantes are moving.” This is no longer a US-only story — it is a wake-up call for global markets, including Korea. The full chronology is laid out in CNBC’s coverage.

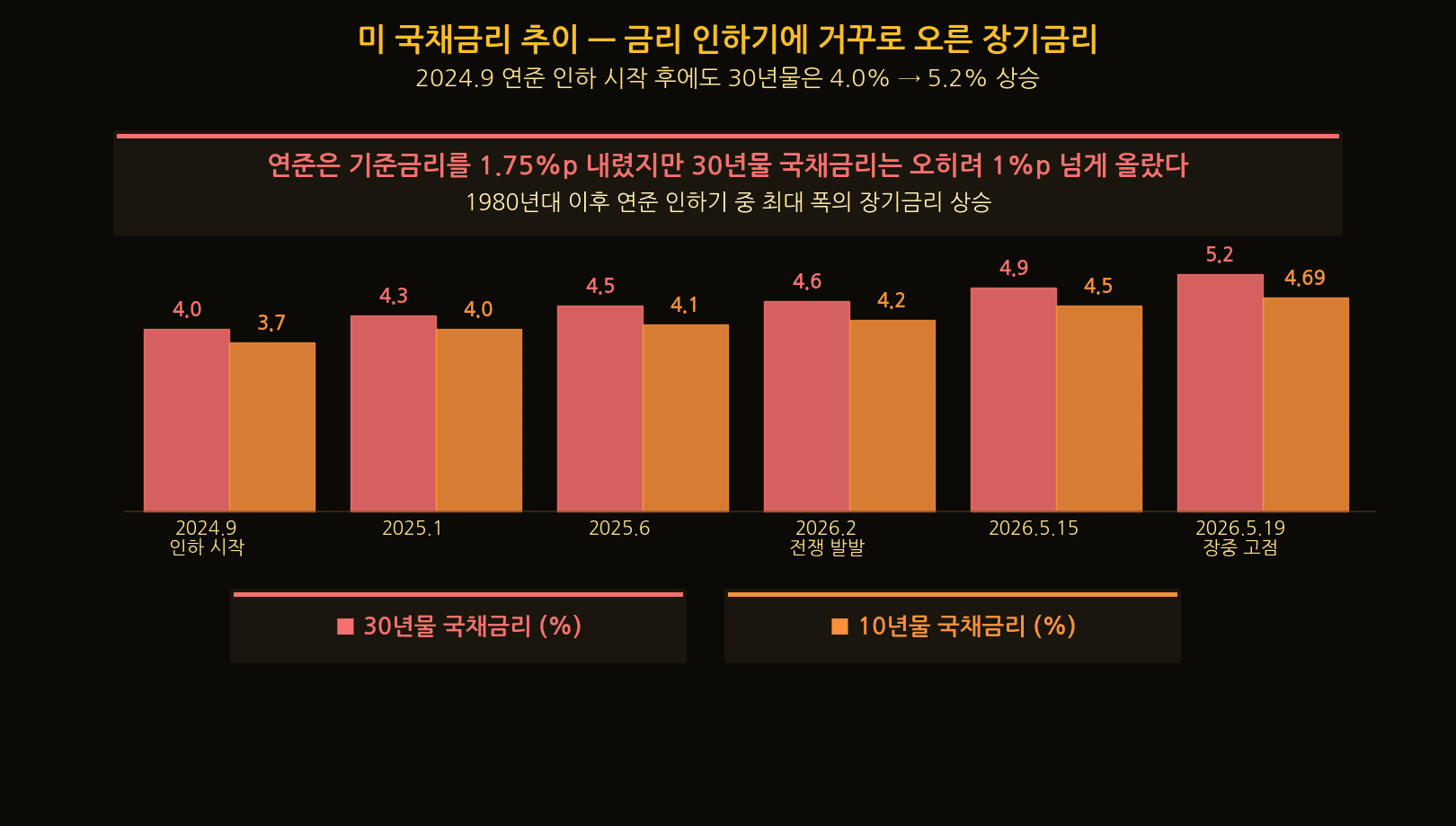

30-year Treasury yield path — long rates rose during a cutting cycle

The strangest feature here is a directional paradox. The Federal Reserve cut its policy rate from 5.25–5.5% to 3.5–3.75% — 1.75 percentage points in total — starting September 2024. Conventional wisdom says market rates should follow.

Instead, the 30-year Treasury yield climbed from roughly 4.0% to 5.2% — a more-than-1-point rise during a cutting cycle. Reports note this is the largest long-end backup seen during a Fed easing cycle since the 1980s. Even as the central bank loosens, the bond market refuses to follow.

| Date | 30Y | 10Y | Note |

|---|---|---|---|

| Sep 2024 (cuts begin) | ~4.0% | ~3.7% | End of Fed tightening |

| Feb 2026 (war) | ~4.6% | ~4.2% | Iran conflict |

| May 15, 2026 | ~4.9% | Breaks 4.5% | Key resistance breached |

| May 19, 2026 intraday | 5.2% | 4.69% | Highest since 2007 |

| May 22, 2026 close | 5.06% | 4.56% | Weekly close |

Even with policy rates cut by 1.75 points, the 30-year yield refused to follow.

