SK Hynix Enters 1 Trillion Dollar Club — Asia’s 3rd 5 Analyses and Strategies

SK Hynix Enters 1 Trillion Dollar Club — Asia’s 3rd 5 Analyses and Strategies

SK Hynix crossed the \$1 trillion market-cap mark on May 27, 2026, becoming the 3rd Asian company to enter the trillion-dollar club (after TSMC and Samsung Electronics). Alongside Micron’s +20% surge on 5/26~27 signaling a memory cycle recovery, SK Hynix rallied ~10% to drive KOSPI to a record 8228.70.

This article synthesizes Hankyung, Edaily, Bloomberg market-cap data, and SK Hynix IR to cover SK Hynix market-cap trajectory (2020~2026), Asian trillion-dollar club comparison, dominant 50% HBM market share, earnings trajectory (2022~2026E), 5 drivers of \$1T entry, \$2T scenarios, 5 risks, and 5 investment strategies. SK Hynix IR at SK Hynix.

| Item | Value | Notes |

|---|---|---|

| Breakthrough Date | 2026.05.27 | Historic KOSPI event |

| Market Cap | ~\$1 trillion (~1,300T KRW) | Asia’s 3rd entrant |

| Ranking | 1st TSMC, 2nd Samsung, 3rd SK Hynix | Korea memory dominance |

| HBM Share | 50% (dominant #1) | Nvidia main supplier |

| Same-day Co-Rally | Micron +20% + KOSPI +2.25% | Memory cycle signal |

| 2026E Op. Income | ~40~55T KRW estimated | All-time high |

| 12M Target | \$1.5T (base scenario) | +50% upside |

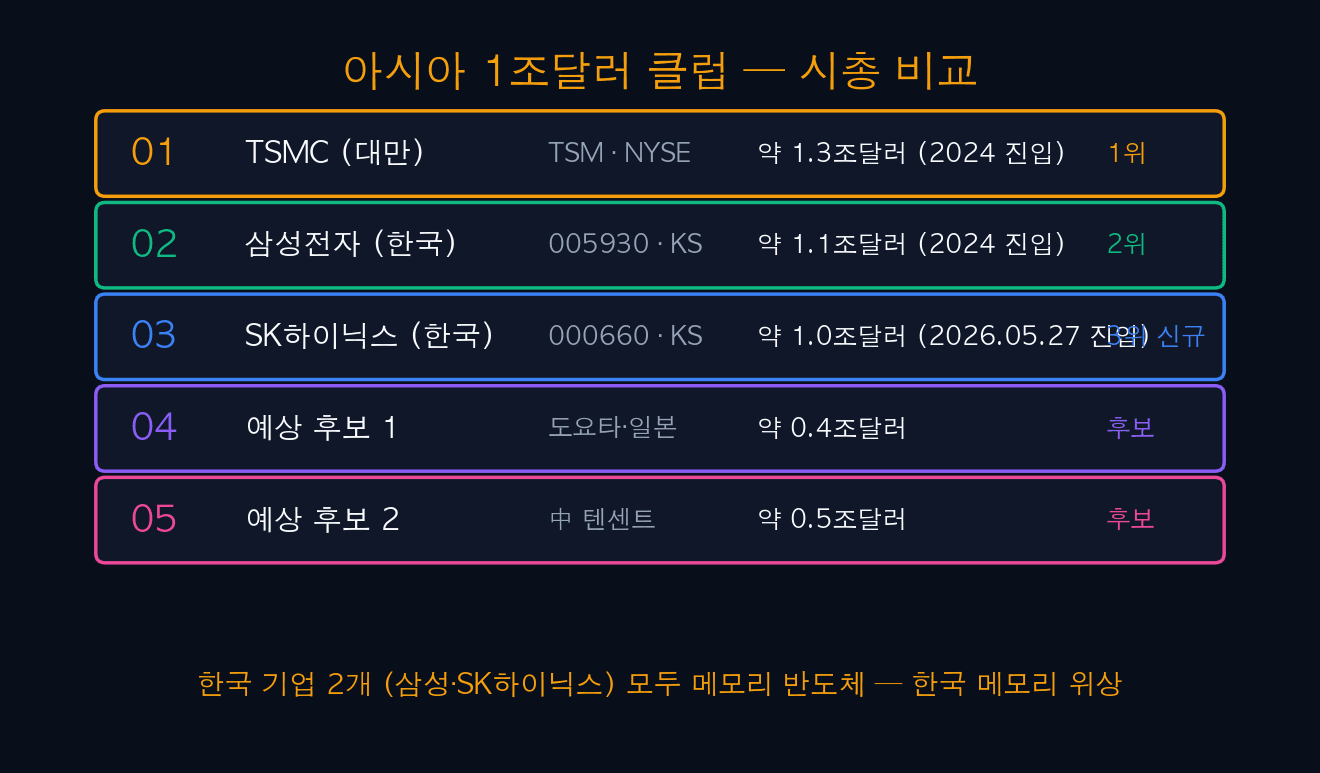

01Asian \$1 Trillion Club — Market Cap Comparison

SK Hynix crossed \$1 trillion market cap on May 27, 2026, becoming the 3rd Asian company in the \$1T club. After 1st TSMC (~\$1.3T, entered 2024) and 2nd Samsung Electronics (~\$1.1T, 2024). With 2 Korean companies included, Korea’s global memory industry status is now firmly established.

