Jusung Engineering Surges 60% in a Week — ALG Equipment, PER 241x Concerns

Real-Time Issue · May 24, 2026

Jusung Engineering Surges 60% in a Week — ALG Equipment, PER 241x Concerns

KOSDAQ semiconductor leader / 10T cap / World-first ALG equipment / Financials / PER 241x / 5 strategies

What Is Jusung Engineering

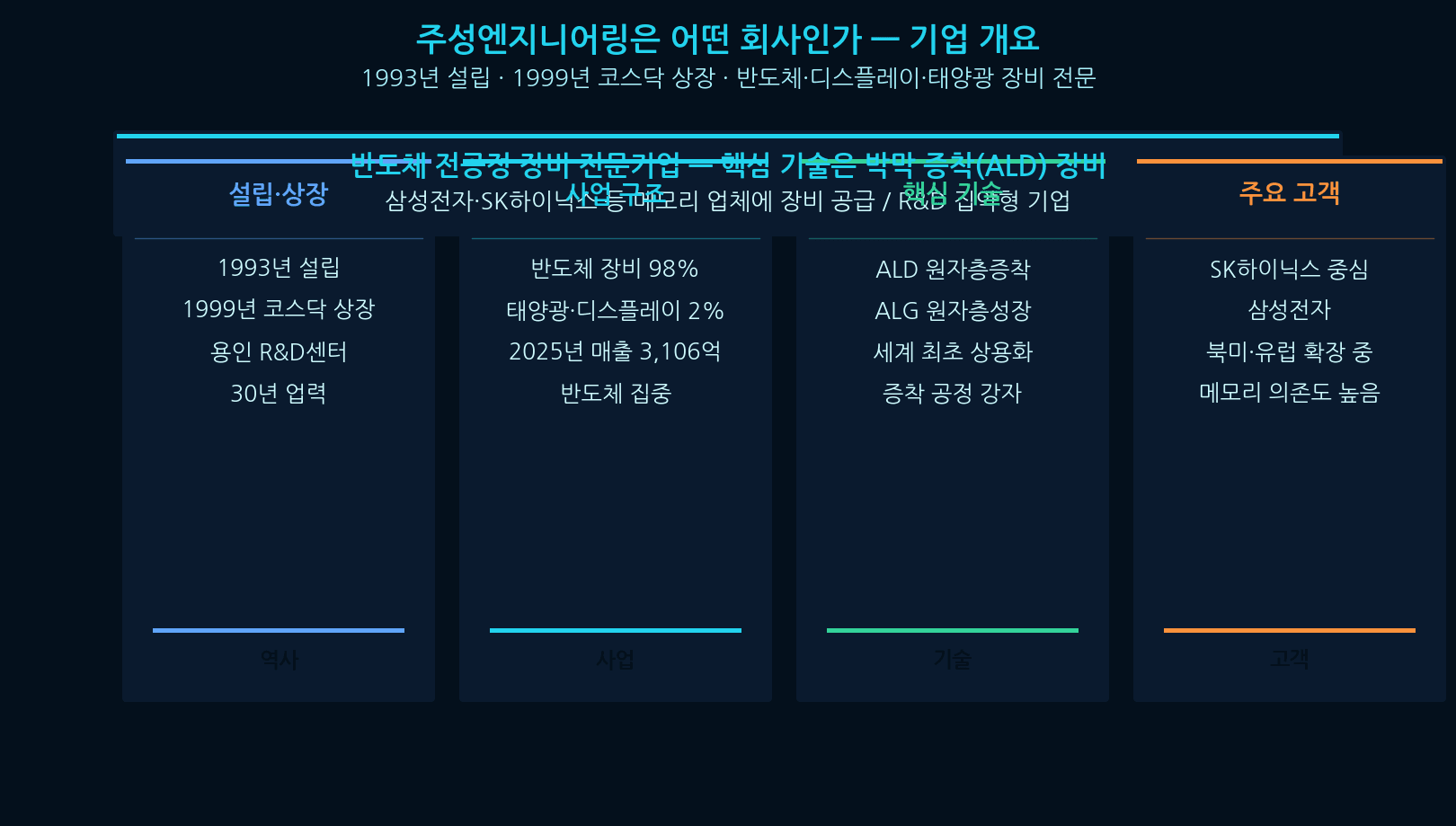

Jusung Engineering, founded in 1993 and listed on KOSDAQ in 1999 (ticker 036930), is a specialist front-end semiconductor equipment maker headquartered in Yongin, Korea. For over 30 years, Jusung Engineering has developed equipment for semiconductor, display, and solar manufacturing. Its core technology is thin-film deposition — particularly ALD (atomic layer deposition) equipment that coats wafers with target materials. In 2025, 98% of revenue came from the semiconductor segment.