— YTN · May 24, 2026

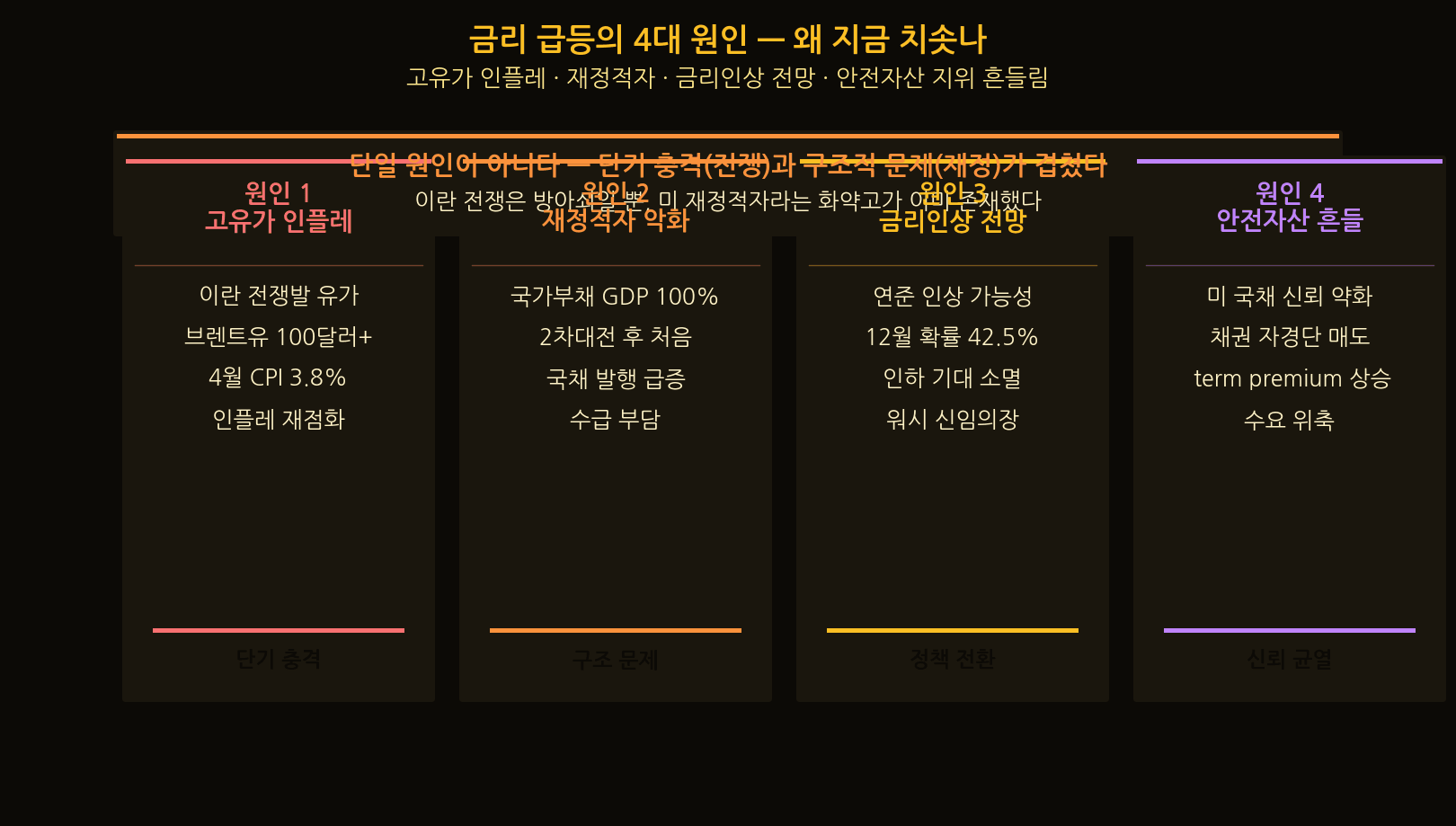

Four drivers behind the surge — why now

No single factor explains this rate spasm. Short-term shocks and structural problems are stacking up at once. The proximate trigger is the oil price shock from the Iran war: Brent crude broke $100 after the Strait of Hormuz blockade, lifting April CPI to 3.8%.