Next \$1T candidates include Toyota (~\$0.4T) and Tencent (~\$0.5T), but reaching \$1T short-term is difficult. SK Hynix’s entry isn’t a single event but the result of AI HBM surge + memory cycle recovery + Korean semi positioning combined, doubled by Micron’s same-day +20% surge for major market impact.

| Rank | Company | Market Cap | Entry | Notes |

|---|---|---|---|---|

| 1 | TSMC (TSM·Taiwan) | ~\$1.3T | 2024 | AI foundry #1 |

| 2 | Samsung Electronics (KS) | ~\$1.1T | 2024 | DRAM #1 |

| 3 | SK Hynix (KS) | ~\$1.0T | 2026.05.27 | HBM #1 |

| Candidate 1 | Toyota (TM·Japan) | ~\$0.4T | — | Global auto #1 |

| Candidate 2 | Tencent (700·China) | ~\$0.5T | — | China big tech |

iINFO — Significance of 2 Korean Companies

Two Korean companies (Samsung + SK Hynix) in the \$1T club means Korea effectively dominates global memory. Korea combined DRAM share is 72%, and HBM 90% (near monopoly). \$1T entry is more than market cap — it’s certification of “global top-tier in tech, market, and capital“.

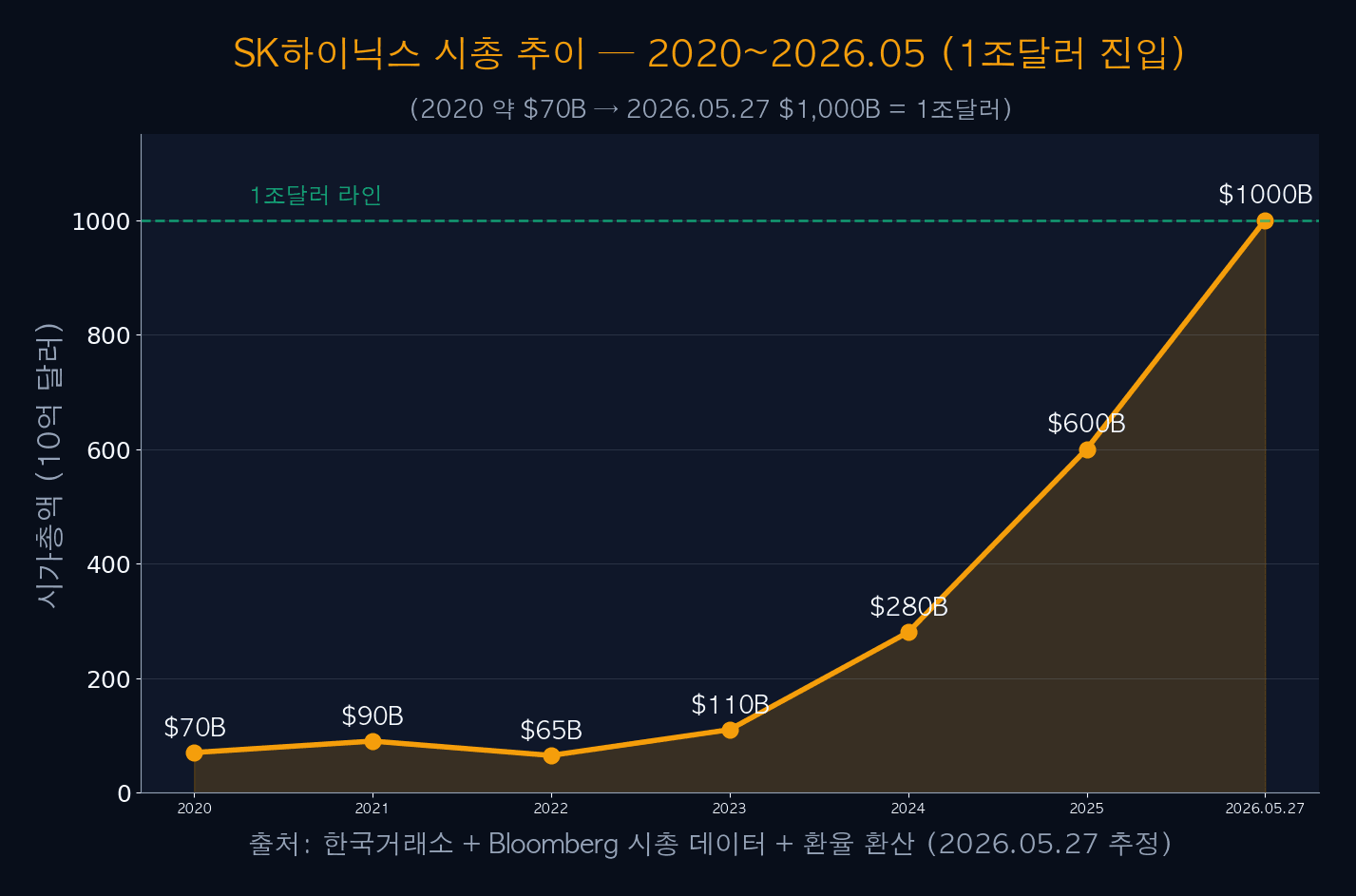

02SK Hynix Market Cap Trajectory — 2020~2026 (14x growth)

SK Hynix market cap rose from ~\$70B in 2020 to ~\$1T on 2026.05.27 — about 14x growth over 6 years. After dropping to \$65B in 2022 due to memory cycle bust, it recovered in 2023, then 2024 \$280B → 2025 \$600B → 2026 \$1T — a steep ascent.

The steepest 2024~2026 climb is driven by AI HBM surge. With SK Hynix HBM3·HBM3E supplied as main memory to Nvidia H100·H200·B100 etc., HBM revenue (selling at 5~7x regular DRAM prices) surged, exploding operating margins. The 5/27 \$1T crossing is both peak of this flow and a new starting point.