Jusung Engineering 60% Weekly Surge — What Happened

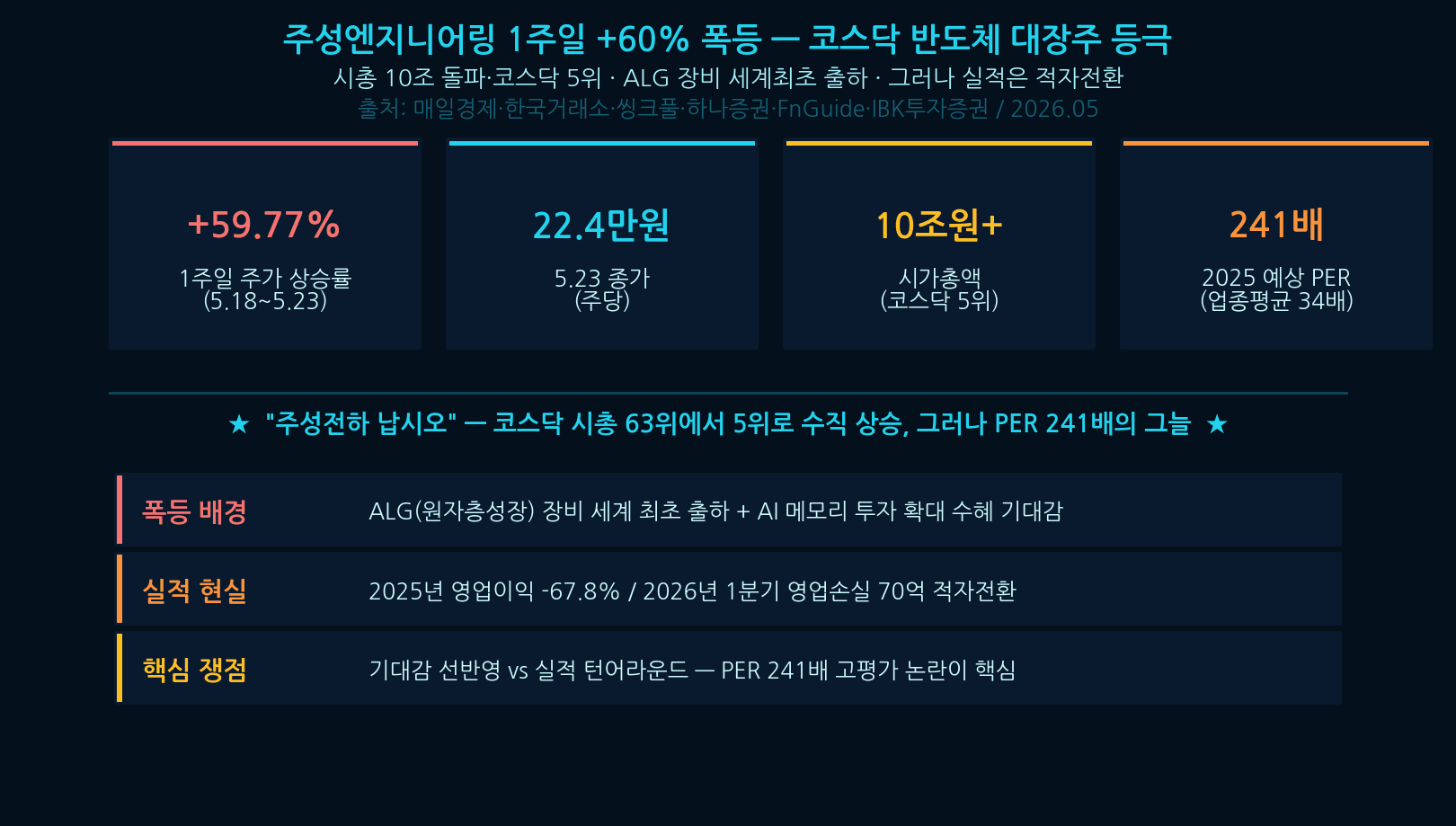

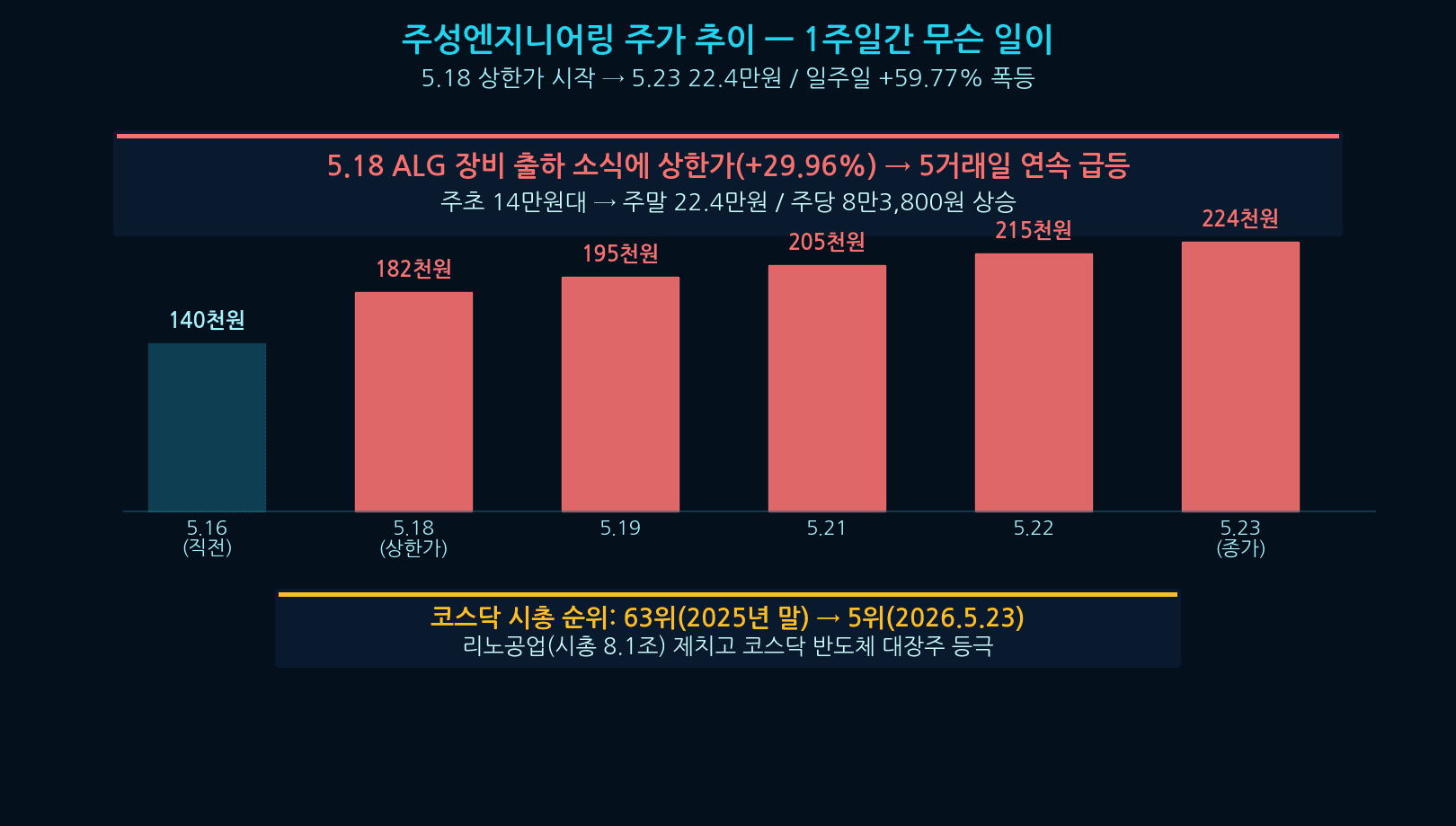

In just 5 trading sessions from May 18 to 23, 2026, Jusung Engineering surged 59.77%. The stock opened the week near 140,000 KRW and closed at 224,000 — a gain of 83,800 per share. The catalyst was the May 18 ALG equipment shipment announcement, which triggered an upper-limit close of +29.96%. KOSDAQ market cap ranking jumped from 63rd at end-2025 to 5th, overtaking Leeno Industrial (8T cap) to become the new KOSDAQ semiconductor leader.