But the deeper fuse is US fiscal deterioration. Publicly held federal debt hit 100.2% of GDP at end-Q1 — a level not seen since just after World War II. As Treasury issuance keeps climbing, even the “safe-haven” status of US government debt is being called into question.

| Driver | Detail | Nature |

|---|---|---|

| Oil-driven inflation | Brent >$100, CPI 3.8% | Short-term shock |

| Fiscal deterioration | Public debt 100.2% of GDP | Structural |

| Hike expectations | ~42.5% odds of Dec hike | Policy turn |

| Safe-haven wobble | Bond vigilante selling | Trust fracture |

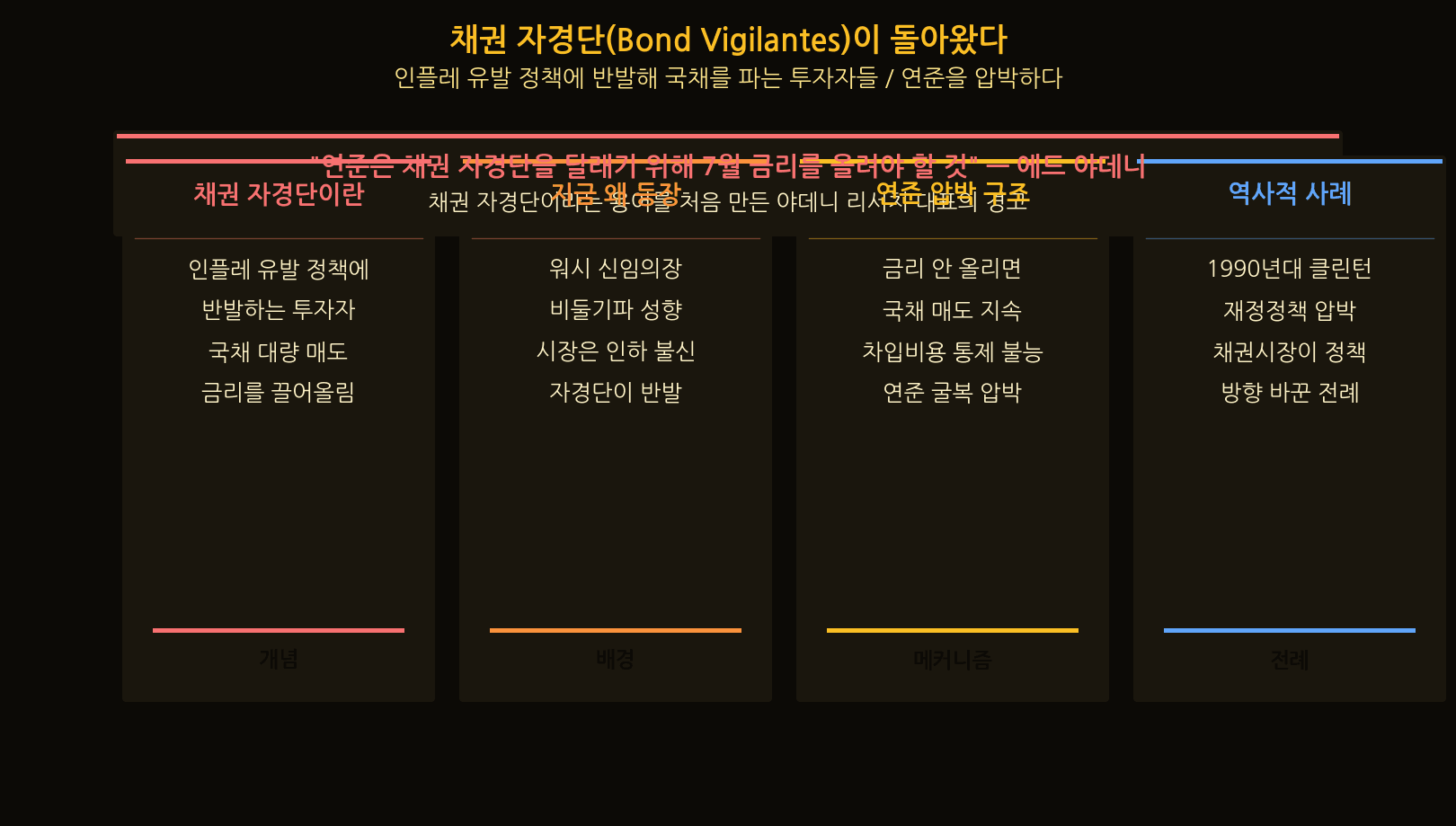

The bond vigilantes are back

The defining keyword of this episode is “bond vigilantes.” Coined in the 1980s, it refers to investors who push back against inflationary fiscal or monetary policy by dumping government bonds. When they sell, prices fall and yields rise — and that yield surge is, in effect, market discipline imposed on policymakers.

Asset manager Prime Capital says the vigilantes are clearly moving. Ed Yardeni, who originally coined the term, has gone further: the Fed, he argues, may have to raise rates simply to appease the bond market.

| Item | Detail |

|---|---|

| Who are bond vigilantes? | Investors who sell government debt to discipline inflationary policy |

| Mechanism | Sell bonds → price falls → yield rises → pressure on government |

| Why now | Market pushback against perceived dovishness of new Chair Warsh |

| Historical analogue | 1990s — disciplining the Clinton fiscal agenda |

The Fed will have to catch up with the market — to keep control of borrowing costs, and to appease the bond vigilantes.