| Year | Market Cap ($B) | Growth | Key Event |

|---|---|---|---|

| 2020 | 70 | Baseline | COVID + memory recovery |

| 2021 | 90 | +29% | Memory cycle entry |

| 2022 | 65 | -28% | Cycle bust |

| 2023 | 110 | +69% | Recovery + AI emergence |

| 2024 | 280 | +155% | AI HBM in earnest |

| 2025 | 600 | +114% | HBM #1 established |

| 2026.05.27 | 1,000 | +67% | \$1T breakthrough |

03HBM Market Share — SK Hynix 50% Dominant #1

In the HBM (High Bandwidth Memory) market, SK Hynix holds a ~50% dominant #1 share. Samsung (40%) and Micron (10%) follow, but SK Hynix’s technology leadership and Nvidia partnership are hard to catch short-term. This 50% HBM share is the decisive driver of \$1T market cap entry.

SK Hynix was first to mass-produce HBM3E and leads in next-gen HBM4. Nvidia’s next-gen AI chips (Blackwell·Rubin) use SK Hynix HBM as main supply. As AI datacenter infrastructure expands, SK Hynix benefits proportionally.

| Company | HBM Share | HBM3E Mass-Prod | HBM4 Dev | Main Customers |

|---|---|---|---|---|

| SK Hynix 000660 | 50% | Lead (2024) | Lead | Nvidia·AMD |

| Samsung 005930 | 40% | 2025 starts | Catching up | Google·MSFT |

| Micron MU | 10% | 2025 entry | Developing | Meta·Amazon |

| China (CXMT) | 0% | — | Developing | — |

!WARNING — HBM Competition Intensifies

SK Hynix is dominant at 50% but Samsung and Micron are ramping HBM3E and HBM4 mass production, intensifying competition. By 2027~2028, share could split SK 40% / Samsung 40% / Micron 20%. Maintaining \$1T requires keeping HBM4·HBM5 technology leadership.