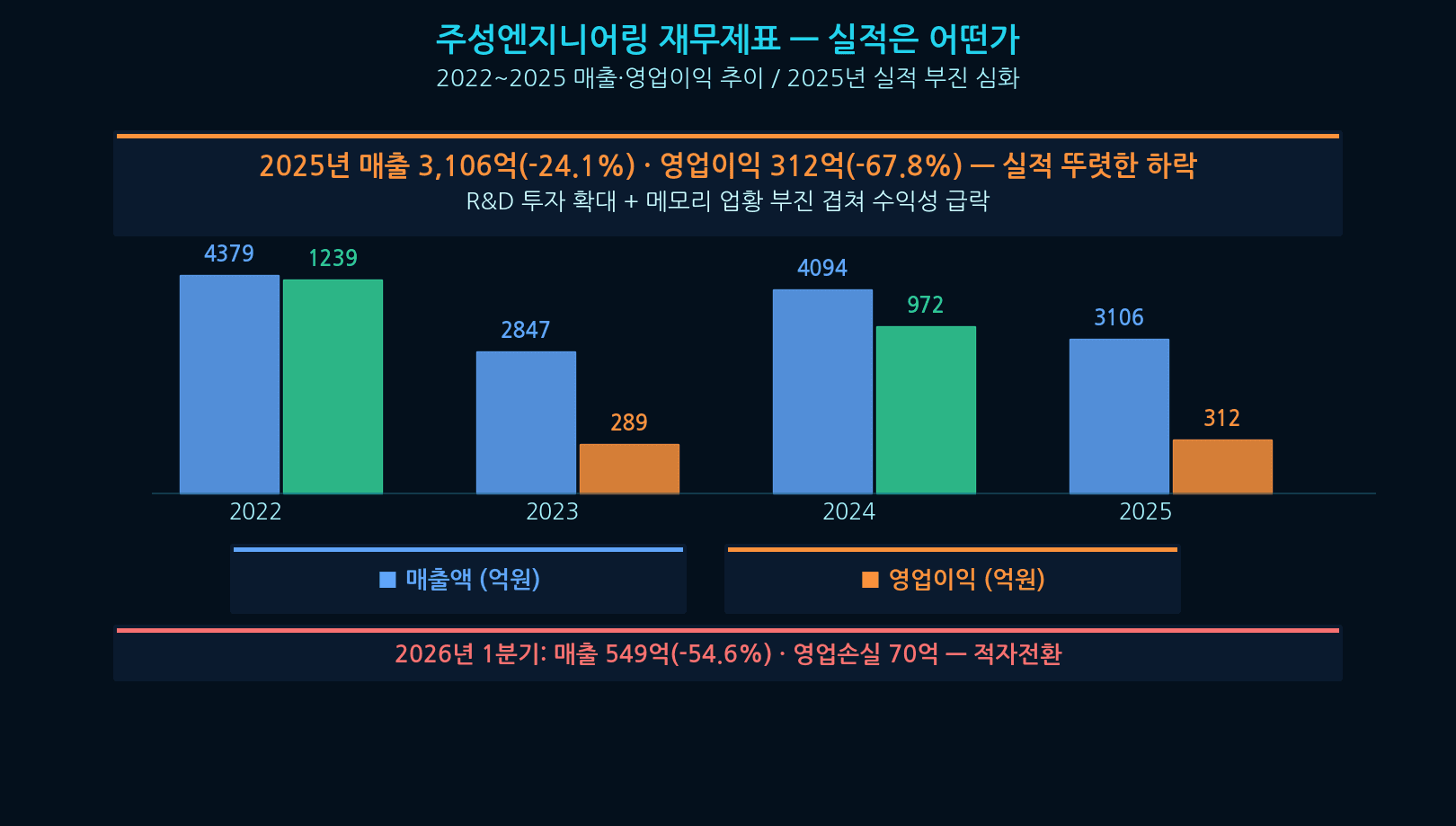

Jusung Engineering Financials — What the Numbers Show

While Jusung Engineering’s stock surged, financial results moved the opposite way. 2025 revenue 310.6B KRW (-24.1% YoY), operating profit 31.2B (-67.8%), net income -66.6%. Q1 2026 was worse: revenue 54.9B (-54.6%), operating loss of 7B — a swing from a 33.9B profit in Q1 2025. The company attributes the weakness to elevated R&D investment in future growth drivers. The current stock price reflects future expectations, not current earnings.