— Ed Yardeni, Yardeni Research · CNBC · May 18, 2026

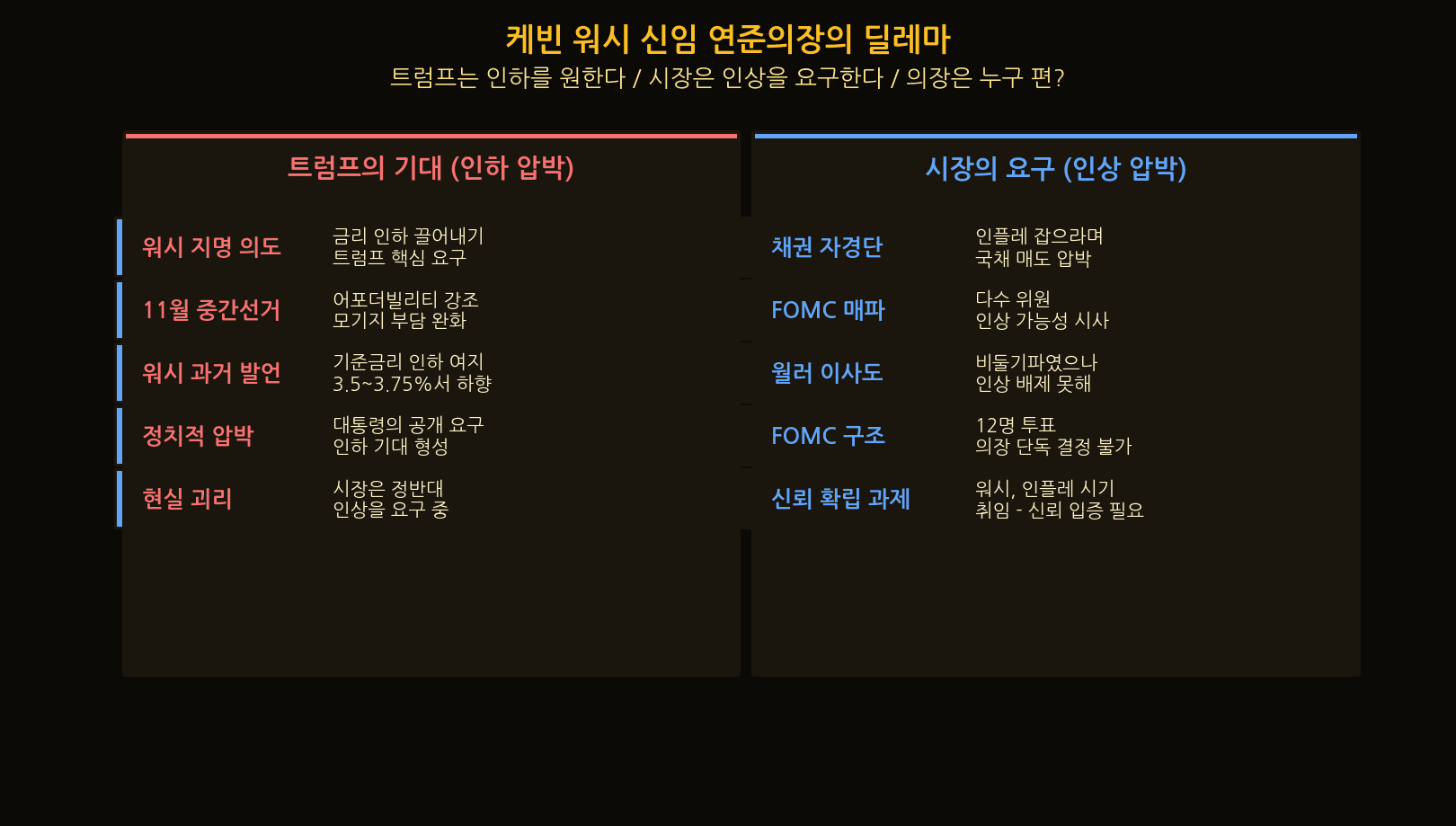

Chair Kevin Warsh’s dilemma

Sworn in on May 22, Federal Reserve Chair Kevin Warsh took office under heavy pressure. President Trump installed him with explicit expectations of rate cuts ahead of the November midterms, framing the move around mortgage relief and consumer “affordability.”

The market, however, is pulling in the opposite direction. Bond vigilantes are demanding tighter policy to contain inflation, and a majority of FOMC members lean hawkish. Even Governor Waller, long considered dovish, has not ruled out a rate hike. The Chair cannot decide alone — the FOMC votes with 12 members.