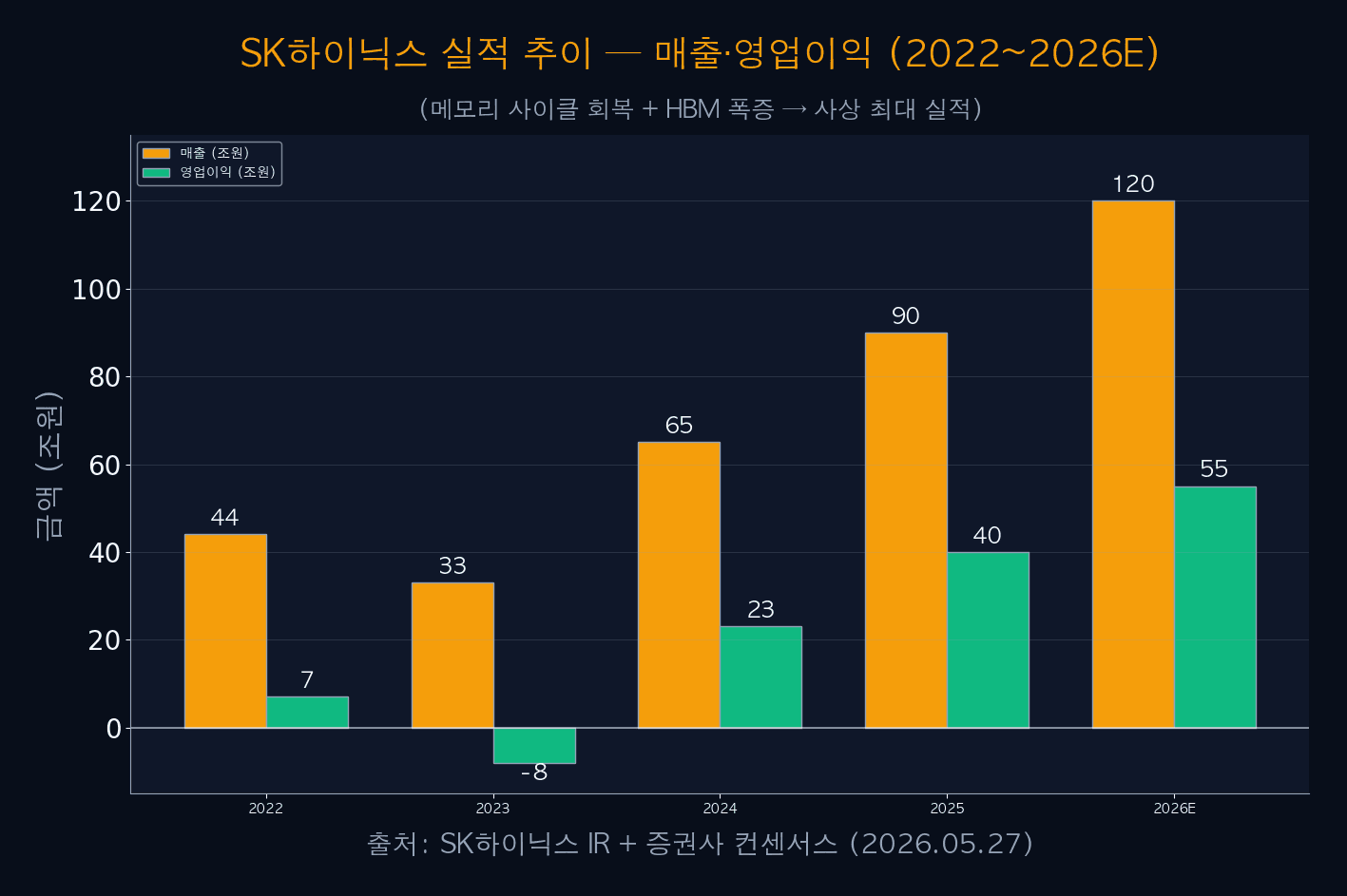

04SK Hynix Earnings — All-Time High Revenue·Op. Income

SK Hynix earnings: 2022 44T revenue / 7T op. income, sharply declined in 2023 (33T / -8T op. loss) due to cycle bust, then V-recovery in 2024 to 65T / 23T. 2025E 90T / 40T, and 2026 expected 120T revenue / 55T op. income — all-time high.

This reflects HBM revenue share expanding to 30%+ with op. margin at record ~45%. Compared to regular DRAM (20~30% op. margin), HBM is 50%+ margin high-end product. This earnings growth underpins the \$1T market cap fundamentals — and is the key driver for the \$2T scenario.

| Year | Revenue (T KRW) | Op. Income (T KRW) | Op. Margin | Notes |

|---|---|---|---|---|

| 2022 | 44 | 7 | 16% | Pre-cycle peak |

| 2023 | 33 | -8 | -24% | Cycle bust |

| 2024 | 65 | 23 | 35% | V-recovery |

| 2025 | 90 | 40 | 44% | HBM in earnest |

| 2026E | 120 | 55 | 46% | All-time high |

iINFO — 46% Op. Margin Meaning

2026E 46% op. margin places SK Hynix among the top of all global semi companies. TSMC is ~40%s, Nvidia ~60%s — SK Hynix is closing on this level. This reflects “HBM effectively becoming an AI infra monopoly part” with strong pricing power.