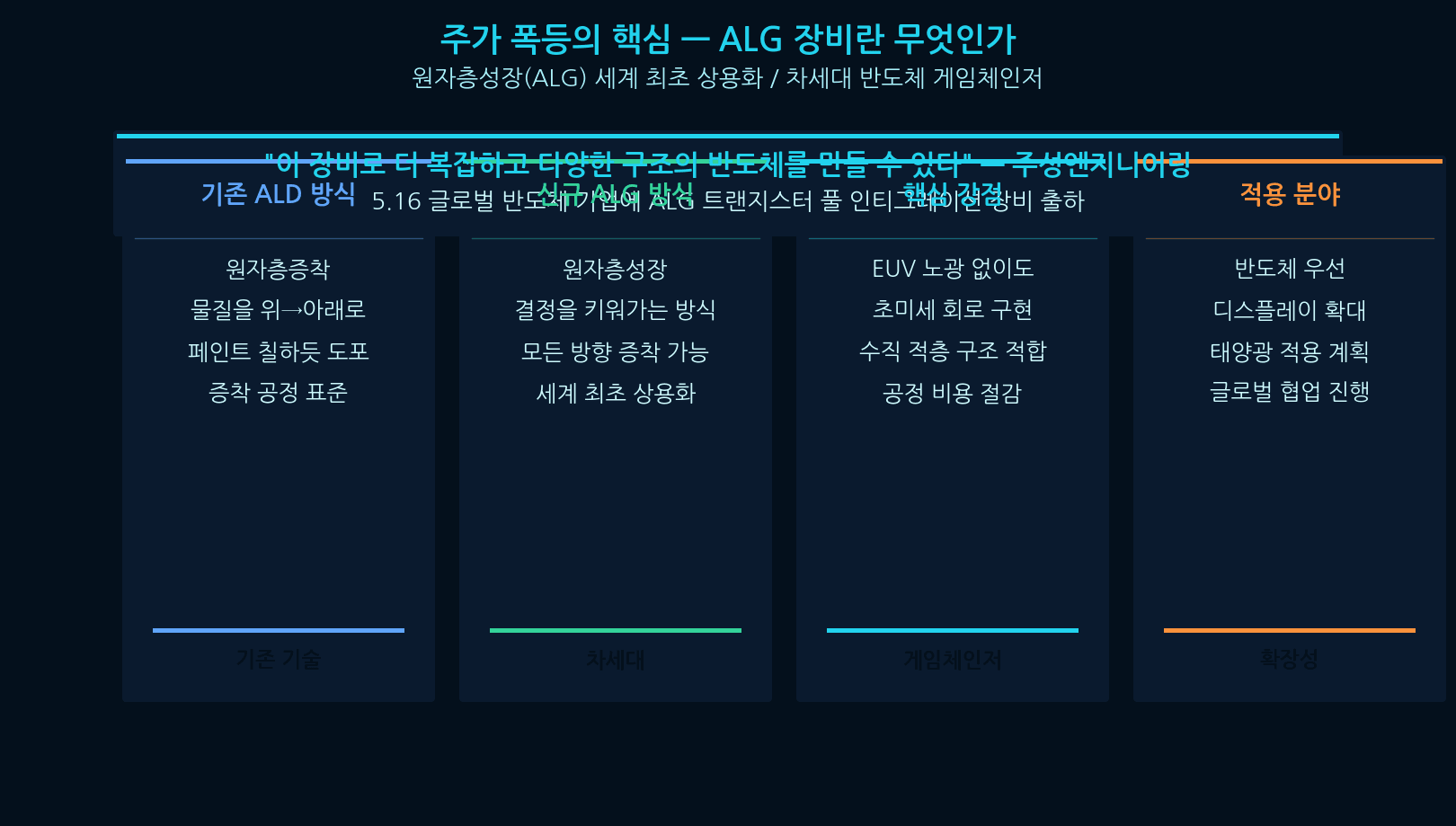

Jusung Engineering ALG Equipment — World’s First Commercialization

The Jusung Engineering ALG equipment was the catalyst for the surge. On May 16, the company announced shipment of its ALG (Atomic Layer Growth) transistor full-integration equipment to a global semiconductor customer. Where conventional ALD deposits material top-down, Jusung Engineering ALG grows crystals from the base. Multidirectional deposition makes it ideal for vertical stack structures, and it enables ultra-fine circuits without EUV lithography. It is viewed as a potential game-changer as semiconductor miniaturization hits physical limits.