| Item | Trump’s expectation | Market demand |

|---|---|---|

| Direction | Cuts | Hikes |

| Backdrop | Midterms, mortgage stress | Inflation containment |

| Source | Political pressure | Bond vigilantes, FOMC hawks |

| Warsh’s stance | Hints at cut potential | Must first earn market trust |

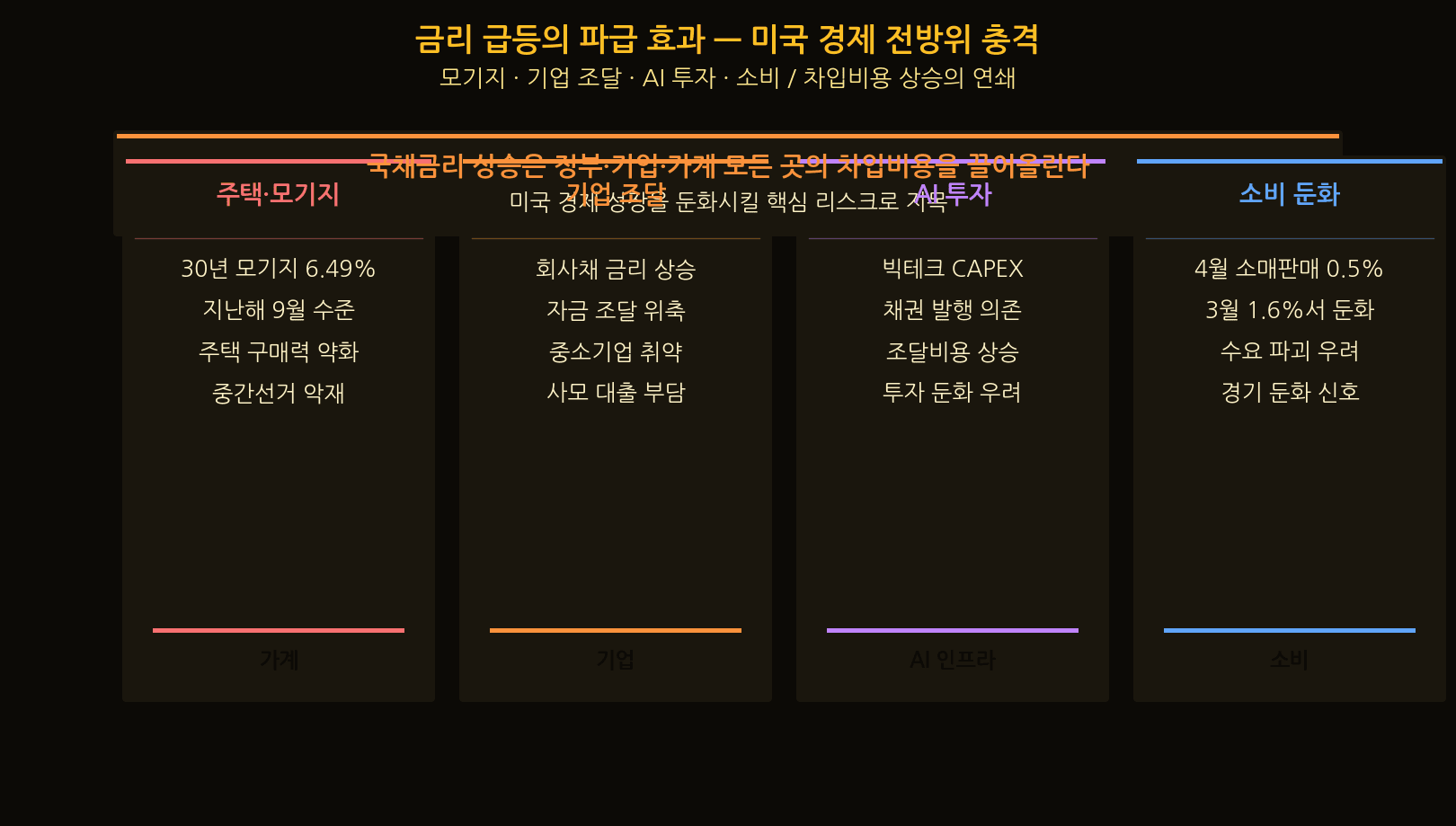

Ripple effects — borrowing costs across the US economy

Long-end yields are not abstract numbers. They push up borrowing costs for government, corporates, and households. For households, 30-year fixed mortgages reached 6.49%, crushing affordability. For a president heading into midterms, that is direct political damage.

Corporates also feel it. Big tech firms financing massive AI data-center buildouts rely on bond issuance, and higher yields mean higher funding costs. There is growing concern that AI capex, the engine of recent US growth, will slow. April retail sales rose only 0.5%, down sharply from March’s 1.6%. For broader macro data, see the FT Markets desk.