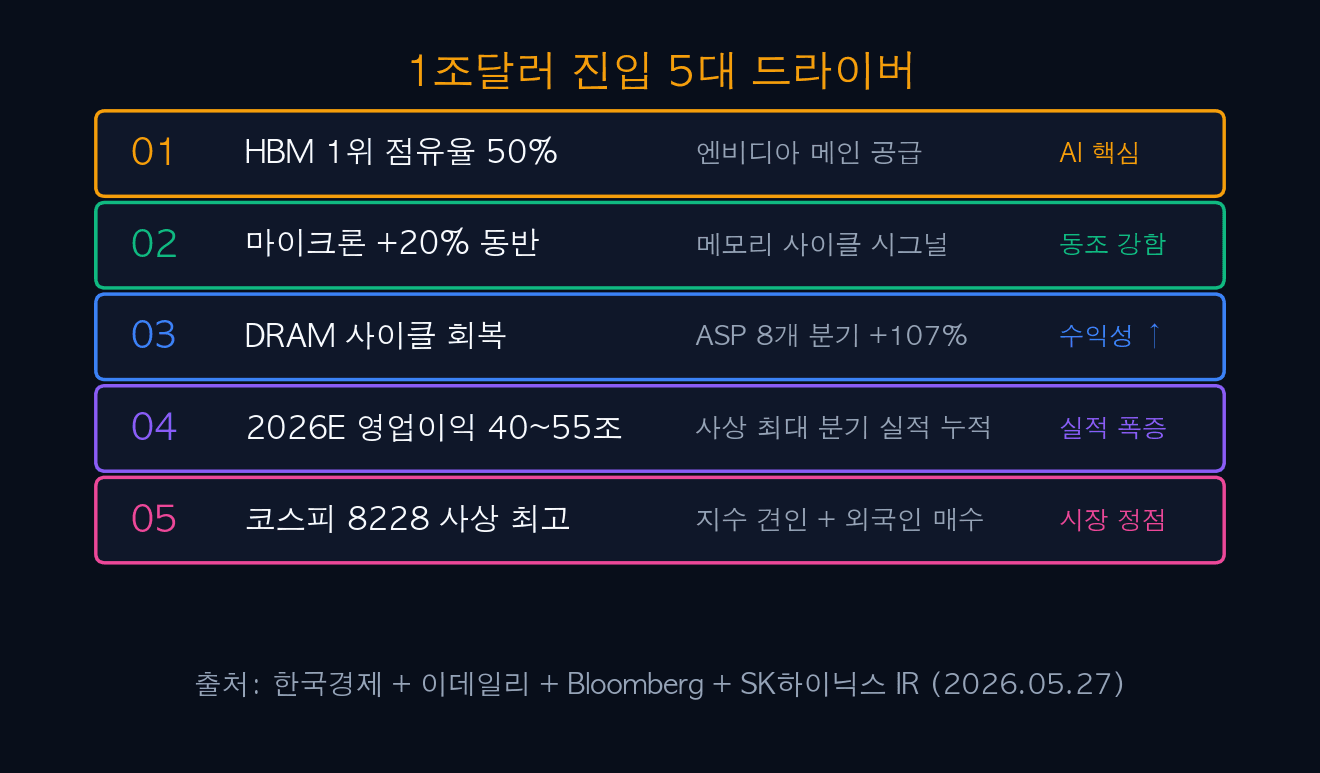

055 Drivers of \$1T Entry

SK Hynix \$1T entry is the result of 5 simultaneous drivers. HBM 1st 50% share, Micron +20% co-rally, DRAM cycle recovery, 2026E all-time high op. income, KOSPI 8228 record high.

The most decisive is 50% HBM share. Being Nvidia AI chip’s main memory drove revenue and margin together. Micron’s 5/27 +20% surge sent a memory cycle signal, with SK Hynix rallying alongside to cross \$1T. Symbolic meaning: “Korean memory leads the global cycle“.