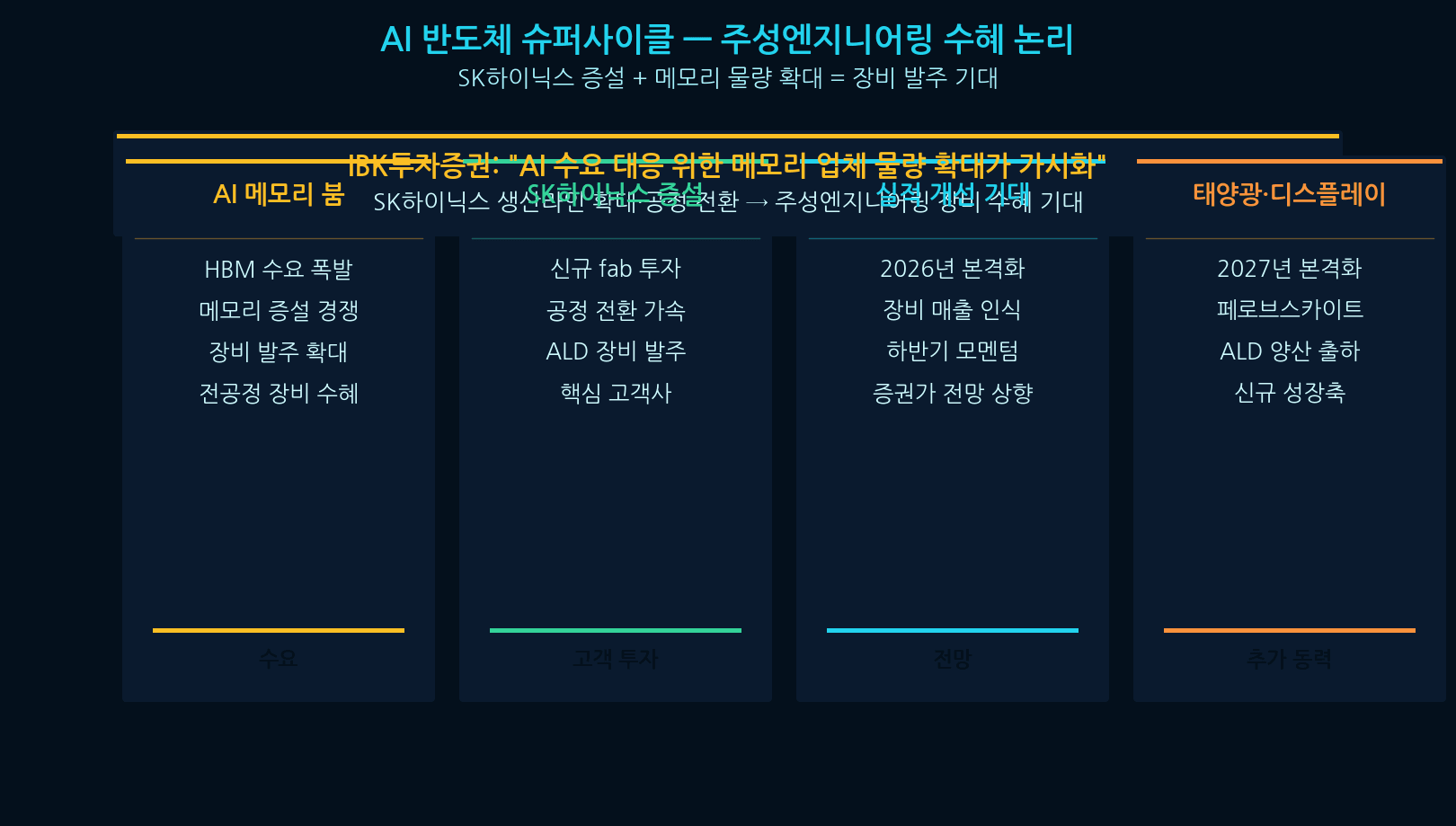

AI Semiconductor Supercycle Beneficiary Thesis

Beyond the ALG catalyst, the AI semiconductor supercycle is the second pillar supporting Jusung Engineering. IBK Investment Securities argues Jusung Engineering will benefit from rising AI-related memory capex. The thesis: memory makers are expanding capacity to meet AI demand, and SK Hynix’s production-line expansion and process transitions should drive larger Jusung Engineering equipment orders. Sell-side expects meaningful earnings recovery starting this year.