| Area | Impact | Channel |

|---|---|---|

| Housing & mortgages | 30Y mortgage 6.49% | Affordability hit |

| Corporate funding | Higher IG yields | Capex tightens |

| AI capex | Big-tech funding cost up | Slowdown risk |

| Consumption | April retail sales +0.5% | Demand destruction risk |

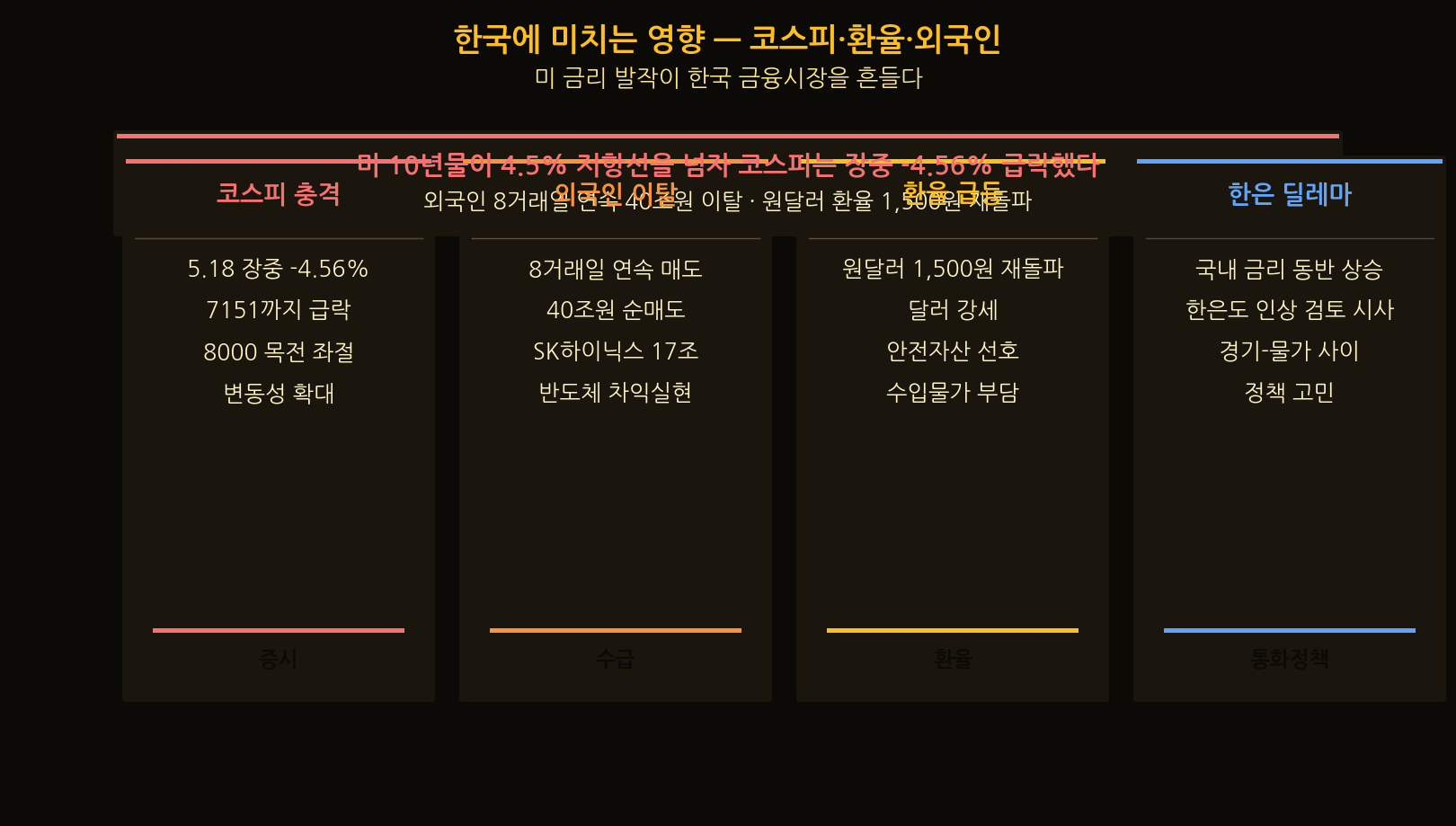

Korea on the receiving end — KOSPI, FX, foreign flows

America’s rate spasm directly rattled Korean markets. Once the US 10-year cleared its psychological 4.5% level, the KOSPI plunged 4.56% intraday on May 18, falling all the way to 7,151, after flirting with 8,000.

Foreign outflows have been heavy. Reports show foreigners net-sold for eight straight sessions, dumping roughly KRW 40 trillion — including nearly KRW 17 trillion in SK Hynix alone after its big rally. The KRW/USD rate punched back above 1,500 on safe-haven flows. The Bank of Korea is hinting that its cutting cycle may need to pause — and even reverse.