| Driver | Core Content | Strength |

|---|---|---|

| 1. HBM 1st 50% Share | Nvidia main supply | Very Strong |

| 2. Micron +20% Co-Rally | Memory cycle signal | Very Strong |

| 3. DRAM Cycle Recovery | ASP 8 quarters +107% | Strong |

| 4. 2026E Op. Income 55T | All-time high earnings | Strong |

| 5. KOSPI 8228 Record | Index lift + foreign buying | Moderate |

| 6. Global AI Paradigm | AI datacenter expansion | Strong |

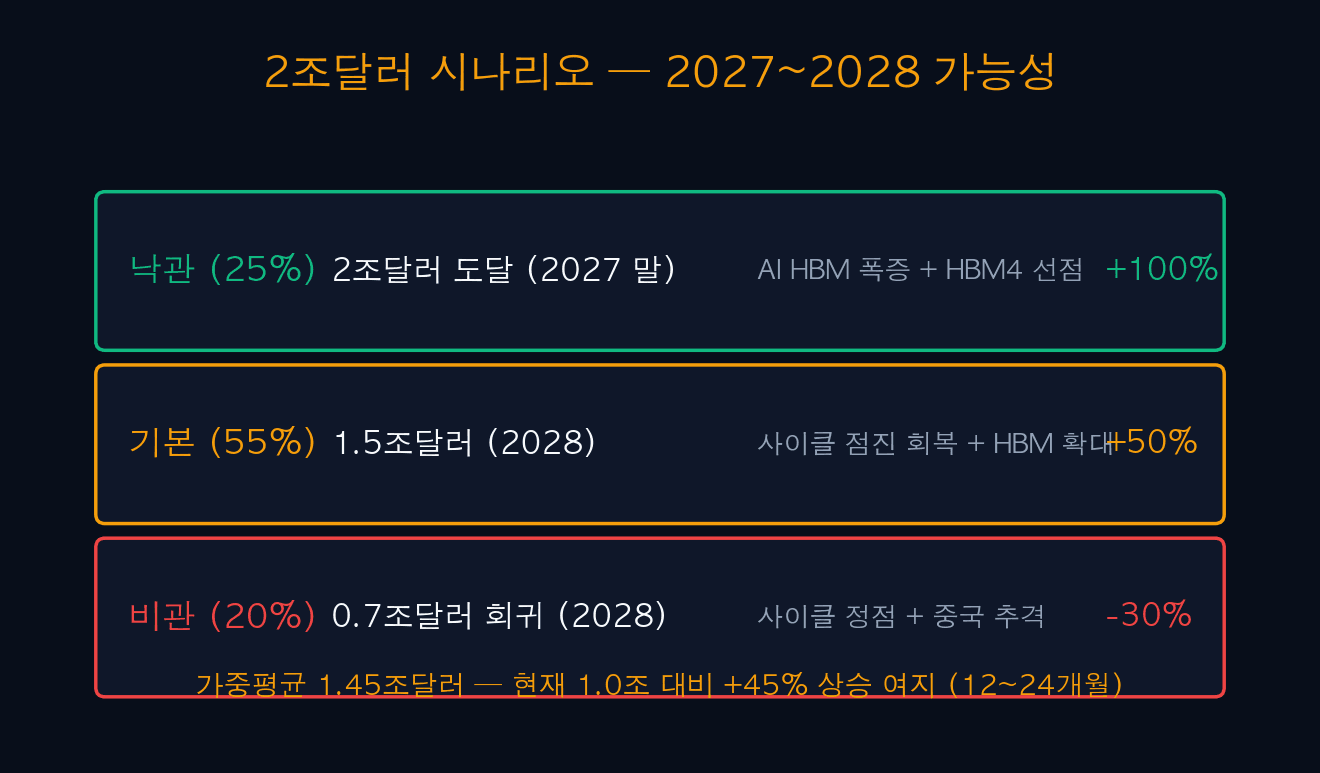

06\$2T Scenarios — 2027~2028 Possibilities

12~24 month market cap scenarios for SK Hynix: Bull \$2T (25%) / Base \$1.5T (55%) / Bear \$0.7T (20%). Weighted average ~\$1.45T = ~+45% upside from current \$1T.

Bull assumes AI HBM surge through 2027 + SK Hynix HBM4 leadership. Bear assumes cycle peak reversion + China memory catch-up. Base is most likely — balancing AI infra expansion and HBM competition intensification.

| Scenario | Target Market Cap | Target Date | Conditions | Probability |

|---|---|---|---|---|

| Bull | \$2T | End-2027 | AI HBM surge + HBM4 lead | 25% |

| Base | \$1.5T | End-2028 | Gradual recovery + HBM | 55% |

| Bear | \$0.7T | End-2028 | Cycle peak + China catch-up | 20% |

| Weighted | \$1.45T | — | Probability-weighted | — |

✓TIP — \$2T Entry Conditions

For \$2T entry, 3 simultaneous conditions: (1) HBM4 mass-prod lead + 50%+ share maintained, (2) AI HBM revenue share expanding to 50%+, (3) Op. margin 50%+ maintained. 2+ of these signals bull scenario.