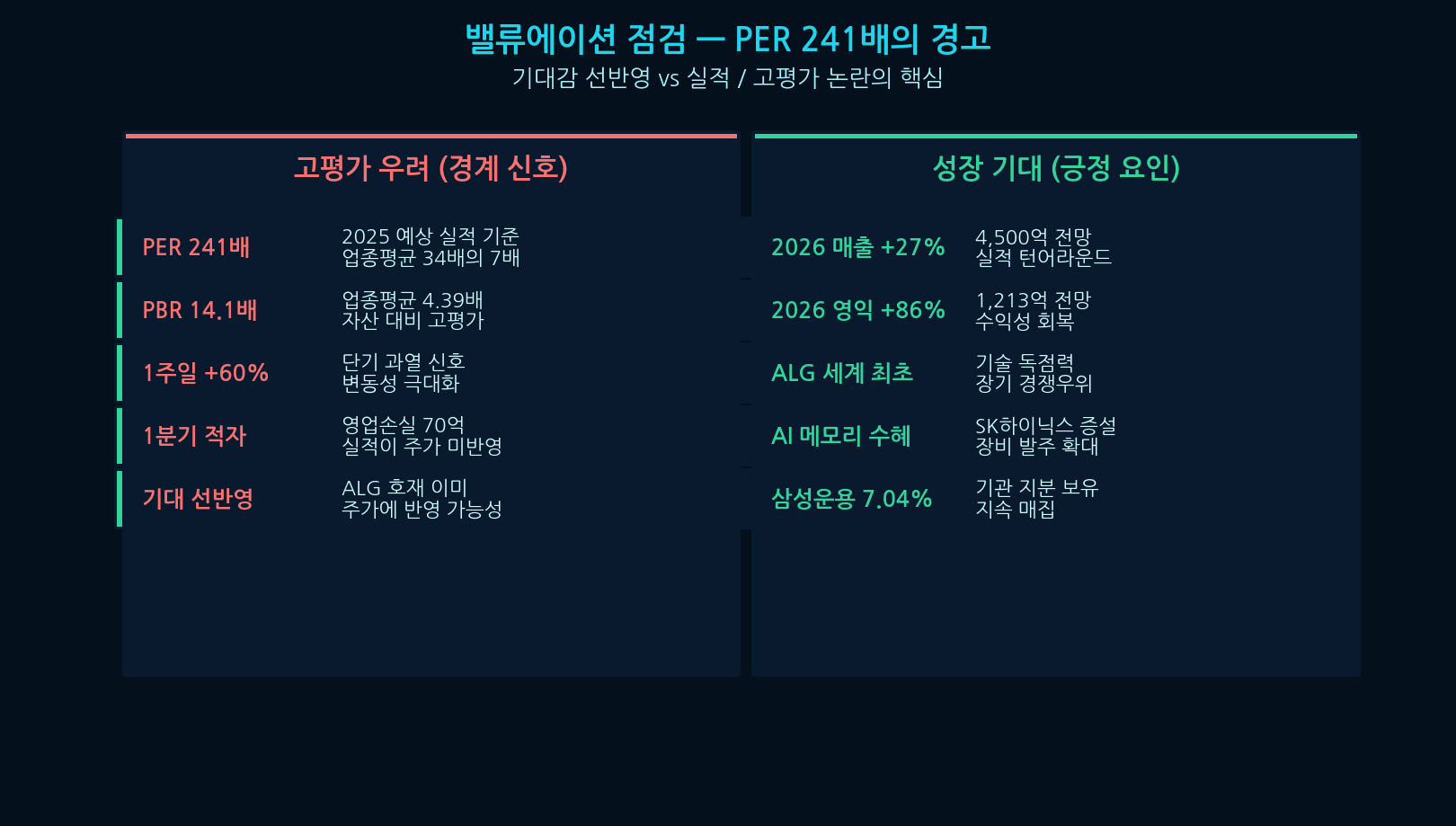

Jusung Engineering at 241x P/E — Valuation Warning

The crucial question: is the current price justified? Based on 2025 estimates, Jusung Engineering trades at a P/E of approximately 241x — 7x the 34x industry average. P/B at 14.1x also far exceeds the 4.39x peer average. The counter-argument: sell-side projects 2026 revenue of 450B KRW (+27%) and operating profit of 121.3B (+86%). If earnings turn around, the P/E compresses naturally. But if that assumption fails, downside risk of -30%+ is real.