| Area | Korea impact | Detail |

|---|---|---|

| KOSPI | May 18 intraday -4.56% | Fell to 7,151 |

| Foreign flows | 8 sessions of net selling | ~KRW 40T outflow |

| FX | USD/KRW back above 1,500 | USD strength |

| Bank of Korea | Hike on the table | Policy regime shift |

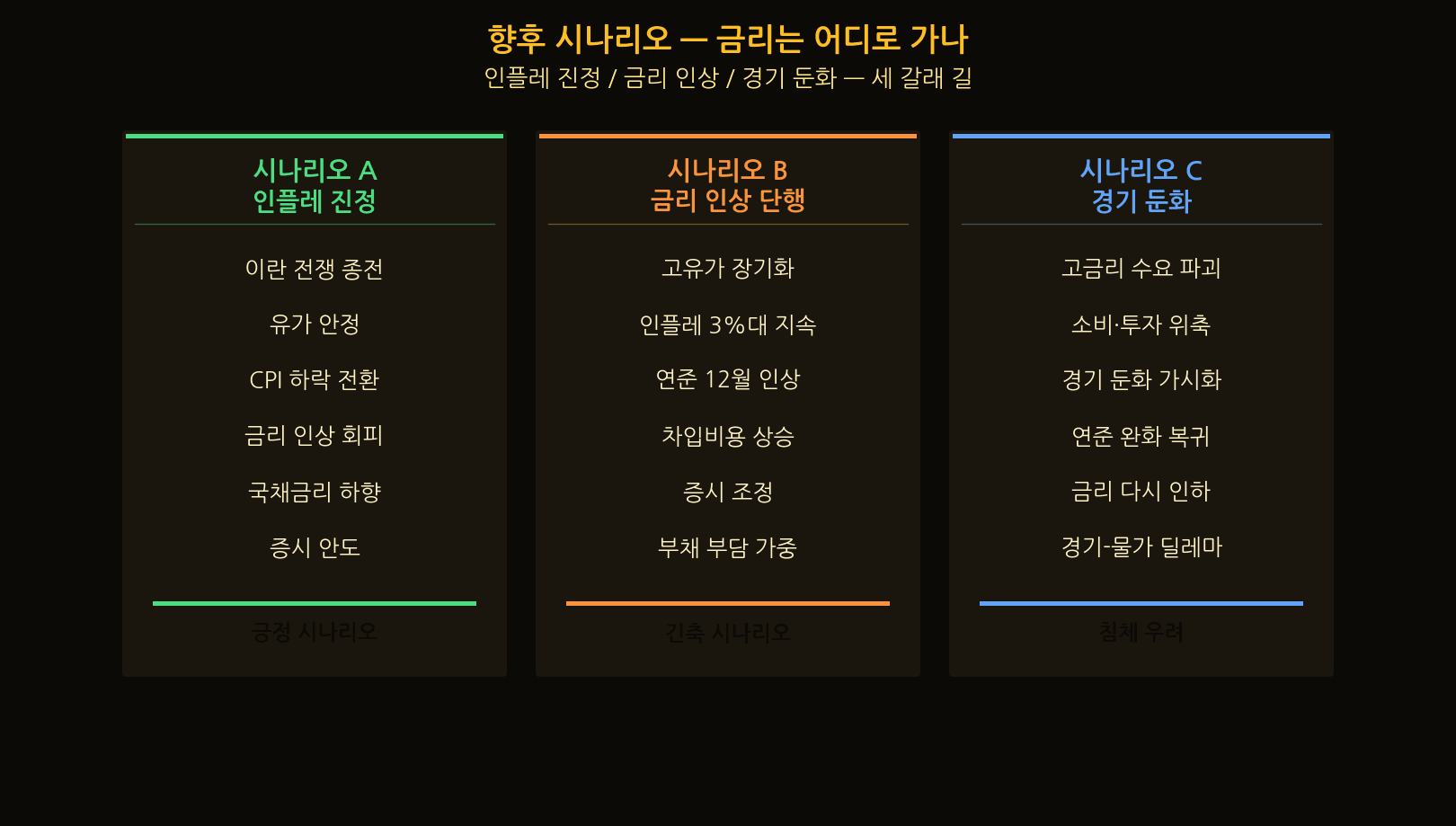

Scenarios — where do yields go from here

The path forward splits into three scenarios. First, inflation cools — if the Iran war winds down and oil stabilizes, CPI rolls over and the Fed can avoid a hike.

Second, the Fed actually hikes — if higher oil persists and CPI sticks in the 3% range, a December hike becomes plausible. Third, growth breaks — if higher yields crush consumption and capex, recession fears could push the Fed back toward easing, but this just deepens the “growth vs. inflation” dilemma.