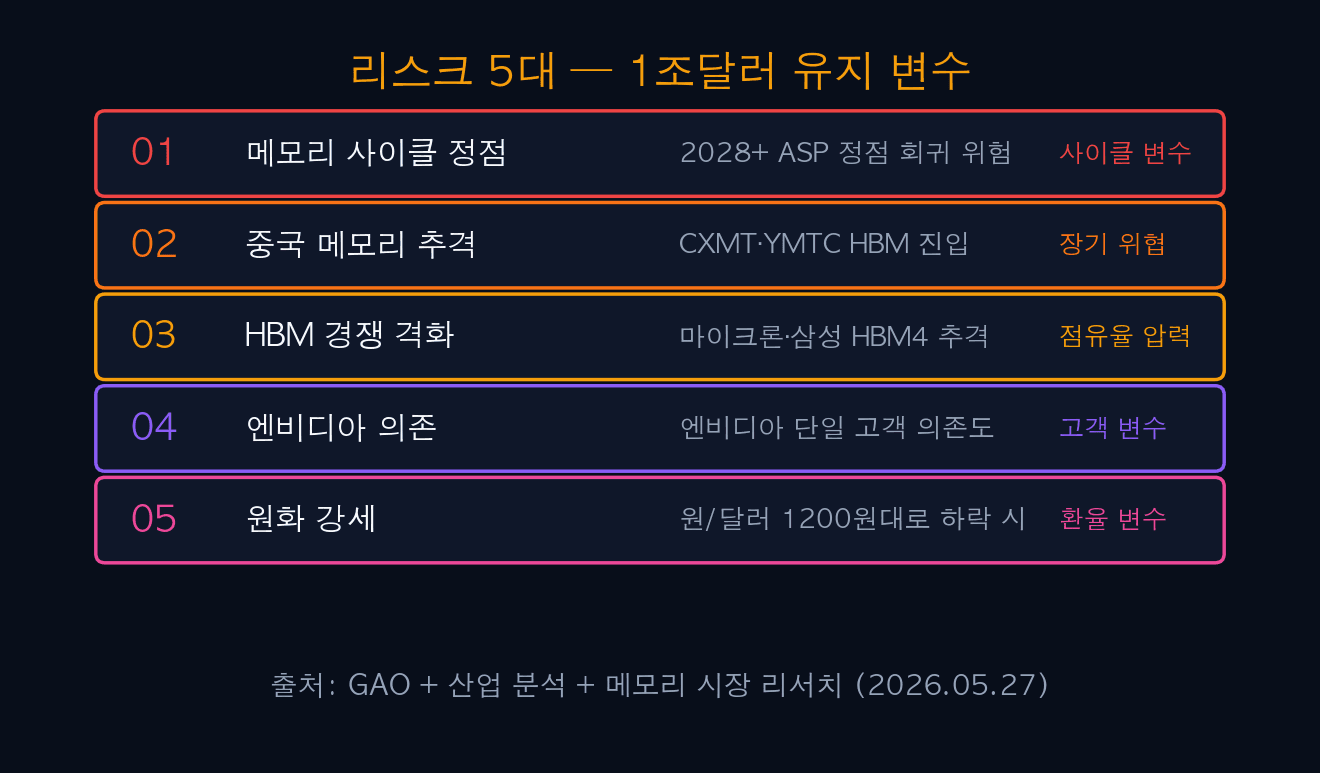

075 Risks — \$1T Maintenance Variables

\$1T market cap is a big catalyst but maintenance isn’t guaranteed. Memory cycle peak, China memory catch-up, HBM competition, Nvidia dependency, KRW strength are 5 risks. 2027~2028 could see these materialize simultaneously.

The biggest risk is “Nvidia single-customer dependency”. A large share of SK Hynix HBM revenue concentrates on Nvidia, making Nvidia’s adoption changes or unit-price negotiations directly impact SK Hynix earnings. Fortunately AMD·Intel·Google·MSFT customer diversification is in progress, but short-term dependency remains high.

| Risk | Scenario | Impact |

|---|---|---|

| 1. Memory Cycle Peak | 2028+ ASP peaks and reverts | Market cap -30% |

| 2. China Memory Catch-Up | CXMT·YMTC HBM entry | Long-term share threat |

| 3. HBM Competition | Micron·Samsung HBM4 catch-up | Share 50% → 40% |

| 4. Nvidia Dependency | Single-customer dependency | Diversification needed |

| 5. KRW Strength | USD/KRW to 1,200 | Translation drag |

| 6. AI Bubble | AI demand slowdown hits HBM | Demand variable |

⚠ALERT — \$1T Maintenance Key Indicators

3 indicators to monitor for \$1T maintenance: (1) HBM share 50%+ maintained (TrendForce quarterly), (2) Op. margin 40%+ maintained (quarterly earnings), (3) Nvidia next-gen AI chip adoption (Blackwell·Rubin·Vera). If any deteriorates, review \$1T departure risk.