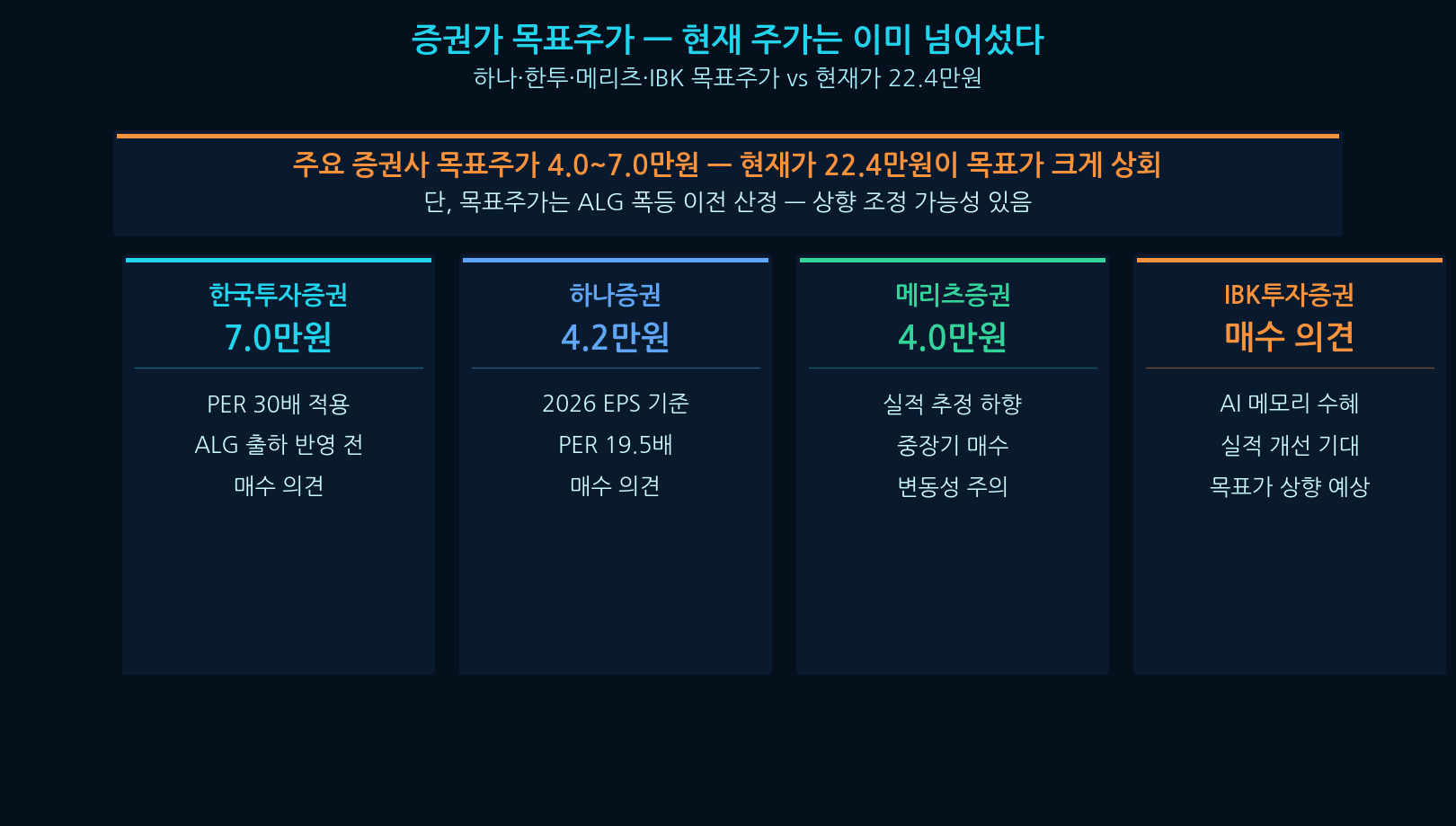

Jusung Engineering Target Price — Sell-Side Consensus

Sell-side target consensus on Jusung Engineering: Hana Securities raised to 280K, IBK 260K, FnGuide average ~250K. Versus the current 224K, that implies +12–25% additional upside. The targets assume Jusung Engineering achieves 121.3B operating profit in 2026 and that ALG revenue ramps meaningfully. On the downside, some analyses suggest a fair value range of 150–170K (based on a 50x 2025 P/E). The gap between the bull case and the fair-value floor is wide.