| Scenario | Setup | Direction |

|---|---|---|

| A. Inflation cools | War ends, oil stabilizes | Yields fall |

| B. Fed hikes | High oil, sticky CPI | Hike |

| C. Growth breaks | High yields crush demand | Possible return to easing |

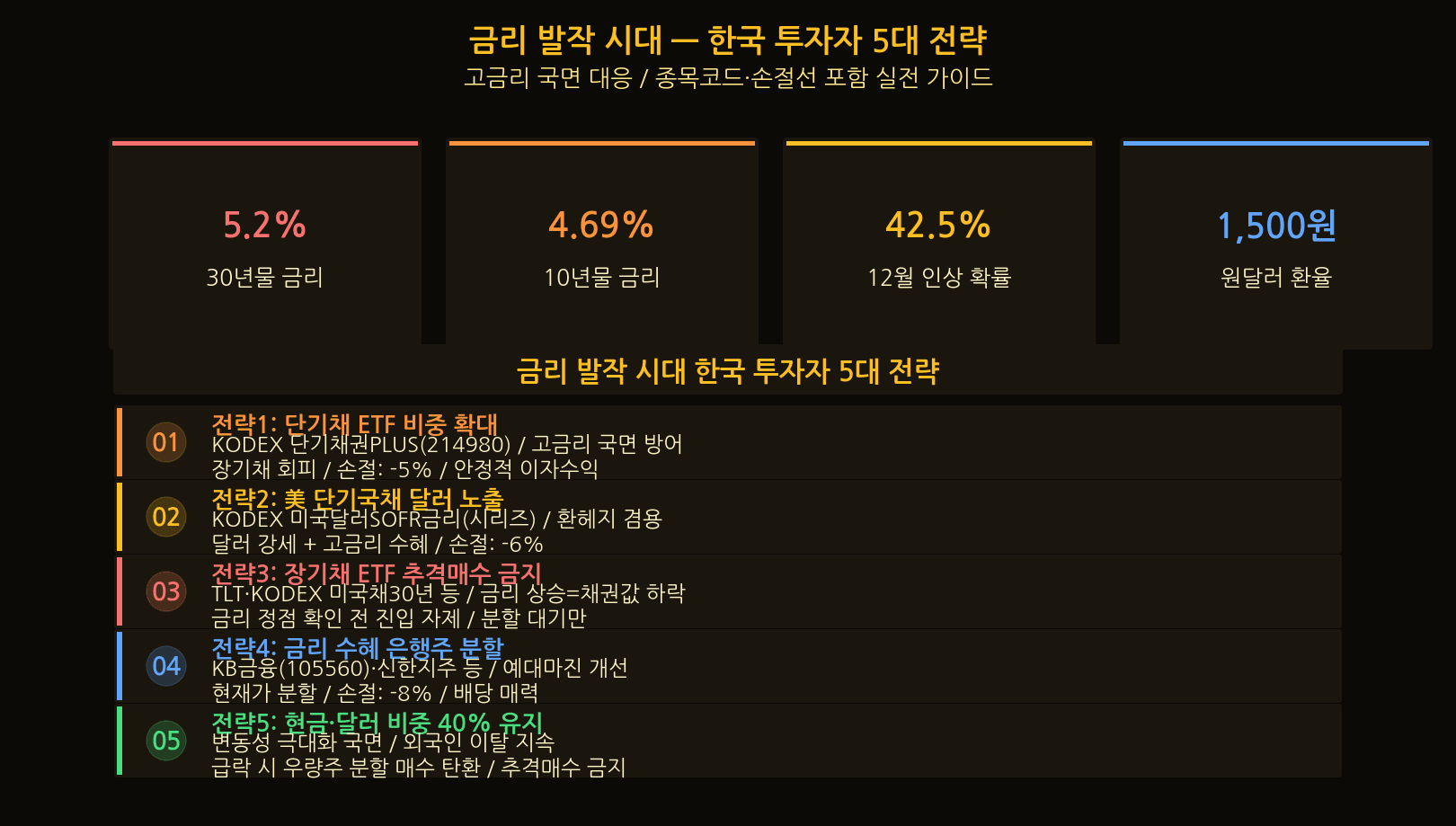

Five investor moves for a rate-spasm era

| Move | Vehicle | Code | How to play | Stop | Weight |

|---|---|---|---|---|---|

| 1. Short-duration KRW | KODEX Short-term Bond PLUS | 214980 | Defend against high rates | -5% | 20% |

| 2. USD short rate | KODEX USD SOFR series | — | FX hedge + yield | -6% | 15% |

| 3. Avoid long duration | UST 30Y ETFs | — | Wait for rate peak | Stand aside | Wait |

| 4. Banks | KB Financial | 105560 | NIM beneficiary, scale in | -8% | 10% |

| 5. Cash & USD | Cash buffer | — | Buy quality on dips | — | 40% |

□ No chasing long-duration ETFs — higher yields = lower bond prices

□ Defend with short-duration KRW and USD instruments

□ Scale into rate-beneficiary sectors like banks

□ Watch KOSPI outflows and the 1,500 KRW/USD line

□ Keep 40% cash/USD as dry powder for quality dips

Sources

- YTN — US 30-year Treasury hits 5.2% intraday; hike expectations spread (May 24, 2026)

- CNN Business — 30-year US Treasury yield hits highest level in 19 years (May 19, 2026)

- CNBC — 30-year Treasury yield tops 5.19%, highest since before the financial crisis (May 19, 2026)

- CNBC — The Fed will have to raise interest rates to appease bond vigilantes, Yardeni says (May 18, 2026)

- Newsis — Foreign outflow fears rise as US Treasury yields spike (May 18, 2026)

- Money Today — Oil, yields, FX surge together; KOSPI under pressure (May 18, 2026)

This article is for informational purposes only and does not recommend any specific security. Rates, FX, and equity prices change constantly; verify current data independently. Investors bear sole responsibility for their decisions.

![[Breaking 21:30 KST] US April CPI 3.8% — oil spike kills Fed rate-cut bets](https://getdir.app/wp-content/uploads/2026/05/01_cpi_trend-768x380.png)