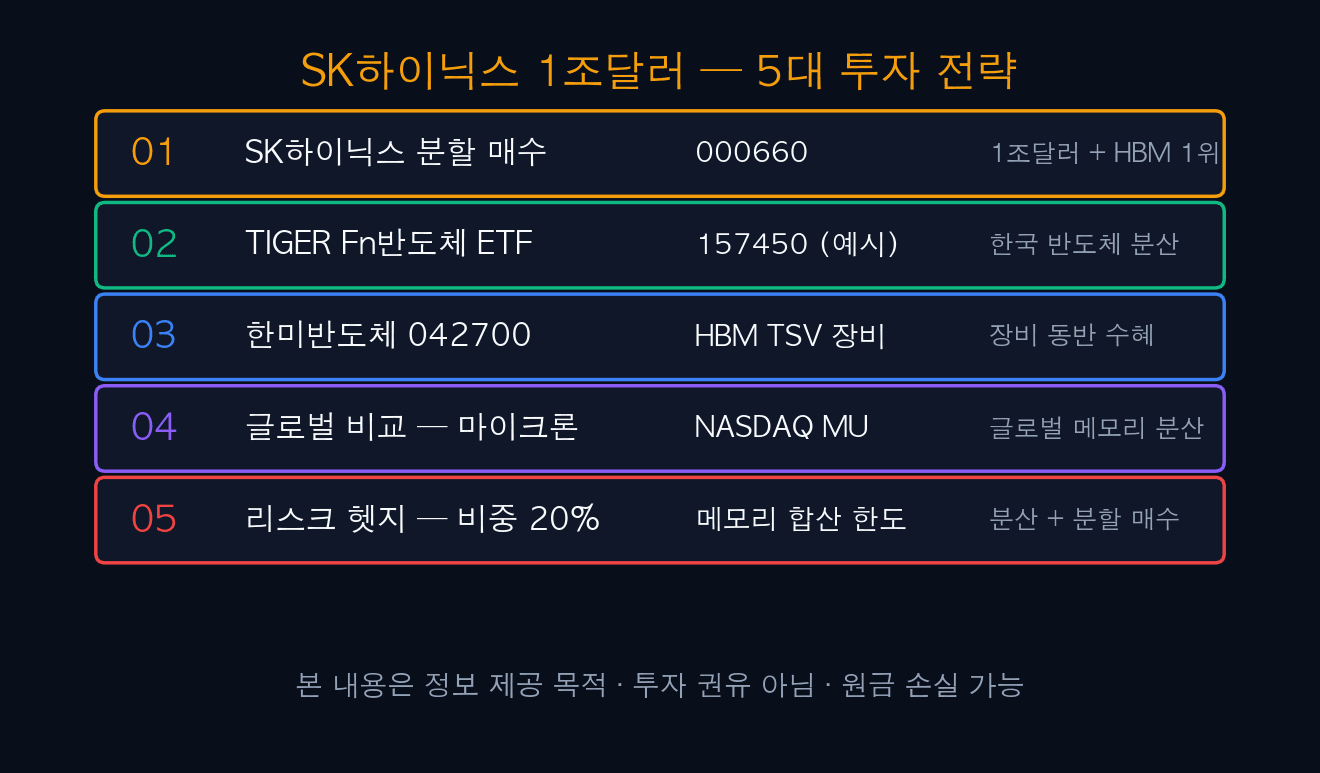

08SK Hynix \$1T — 5 Investment Strategies

Five strategies for SK Hynix \$1T entry: SK Hynix phased buying + TIGER Fn Semi ETF + Hanmi Semi + Micron + risk hedge. Single position 5~10%, memory combined ≤25% caps.

| Strategy | Ticker | Allocation | Rule |

|---|---|---|---|

| S1: SK Hynix | 000660 | 5~10% | -12% stop |

| S2: TIGER Semi | ETF | 5% | -10% stop |

| S3: Hanmi Semi | 042700 | 3% | -15% stop |

| S4: Micron | MU | 3% | -12% stop |

| S5: Risk Hedge | Combined 25% / Cash 20% | Cap | Diversify + phased |

- Date: 2026.05.27 · Asia’s 3rd \$1T club entry

- Ranking: 1st TSMC · 2nd Samsung · 3rd SK Hynix

- HBM share: 50% (dominant #1) · Nvidia main supply

- Micron +20% co-rally: Memory cycle signal

- 2026E op. income: 55T KRW (all-time high) · 46% margin

- 12M scenarios: Bull \$2T / Base \$1.5T / Bear \$0.7T

- Risks: Cycle peak + China + Nvidia dependency

- Maintenance: HBM 50%+ + Op. margin 40%+ + Nvidia adoption

- Strategy: Phased + memory 25% cap + 20% cash

🔗 [This] SK Hynix \$1T Club Entry — Asia’s 3rd 5 Analyses and Strategies

🔗 [Related] Micron +20% Surge — UBS Triple Upgrade 5 Analyses

🔗 [Related] KOSPI 8228 Record High — Peak vs Upside (Planned)

🔗 [Related] Sam Altman ‘AI Jobs Apocalypse X’ Sydney Confession

🔗 [Related] MakinaRocks 477850 Stock Outlook 5/27

🔗 [Next] \$2T Entry Scenarios + HBM4 Mass-Prod D-Day (Planned)

#SKHynix

#000660

#1Trillion

#TrillionClub

#SKHynixStock

#HBM

#HBM3E

#HBM4

#Nvidia

#Micron

#SamsungElectronics

#005930

#DRAM

#MemoryStocks

#KoreaSemi

#TIGERFnSemi

#KODEXSemi

#HanmiSemi

#042700

#AIHBM

#Asia1Trillion

#TSMC

#KOSPIRecordHigh

#KOSPI8228

#MemoryCycle

#getdirRealTime

#getdirSKHynix

#jyfamilyoffice

#2026Semi

#KoreaMemory