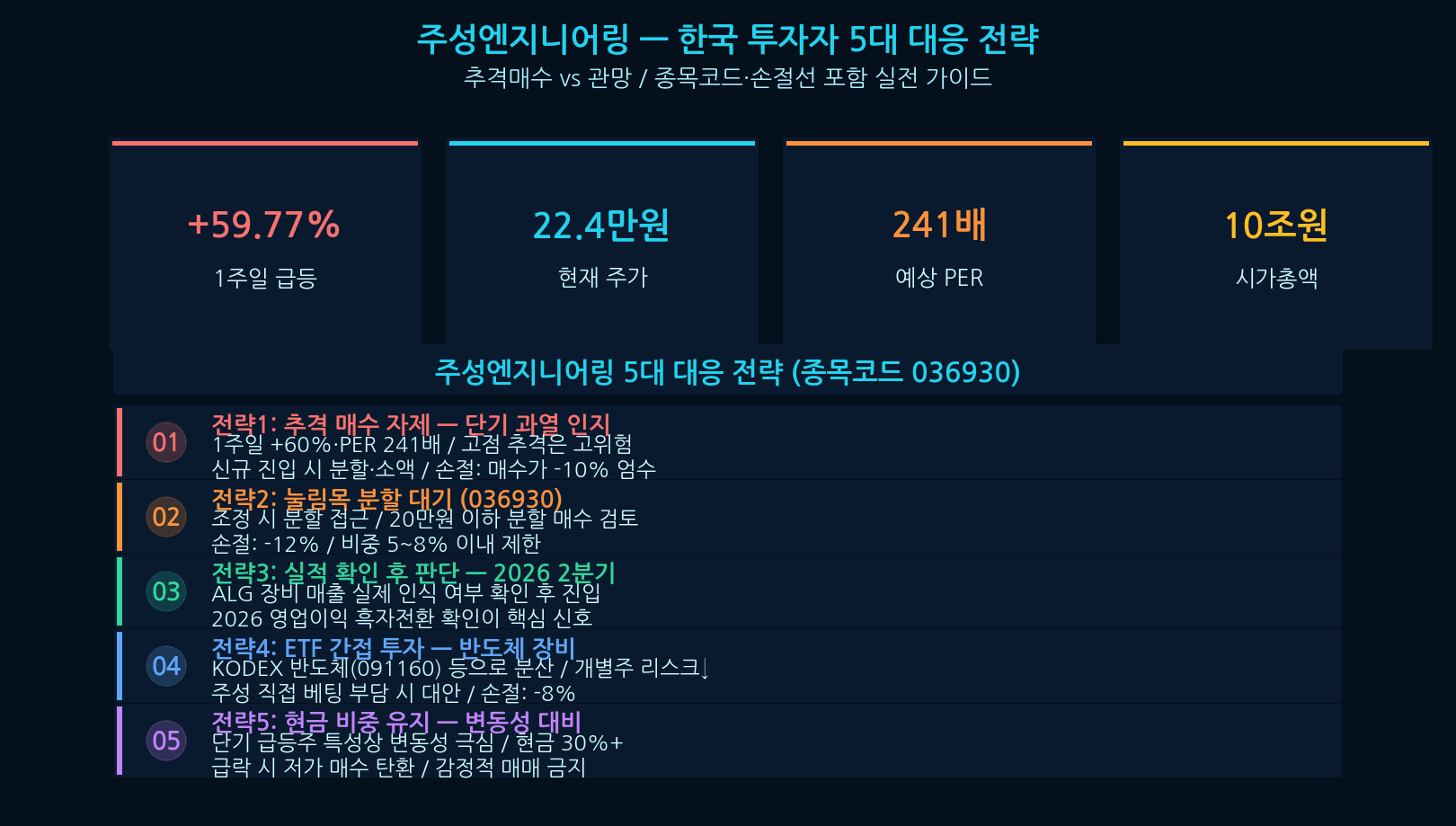

5 Strategies for Korean Investors — Jusung Engineering

Five strategies on Jusung Engineering. ① Direct buy — entering at 224K is chasing; wait for the 190K pullback, dollar-cost average, stop-loss -12%, weight 5%. ② Peer alternatives — Wonik IPS (240810) and other ALD competitors, stop-loss -10%, weight 5%. ③ SK Hynix (000660) — Jusung Engineering’s key customer, stable exposure, stop-loss -9%, weight 15%. ④ KODEX KOSDAQ 150 (229200) — thematic diversification, stop-loss -8%, weight 10%. ⑤ Cash 30% — volatility cushion plus entry reserve.

Conclusion — Jusung Engineering: Bubble or Future?

Jusung Engineering is a stock with two distinct faces. On the growth side, the world-first ALG commercialization and AI memory tailwind are real. But at this moment, a swing to losses and a 241x P/E represent clear burdens. Bottom line: no chasing, only dollar-cost averaging on pullbacks, with portfolio weight capped at 5%. Volatility likely persists until H2 2026 earnings clarity. Approaches should differ markedly between short-term traders and long-term investors.